Auckland International Airport: Financial Management Plan Report

VerifiedAdded on 2022/08/13

|29

|4059

|17

Report

AI Summary

This report provides a financial management plan for Auckland International Airport, analyzing its financial performance based on annual reports. The report includes an executive summary, stakeholder analysis (government and shareholders), and capital budgeting using NPV and IRR methods. It evaluates profitability ratios (net profit margin, operating profit margin, return on equity, return on assets) and efficiency ratios (asset turnover, inventory turnover, accounts payable turnover). The analysis covers risk and return, country risks, and the company's hedging strategies. The report also includes suggestions for improvements and concludes with an assessment of the airport's financial health and future prospects. The report finds that the company is committed to meeting the needs of its stakeholders and has increased revenue, despite some declines in profitability ratios. The company is also shown to be managing its operations effectively.

Running Head: FINANCIAL MANAGEMENT PLAN

Executive Summary

The purpose of the report is to do a financial management

plan of Auckland International Airport. The study is supported by

analysing the annual reports of the three financial year of the

company. It is found that Auckland airport is committed to

meeting the needs of the stakeholders and the shareholders of

the company. The business has increased its revenue in the

current financial year. The company is able to manage their

operations.

Executive Summary

The purpose of the report is to do a financial management

plan of Auckland International Airport. The study is supported by

analysing the annual reports of the three financial year of the

company. It is found that Auckland airport is committed to

meeting the needs of the stakeholders and the shareholders of

the company. The business has increased its revenue in the

current financial year. The company is able to manage their

operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL MANAGEMENT PLAN

Contents

Part A.........................................................................................................................................2

Part B..........................................................................................................................................3

Part C..........................................................................................................................................4

Part D.........................................................................................................................................5

Part E..........................................................................................................................................7

Part F..........................................................................................................................................8

Part G.........................................................................................................................................9

Part H.......................................................................................................................................13

Part I.........................................................................................................................................15

Part J.........................................................................................................................................16

References...........................................................................................................................19

Part A.........................................................................................................................................2

Part B..........................................................................................................................................3

Part C..........................................................................................................................................4

Part D.........................................................................................................................................5

Part E..........................................................................................................................................7

Part F..........................................................................................................................................7

Part G.........................................................................................................................................9

The company communication framework and structure designed in such a

way in order to ensure proper communication with shareholders and other

FINANCIAL MANAGEMENT PLAN

Contents

Part A.........................................................................................................................................2

Part B..........................................................................................................................................3

Part C..........................................................................................................................................4

Part D.........................................................................................................................................5

Part E..........................................................................................................................................7

Part F..........................................................................................................................................8

Part G.........................................................................................................................................9

Part H.......................................................................................................................................13

Part I.........................................................................................................................................15

Part J.........................................................................................................................................16

References...........................................................................................................................19

Part A.........................................................................................................................................2

Part B..........................................................................................................................................3

Part C..........................................................................................................................................4

Part D.........................................................................................................................................5

Part E..........................................................................................................................................7

Part F..........................................................................................................................................7

Part G.........................................................................................................................................9

The company communication framework and structure designed in such a

way in order to ensure proper communication with shareholders and other

2

FINANCIAL MANAGEMENT PLAN

stakeholders of the company properly managed.This strategy forms part

of the disclosure and communication policy.The company keep internal

stakeholder and shareholder informed and communicated through various

strategy involved namely:.............................................................................................12

Part H.......................................................................................................................................13

Part I.........................................................................................................................................15

Part J.........................................................................................................................................16

References...........................................................................................................................18

FINANCIAL MANAGEMENT PLAN

stakeholders of the company properly managed.This strategy forms part

of the disclosure and communication policy.The company keep internal

stakeholder and shareholder informed and communicated through various

strategy involved namely:.............................................................................................12

Part H.......................................................................................................................................13

Part I.........................................................................................................................................15

Part J.........................................................................................................................................16

References...........................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL MANAGEMENT PLAN

Part A

Auckland International airport is one of the largest

airportairports of New Zealand and Itand It is a service provider,

Thethe company is listed both in the New Zealand Stock Exchange.

