UGB 238 Audit and Assurance 2020 Alternative Assessment Analysis

VerifiedAdded on 2022/02/19

|15

|5041

|14

Report

AI Summary

This comprehensive report analyzes an audit and assurance assessment, addressing key areas such as auditor independence, audit procedures, and the concept of objectivity. It examines various scenarios, including potential threats and safeguards, and describes the procedures auditors should undertake. The report further delves into potential indicators of a company's going concern issues, detailing the related audit procedures to assess these concerns and their impact on the auditor's report. Additionally, it explores audit risk and its components, identifying risks and the auditor's responses. The report also differentiates between interim and final audits, outlining relevant procedures and their impact. This analysis is critical for understanding the complexities of audit processes and the importance of financial statement accuracy.

UGB 238 Audit and Assurance 2020

Alternative Assessment 2020

Student Number:

Alternative Assessment 2020

Student Number:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1..................................................................................................................................3

(a) Matters Other Than Independence....................................................................................3

(b) Discussions of Situations in the Context of the Independence of the Auditor.................4

(c) Concept of Objectivity......................................................................................................4

Question 2..................................................................................................................................5

(a) Describing the procedures the auditors of John and Jane Co Should undertake..............5

(b) Explanation of SIX potential indicators that John and Jane Co is not going to concern. 5

(c) Description of audit procedures which one should consider to assess the concern of

John and Jane Co....................................................................................................................6

(d) Impact on the auditor’s report of John and Jane Co.........................................................7

Question 3..................................................................................................................................7

(a) Audit Risk and the Components of Audit Risk................................................................7

(b) Identification of Risks and Responses of the Auditor to those........................................9

(c) Identification of the Main Areas Other Than Audit Risks...............................................9

(d) Explanation of the Difference between an Interim and a Final Audit............................10

(e) Procedures to be performed during an Interim Audit of Peter and Its Impact on Final

Audit.....................................................................................................................................10

References................................................................................................................................12

Page | 2

Question 1..................................................................................................................................3

(a) Matters Other Than Independence....................................................................................3

(b) Discussions of Situations in the Context of the Independence of the Auditor.................4

(c) Concept of Objectivity......................................................................................................4

Question 2..................................................................................................................................5

(a) Describing the procedures the auditors of John and Jane Co Should undertake..............5

(b) Explanation of SIX potential indicators that John and Jane Co is not going to concern. 5

(c) Description of audit procedures which one should consider to assess the concern of

John and Jane Co....................................................................................................................6

(d) Impact on the auditor’s report of John and Jane Co.........................................................7

Question 3..................................................................................................................................7

(a) Audit Risk and the Components of Audit Risk................................................................7

(b) Identification of Risks and Responses of the Auditor to those........................................9

(c) Identification of the Main Areas Other Than Audit Risks...............................................9

(d) Explanation of the Difference between an Interim and a Final Audit............................10

(e) Procedures to be performed during an Interim Audit of Peter and Its Impact on Final

Audit.....................................................................................................................................10

References................................................................................................................................12

Page | 2

Question 1

(a) Matters Other Than Independence

Audit credibility requires the willingness of independent auditors to conduct their auditing

activities in a fair and critical manner. Public opinion on the value of audit quality is founded

not only on a statute that presumes audit independence but also on a consumer's view of

independent audit.

I. Commission of Audit:

To make the accountant completely unbiased, an auditor should include a specified

number, instead of supervision, for the accountants of the committee of employees of

the organisation whose main roles are to help auditors to stand entirely independent

(Alkasim, Agbi and Ahmed, 2019).

II. Audit business scale:

The scale of the auditing sector is an important consideration when choosing an outside

auditor. The accuracy of the report is based on the integrity of the auditor. The fastest

growing audit companies appear to be getting stronger analytical equipment, effective

accounting tools, more modern technologies and far more skilled practitioners

conducting big corporate audits, in comparison to larger accounting companies (Noor,

N.R.A.M. and Mansor, 2020). Even if large auditing companies have a broad client base

of clients that helps them to fulfil management’s requirements, smaller firms have

customised resources because they have limited portfolios of clients, and must

accommodate management’s expectations in a desired period.

III. Participate in auditor sector competition:

Competition was often thought to be an intrinsic market factor that determines how

autonomous auditors are. As the clients can reach other investigator’s services through

the telephonic call or mail or digital platforms, several companies cannot operate

independently in such competitive dynamo (Kend and Basioudis, 2018).

IV. Auditing company which meets the needs of a specific customer:

The concept of an audit firm includes the time needed to meet the auditing requirements

of a particular client. There will definitely be a long association with an organisation

and accountancy, making it difficult for the Impartial Auditor to undertake independent

intervention by tightly linking the company to the interests of its clients.

