Audit Planning and Analysis of Seven Accounts: A Comprehensive Report

VerifiedAdded on 2020/03/07

|10

|2122

|96

Report

AI Summary

This report provides a comprehensive audit planning and analysis of seven key accounts for Fulvous Enterprises. It begins with an overview of audit planning, including analytical review and preliminary judgment of materiality. The report then delves into a detailed examination of each account: bank loan, interest income, miscellaneous expenses, accounts receivable, interest expense, inventory, and depreciation. For each account, the rationale for selection, assertions made by the auditor, and recommended audit procedures are presented. The analysis includes a review of the company's financial statements, focusing on areas of potential risk and the need for specific audit steps. The report also references relevant accounting standards and provides supporting financial statements in the appendix, offering a practical guide to audit procedures and financial statement analysis. This student assignment is designed to provide a practical understanding of audit processes and the analysis of key financial statement components.

AUDIT PLANNING AND ANALYSIS OF SEVEN ACCOUNTS

Student Name: Student ID:

9/25/2017

Student Name: Student ID:

9/25/2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

AUDIT PLANNING........................................................................................................................................4

ANALYTICAL REVIEW...............................................................................................................................4

PRELIMINARY JUDGMENT OF MATERIALITY............................................................................................4

BANK LOAN ACCOUNT.................................................................................................................................4

RATIONALE FOR SELECTION....................................................................................................................4

ASSERTION AND EXPLANATION...............................................................................................................4

RECOMMENDED AUDIT PROCEDURE......................................................................................................4

INTEREST INCOME.......................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................5

RECOMMENDED AUDIT PROCEDURE......................................................................................................5

MISCELLANEOUS.........................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................5

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

ACCOUNTS RECEIVABLE..............................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

INTEREST EXPENSE......................................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

INVENTORY..................................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................7

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

DEPRECIATION.............................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

AUDIT PLANNING........................................................................................................................................4

ANALYTICAL REVIEW...............................................................................................................................4

PRELIMINARY JUDGMENT OF MATERIALITY............................................................................................4

BANK LOAN ACCOUNT.................................................................................................................................4

RATIONALE FOR SELECTION....................................................................................................................4

ASSERTION AND EXPLANATION...............................................................................................................4

RECOMMENDED AUDIT PROCEDURE......................................................................................................4

INTEREST INCOME.......................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................5

RECOMMENDED AUDIT PROCEDURE......................................................................................................5

MISCELLANEOUS.........................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................5

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

ACCOUNTS RECEIVABLE..............................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

INTEREST EXPENSE......................................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

INVENTORY..................................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................7

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

DEPRECIATION.............................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

REFERENCES................................................................................................................................................8

APPENDIX....................................................................................................................................................9

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

REFERENCES................................................................................................................................................8

APPENDIX....................................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT PLANNING

Audit planning is done by the auditor of the company before starting of the audit.

ANALYTICAL REVIEW

Analytical review is the preliminary stage in the audit planning. The auditors of the company are

required to conduct the analytical review of the financial statements of the company which are

unaudited. In this the auditors perform the ratio analysis and the trend analysis based on the

financial statements of the earlier three consecutive years (ACCA, 2016).

PRELIMINARY JUDGMENT OF MATERIALITY

Along with the analytical review the auditor is required to conduct the preliminary judgment of

the items which can have the material effect on the financial position and the financial

performance of the company (Ullah, 2014).

BANK LOAN ACCOUNT

RATIONALE FOR SELECTION

The bank loan account has been selected at first for the purpose of the analysis. It represents the

amount of the loan taken by the company for the purpose of the expansion of the business. It has

been selected because of the no movement of the loan account for the last two years. The balance

of the loan is same (PCAOB, 2017).

ASSERTION AND EXPLANATION

The assertion that has been made is that the amount of bank loan has been made in tact with an

amount of 240000 dollars irrespective of the passing of period of the two years. In other words,

the amount of loan is same as on 2016 and as on 2017, no payment has been made during the last

two years.

