University of XXXXXXXXXXXX: BUS000 Audit Planning Report 2018

VerifiedAdded on 2023/06/04

|12

|2469

|496

Report

AI Summary

This report, prepared for an audit partner, focuses on audit planning for Cadmium Enterprises. It begins with an executive summary, table of contents, and an introduction. The report details the trial balance, determination of materiality, and a preliminary analytical review, including a common size income statement and variance analysis. Key income statement accounts like sales, cost of sales, repair and maintenance, and superannuation are analyzed, with identified assertions and related risks. The report outlines audit procedures for these accounts. The report also includes a fraud risk analysis, and concludes with recommendations, including a suggestion to check the balance sheet for evidence. References are provided at the end.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Issues in Auditing

Practice Assignment

1

2018

BUS000, Tutor Name, Tutorial Time

Student Name, SID: XXXXXXXXXX

University of XXXXXXXXXXXXX | [Company address]

Practice Assignment

1

2018

BUS000, Tutor Name, Tutorial Time

Student Name, SID: XXXXXXXXXX

University of XXXXXXXXXXXXX | [Company address]

Executive Summary

A report has been prepared on the topic of audit planning. The report will be submitted to

the audit partner of the firm. The report incorporates the identification of the critical

accounts to be audited, the risks and the key assertions with respect to the same and the

audit procedures to be taken up by the auditors in this regard. The report also highlights the

fraud risk analysis for the given entity and why the same is critical. All these analysis have

been done using preliminary analytical review.

i

A report has been prepared on the topic of audit planning. The report will be submitted to

the audit partner of the firm. The report incorporates the identification of the critical

accounts to be audited, the risks and the key assertions with respect to the same and the

audit procedures to be taken up by the auditors in this regard. The report also highlights the

fraud risk analysis for the given entity and why the same is critical. All these analysis have

been done using preliminary analytical review.

i

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table of Contents

Executive Summary................................................................................................................................i

Table of Contents...................................................................................................................................ii

1. Introduction...................................................................................................................................1

1.1. Authorisation.........................................................................................................................1

1.2. Limitations.............................................................................................................................1

1.3. Scope.....................................................................................................................................1

2. Inputs to the report - Analysis.......................................................................................................2

2.1. Trial balance input.................................................................................................................2

2.2. Determination of Materiality.................................................................................................2

2.3. Preliminary Analytical Review................................................................................................3

3. Discussion on the report................................................................................................................4

3.1. Income statement accounts to be analysed..........................................................................4

3.2. Audit procedures to be undertaken.......................................................................................5

4. Conclusion – Fraud Risk Analysis...................................................................................................6

5. Recommendations.........................................................................................................................6

References.............................................................................................................................................7

ii

Executive Summary................................................................................................................................i

Table of Contents...................................................................................................................................ii

1. Introduction...................................................................................................................................1

1.1. Authorisation.........................................................................................................................1

1.2. Limitations.............................................................................................................................1

1.3. Scope.....................................................................................................................................1

2. Inputs to the report - Analysis.......................................................................................................2

2.1. Trial balance input.................................................................................................................2

2.2. Determination of Materiality.................................................................................................2

2.3. Preliminary Analytical Review................................................................................................3

3. Discussion on the report................................................................................................................4

3.1. Income statement accounts to be analysed..........................................................................4

3.2. Audit procedures to be undertaken.......................................................................................5

4. Conclusion – Fraud Risk Analysis...................................................................................................6

5. Recommendations.........................................................................................................................6

References.............................................................................................................................................7

ii

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.Introduction

1.1. Authorisation

The given report has been prepared for the audit partner of the firm and will be handed over

with the details on the audit planning of one of the small entities “Cadmium Enterprises”.

The report also has conclusion and the recommendation at the end.

1.2. Limitations

The given report has only one of the limitations in the form of the trial balances which is not

balanced. The debit and the credit totals are not matching for both the periods and

therefore the same has been assumed to be suspense account. Since the nature of the same

is not known, it has not been considered in any of the analytics (Bumgarner & Vasarhelyi,

2018).

1.3. Scope

The report starts with the determination of the materiality limit for the entity. It also enlists

the critical accounts to be audited and the audit procedures to be undertaken to audit them.

It encloses the common size income statement and the variance analysis in respect of the

entity. Towards the end, the fraud risk analysis has been done for the given entity to check

on the possibility of fraud (Willcocks, 2017).

1

1.1. Authorisation

The given report has been prepared for the audit partner of the firm and will be handed over

with the details on the audit planning of one of the small entities “Cadmium Enterprises”.

The report also has conclusion and the recommendation at the end.

1.2. Limitations

The given report has only one of the limitations in the form of the trial balances which is not

balanced. The debit and the credit totals are not matching for both the periods and

therefore the same has been assumed to be suspense account. Since the nature of the same

is not known, it has not been considered in any of the analytics (Bumgarner & Vasarhelyi,

2018).

