Comprehensive Auditing and Assurance Report: Aristocrat Leisure Ltd

VerifiedAdded on 2021/05/30

|11

|2098

|35

Report

AI Summary

This report provides a thorough examination of the financial statements of Aristocrat Leisure Ltd, focusing on auditing and assurance practices. The report begins with an executive summary, outlining the scope and objectives of the analysis. It then delves into the company's adherence to ASX Corporate Governance Principles, assessing the board's structure, ethical conduct, reporting integrity, disclosure practices, shareholder rights, risk management, and remuneration policies. A detailed risk assessment is conducted, evaluating the nature of the company, market overview, regulating authorities, and key financial ratios. Horizontal analysis, including income statements and balance sheets, is presented, along with significant ratio computations. The report identifies potential audit risks, such as those related to debt-equity ratios and provisions, and suggests appropriate measures to mitigate these risks. The analysis incorporates relevant references to support the findings and recommendations, providing a comprehensive overview of the company's financial health and governance practices.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING AND ASSURANCE

Table of Contents

ASX Corporate Governance Principles...........................................................................................2

Risk Assessment..........................................................................................................................4

Nature of the Company................................................................................................................4

Market Overview.........................................................................................................................5

Regulating Authority...................................................................................................................5

Ratio Analysis..................................................................................................................................5

Horizontal Analysis.........................................................................................................................5

Audit Risks......................................................................................................................................7

Measures..........................................................................................................................................7

Reference.........................................................................................................................................9

AUDITING AND ASSURANCE

Table of Contents

ASX Corporate Governance Principles...........................................................................................2

Risk Assessment..........................................................................................................................4

Nature of the Company................................................................................................................4

Market Overview.........................................................................................................................5

Regulating Authority...................................................................................................................5

Ratio Analysis..................................................................................................................................5

Horizontal Analysis.........................................................................................................................5

Audit Risks......................................................................................................................................7

Measures..........................................................................................................................................7

Reference.........................................................................................................................................9

2

AUDITING AND ASSURANCE

1. Executive Summary

The main purpose of this assignment to review the financial statements as prepared by Aristocrat

Leisure ltd. The assignment will be dealing with how the company follows and implements ASX

Corporate Governance Principles for day to day management of the business. In addition to this,

a risk assessment will be conducted on the financial statements of the company to ascertain if the

business faces any risks or not. The assignment will also be including horizontal analysis which

consists of a Common Sized Income statement and Balance sheet and significant ratio

computation will also be included in the assignment. The report will be concluding with

recommendations which are applicable to the business and which can reduce the risks which are

related to the business.

ASX Corporate Governance Principles

1. Lay Solid Foundation for management and Oversight: The board has clearly set out the

functions which are to be handled by the board and delegated those functions which are

to be handled by the management (Beekes, Brown and Zhang 2015). The board has

delegated authority to the CEO of Aristocrat Leisure ltd to look after the day to day

business of the company and regulate the same within the purview of the authority

provided. The board is responsible for reviewing the management and various roles and

responsibilities of the company. The company secretary is directly accountable to the

board for facilitating the corporate governance policies of the business and also overall

management of the business (Picken 2017). The company follows strict code so as to

ensure that the corporate governance policy of the company is being followed.

2. Structure the board to add value: The board of directors of the company is made up of

Executive and Non-Executive directors. Out of the Non-Executive directors 50% of the

AUDITING AND ASSURANCE

1. Executive Summary

The main purpose of this assignment to review the financial statements as prepared by Aristocrat

Leisure ltd. The assignment will be dealing with how the company follows and implements ASX

Corporate Governance Principles for day to day management of the business. In addition to this,

a risk assessment will be conducted on the financial statements of the company to ascertain if the

business faces any risks or not. The assignment will also be including horizontal analysis which

consists of a Common Sized Income statement and Balance sheet and significant ratio

computation will also be included in the assignment. The report will be concluding with

recommendations which are applicable to the business and which can reduce the risks which are

related to the business.