Auckland airport is an aviation industry, which is located in the

Ray Emery Drive of Auckland. It handles around 71 per cent of the

international passengers. The number of flights operated by the

giant airport on an average is 420 per day with an annual

turnover of approximately 153,300. Auckland Airport is also the

busiest airport of New Zealand and has more than 21 Million

passengerpassengers catered to in 2019. The airport is the hub for the

aircraft Air New Zealand, Virgin Australia and Jetstar Airways. (Auckland

International Airport Ltd, 2020)

https://corporate.aucklandairport.co.nz/corporate-responsibility/

managing-aircraft-noise/understanding-aircraft-noise/auckland-flight-paths

The services provided by Auckland airport encompass the

following:

(a) Flight Information;

(b) Providing parking space for visitors and local cabs;

(c) Shopping and dining;

(d) Clubs;

FINANCIAL MANAGEMENT PLAN

Part A

Auckland International airport is one of the largest

airportairports of New Zealand and Itand It is a service provider,

Thethe company is listed both in the New Zealand Stock Exchange.

Auckland airport is an aviation industry, which is located in the

Ray Emery Drive of Auckland. It handles around 71 per cent of the

international passengers. The number of flights operated by the

giant airport on an average is 420 per day with an annual

turnover of approximately 153,300. Auckland Airport is also the

busiest airport of New Zealand and has more than 21 Million

passengerpassengers catered to in 2019. The airport is the hub for the

aircraft Air New Zealand, Virgin Australia and Jetstar Airways. (Auckland

International Airport Ltd, 2020)

https://corporate.aucklandairport.co.nz/corporate-responsibility/

managing-aircraft-noise/understanding-aircraft-noise/auckland-flight-paths

The services provided by Auckland airport encompass the

following:

(a) Flight Information;

(b) Providing parking space for visitors and local cabs;

(c) Shopping and dining;

(d) Clubs;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL MANAGEMENT PLAN

(e) Transportation (Auckland International Airport Ltd. , 2020)

https://www.aucklandairport.co.nz/information/terminal-services-and-

facilities

Part B

In any business organisation, there is an owner who invests fund

in the business of the company with an expectation to earn

sustainable returns over the investment horizon. These people in

the accounts of the company are considered as shareholders or

principal. On the other hand, for a company to operate efficiently,

it needs to be managed by a group of experts with diverse

knowledge and wisdom. These people who are managing the

affairs of the company on behalf of the owners/ principal are

considered as agent.

The relation between these two group are critical for the success

of the organisation and vision of the Auckland International

Airport to be the best in the field and catering to a large group

and section of the commuters. In the concerned case, the needs

of the principal isare to earn a steady return on the investment

made over the investment horizon. On the other hand, the agent

shall be required to manage the affairs of the company in a

manner that take care of both the shareholder and stakeholder.

Principal is shareholder of Auckland airport and the agent is the

board of directors and discuss the relationship.

FINANCIAL MANAGEMENT PLAN

(e) Transportation (Auckland International Airport Ltd. , 2020)

https://www.aucklandairport.co.nz/information/terminal-services-and-

facilities

Part B

In any business organisation, there is an owner who invests fund

in the business of the company with an expectation to earn

sustainable returns over the investment horizon. These people in

the accounts of the company are considered as shareholders or

principal. On the other hand, for a company to operate efficiently,

it needs to be managed by a group of experts with diverse

knowledge and wisdom. These people who are managing the

affairs of the company on behalf of the owners/ principal are

considered as agent.

The relation between these two group are critical for the success

of the organisation and vision of the Auckland International

Airport to be the best in the field and catering to a large group

and section of the commuters. In the concerned case, the needs

of the principal isare to earn a steady return on the investment

made over the investment horizon. On the other hand, the agent

shall be required to manage the affairs of the company in a

manner that take care of both the shareholder and stakeholder.

Principal is shareholder of Auckland airport and the agent is the

board of directors and discuss the relationship.