1.3. Scope

The report starts with the determination of the materiality limit for the entity. It also enlists

the critical accounts to be audited and the audit procedures to be undertaken to audit them.

It encloses the common size income statement and the variance analysis in respect of the

entity. Towards the end, the fraud risk analysis has been done for the given entity to check

on the possibility of fraud (Willcocks, 2017).

1

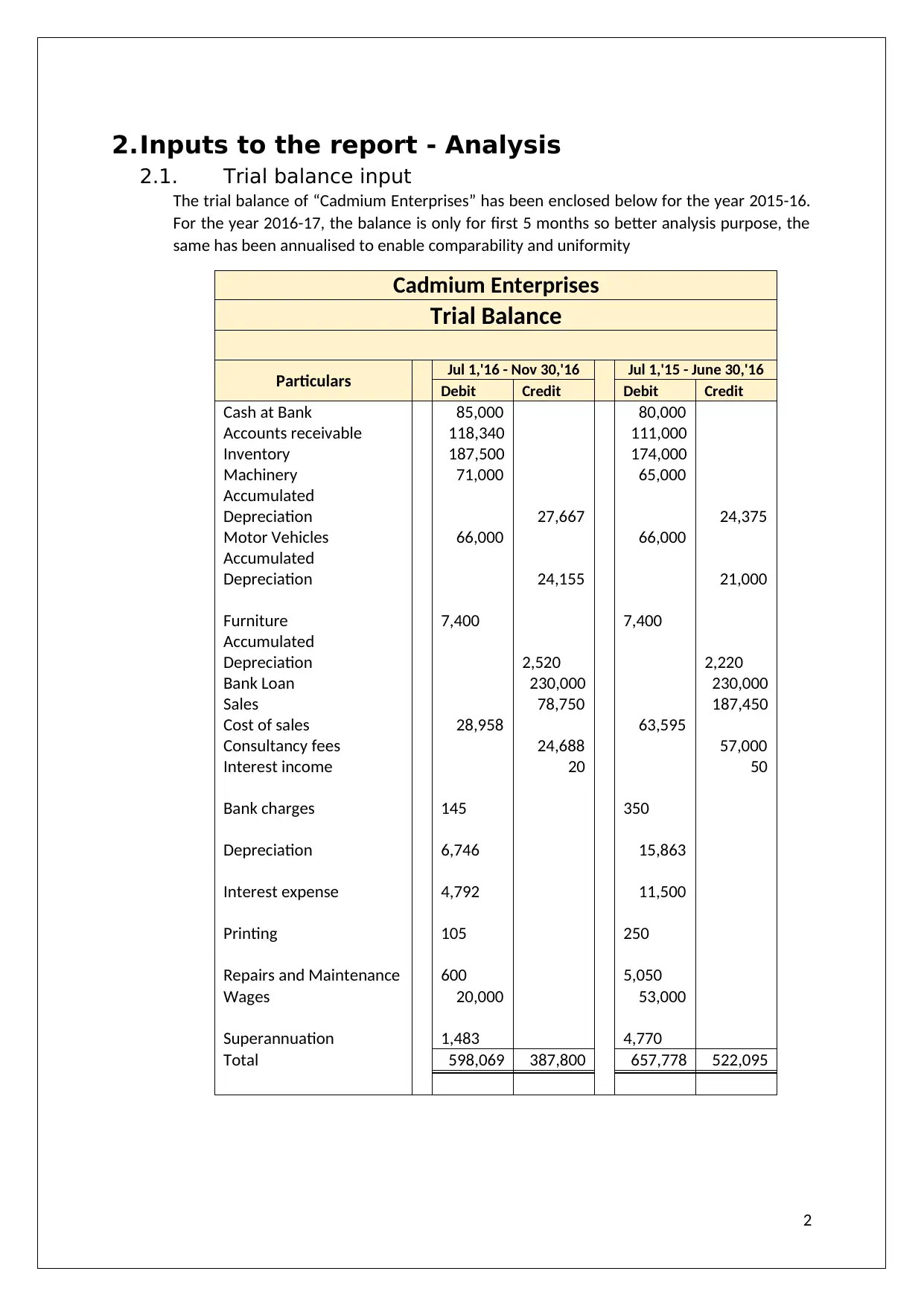

2.Inputs to the report - Analysis

2.1. Trial balance input

The trial balance of “Cadmium Enterprises” has been enclosed below for the year 2015-16.