ASX Corporate Governance Principles

1. Lay Solid Foundation for management and Oversight: The board has clearly set out the

functions which are to be handled by the board and delegated those functions which are

to be handled by the management (Beekes, Brown and Zhang 2015). The board has

delegated authority to the CEO of Aristocrat Leisure ltd to look after the day to day

business of the company and regulate the same within the purview of the authority

provided. The board is responsible for reviewing the management and various roles and

responsibilities of the company. The company secretary is directly accountable to the

board for facilitating the corporate governance policies of the business and also overall

management of the business (Picken 2017). The company follows strict code so as to

ensure that the corporate governance policy of the company is being followed.

2. Structure the board to add value: The board of directors of the company is made up of

Executive and Non-Executive directors. Out of the Non-Executive directors 50% of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING AND ASSURANCE

composition is taken by women (Kumar and Singh 2013). For effective delegation of

power and responsibility the board has set up audit committee, nomination committee

and other regulatory committee as well.

3. Act Ethically and Responsibly: The board of Aristocrat Leisure ltd has put in all efforts

to establish a working environment which is ethically developed for business dealings

and other business-related activities (Weiss 2014). The company has developed a code of

conduct which is applicable to all directors, managers and all personnel of the business.

The main purpose of the establishing the code of conduct in the business is to ensure that

the financial statements are effectively prepared and integrity is maintained.

4. Safeguard Integrity in Corporate Reporting: The board is responsible for the effective

representation of the financial statements of the company. The board has set up audit

committee which is responsible to recommend to the board about the accounting policies

risk management practice of the business (Gao and Jia 2016). There is also an audit

committee charter which defines the role and responsibility of the committee more

effectively (Ezzine and Olivero 2013). In addition to this, the management of the

company has given the power to conduct independent examinations for the ensuing

effective risk management standard and reporting framework is followed.

5. Make timely and Balanced Disclosures: Aristocrat Leisure ltd has successfully developed

and implemented the policy which relates to continuous disclosure of significant items.

The management of the company understands that timely disclosure of price sensitive

information is necessary and effective communicaat6ion of the same is necessary (Fung

2014). The company secretary in conjunction with the CEO of the business has the

responsibility to look into such requirements.

AUDITING AND ASSURANCE

composition is taken by women (Kumar and Singh 2013). For effective delegation of

power and responsibility the board has set up audit committee, nomination committee

and other regulatory committee as well.

3. Act Ethically and Responsibly: The board of Aristocrat Leisure ltd has put in all efforts

to establish a working environment which is ethically developed for business dealings

and other business-related activities (Weiss 2014). The company has developed a code of

conduct which is applicable to all directors, managers and all personnel of the business.

The main purpose of the establishing the code of conduct in the business is to ensure that

the financial statements are effectively prepared and integrity is maintained.

4. Safeguard Integrity in Corporate Reporting: The board is responsible for the effective

representation of the financial statements of the company. The board has set up audit

committee which is responsible to recommend to the board about the accounting policies

risk management practice of the business (Gao and Jia 2016). There is also an audit

committee charter which defines the role and responsibility of the committee more

effectively (Ezzine and Olivero 2013). In addition to this, the management of the

company has given the power to conduct independent examinations for the ensuing

effective risk management standard and reporting framework is followed.

5. Make timely and Balanced Disclosures: Aristocrat Leisure ltd has successfully developed

and implemented the policy which relates to continuous disclosure of significant items.

The management of the company understands that timely disclosure of price sensitive

information is necessary and effective communicaat6ion of the same is necessary (Fung

2014). The company secretary in conjunction with the CEO of the business has the

responsibility to look into such requirements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING AND ASSURANCE

6. Respect the rights of the Shareholders: The company is committed towards effective

investor programs. For such a program, the company conducts regulars briefing interim

financial results, half yearly results and other similar documents. The company also

facilitates investors open days where the investor can have conversation with the

management of the company (Cremers and Ferrell 2014). The objective of the company

is to follow best disclosure practices which will benefit the employee of the company.