5

FINANCIAL MANAGEMENT PLAN

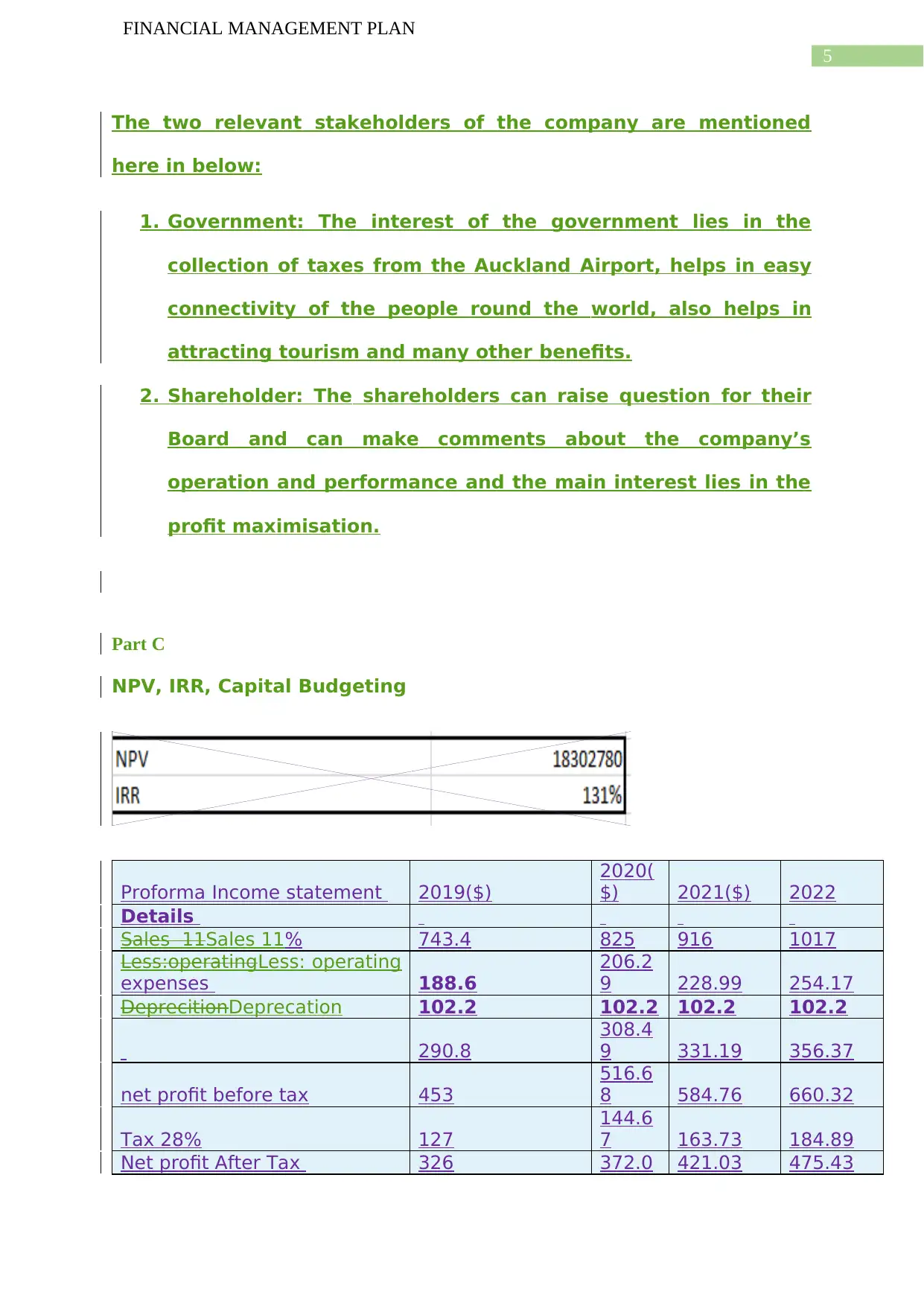

The two relevant stakeholders of the company are mentioned

here in below:

1. Government: The interest of the government lies in the

collection of taxes from the Auckland Airport, helps in easy

connectivity of the people round the world, also helps in

attracting tourism and many other benefits.

2. Shareholder: The shareholders can raise question for their

Board and can make comments about the company’s

operation and performance and the main interest lies in the

profit maximisation.