For the year 2016-17, the balance is only for first 5 months so better analysis purpose, the

same has been annualised to enable comparability and uniformity

Cadmium Enterprises

Trial Balance

Particulars Jul 1,'16 - Nov 30,'16 Jul 1,'15 - June 30,'16

Debit Credit Debit Credit

Cash at Bank 85,000 80,000

Accounts receivable 118,340 111,000

Inventory 187,500 174,000

Machinery 71,000 65,000

Accumulated

Depreciation 27,667 24,375

Motor Vehicles 66,000 66,000

Accumulated

Depreciation 24,155 21,000

Furniture 7,400 7,400

Accumulated

Depreciation 2,520 2,220

Bank Loan 230,000 230,000

Sales 78,750 187,450

Cost of sales 28,958 63,595

Consultancy fees 24,688 57,000

Interest income 20 50

Bank charges 145 350

Depreciation 6,746 15,863

Interest expense 4,792 11,500

Printing 105 250

Repairs and Maintenance 600 5,050

Wages 20,000 53,000

Superannuation 1,483 4,770

Total 598,069 387,800 657,778 522,095

2

2.1. Trial balance input

The trial balance of “Cadmium Enterprises” has been enclosed below for the year 2015-16.

For the year 2016-17, the balance is only for first 5 months so better analysis purpose, the