7. Recognize and Manage Risks: The company has an already risk management policies in

place which is working effectively. The board is of the view that the sound framework

and policies which are in place ensures that the risks are kept at a minimum (Richardson,

Taylor and Lanis 2013). The company has established a strategic risk committee which

8. Remunerate Fairly and Responsibly: The management has established a remuneration

committee which reports to the board of directors (Cybinski and Windsor 2013). The

purpose of this committee is to ensure that the top-level employee are compensated in

affair manner and thus in this way can be retained by the business.

Risk Assessment

Nature of the Company

The company is engaged in the manufacturing process of products which can be used for

games and other related stuffs. The company is regarded as one of the leading brands which is

engaged in the production of the games and stuff. The company has diverse products which

ranges from electronic gaming devices which are used by children but also systems which are

used in casinos are also developed by the company. The company operates for both online

gaming market and real markets where such games are sold.

AUDITING AND ASSURANCE

6. Respect the rights of the Shareholders: The company is committed towards effective

investor programs. For such a program, the company conducts regulars briefing interim

financial results, half yearly results and other similar documents. The company also

facilitates investors open days where the investor can have conversation with the

management of the company (Cremers and Ferrell 2014). The objective of the company

is to follow best disclosure practices which will benefit the employee of the company.

7. Recognize and Manage Risks: The company has an already risk management policies in

place which is working effectively. The board is of the view that the sound framework

and policies which are in place ensures that the risks are kept at a minimum (Richardson,

Taylor and Lanis 2013). The company has established a strategic risk committee which

8. Remunerate Fairly and Responsibly: The management has established a remuneration

committee which reports to the board of directors (Cybinski and Windsor 2013). The

purpose of this committee is to ensure that the top-level employee are compensated in

affair manner and thus in this way can be retained by the business.

Risk Assessment

Nature of the Company

The company is engaged in the manufacturing process of products which can be used for

games and other related stuffs. The company is regarded as one of the leading brands which is

engaged in the production of the games and stuff. The company has diverse products which

ranges from electronic gaming devices which are used by children but also systems which are

used in casinos are also developed by the company. The company operates for both online

gaming market and real markets where such games are sold.