Part C

NPV, IRR, Capital Budgeting

Proforma Income statement 2019($)

2020(

$) 2021($) 2022

Details

Sales 11Sales 11% 743.4 825 916 1017

Less:operatingLess: operating

expenses 188.6

206.2

9 228.99 254.17

DeprecitionDeprecation 102.2 102.2 102.2 102.2

290.8

308.4

9 331.19 356.37

net profit before tax 453

516.6

8 584.76 660.32

Tax 28% 127

144.6

7 163.73 184.89

Net profit After Tax 326 372.0 421.03 475.43

FINANCIAL MANAGEMENT PLAN

The two relevant stakeholders of the company are mentioned

here in below:

1. Government: The interest of the government lies in the

collection of taxes from the Auckland Airport, helps in easy

connectivity of the people round the world, also helps in

attracting tourism and many other benefits.

2. Shareholder: The shareholders can raise question for their

Board and can make comments about the company’s

operation and performance and the main interest lies in the

profit maximisation.

Part C

NPV, IRR, Capital Budgeting

Proforma Income statement 2019($)

2020(

$) 2021($) 2022

Details

Sales 11Sales 11% 743.4 825 916 1017

Less:operatingLess: operating

expenses 188.6

206.2

9 228.99 254.17

DeprecitionDeprecation 102.2 102.2 102.2 102.2

290.8

308.4

9 331.19 356.37

net profit before tax 453

516.6

8 584.76 660.32

Tax 28% 127

144.6

7 163.73 184.89

Net profit After Tax 326 372.0 421.03 475.43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL MANAGEMENT PLAN