V. Scale and non-audit costs auditing:

Page | 3

(a) Matters Other Than Independence

Audit credibility requires the willingness of independent auditors to conduct their auditing

activities in a fair and critical manner. Public opinion on the value of audit quality is founded

not only on a statute that presumes audit independence but also on a consumer's view of

independent audit.

I. Commission of Audit:

To make the accountant completely unbiased, an auditor should include a specified

number, instead of supervision, for the accountants of the committee of employees of

the organisation whose main roles are to help auditors to stand entirely independent

(Alkasim, Agbi and Ahmed, 2019).

II. Audit business scale:

The scale of the auditing sector is an important consideration when choosing an outside

auditor. The accuracy of the report is based on the integrity of the auditor. The fastest

growing audit companies appear to be getting stronger analytical equipment, effective

accounting tools, more modern technologies and far more skilled practitioners

conducting big corporate audits, in comparison to larger accounting companies (Noor,

N.R.A.M. and Mansor, 2020). Even if large auditing companies have a broad client base

of clients that helps them to fulfil management’s requirements, smaller firms have

customised resources because they have limited portfolios of clients, and must

accommodate management’s expectations in a desired period.

III. Participate in auditor sector competition:

Competition was often thought to be an intrinsic market factor that determines how

autonomous auditors are. As the clients can reach other investigator’s services through

the telephonic call or mail or digital platforms, several companies cannot operate

independently in such competitive dynamo (Kend and Basioudis, 2018).

IV. Auditing company which meets the needs of a specific customer:

The concept of an audit firm includes the time needed to meet the auditing requirements

of a particular client. There will definitely be a long association with an organisation

and accountancy, making it difficult for the Impartial Auditor to undertake independent

intervention by tightly linking the company to the interests of its clients.

V. Scale and non-audit costs auditing:

Page | 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IFAC Ethical standards imply that the size of a custodian should challenge the

credibility of an audit as measured by the quantity of sum charged. In compliance with

transparent conditions, the accounting experts (auditors) tended to already be in

collaboration with the executive committee to continue to hide fraudulent practises

(Meuwissen and Quick, 2019). “A certain portion of the global audit scale is not

exceeded by the (total) consumer fee,” states EFAA.

(b) Discussions of Situations in the Context of the Independence of the Auditor

i) As seen in this case, the external auditor who owns shares in the business model is

inefficient and will affect the decision, even the accountant.

(ii) This case is subjective in nature but critical in such sense is that consumers are the

primary sources of income of the audit committee as the tax contribution is owed by

customers can vary from 700,000 to 100,000.

(iii) There is an income deficit of external auditor in this case because the accountant has

been loaned from the inspector's own fund.

(iv) In such a case, there is actually no accountant’s judgement needed, so the auditor is

required to give advice that there is no duty of him to monitor the autonomy and discretion of

the inspector.

(c) Concept of Objectivity

i) External Auditors

An auditing agency that controls, audits and conducts other market functions is an

international auditor (Lu, Simnett and Zhou, 2019). Audit committees that externally conduct

their audit function are self-employed by corporations in a way that impartially checks the

financial records and internal compliance procedures of those companies. This advice from

senior management is completely in accordance with consumers and creditors who want an

impartial review of account books.

ii) Internal Auditors

Internal audit becomes trained practitioners performing unbiased or independent financial

compliance assessments in accounting and corporate financial regulations. They are obliged

to ensure that corporations adhere with the regulations, comply with the appropriate

Page | 4

credibility of an audit as measured by the quantity of sum charged. In compliance with

transparent conditions, the accounting experts (auditors) tended to already be in

collaboration with the executive committee to continue to hide fraudulent practises

(Meuwissen and Quick, 2019). “A certain portion of the global audit scale is not

exceeded by the (total) consumer fee,” states EFAA.

(b) Discussions of Situations in the Context of the Independence of the Auditor

i) As seen in this case, the external auditor who owns shares in the business model is

inefficient and will affect the decision, even the accountant.

(ii) This case is subjective in nature but critical in such sense is that consumers are the

primary sources of income of the audit committee as the tax contribution is owed by

customers can vary from 700,000 to 100,000.

(iii) There is an income deficit of external auditor in this case because the accountant has

been loaned from the inspector's own fund.

(iv) In such a case, there is actually no accountant’s judgement needed, so the auditor is

required to give advice that there is no duty of him to monitor the autonomy and discretion of

the inspector.