5

AUDITING AND ASSURANCE

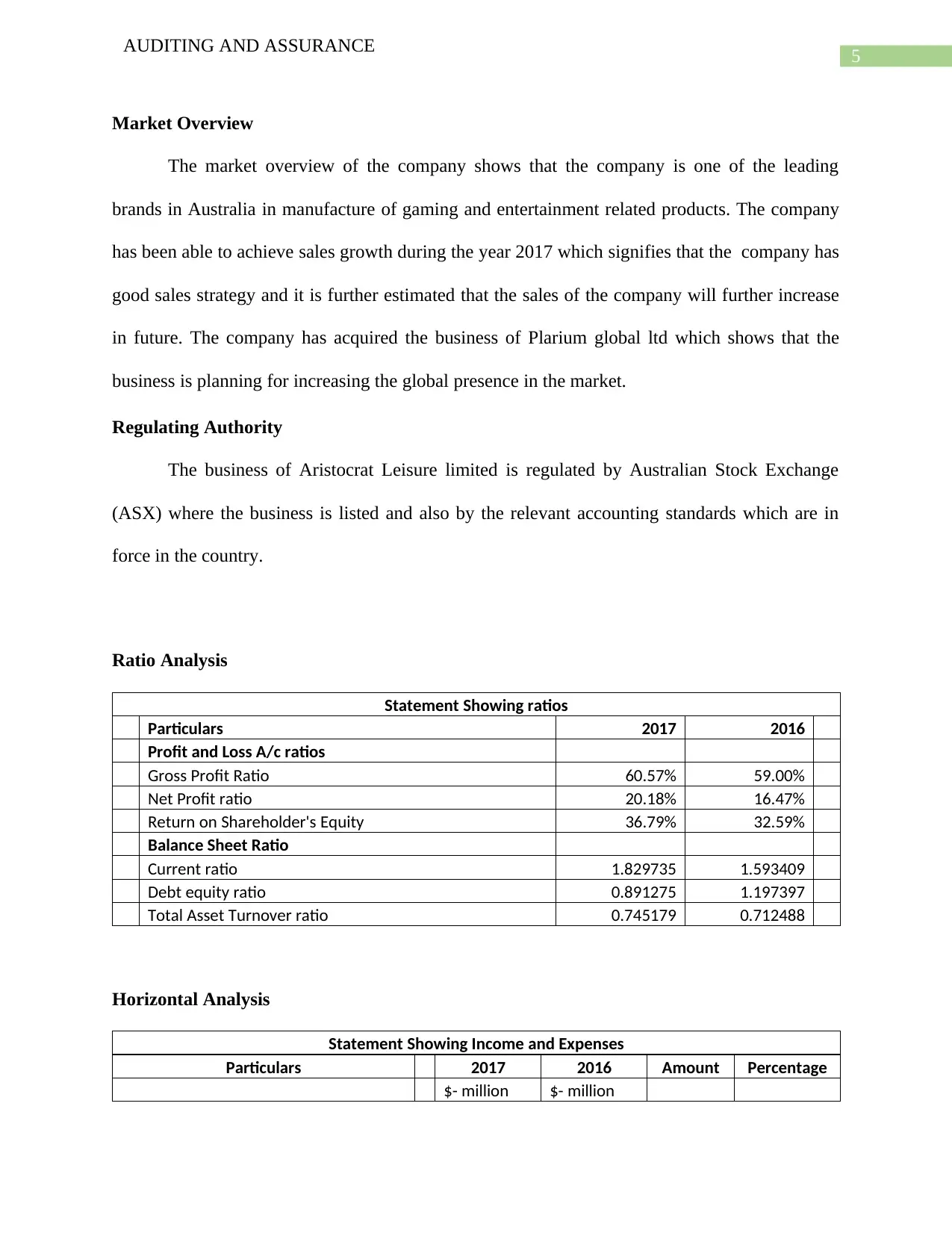

Market Overview

The market overview of the company shows that the company is one of the leading

brands in Australia in manufacture of gaming and entertainment related products. The company

has been able to achieve sales growth during the year 2017 which signifies that the company has

good sales strategy and it is further estimated that the sales of the company will further increase

in future. The company has acquired the business of Plarium global ltd which shows that the

business is planning for increasing the global presence in the market.

Regulating Authority

The business of Aristocrat Leisure limited is regulated by Australian Stock Exchange

(ASX) where the business is listed and also by the relevant accounting standards which are in

force in the country.

Ratio Analysis

Statement Showing ratios

Particulars 2017 2016

Profit and Loss A/c ratios

Gross Profit Ratio 60.57% 59.00%

Net Profit ratio 20.18% 16.47%

Return on Shareholder's Equity 36.79% 32.59%

Balance Sheet Ratio

Current ratio 1.829735 1.593409

Debt equity ratio 0.891275 1.197397

Total Asset Turnover ratio 0.745179 0.712488

Horizontal Analysis

Statement Showing Income and Expenses

Particulars 2017 2016 Amount Percentage

$- million $- million

AUDITING AND ASSURANCE

Market Overview

The market overview of the company shows that the company is one of the leading

brands in Australia in manufacture of gaming and entertainment related products. The company

has been able to achieve sales growth during the year 2017 which signifies that the company has

good sales strategy and it is further estimated that the sales of the company will further increase

in future. The company has acquired the business of Plarium global ltd which shows that the

business is planning for increasing the global presence in the market.

Regulating Authority

The business of Aristocrat Leisure limited is regulated by Australian Stock Exchange

(ASX) where the business is listed and also by the relevant accounting standards which are in

force in the country.