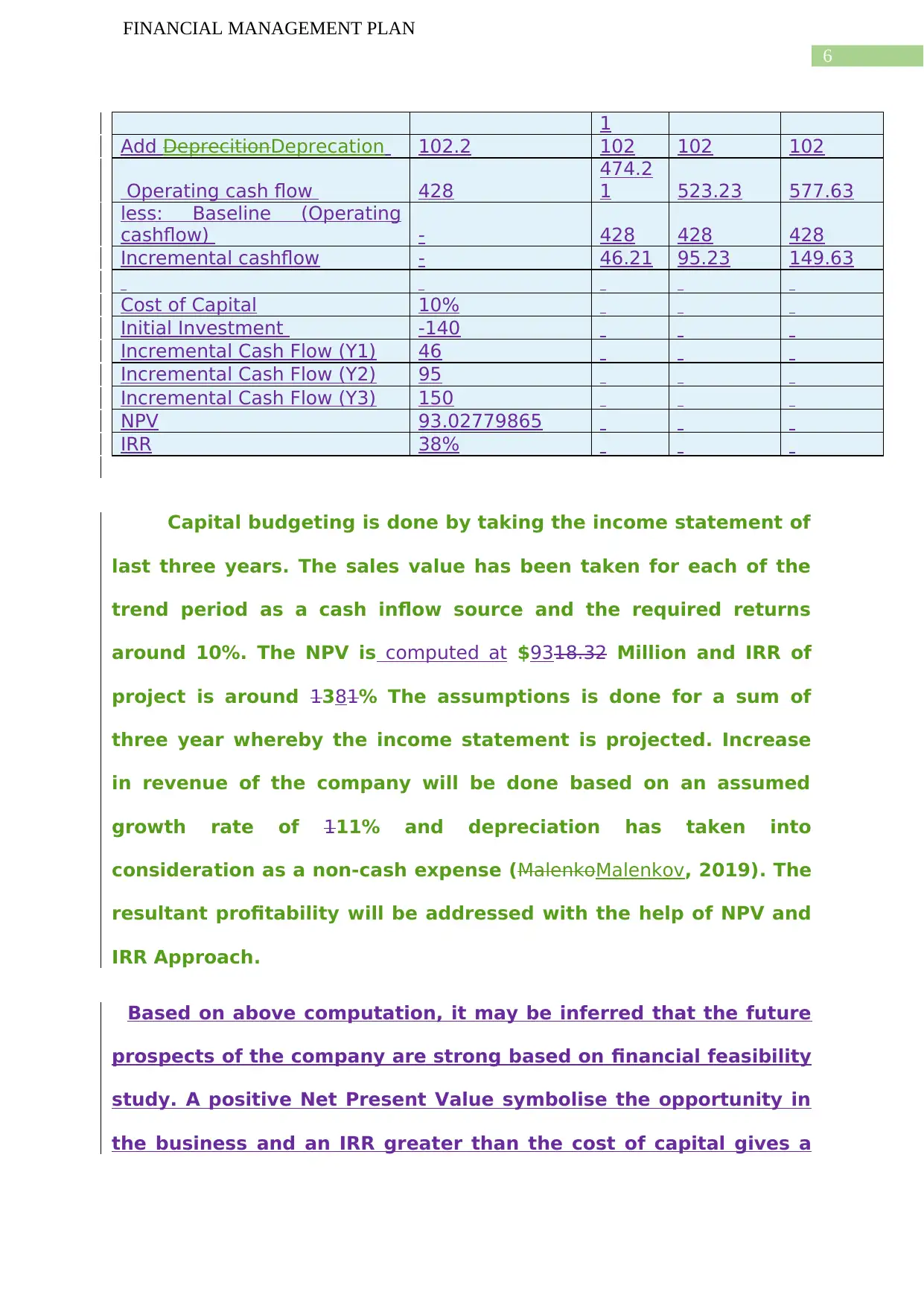

1

Add DeprecitionDeprecation 102.2 102 102 102

Operating cash flow 428

474.2

1 523.23 577.63

less: Baseline (Operating

cashflow) - 428 428 428

Incremental cashflow - 46.21 95.23 149.63

Cost of Capital 10%

Initial Investment -140

Incremental Cash Flow (Y1) 46

Incremental Cash Flow (Y2) 95

Incremental Cash Flow (Y3) 150

NPV 93.02779865

IRR 38%

Capital budgeting is done by taking the income statement of

last three years. The sales value has been taken for each of the

trend period as a cash inflow source and the required returns

around 10%. The NPV is computed at $9318.32 Million and IRR of

project is around 1381% The assumptions is done for a sum of

three year whereby the income statement is projected. Increase

in revenue of the company will be done based on an assumed

growth rate of 111% and depreciation has taken into

consideration as a non-cash expense (MalenkoMalenkov, 2019). The

resultant profitability will be addressed with the help of NPV and

IRR Approach.

Based on above computation, it may be inferred that the future

prospects of the company are strong based on financial feasibility

study. A positive Net Present Value symbolise the opportunity in

the business and an IRR greater than the cost of capital gives a

FINANCIAL MANAGEMENT PLAN

1

Add DeprecitionDeprecation 102.2 102 102 102

Operating cash flow 428

474.2

1 523.23 577.63

less: Baseline (Operating

cashflow) - 428 428 428

Incremental cashflow - 46.21 95.23 149.63

Cost of Capital 10%

Initial Investment -140

Incremental Cash Flow (Y1) 46

Incremental Cash Flow (Y2) 95

Incremental Cash Flow (Y3) 150

NPV 93.02779865

IRR 38%

Capital budgeting is done by taking the income statement of

last three years. The sales value has been taken for each of the

trend period as a cash inflow source and the required returns

around 10%. The NPV is computed at $9318.32 Million and IRR of

project is around 1381% The assumptions is done for a sum of

three year whereby the income statement is projected. Increase

in revenue of the company will be done based on an assumed

growth rate of 111% and depreciation has taken into

consideration as a non-cash expense (MalenkoMalenkov, 2019). The

resultant profitability will be addressed with the help of NPV and

IRR Approach.

Based on above computation, it may be inferred that the future

prospects of the company are strong based on financial feasibility

study. A positive Net Present Value symbolise the opportunity in

the business and an IRR greater than the cost of capital gives a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL MANAGEMENT PLAN

green signal to further investment in the project. In the current

case, since the IRR and NPV of the project are good, investment

in Auckland International Airport from an investor point of view is

a good opportunity.