RECOMMENDED AUDIT PROCEDURE

The auditor is required to perform the additional audit procedures as to obtaining the sanction

letter of the bank or the financial institutions from whom the loan has been obtained and what are

the terms and conditions that have been laid down with the sanction letter regarding the mode of

payment and the time of payment. The auditor is required to check whether the company is under

Audit planning is done by the auditor of the company before starting of the audit.

ANALYTICAL REVIEW

Analytical review is the preliminary stage in the audit planning. The auditors of the company are

required to conduct the analytical review of the financial statements of the company which are

unaudited. In this the auditors perform the ratio analysis and the trend analysis based on the

financial statements of the earlier three consecutive years (ACCA, 2016).

PRELIMINARY JUDGMENT OF MATERIALITY

Along with the analytical review the auditor is required to conduct the preliminary judgment of

the items which can have the material effect on the financial position and the financial

performance of the company (Ullah, 2014).

BANK LOAN ACCOUNT

RATIONALE FOR SELECTION

The bank loan account has been selected at first for the purpose of the analysis. It represents the

amount of the loan taken by the company for the purpose of the expansion of the business. It has

been selected because of the no movement of the loan account for the last two years. The balance

of the loan is same (PCAOB, 2017).

ASSERTION AND EXPLANATION

The assertion that has been made is that the amount of bank loan has been made in tact with an

amount of 240000 dollars irrespective of the passing of period of the two years. In other words,

the amount of loan is same as on 2016 and as on 2017, no payment has been made during the last

two years.

RECOMMENDED AUDIT PROCEDURE

The auditor is required to perform the additional audit procedures as to obtaining the sanction

letter of the bank or the financial institutions from whom the loan has been obtained and what are

the terms and conditions that have been laid down with the sanction letter regarding the mode of

payment and the time of payment. The auditor is required to check whether the company is under

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the moratorium period or had defaulted in making the payment to the banks or concerned

financial institutions.

INTEREST INCOME

RATIONALE FOR SELECTION

Interest income is the source of revenue that the company earns from the fixed deposit made with

the bank or from the funds deposited with other institutions. It has been selected because of the

decrease in the figures irrespective of the increase in the revenue of the company.

ASSERTION AND EXPLANATION

The assertion that has been made while selecting the account for the purpose of the analysis is

that the company has not earned the income in relation to the figure of the revenue earned by the

company. The interest income has been declined from $ 50 in the year 2016 to $44 in the year of

2017. It depicts that the company has either failed to book the interest income in the accounting

books or else had not followed the proper way of depositing the money or advancing the money

in the market.

RECOMMENDED AUDIT PROCEDURE

The auditor in this case is required to check the securities in which the company has made the

deposits or the other entities where the company has invested their amount in order to earn

interest income. Secondly, the auditor shall check whether the company has accounted for all the

interest income that has been earned by the company whether it has been accounted for the same

periods.

MISCELLANEOUS

RATIONALE FOR SELECTION

The miscellaneous expense has been selected because the company has incurred the

miscellaneous expense amounting to 1320 in the current year. Secondly the miscellaneous

expense consists of the expense which cannot be bifurcated and is common for all type of the

business whether it is trading, manufacturing or the service providing company.

ASSERTION AND EXPLANATION

The assertion that has been placed is that the company has incurred the zero value of the expense

under the head of miscellaneous expense in the previous year where as in the current year under

consideration, the company has incurred the expenditure of 1320. It depicts that the company has

started incurring certain expenditures which have not been incurred earlier before. There might

financial institutions.

INTEREST INCOME

RATIONALE FOR SELECTION

Interest income is the source of revenue that the company earns from the fixed deposit made with

the bank or from the funds deposited with other institutions. It has been selected because of the

decrease in the figures irrespective of the increase in the revenue of the company.

ASSERTION AND EXPLANATION

The assertion that has been made while selecting the account for the purpose of the analysis is

that the company has not earned the income in relation to the figure of the revenue earned by the

company. The interest income has been declined from $ 50 in the year 2016 to $44 in the year of

2017. It depicts that the company has either failed to book the interest income in the accounting

books or else had not followed the proper way of depositing the money or advancing the money

in the market.