Ratio Analysis

Statement Showing ratios

Particulars 2017 2016

Profit and Loss A/c ratios

Gross Profit Ratio 60.57% 59.00%

Net Profit ratio 20.18% 16.47%

Return on Shareholder's Equity 36.79% 32.59%

Balance Sheet Ratio

Current ratio 1.829735 1.593409

Debt equity ratio 0.891275 1.197397

Total Asset Turnover ratio 0.745179 0.712488

Horizontal Analysis

Statement Showing Income and Expenses

Particulars 2017 2016 Amount Percentage

$- million $- million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING AND ASSURANCE

Revenue $ 2,453.80 $ 2,128.70 325.1000 0.1527

Cost of revenue $ 967.60 $ 872.70 94.9 0.1087

Gross Profit $ 1,486.20 $ 1,256.00 230.2 0.1833

Other income $ 10.00 $ 11.60 -1.600 -0.138

Design and development costs $ 268.40 $ 239.20 29.200 0.122

Sales and marketing costs $ 116.80 $ 119.50 -2.700 -0.023

General and administration costs $ 320.20 $ 301.50 18.700 0.062

Finance costs $ 62.70 $ 100.20 -37.500 -0.374

Profit before income tax $ 728.10 $ 507.20 220.900 0.436

Income tax (expense)/benefit $ 233.00 $ 156.70 76.300 0.487

Profit for the year $ 495.10 $ 350.50 144.600 0.413

Balance Sheet

2017 2016 Amount Percentage

Assets $- million $- million

Current assets

Cash and cash equivalents 547.1 283.2 263.900 93%

Trade and other receivables 512.3 432.9 79.400 18%

Inventories 116.4 124.3 -7.900 -6%

Financial assets 6.4 7 -0.600 -9%

Current tax assets 12.8 27.7 -14.900 -54%

Total current assets 1195 875.1 319.900 37%

Non-current assets

Trade and other receivables 107 96.9 10.1 0.1042

Financial assets 7.8 6.6 1.2 0.1818

Property, plant and equipment 241.3 217.5 23.800 11%

Intangible assets 1687.7 1736.5 -48.800 -3%

Deferred tax assets 54.1 55.1 -1.000 -2%

Total non-current assets 2097.9 2112.6 -14.700 -1%

Total assets 3292.9 2987.7 305.200 10%

LIABILITIES

Current liabilities

Trade and other payables 404.7 371.1 33.600 9%

Provisions 44.3 32.5 11.800 36%

Borrowings 0.1 0

Current tax liabilities 148.7 81.8 66.900 82%

Financial liabilities 0.5 0

Deferred revenue 54.8 63.8 -9.000 -14%

Total current liabilities 653.1 549.2 103.900 19%

Non-current liabilities

AUDITING AND ASSURANCE

Revenue $ 2,453.80 $ 2,128.70 325.1000 0.1527

Cost of revenue $ 967.60 $ 872.70 94.9 0.1087

Gross Profit $ 1,486.20 $ 1,256.00 230.2 0.1833

Other income $ 10.00 $ 11.60 -1.600 -0.138

Design and development costs $ 268.40 $ 239.20 29.200 0.122

Sales and marketing costs $ 116.80 $ 119.50 -2.700 -0.023

General and administration costs $ 320.20 $ 301.50 18.700 0.062

Finance costs $ 62.70 $ 100.20 -37.500 -0.374

Profit before income tax $ 728.10 $ 507.20 220.900 0.436

Income tax (expense)/benefit $ 233.00 $ 156.70 76.300 0.487

Profit for the year $ 495.10 $ 350.50 144.600 0.413

Balance Sheet

2017 2016 Amount Percentage

Assets $- million $- million

Current assets

Cash and cash equivalents 547.1 283.2 263.900 93%

Trade and other receivables 512.3 432.9 79.400 18%

Inventories 116.4 124.3 -7.900 -6%

Financial assets 6.4 7 -0.600 -9%

Current tax assets 12.8 27.7 -14.900 -54%

Total current assets 1195 875.1 319.900 37%

Non-current assets

Trade and other receivables 107 96.9 10.1 0.1042

Financial assets 7.8 6.6 1.2 0.1818

Property, plant and equipment 241.3 217.5 23.800 11%

Intangible assets 1687.7 1736.5 -48.800 -3%

Deferred tax assets 54.1 55.1 -1.000 -2%

Total non-current assets 2097.9 2112.6 -14.700 -1%

Total assets 3292.9 2987.7 305.200 10%

LIABILITIES

Current liabilities

Trade and other payables 404.7 371.1 33.600 9%

Provisions 44.3 32.5 11.800 36%

Borrowings 0.1 0

Current tax liabilities 148.7 81.8 66.900 82%

Financial liabilities 0.5 0

Deferred revenue 54.8 63.8 -9.000 -14%

Total current liabilities 653.1 549.2 103.900 19%

Non-current liabilities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING AND ASSURANCE