same has been annualised to enable comparability and uniformity

Cadmium Enterprises

Trial Balance

Particulars Jul 1,'16 - Nov 30,'16 Jul 1,'15 - June 30,'16

Debit Credit Debit Credit

Cash at Bank 85,000 80,000

Accounts receivable 118,340 111,000

Inventory 187,500 174,000

Machinery 71,000 65,000

Accumulated

Depreciation 27,667 24,375

Motor Vehicles 66,000 66,000

Accumulated

Depreciation 24,155 21,000

Furniture 7,400 7,400

Accumulated

Depreciation 2,520 2,220

Bank Loan 230,000 230,000

Sales 78,750 187,450

Cost of sales 28,958 63,595

Consultancy fees 24,688 57,000

Interest income 20 50

Bank charges 145 350

Depreciation 6,746 15,863

Interest expense 4,792 11,500

Printing 105 250

Repairs and Maintenance 600 5,050

Wages 20,000 53,000

Superannuation 1,483 4,770

Total 598,069 387,800 657,778 522,095

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

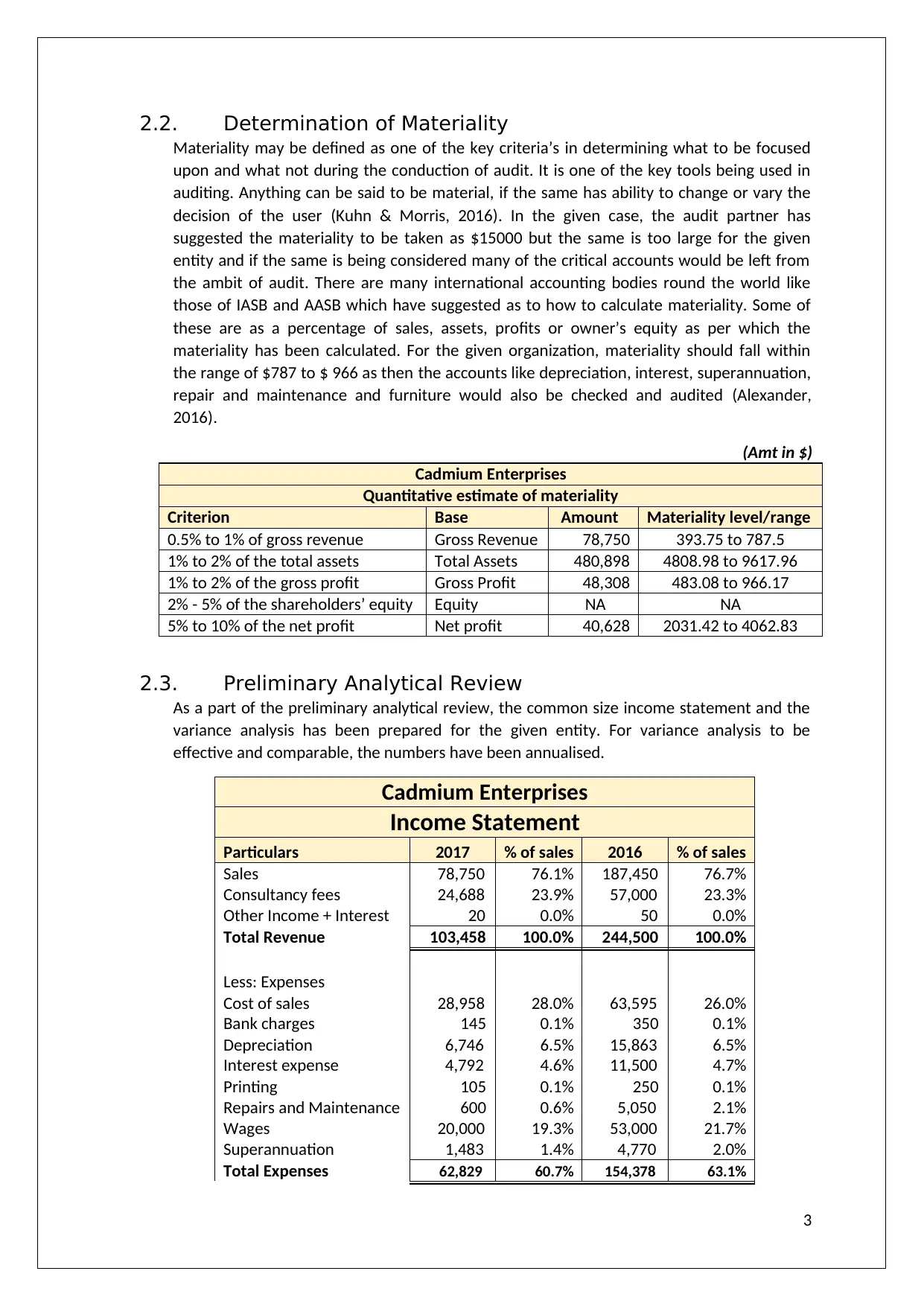

2.2. Determination of Materiality

Materiality may be defined as one of the key criteria’s in determining what to be focused

upon and what not during the conduction of audit. It is one of the key tools being used in

auditing. Anything can be said to be material, if the same has ability to change or vary the

decision of the user (Kuhn & Morris, 2016). In the given case, the audit partner has

suggested the materiality to be taken as $15000 but the same is too large for the given

entity and if the same is being considered many of the critical accounts would be left from

the ambit of audit. There are many international accounting bodies round the world like

those of IASB and AASB which have suggested as to how to calculate materiality. Some of

these are as a percentage of sales, assets, profits or owner’s equity as per which the

materiality has been calculated. For the given organization, materiality should fall within

the range of $787 to $ 966 as then the accounts like depreciation, interest, superannuation,

repair and maintenance and furniture would also be checked and audited (Alexander,

2016).

(Amt in $)

Cadmium Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 78,750 393.75 to 787.5

1% to 2% of the total assets Total Assets 480,898 4808.98 to 9617.96

1% to 2% of the gross profit Gross Profit 48,308 483.08 to 966.17

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 40,628 2031.42 to 4062.83

2.3. Preliminary Analytical Review