RECOMMENDED AUDIT PROCEDURE

The auditor in this case is required to check the securities in which the company has made the

deposits or the other entities where the company has invested their amount in order to earn

interest income. Secondly, the auditor shall check whether the company has accounted for all the

interest income that has been earned by the company whether it has been accounted for the same

periods.

MISCELLANEOUS

RATIONALE FOR SELECTION

The miscellaneous expense has been selected because the company has incurred the

miscellaneous expense amounting to 1320 in the current year. Secondly the miscellaneous

expense consists of the expense which cannot be bifurcated and is common for all type of the

business whether it is trading, manufacturing or the service providing company.

ASSERTION AND EXPLANATION

The assertion that has been placed is that the company has incurred the zero value of the expense

under the head of miscellaneous expense in the previous year where as in the current year under

consideration, the company has incurred the expenditure of 1320. It depicts that the company has

started incurring certain expenditures which have not been incurred earlier before. There might

be the possibility that the company might have incurred certain expenditure which might be

disallowable as per Income Tax laws and therefore the basic name of the expenditure has been

removed rather has been clubbed under the head of Miscellaneous expense.

RECOMMENDED AUDIT PROCEDURE

The auditors of the company shall extend their audit procedures with the introduction of the test

of balances and test of controls. In this regard it will be checked whether the company has been

able to substantiate the expenditure incurred with the supporting evidence. The second procedure

is to check the linkage of the expenditure so incurred with the nature of the business of the

company.

ACCOUNTS RECEIVABLE

RATIONALE FOR SELECTION

The accounts receivable consists of the customers of the companies from whom the company

have the legal right to receive the payments. The accounting trial balance of the company depicts

that the company has not received any payments from the accounts receivables from the last

previous year till the current year. Because of this nature, the accounts have been selected.

ASSERTION AND EXPLANATION

The assertion that has been made by the auditor of the company is that the company does not

focus at all on the liquidity ratio of the company and how far the company will be able to make

the liquid cash available from the market. The second assertion that has been made by the auditor

is that the account receivable may contain certain parties which may be bogus. It is because of

the covenants that the banks or the financial institutions made while issuing the loan like

maintenance of the current ratio in accordance with minimum stipulated value like 1.32 or 1.40.

RECOMMENDED AUDIT PROCEDURE

The auditor is required to perform the extra checks to see whether the accounts receivables so

shown by the company are genuine and real and it tallies with the sale invoices and the bank

details supporting each sale recorded and payment received respectively.

INTEREST EXPENSE

RATIONALE FOR SELECTION

The interest expense is the expense that the company incurs on the amount borrowed from the

financial institutions or banks or some other parties. The interest amount majorly affects the

financial statements of the company in the materialistic manner. The rationale for selecting the

account for the analysis is to ascertain what type of amounts is included in the expense and from

where the same has been originated.

disallowable as per Income Tax laws and therefore the basic name of the expenditure has been

removed rather has been clubbed under the head of Miscellaneous expense.

RECOMMENDED AUDIT PROCEDURE

The auditors of the company shall extend their audit procedures with the introduction of the test

of balances and test of controls. In this regard it will be checked whether the company has been

able to substantiate the expenditure incurred with the supporting evidence. The second procedure

is to check the linkage of the expenditure so incurred with the nature of the business of the

company.

ACCOUNTS RECEIVABLE

RATIONALE FOR SELECTION

The accounts receivable consists of the customers of the companies from whom the company

have the legal right to receive the payments. The accounting trial balance of the company depicts

that the company has not received any payments from the accounts receivables from the last

previous year till the current year. Because of this nature, the accounts have been selected.

ASSERTION AND EXPLANATION

The assertion that has been made by the auditor of the company is that the company does not

focus at all on the liquidity ratio of the company and how far the company will be able to make

the liquid cash available from the market. The second assertion that has been made by the auditor

is that the account receivable may contain certain parties which may be bogus. It is because of

the covenants that the banks or the financial institutions made while issuing the loan like

maintenance of the current ratio in accordance with minimum stipulated value like 1.32 or 1.40.

RECOMMENDED AUDIT PROCEDURE

The auditor is required to perform the extra checks to see whether the accounts receivables so

shown by the company are genuine and real and it tallies with the sale invoices and the bank

details supporting each sale recorded and payment received respectively.