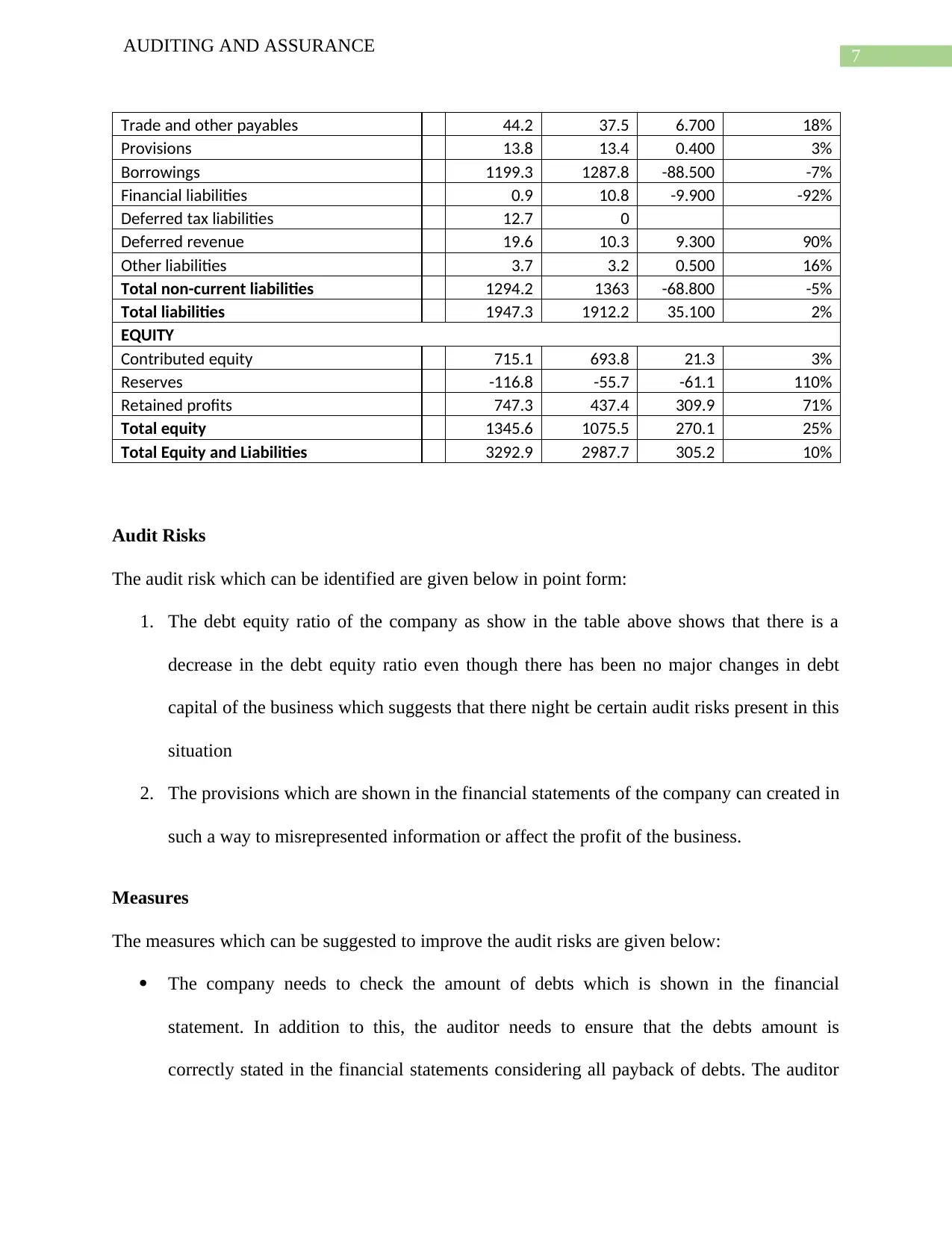

Trade and other payables 44.2 37.5 6.700 18%

Provisions 13.8 13.4 0.400 3%

Borrowings 1199.3 1287.8 -88.500 -7%

Financial liabilities 0.9 10.8 -9.900 -92%

Deferred tax liabilities 12.7 0

Deferred revenue 19.6 10.3 9.300 90%

Other liabilities 3.7 3.2 0.500 16%

Total non-current liabilities 1294.2 1363 -68.800 -5%

Total liabilities 1947.3 1912.2 35.100 2%

EQUITY

Contributed equity 715.1 693.8 21.3 3%

Reserves -116.8 -55.7 -61.1 110%

Retained profits 747.3 437.4 309.9 71%

Total equity 1345.6 1075.5 270.1 25%

Total Equity and Liabilities 3292.9 2987.7 305.2 10%

Audit Risks

The audit risk which can be identified are given below in point form:

1. The debt equity ratio of the company as show in the table above shows that there is a

decrease in the debt equity ratio even though there has been no major changes in debt

capital of the business which suggests that there night be certain audit risks present in this

situation

2. The provisions which are shown in the financial statements of the company can created in

such a way to misrepresented information or affect the profit of the business.

Measures

The measures which can be suggested to improve the audit risks are given below:

The company needs to check the amount of debts which is shown in the financial