As a part of the preliminary analytical review, the common size income statement and the

variance analysis has been prepared for the given entity. For variance analysis to be

effective and comparable, the numbers have been annualised.

Cadmium Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 78,750 76.1% 187,450 76.7%

Consultancy fees 24,688 23.9% 57,000 23.3%

Other Income + Interest 20 0.0% 50 0.0%

Total Revenue 103,458 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 28,958 28.0% 63,595 26.0%

Bank charges 145 0.1% 350 0.1%

Depreciation 6,746 6.5% 15,863 6.5%

Interest expense 4,792 4.6% 11,500 4.7%

Printing 105 0.1% 250 0.1%

Repairs and Maintenance 600 0.6% 5,050 2.1%

Wages 20,000 19.3% 53,000 21.7%

Superannuation 1,483 1.4% 4,770 2.0%

Total Expenses 62,829 60.7% 154,378 63.1%

3

Materiality may be defined as one of the key criteria’s in determining what to be focused

upon and what not during the conduction of audit. It is one of the key tools being used in

auditing. Anything can be said to be material, if the same has ability to change or vary the

decision of the user (Kuhn & Morris, 2016). In the given case, the audit partner has

suggested the materiality to be taken as $15000 but the same is too large for the given

entity and if the same is being considered many of the critical accounts would be left from

the ambit of audit. There are many international accounting bodies round the world like

those of IASB and AASB which have suggested as to how to calculate materiality. Some of

these are as a percentage of sales, assets, profits or owner’s equity as per which the

materiality has been calculated. For the given organization, materiality should fall within

the range of $787 to $ 966 as then the accounts like depreciation, interest, superannuation,

repair and maintenance and furniture would also be checked and audited (Alexander,

2016).

(Amt in $)

Cadmium Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 78,750 393.75 to 787.5

1% to 2% of the total assets Total Assets 480,898 4808.98 to 9617.96

1% to 2% of the gross profit Gross Profit 48,308 483.08 to 966.17

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 40,628 2031.42 to 4062.83

2.3. Preliminary Analytical Review

As a part of the preliminary analytical review, the common size income statement and the

variance analysis has been prepared for the given entity. For variance analysis to be

effective and comparable, the numbers have been annualised.