INTEREST EXPENSE

RATIONALE FOR SELECTION

The interest expense is the expense that the company incurs on the amount borrowed from the

financial institutions or banks or some other parties. The interest amount majorly affects the

financial statements of the company in the materialistic manner. The rationale for selecting the

account for the analysis is to ascertain what type of amounts is included in the expense and from

where the same has been originated.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSERTION AND EXPLANATION

The first assertion that has been made by the auditor of the company is that how the interest

expense has been recognized during the year irrespective of the fact that no payment has been

made for the loan during the year. It has been kept intact for the last two consecutive years. The

second assertion that has been made by the auditor is that on what basis the interest expense over

the last two years has been decreased from 12000 to 10541.667 rather it shall be increased as

when the borrower fails to make the payment for one month then it goes on accumulating and the

interest thereon is charged as per the compounding interest method.

RECOMMENDED AUDIT PROCEDURE

The first audit procedure that is recommended for the auditor is to check the schedule of payment

if any provided by the banks and how the company has treated the same in the books of

accounts. Secondly, the documents relating to the entries made in the books of accounts shall be

checked and reviewed on regularly basis.

INVENTORY

RATIONALE FOR SELECTION

The inventory plays the important role in the financial statements as it tells about how much

goods are possessed by the company as on date and how the same shall be dealt with in the

books of accounts of the company. On the hypothecation of the inventory the company can

easily obtains the loan from the banks or the financial institutions (Anastasia, 2015).

ASSERTION AND EXPLANATION

The first assertion that is made by the auditor is that how the inventory equals to the approximate

cost of the goods that have been sold in the market in the current year as well as in the previous

year. The second assertion is that despite of the lower cost of sales, the company has reported the

higher turnover in the current year as well as in the previous year.

RECOMMENDED AUDIT PROCEDURE

The auditor shall at first check the valuation of inventory along with the bills supporting the

valuation. Secondly the auditor shall have the bin card so as to assess whether the company has

been following the FIFO method or the weighted average method.

DEPRECIATION

RATIONALE FOR SELECTION

Depreciation is the expense on the loss of wear and tear of the asset of the company. The basis

for selection of the depreciation expense is the variation in the figures in relation to the asset

The first assertion that has been made by the auditor of the company is that how the interest

expense has been recognized during the year irrespective of the fact that no payment has been

made for the loan during the year. It has been kept intact for the last two consecutive years. The

second assertion that has been made by the auditor is that on what basis the interest expense over

the last two years has been decreased from 12000 to 10541.667 rather it shall be increased as

when the borrower fails to make the payment for one month then it goes on accumulating and the

interest thereon is charged as per the compounding interest method.

RECOMMENDED AUDIT PROCEDURE

The first audit procedure that is recommended for the auditor is to check the schedule of payment

if any provided by the banks and how the company has treated the same in the books of

accounts. Secondly, the documents relating to the entries made in the books of accounts shall be

checked and reviewed on regularly basis.

INVENTORY

RATIONALE FOR SELECTION

The inventory plays the important role in the financial statements as it tells about how much

goods are possessed by the company as on date and how the same shall be dealt with in the

books of accounts of the company. On the hypothecation of the inventory the company can

easily obtains the loan from the banks or the financial institutions (Anastasia, 2015).

ASSERTION AND EXPLANATION

The first assertion that is made by the auditor is that how the inventory equals to the approximate

cost of the goods that have been sold in the market in the current year as well as in the previous

year. The second assertion is that despite of the lower cost of sales, the company has reported the

higher turnover in the current year as well as in the previous year.

RECOMMENDED AUDIT PROCEDURE

The auditor shall at first check the valuation of inventory along with the bills supporting the

valuation. Secondly the auditor shall have the bin card so as to assess whether the company has

been following the FIFO method or the weighted average method.

DEPRECIATION

RATIONALE FOR SELECTION

Depreciation is the expense on the loss of wear and tear of the asset of the company. The basis

for selection of the depreciation expense is the variation in the figures in relation to the asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

figure of the company. The depreciation has been selected for the study because it gives the tax

saving to the company concerned.