statement. In addition to this, the auditor needs to ensure that the debts amount is

correctly stated in the financial statements considering all payback of debts. The auditor

AUDITING AND ASSURANCE

Trade and other payables 44.2 37.5 6.700 18%

Provisions 13.8 13.4 0.400 3%

Borrowings 1199.3 1287.8 -88.500 -7%

Financial liabilities 0.9 10.8 -9.900 -92%

Deferred tax liabilities 12.7 0

Deferred revenue 19.6 10.3 9.300 90%

Other liabilities 3.7 3.2 0.500 16%

Total non-current liabilities 1294.2 1363 -68.800 -5%

Total liabilities 1947.3 1912.2 35.100 2%

EQUITY

Contributed equity 715.1 693.8 21.3 3%

Reserves -116.8 -55.7 -61.1 110%

Retained profits 747.3 437.4 309.9 71%

Total equity 1345.6 1075.5 270.1 25%

Total Equity and Liabilities 3292.9 2987.7 305.2 10%

Audit Risks

The audit risk which can be identified are given below in point form:

1. The debt equity ratio of the company as show in the table above shows that there is a

decrease in the debt equity ratio even though there has been no major changes in debt

capital of the business which suggests that there night be certain audit risks present in this

situation

2. The provisions which are shown in the financial statements of the company can created in

such a way to misrepresented information or affect the profit of the business.