Cadmium Enterprises

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 78,750 76.1% 187,450 76.7%

Consultancy fees 24,688 23.9% 57,000 23.3%

Other Income + Interest 20 0.0% 50 0.0%

Total Revenue 103,458 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 28,958 28.0% 63,595 26.0%

Bank charges 145 0.1% 350 0.1%

Depreciation 6,746 6.5% 15,863 6.5%

Interest expense 4,792 4.6% 11,500 4.7%

Printing 105 0.1% 250 0.1%

Repairs and Maintenance 600 0.6% 5,050 2.1%

Wages 20,000 19.3% 53,000 21.7%

Superannuation 1,483 1.4% 4,770 2.0%

Total Expenses 62,829 60.7% 154,378 63.1%

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

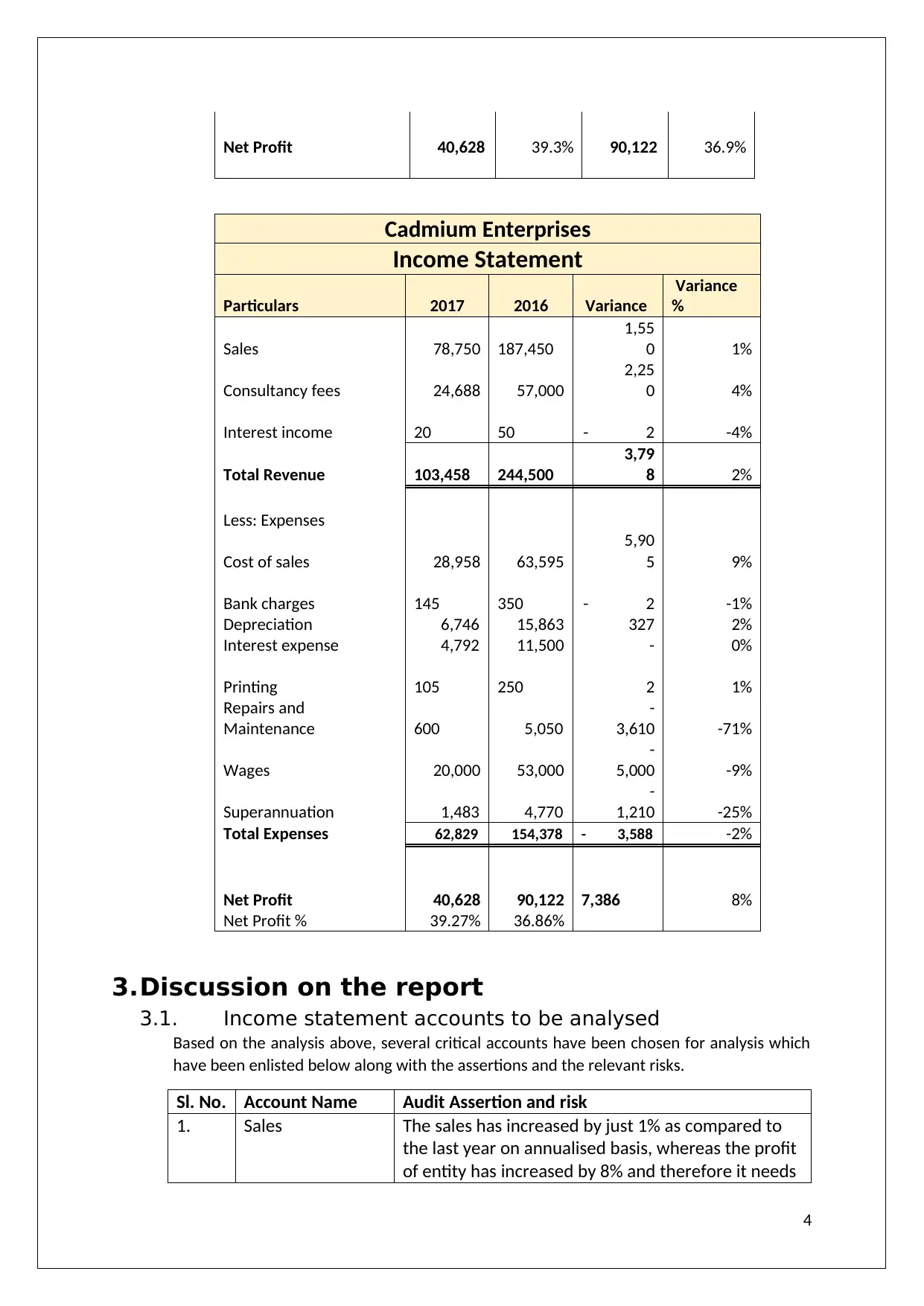

Net Profit 40,628 39.3% 90,122 36.9%

Cadmium Enterprises

Income Statement

Particulars 2017 2016 Variance

Variance

%

Sales 78,750 187,450

1,55

0 1%

Consultancy fees 24,688 57,000

2,25

0 4%

Interest income 20 50 - 2 -4%

Total Revenue 103,458 244,500

3,79

8 2%

Less: Expenses

Cost of sales 28,958 63,595

5,90

5 9%

Bank charges 145 350 - 2 -1%

Depreciation 6,746 15,863 327 2%

Interest expense 4,792 11,500 - 0%

Printing 105 250 2 1%

Repairs and

Maintenance 600 5,050

-

3,610 -71%

Wages 20,000 53,000

-

5,000 -9%

Superannuation 1,483 4,770

-

1,210 -25%

Total Expenses 62,829 154,378 - 3,588 -2%

Net Profit 40,628 90,122 7,386 8%

Net Profit % 39.27% 36.86%

3.Discussion on the report

3.1. Income statement accounts to be analysed

Based on the analysis above, several critical accounts have been chosen for analysis which

have been enlisted below along with the assertions and the relevant risks.

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has increased by just 1% as compared to

the last year on annualised basis, whereas the profit

of entity has increased by 8% and therefore it needs

4

Cadmium Enterprises

Income Statement

Particulars 2017 2016 Variance

Variance

%

Sales 78,750 187,450

1,55

0 1%

Consultancy fees 24,688 57,000

2,25

0 4%

Interest income 20 50 - 2 -4%

Total Revenue 103,458 244,500

3,79

8 2%

Less: Expenses

Cost of sales 28,958 63,595

5,90

5 9%

Bank charges 145 350 - 2 -1%

Depreciation 6,746 15,863 327 2%

Interest expense 4,792 11,500 - 0%

Printing 105 250 2 1%

Repairs and

Maintenance 600 5,050

-

3,610 -71%

Wages 20,000 53,000

-

5,000 -9%

Superannuation 1,483 4,770

-

1,210 -25%

Total Expenses 62,829 154,378 - 3,588 -2%

Net Profit 40,628 90,122 7,386 8%

Net Profit % 39.27% 36.86%

3.Discussion on the report

3.1. Income statement accounts to be analysed

Based on the analysis above, several critical accounts have been chosen for analysis which

have been enlisted below along with the assertions and the relevant risks.

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has increased by just 1% as compared to