(c) Concept of Objectivity

i) External Auditors

An auditing agency that controls, audits and conducts other market functions is an

international auditor (Lu, Simnett and Zhou, 2019). Audit committees that externally conduct

their audit function are self-employed by corporations in a way that impartially checks the

financial records and internal compliance procedures of those companies. This advice from

senior management is completely in accordance with consumers and creditors who want an

impartial review of account books.

ii) Internal Auditors

Internal audit becomes trained practitioners performing unbiased or independent financial

compliance assessments in accounting and corporate financial regulations. They are obliged

to ensure that corporations adhere with the regulations, comply with the appropriate

Page | 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

procedures and function as quickly as possible (Kend and Basioudis, 2018). Fair and

accountable information on the company should be given to an independent consultant.

(iii) Threats and Safeguards

Threats in Situation 1: There is a threat of personality, whether the inspector is expressly or

implicitly involved or depending on the customer for significant rewards. In this regard,

during the first case, there is a probability of personality since the accountant receives from

Bakers co. about 7 percent of his total profits.

Safeguard to Objectivity: This vulnerability can also be safeguarded by external

quality control systems or meetings with third parties or agencies. The auditor may

mitigate customer dependency.

Threats in Situation 2: There appears to be a risk of freedom in this case, as Peter is a

customer worker who now has to execute a company audit firm. It can, however, act as an

investigative contractor and it is not necessary to assess the degree of freedom for

independent inquiry.

Safeguarding to Objectivity: Peter should be assured of providing unbiased advice

and replacing an in-house auditor who may not have any personal disagreements with

the company’s personnel.

Question 2

(a) Describing the procedures, the auditors of John and Jane Co Should undertake

1. Evaluating the degree of materiality of the improper inventory deficiency in the financial

statements.

2. Since a revision of the loss inventory is a revision occurrence that demonstrates the

situation at the end of the year (30 April 2014). The auditor may instruct John and Jane Co to

note down the inventory if the misstatement is material. If the error is immaterial, the auditor

should instruct John and Jane Co to make the financial statements disclosures (Denisov,

Khachaturyan and Umnova, 2018).

3. Discuss the effect on the auditor report whether the uncorrected inventory misstatement is

not adjusted or disclosed in compliance with IAS 2 Inventories and IAS 10 Events during the

Page | 5

accountable information on the company should be given to an independent consultant.

(iii) Threats and Safeguards

Threats in Situation 1: There is a threat of personality, whether the inspector is expressly or

implicitly involved or depending on the customer for significant rewards. In this regard,

during the first case, there is a probability of personality since the accountant receives from

Bakers co. about 7 percent of his total profits.

Safeguard to Objectivity: This vulnerability can also be safeguarded by external

quality control systems or meetings with third parties or agencies. The auditor may

mitigate customer dependency.

Threats in Situation 2: There appears to be a risk of freedom in this case, as Peter is a

customer worker who now has to execute a company audit firm. It can, however, act as an

investigative contractor and it is not necessary to assess the degree of freedom for

independent inquiry.

Safeguarding to Objectivity: Peter should be assured of providing unbiased advice

and replacing an in-house auditor who may not have any personal disagreements with

the company’s personnel.

Question 2

(a) Describing the procedures, the auditors of John and Jane Co Should undertake

1. Evaluating the degree of materiality of the improper inventory deficiency in the financial

statements.

2. Since a revision of the loss inventory is a revision occurrence that demonstrates the

situation at the end of the year (30 April 2014). The auditor may instruct John and Jane Co to

note down the inventory if the misstatement is material. If the error is immaterial, the auditor

should instruct John and Jane Co to make the financial statements disclosures (Denisov,

Khachaturyan and Umnova, 2018).

3. Discuss the effect on the auditor report whether the uncorrected inventory misstatement is

not adjusted or disclosed in compliance with IAS 2 Inventories and IAS 10 Events during the

Page | 5

monitoring date with John and Jane Co management (Denisov, Khachaturyan and Umnova,

2018).

4. In order to ensure mathematically accurate/mathematical precision, the listing of the

inventory without correction/damages must be verified.

5. Review reports on the financial statements as of 30 April 2014 in order to verify that the

incorrect inventory mistake was correctly disclosed.

6. Preview the financial Statements for April 2014 and verify that the inventory of errors has

been excluded from the profit/loss statement.

7. Ask the administration for a written representation of the malfunction or error in the

inventory (Denisov, Khachaturyan and Umnova, 2018).

(b) Explanation of SIX potential indicators that John and Jane Co. is not going to

concern

1. A successful rival emerges named Drums. By means of aggressive pricing Drum acquired

substantial market share from John and Jane Co. There is the possibility in a substantial

reduction in potential sales and cash flow caused by a loss in market share.