Measures

The measures which can be suggested to improve the audit risks are given below:

The company needs to check the amount of debts which is shown in the financial

statement. In addition to this, the auditor needs to ensure that the debts amount is

correctly stated in the financial statements considering all payback of debts. The auditor

8

AUDITING AND ASSURANCE

while conducting the process of audit needs to verify the same and also ensure that the

debts are accurately recorded and no misstatements are present.

Th auditor needs to verify the genuineness of a provision and establish whether the

provision is really required or not for effective presentation of financial information.

AUDITING AND ASSURANCE

while conducting the process of audit needs to verify the same and also ensure that the

debts are accurately recorded and no misstatements are present.

Th auditor needs to verify the genuineness of a provision and establish whether the

provision is really required or not for effective presentation of financial information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING AND ASSURANCE

Reference

Beekes, W., Brown, P. and Zhang, Q., 2015. Corporate governance and the informativeness of

disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), pp.931-963.

Cremers, M. and Ferrell, A., 2014. Thirty years of shareholder rights and firm value. The

Journal of Finance, 69(3), pp.1167-1196.

Cybinski, P. and Windsor, C., 2013. Remuneration committee independence and CEO

remuneration for firm financial performance. Accounting Research Journal, 26(3), pp.197-221.

Ezzine, H. and Olivero, B., 2013. Evolution of corporate governance during the recent financial

crises.

Fung, B., 2014. The demand and need for transparency and disclosure in corporate

governance. Universal Journal of Management, 2(2), pp.72-80.

Gao, X. and Jia, Y., 2016. Internal control over financial reporting and the safeguarding of

corporate resources: Evidence from the value of cash holdings. Contemporary Accounting

Research, 33(2), pp.783-814.

Kumar, N. and Singh, J.P., 2013. Effect of board size and promoter ownership on firm value:

some empirical findings from India. Corporate Governance: The international journal of

business in society, 13(1), pp.88-98.

Picken, J.C., 2017. From startup to scalable enterprise: Laying the foundation. Business

Horizons, 60(5), pp.587-595.

Richardson, G., Taylor, G. and Lanis, R., 2013. The impact of board of director oversight

characteristics on corporate tax aggressiveness: An empirical analysis. Journal of Accounting

and Public Policy, 32(3), pp.68-88.

AUDITING AND ASSURANCE

Reference

Beekes, W., Brown, P. and Zhang, Q., 2015. Corporate governance and the informativeness of

disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), pp.931-963.

Cremers, M. and Ferrell, A., 2014. Thirty years of shareholder rights and firm value. The

Journal of Finance, 69(3), pp.1167-1196.

Cybinski, P. and Windsor, C., 2013. Remuneration committee independence and CEO

remuneration for firm financial performance. Accounting Research Journal, 26(3), pp.197-221.

Ezzine, H. and Olivero, B., 2013. Evolution of corporate governance during the recent financial

crises.

Fung, B., 2014. The demand and need for transparency and disclosure in corporate

governance. Universal Journal of Management, 2(2), pp.72-80.

Gao, X. and Jia, Y., 2016. Internal control over financial reporting and the safeguarding of

corporate resources: Evidence from the value of cash holdings. Contemporary Accounting

Research, 33(2), pp.783-814.

Kumar, N. and Singh, J.P., 2013. Effect of board size and promoter ownership on firm value:

some empirical findings from India. Corporate Governance: The international journal of

business in society, 13(1), pp.88-98.

Picken, J.C., 2017. From startup to scalable enterprise: Laying the foundation. Business

Horizons, 60(5), pp.587-595.

Richardson, G., Taylor, G. and Lanis, R., 2013. The impact of board of director oversight

characteristics on corporate tax aggressiveness: An empirical analysis. Journal of Accounting

and Public Policy, 32(3), pp.68-88.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING AND ASSURANCE

Weiss, J.W., 2014. Business ethics: A stakeholder and issues management approach. Berrett-

Koehler Publishers.

AUDITING AND ASSURANCE

Weiss, J.W., 2014. Business ethics: A stakeholder and issues management approach. Berrett-

Koehler Publishers.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.