Suggestion: Based on above deliberation it may be inferred that

investment in Auckland International Airport is a feasible option

Part D

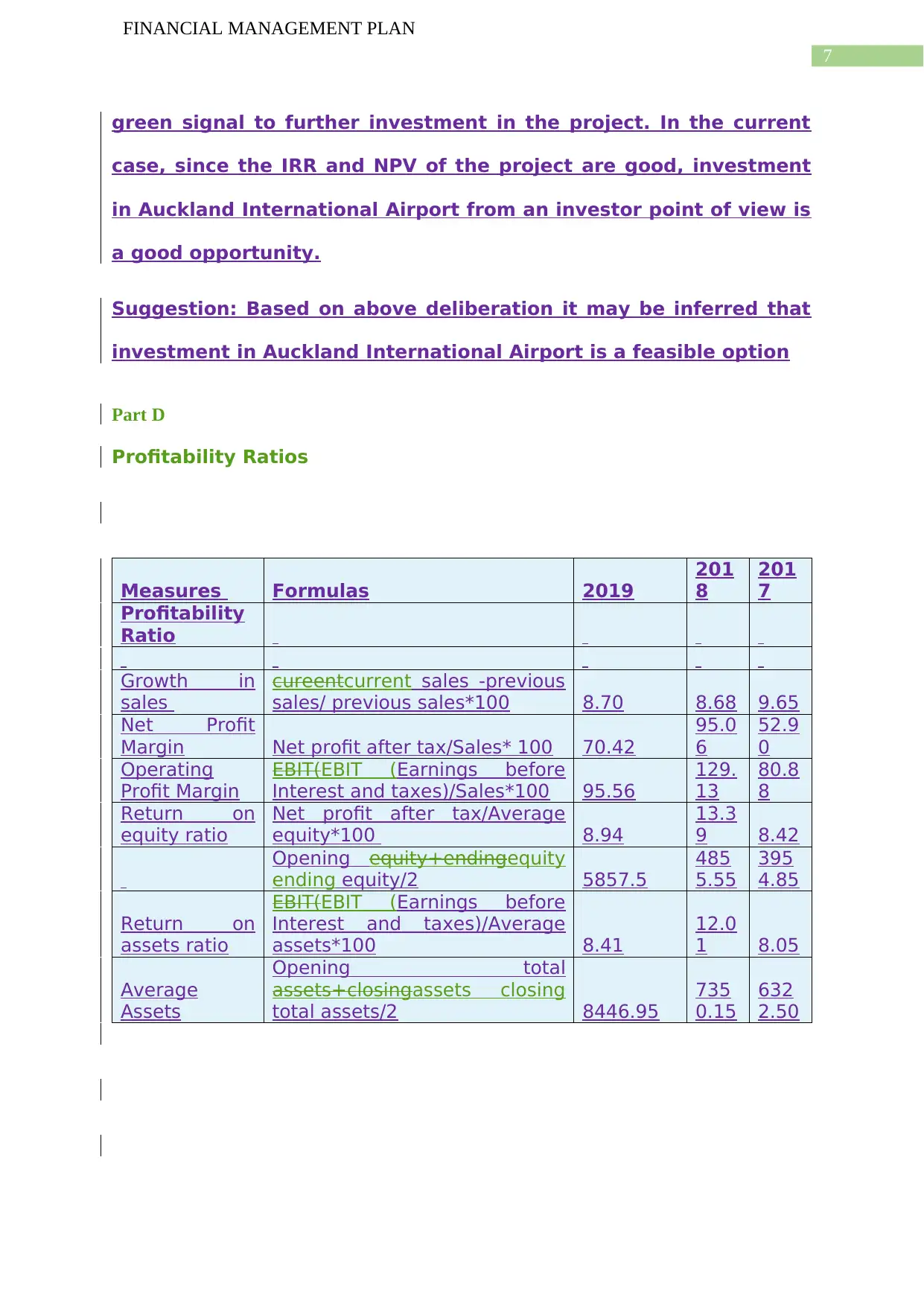

Profitability Ratios

Measures Formulas 2019

201

8

201

7

Profitability

Ratio

Growth in

sales

cureentcurrent sales -previous

sales/ previous sales*100 8.70 8.68 9.65

Net Profit

Margin Net profit after tax/Sales* 100 70.42

95.0

6

52.9

0

Operating

Profit Margin

EBIT(EBIT (Earnings before

Interest and taxes)/Sales*100 95.56

129.

13

80.8

8

Return on

equity ratio

Net profit after tax/Average

equity*100 8.94

13.3

9 8.42

Opening equity+endingequity

ending equity/2 5857.5

485

5.55

395

4.85

Return on

assets ratio

EBIT(EBIT (Earnings before

Interest and taxes)/Average

assets*100 8.41

12.0

1 8.05

Average

Assets

Opening total

assets+closingassets closing

total assets/2 8446.95

735

0.15

632

2.50

FINANCIAL MANAGEMENT PLAN

green signal to further investment in the project. In the current

case, since the IRR and NPV of the project are good, investment

in Auckland International Airport from an investor point of view is

a good opportunity.