the last year on annualised basis, whereas the profit

of entity has increased by 8% and therefore it needs

4

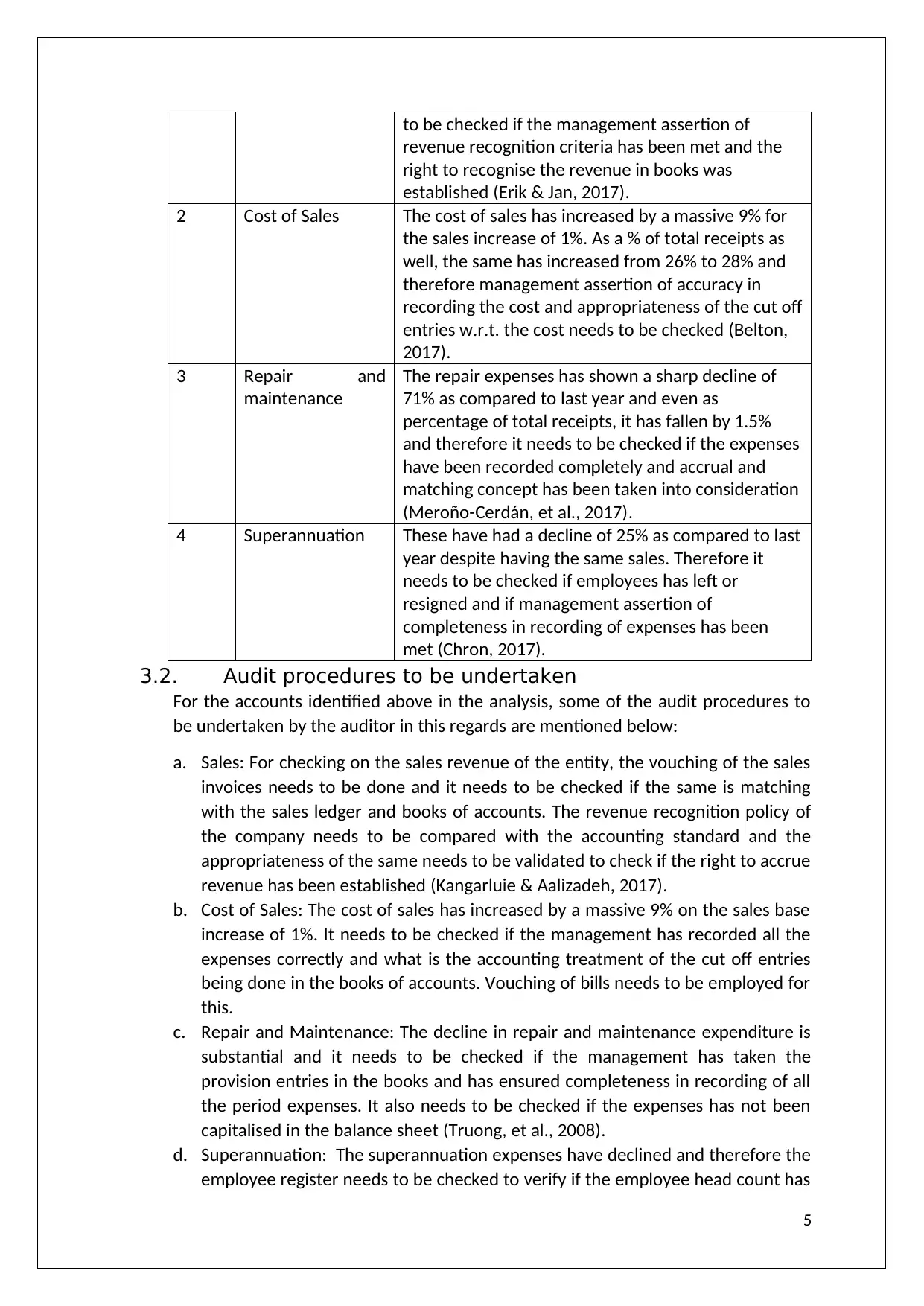

to be checked if the management assertion of

revenue recognition criteria has been met and the

right to recognise the revenue in books was

established (Erik & Jan, 2017).

2 Cost of Sales The cost of sales has increased by a massive 9% for

the sales increase of 1%. As a % of total receipts as

well, the same has increased from 26% to 28% and

therefore management assertion of accuracy in

recording the cost and appropriateness of the cut off

entries w.r.t. the cost needs to be checked (Belton,

2017).

3 Repair and

maintenance

The repair expenses has shown a sharp decline of

71% as compared to last year and even as

percentage of total receipts, it has fallen by 1.5%

and therefore it needs to be checked if the expenses

have been recorded completely and accrual and

matching concept has been taken into consideration

(Meroño-Cerdán, et al., 2017).

4 Superannuation These have had a decline of 25% as compared to last

year despite having the same sales. Therefore it

needs to be checked if employees has left or

resigned and if management assertion of

completeness in recording of expenses has been

met (Chron, 2017).

3.2. Audit procedures to be undertaken

For the accounts identified above in the analysis, some of the audit procedures to

be undertaken by the auditor in this regards are mentioned below:

a. Sales: For checking on the sales revenue of the entity, the vouching of the sales

invoices needs to be done and it needs to be checked if the same is matching

with the sales ledger and books of accounts. The revenue recognition policy of

the company needs to be compared with the accounting standard and the

appropriateness of the same needs to be validated to check if the right to accrue

revenue has been established (Kangarluie & Aalizadeh, 2017).

b. Cost of Sales: The cost of sales has increased by a massive 9% on the sales base

increase of 1%. It needs to be checked if the management has recorded all the

expenses correctly and what is the accounting treatment of the cut off entries

being done in the books of accounts. Vouching of bills needs to be employed for

this.

c. Repair and Maintenance: The decline in repair and maintenance expenditure is

substantial and it needs to be checked if the management has taken the

provision entries in the books and has ensured completeness in recording of all

the period expenses. It also needs to be checked if the expenses has not been

capitalised in the balance sheet (Truong, et al., 2008).

d. Superannuation: The superannuation expenses have declined and therefore the

employee register needs to be checked to verify if the employee head count has

5

revenue recognition criteria has been met and the

right to recognise the revenue in books was

established (Erik & Jan, 2017).

2 Cost of Sales The cost of sales has increased by a massive 9% for

the sales increase of 1%. As a % of total receipts as

well, the same has increased from 26% to 28% and

therefore management assertion of accuracy in

recording the cost and appropriateness of the cut off

entries w.r.t. the cost needs to be checked (Belton,

2017).

3 Repair and

maintenance

The repair expenses has shown a sharp decline of

71% as compared to last year and even as

percentage of total receipts, it has fallen by 1.5%

and therefore it needs to be checked if the expenses

have been recorded completely and accrual and

matching concept has been taken into consideration

(Meroño-Cerdán, et al., 2017).

4 Superannuation These have had a decline of 25% as compared to last

year despite having the same sales. Therefore it

needs to be checked if employees has left or

resigned and if management assertion of

completeness in recording of expenses has been

met (Chron, 2017).

