Accounting Information System Audit: Revenue Cycle & Weakness

VerifiedAdded on 2023/06/16

|7

|847

|469

Homework Assignment

AI Summary

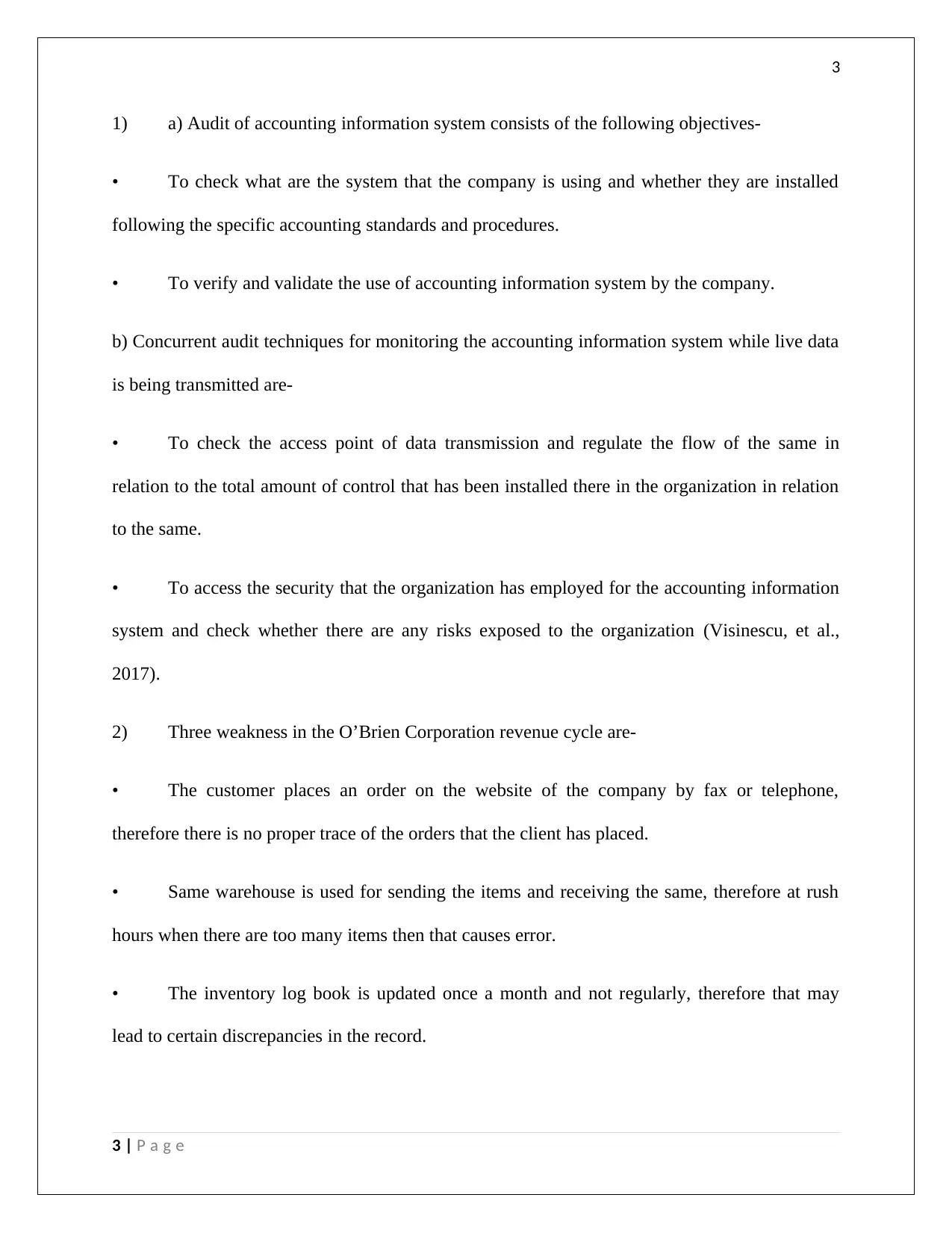

This assignment solution covers key aspects of accounting information systems, including auditing objectives, concurrent audit techniques, and weaknesses in the revenue cycle of O'Brien Corporation. It addresses issues such as order tracing, warehouse management, and inventory log maintenance, proposing improvements for each. The document also discusses the expenditure cycle's relationship to the revenue cycle, general threat elements, and controls. Furthermore, it delves into product design aims, threats, and the role of Product Lifecycle Management (PLM) software in product development. The solution provides a comprehensive overview of these topics with relevant references and is available on Desklib, a platform offering study tools and resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.