ASSERTION AND EXPLANATION

The first assertion that has been made by the auditor of the company is that the depreciation

might be inflated so as to have the extra tax savings on the allowable expense of depreciation and

how the same have been accounted in the books of accounts. The second assertion that has been

made by the auditor of the company is that the depreciation amount might have been wrongly

calculated.

RECOMMENDED AUDIT PROCEDURE

The auditor shall calculate the depreciation on its own and check the accounting policies adopted

by the company with regard to its useful life of an asset.

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html accessed on 27-09-2017.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 27-09-2017

PCAOB, (2017), “Analytical Procedures” available at

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 27-09-2017

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-financial -

statements/ accessed on 27-09-2017

saving to the company concerned.

ASSERTION AND EXPLANATION

The first assertion that has been made by the auditor of the company is that the depreciation

might be inflated so as to have the extra tax savings on the allowable expense of depreciation and

how the same have been accounted in the books of accounts. The second assertion that has been

made by the auditor of the company is that the depreciation amount might have been wrongly

calculated.

RECOMMENDED AUDIT PROCEDURE

The auditor shall calculate the depreciation on its own and check the accounting policies adopted

by the company with regard to its useful life of an asset.

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html accessed on 27-09-2017.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 27-09-2017

PCAOB, (2017), “Analytical Procedures” available at

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 27-09-2017

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-financial -

statements/ accessed on 27-09-2017

APPENDIX

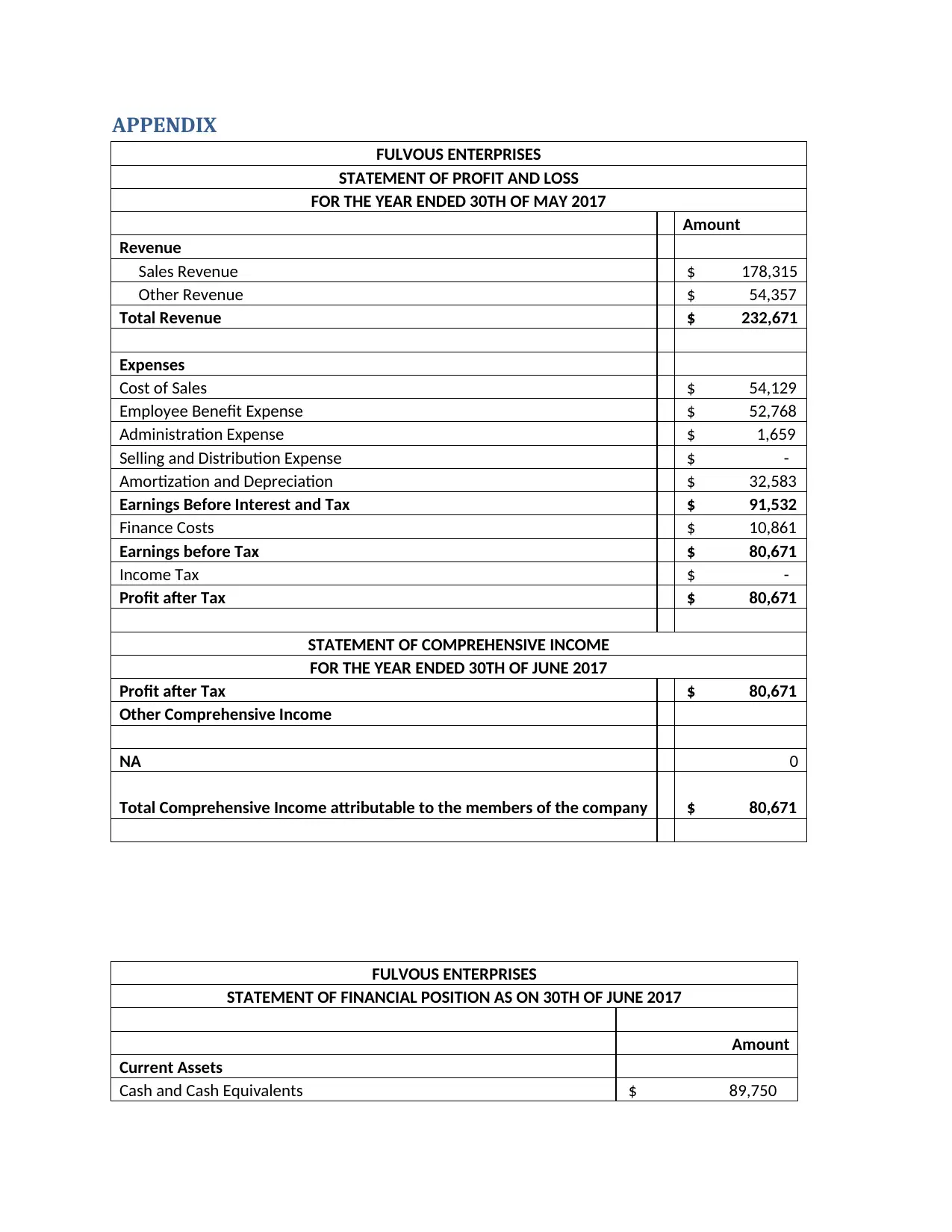

FULVOUS ENTERPRISES

STATEMENT OF PROFIT AND LOSS

FOR THE YEAR ENDED 30TH OF MAY 2017

Amount

Revenue

Sales Revenue $ 178,315

Other Revenue $ 54,357

Total Revenue $ 232,671

Expenses

Cost of Sales $ 54,129

Employee Benefit Expense $ 52,768

Administration Expense $ 1,659

Selling and Distribution Expense $ -

Amortization and Depreciation $ 32,583

Earnings Before Interest and Tax $ 91,532

Finance Costs $ 10,861

Earnings before Tax $ 80,671

Income Tax $ -

Profit after Tax $ 80,671

STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30TH OF JUNE 2017

Profit after Tax $ 80,671

Other Comprehensive Income

NA 0

Total Comprehensive Income attributable to the members of the company $ 80,671

FULVOUS ENTERPRISES

STATEMENT OF FINANCIAL POSITION AS ON 30TH OF JUNE 2017

Amount

Current Assets

Cash and Cash Equivalents $ 89,750

FULVOUS ENTERPRISES

STATEMENT OF PROFIT AND LOSS

FOR THE YEAR ENDED 30TH OF MAY 2017

Amount

Revenue

Sales Revenue $ 178,315

Other Revenue $ 54,357

Total Revenue $ 232,671

Expenses

Cost of Sales $ 54,129

Employee Benefit Expense $ 52,768

Administration Expense $ 1,659

Selling and Distribution Expense $ -

Amortization and Depreciation $ 32,583

Earnings Before Interest and Tax $ 91,532

Finance Costs $ 10,861

Earnings before Tax $ 80,671