Suggestion: Based on above deliberation it may be inferred that

investment in Auckland International Airport is a feasible option

Part D

Profitability Ratios

Measures Formulas 2019

201

8

201

7

Profitability

Ratio

Growth in

sales

cureentcurrent sales -previous

sales/ previous sales*100 8.70 8.68 9.65

Net Profit

Margin Net profit after tax/Sales* 100 70.42

95.0

6

52.9

0

Operating

Profit Margin

EBIT(EBIT (Earnings before

Interest and taxes)/Sales*100 95.56

129.

13

80.8

8

Return on

equity ratio

Net profit after tax/Average

equity*100 8.94

13.3

9 8.42

Opening equity+endingequity

ending equity/2 5857.5

485

5.55

395

4.85

Return on

assets ratio

EBIT(EBIT (Earnings before

Interest and taxes)/Average

assets*100 8.41

12.0

1 8.05

Average

Assets

Opening total

assets+closingassets closing

total assets/2 8446.95

735

0.15

632

2.50

8

FINANCIAL MANAGEMENT PLAN

Trend-

Net profit margin of the company has decreased from 95.06 to

70.42 on account of increase in direct and indirect expenditure of

the company without a parallel increase in the revenue of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

improvement compared to 2017. The formula for computation of

net profit margin is described as under:

(Revenue- direct and indirect cost) / Revenue

Operating profit margin of the company has decreased from

129.13 to 95.56 on account of increase in operating expenditure

of the company without a parallel increase in the revenue of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

improvement compared to 2017. The formula for computation of

operating profit margin is described as under:

(Revenue-operating expenditure) / Revenue

Return on Equity of the company has decreased from 13.39 to

8.94 on account of increase in direct and indirect expenditure of

the company with a parallel increase in the equity of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

FINANCIAL MANAGEMENT PLAN

Trend-

Net profit margin of the company has decreased from 95.06 to

70.42 on account of increase in direct and indirect expenditure of

the company without a parallel increase in the revenue of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

improvement compared to 2017. The formula for computation of

net profit margin is described as under:

(Revenue- direct and indirect cost) / Revenue

Operating profit margin of the company has decreased from

129.13 to 95.56 on account of increase in operating expenditure

of the company without a parallel increase in the revenue of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

improvement compared to 2017. The formula for computation of

operating profit margin is described as under:

(Revenue-operating expenditure) / Revenue

Return on Equity of the company has decreased from 13.39 to

8.94 on account of increase in direct and indirect expenditure of

the company with a parallel increase in the equity of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL MANAGEMENT PLAN

improvement compared to 2017. The formula for computation of

return on equity is described as under:

Net Profit Margin / Avg. Equity

Return on Assets of the company has decreased from 12.01 to

8.41 on account of increase in direct and indirect expenditure of

the company with a parallel increase in the assets of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

improvement compared to 2017. The formula for computation of

return on assets is described as under:

EBIT / Avg. Assets

Interpretation- The overall profitability ratios has been decreased

as compared to past years by a significant margin on account of

increase in both direct and indirect cost of the company. This indicates

that, the business has not generated enough revenue inrevenue in

the current year..year. It has done investments in the Queensland

airport (Laitinen, & Laitinen, 2018). However, when compared with

the 2017, a good return has been observed so one may also consider that

2018 was a one offone-off spin. Further, the airport has been generating

constant growth and returns over the periodThe company is unable to

manage its assets.

FINANCIAL MANAGEMENT PLAN

improvement compared to 2017. The formula for computation of

return on equity is described as under:

Net Profit Margin / Avg. Equity

Return on Assets of the company has decreased from 12.01 to

8.41 on account of increase in direct and indirect expenditure of

the company with a parallel increase in the assets of the

company. Accordingly, the Airport has witnessed a downward

trend in margin from last year. However, there has been an

improvement compared to 2017. The formula for computation of

return on assets is described as under:

EBIT / Avg. Assets

Interpretation- The overall profitability ratios has been decreased

as compared to past years by a significant margin on account of

increase in both direct and indirect cost of the company. This indicates

that, the business has not generated enough revenue inrevenue in

the current year..year. It has done investments in the Queensland

airport (Laitinen, & Laitinen, 2018). However, when compared with

the 2017, a good return has been observed so one may also consider that

2018 was a one offone-off spin. Further, the airport has been generating

constant growth and returns over the periodThe company is unable to

manage its assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL MANAGEMENT PLAN

Suggestions- Auckland International airport should continue

doing investments for increasing the business profitability and

properly manage their assets.