3.2. Audit procedures to be undertaken

For the accounts identified above in the analysis, some of the audit procedures to

be undertaken by the auditor in this regards are mentioned below:

a. Sales: For checking on the sales revenue of the entity, the vouching of the sales

invoices needs to be done and it needs to be checked if the same is matching

with the sales ledger and books of accounts. The revenue recognition policy of

the company needs to be compared with the accounting standard and the

appropriateness of the same needs to be validated to check if the right to accrue

revenue has been established (Kangarluie & Aalizadeh, 2017).

b. Cost of Sales: The cost of sales has increased by a massive 9% on the sales base

increase of 1%. It needs to be checked if the management has recorded all the

expenses correctly and what is the accounting treatment of the cut off entries

being done in the books of accounts. Vouching of bills needs to be employed for

this.

c. Repair and Maintenance: The decline in repair and maintenance expenditure is

substantial and it needs to be checked if the management has taken the

provision entries in the books and has ensured completeness in recording of all

the period expenses. It also needs to be checked if the expenses has not been

capitalised in the balance sheet (Truong, et al., 2008).

d. Superannuation: The superannuation expenses have declined and therefore the

employee register needs to be checked to verify if the employee head count has

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gone down or the company has changed the policy in respect of the

superannuation expenses. The auditor also needs to check if the company has

followed all the laws and regulations in place (Vieira, et al., 2017).

6

superannuation expenses. The auditor also needs to check if the company has

followed all the laws and regulations in place (Vieira, et al., 2017).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.Conclusion – Fraud Risk Analysis

The last section in the audit of the entity is the fraud risk analysis which is generally done to

check the possibility of fraud in the organization but in the given case, the partner of the

firm has suggested that the fraud risk analysis need not be done for the given client as the

client is trustworthy. But this is completely against the concept of professional scepticism

and the ethics for auditors as stated in APES 110 as per which the auditor should apply

professional judgement in such circumstances and check the client for FRF irrespective of

anything else (Fay & Negangard, 2017).

There are few accounts of the entity which hint towards the possibility of the fraud in the

organization. Some of such accounts are cost of sales and the repair and expenditure

account for the reasons which have already been explained above. Furthermore the wages

account and the superannuation account needs to be verified as there is a substantial

decline with decrease in the sales.

5.Recommendations

Few of the recommendations for the given client’s audit is:

The auditors should not only be emphasizing on the income statement accounts but

also be checking the balance sheet for further evidences.

The opening balance verification also needs to be done in case the auditor is new.

7

The last section in the audit of the entity is the fraud risk analysis which is generally done to

check the possibility of fraud in the organization but in the given case, the partner of the

firm has suggested that the fraud risk analysis need not be done for the given client as the

client is trustworthy. But this is completely against the concept of professional scepticism

and the ethics for auditors as stated in APES 110 as per which the auditor should apply

professional judgement in such circumstances and check the client for FRF irrespective of

anything else (Fay & Negangard, 2017).

There are few accounts of the entity which hint towards the possibility of the fraud in the

organization. Some of such accounts are cost of sales and the repair and expenditure

account for the reasons which have already been explained above. Furthermore the wages

account and the superannuation account needs to be verified as there is a substantial

decline with decrease in the sales.

5.Recommendations

Few of the recommendations for the given client’s audit is:

The auditors should not only be emphasizing on the income statement accounts but

also be checking the balance sheet for further evidences.

The opening balance verification also needs to be done in case the auditor is new.

7

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London:

Macat International ltd.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing:

Theory and Application, 20(1), pp. 7-51.

Chron, 2017. five-common-features-internal-control-system-business. [Online]

Available at: http://smallbusiness.chron.com/five-common-features-internal-control-system-

business-430.html

[Accessed 07 december 2017].

Erik, H. & Jan, B., 2017. Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), pp. 712-735.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Kangarluie, S. & Aalizadeh, A., 2017. 'The expectation gap in auditing. Accounting, 3(1), pp. 19-22.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Truong, G., Partington, G. & M, P., 2008. Cost of Capital Estimation and Capital Budgeting Practice in

Australia. Australian Journal of Management, 33(1), pp. 95-121.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1).

Willcocks, L. P. L. M. C. &. S. C., 2017. Introduction. In Outsourcing and Offshoring Business Services.

Cham: Palgrave Macmillan,.

8

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London:

Macat International ltd.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing:

Theory and Application, 20(1), pp. 7-51.

Chron, 2017. five-common-features-internal-control-system-business. [Online]

Available at: http://smallbusiness.chron.com/five-common-features-internal-control-system-

business-430.html

[Accessed 07 december 2017].

Erik, H. & Jan, B., 2017. Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), pp. 712-735.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Kangarluie, S. & Aalizadeh, A., 2017. 'The expectation gap in auditing. Accounting, 3(1), pp. 19-22.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Truong, G., Partington, G. & M, P., 2008. Cost of Capital Estimation and Capital Budgeting Practice in

Australia. Australian Journal of Management, 33(1), pp. 95-121.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1).

Willcocks, L. P. L. M. C. &. S. C., 2017. Introduction. In Outsourcing and Offshoring Business Services.

Cham: Palgrave Macmillan,.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.