Income Tax $ -

Profit after Tax $ 80,671

STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30TH OF JUNE 2017

Profit after Tax $ 80,671

Other Comprehensive Income

NA 0

Total Comprehensive Income attributable to the members of the company $ 80,671

FULVOUS ENTERPRISES

STATEMENT OF FINANCIAL POSITION AS ON 30TH OF JUNE 2017

Amount

Current Assets

Cash and Cash Equivalents $ 89,750

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

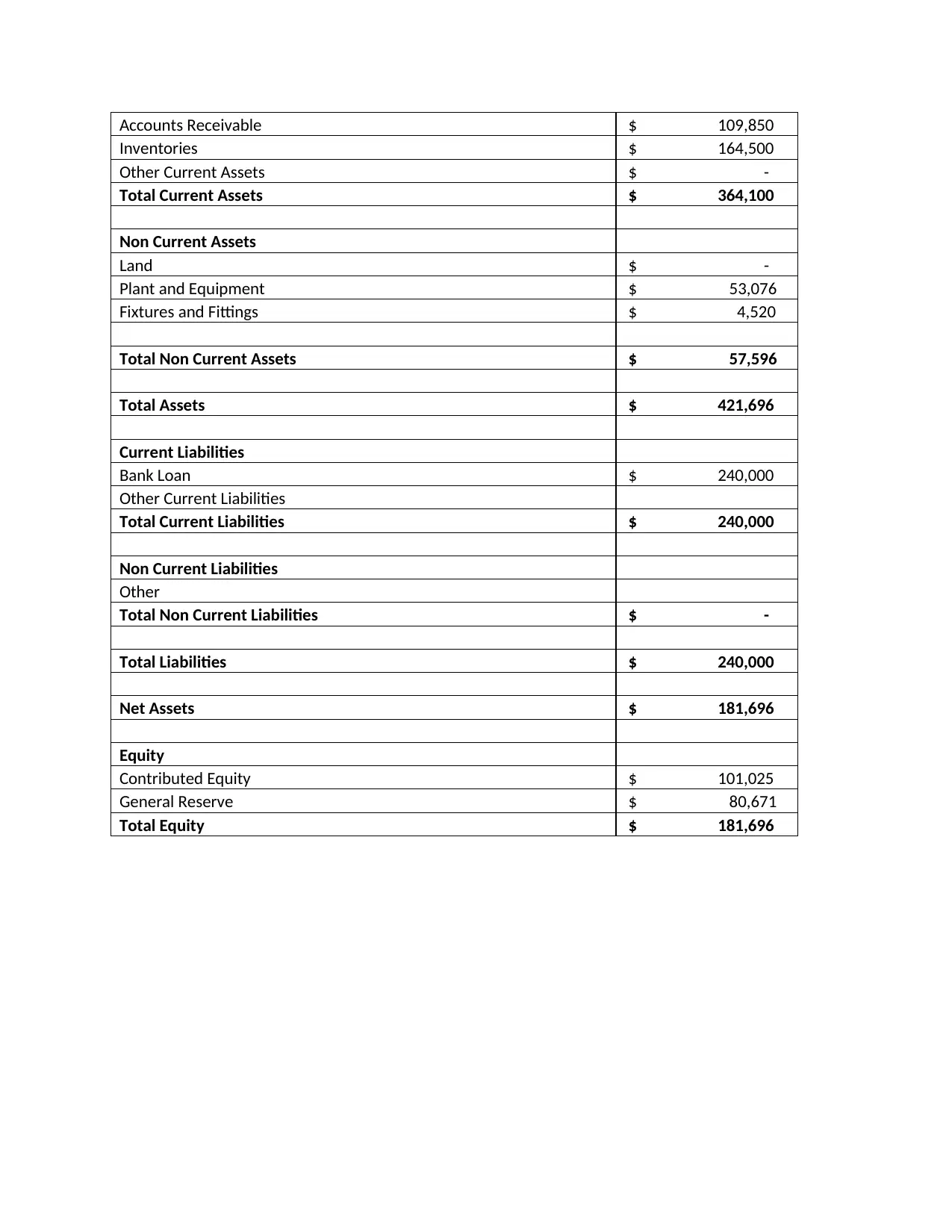

Accounts Receivable $ 109,850

Inventories $ 164,500

Other Current Assets $ -

Total Current Assets $ 364,100

Non Current Assets

Land $ -

Plant and Equipment $ 53,076

Fixtures and Fittings $ 4,520

Total Non Current Assets $ 57,596

Total Assets $ 421,696

Current Liabilities

Bank Loan $ 240,000

Other Current Liabilities

Total Current Liabilities $ 240,000

Non Current Liabilities

Other

Total Non Current Liabilities $ -

Total Liabilities $ 240,000

Net Assets $ 181,696

Equity

Contributed Equity $ 101,025

General Reserve $ 80,671

Total Equity $ 181,696

Inventories $ 164,500

Other Current Assets $ -

Total Current Assets $ 364,100

Non Current Assets

Land $ -

Plant and Equipment $ 53,076

Fixtures and Fittings $ 4,520

Total Non Current Assets $ 57,596

Total Assets $ 421,696

Current Liabilities

Bank Loan $ 240,000

Other Current Liabilities

Total Current Liabilities $ 240,000

Non Current Liabilities

Other

Total Non Current Liabilities $ -

Total Liabilities $ 240,000

Net Assets $ 181,696

Equity

Contributed Equity $ 101,025

General Reserve $ 80,671

Total Equity $ 181,696

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.