EfficiencySolvency Ratios

Trend-

Total Assets Turnover Ratio - There has been a decline in the ratio

from 0.4 to 0.3. This reflects an increase in the average total

assets or more specifically the assets at the end of the closing

period, thereby, signifying an increased investment in the assets

by the concern. Also, it may be observed sales has increased but

the relative increase of sales is lower compared to assets.

Further, the increase in assets has been mostly on account of

investments in fixed assets made by airport.

Fixed Assets Turnover Ratio - There has been a decline in the

ratio from 0.3 to 0.2. This reflects an increase in the average total

fixed assets or more specifically the fixed assets at the end of the

closing period, thereby, signifying an increased investment in the

assets by the concern. Also, it may be observed sales has

increased but the relative increase of sales is lower compared to

FINANCIAL MANAGEMENT PLAN

Suggestions- Auckland International airport should continue

doing investments for increasing the business profitability and

properly manage their assets.

EfficiencySolvency Ratios

Trend-

Total Assets Turnover Ratio - There has been a decline in the ratio

from 0.4 to 0.3. This reflects an increase in the average total

assets or more specifically the assets at the end of the closing

period, thereby, signifying an increased investment in the assets

by the concern. Also, it may be observed sales has increased but

the relative increase of sales is lower compared to assets.

Further, the increase in assets has been mostly on account of

investments in fixed assets made by airport.

Fixed Assets Turnover Ratio - There has been a decline in the

ratio from 0.3 to 0.2. This reflects an increase in the average total

fixed assets or more specifically the fixed assets at the end of the

closing period, thereby, signifying an increased investment in the

assets by the concern. Also, it may be observed sales has

increased but the relative increase of sales is lower compared to

11

FINANCIAL MANAGEMENT PLAN

assets. Further, the increase in assets has been mostly on

account of investments in fixed assets made by airport.

Inventory Turnover Ratio - The significant increase in this ratio is

an evidence of better working capital management on the part of

the company. The ratio has increased on account of higher

increase in sales volume compared to increase in inventory.

Trade Receivable Turnover Ratio – Overall, there has been an

improvement in the ratio which shows that less funds are getting

blocked with debtors while the sales levels are rising which

augurs well for the business.

Age of Trade Receivables Ratio – The ratio is reflecting an

downward trend compared to last year, thereby, indicating a

decrease in the credit period of debtors. This indicates a

stringent credit policy has been adopted. Further, when

compared to 2017, the aging has increased.

Accounts Payable Turnover Ratio – Overall, there has been an

increase in the ratio which shows that average creditors with

respect to level of sales is on a decline indicating that the

business is able to maintain a low level of creditors with increase

in sales.

Age of creditors Turnover Ratio - This ratio is also reflecting a

downward trend, thereby, indicating a decrease in the credit

FINANCIAL MANAGEMENT PLAN

assets. Further, the increase in assets has been mostly on

account of investments in fixed assets made by airport.

Inventory Turnover Ratio - The significant increase in this ratio is

an evidence of better working capital management on the part of

the company. The ratio has increased on account of higher

increase in sales volume compared to increase in inventory.

Trade Receivable Turnover Ratio – Overall, there has been an

improvement in the ratio which shows that less funds are getting

blocked with debtors while the sales levels are rising which

augurs well for the business.

Age of Trade Receivables Ratio – The ratio is reflecting an

downward trend compared to last year, thereby, indicating a

decrease in the credit period of debtors. This indicates a

stringent credit policy has been adopted. Further, when

compared to 2017, the aging has increased.

Accounts Payable Turnover Ratio – Overall, there has been an

increase in the ratio which shows that average creditors with

respect to level of sales is on a decline indicating that the

business is able to maintain a low level of creditors with increase

in sales.

Age of creditors Turnover Ratio - This ratio is also reflecting a

downward trend, thereby, indicating a decrease in the credit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.