2. Labour problems with well trained workers recruitment. A few developers from John and

Jane have quit the firm and entered Drums. Because of their experience and expertise, John

and Jane find it difficult to substitute these staff. Since the company of John and Jane Co is

led by specialists. There is a risk that the company would be unable to compete in the market

if the professional is not well substituted. John and Jane Co would therefore not be willing to

produce innovative innovations to distinguish the firm from its competitors (Ji, Lu and Qu,

2018).

3. The main supplier of John and Jane has stopped dealing with the company. This shows that

vital supplies are lacking. Unless alternative providers for supplying the specialized

equipment could be identified by John and Jane Co, the possibility exists that the firm cannot

produce products that could contribute to loss of tradability (Kahyaoglu and Caliyurt, 2018).

The new supplier would therefore pose risk by contracting providing the equipment at a

higher price and reducing potential cash flow.

4. The shareholders of John and Jane Co also refused to invest more in the company to

produce new products. This shows that John and Jane Co. have been unable to secure funding

Page | 6

2018).

4. In order to ensure mathematically accurate/mathematical precision, the listing of the

inventory without correction/damages must be verified.

5. Review reports on the financial statements as of 30 April 2014 in order to verify that the

incorrect inventory mistake was correctly disclosed.

6. Preview the financial Statements for April 2014 and verify that the inventory of errors has

been excluded from the profit/loss statement.

7. Ask the administration for a written representation of the malfunction or error in the

inventory (Denisov, Khachaturyan and Umnova, 2018).

(b) Explanation of SIX potential indicators that John and Jane Co. is not going to

concern

1. A successful rival emerges named Drums. By means of aggressive pricing Drum acquired

substantial market share from John and Jane Co. There is the possibility in a substantial

reduction in potential sales and cash flow caused by a loss in market share.

2. Labour problems with well trained workers recruitment. A few developers from John and

Jane have quit the firm and entered Drums. Because of their experience and expertise, John

and Jane find it difficult to substitute these staff. Since the company of John and Jane Co is

led by specialists. There is a risk that the company would be unable to compete in the market

if the professional is not well substituted. John and Jane Co would therefore not be willing to

produce innovative innovations to distinguish the firm from its competitors (Ji, Lu and Qu,

2018).

3. The main supplier of John and Jane has stopped dealing with the company. This shows that

vital supplies are lacking. Unless alternative providers for supplying the specialized

equipment could be identified by John and Jane Co, the possibility exists that the firm cannot

produce products that could contribute to loss of tradability (Kahyaoglu and Caliyurt, 2018).

The new supplier would therefore pose risk by contracting providing the equipment at a

higher price and reducing potential cash flow.

4. The shareholders of John and Jane Co also refused to invest more in the company to

produce new products. This shows that John and Jane Co. have been unable to secure funding

Page | 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to produce key new products or other important investments (Kahyaoglu and Caliyurt, 2018).

There is a possibility that because of financial problems, the company may have to postpone

or pause the schedule for developing new goods.

5. Over the course of the year, the overdraft of John and Jane Co has risen considerably and

will be renewed next month. This shows that the company was mostly dependent on the

overdraft (Kahyaoglu and Caliyurt, 2018). If the banking firm may not resume the overdraft

and the company may not secure substitute financing, it will not be possible for John and

Jane to begin trading.

6. The cash flow forecast for John and Jane reveals a considerably deteriorating position over

the next 12 months. This shows that the cash inflow of John and Jane Co to fund the

everyday costs will not be accessible. In addition, the company could have insufficient capital

to service its obligations and contribute to liquidation according to the Section X Companies

Act 2016 (Kahyaoglu and Caliyurt, 2018).

(c) Description of audit procedures which one should consider to assess the concern

of John and Jane Co.

1. Discuss and assess the corporate future management strategy. Discuss if the firm won any

new customers to offset the lost customer, with the financial officer.

2. Discuss and review Management plans for properly hiring expert developers to ensure

John and Jane Co's capacity to deliver new products in a competitive way (Martínez-Ferrero

and García-Sánchez, 2018). If the company's recruitment is ongoing, Review Board Meetings

of progress on hiring developers to substitute those left to Drum.

3. Discuss and assess the management plan to make the latest provider accessible. If there is

no other supplier on the market, the ongoing issue appraisal can be affected. If the

competition is open to other suppliers, check the offer from the latest supplier to evaluate the

rationality of John and Jane's cash flow to keep the price quoted (Martínez-Ferrero and

García-Sánchez, 2018).

4. Discuss and review management's proposed product growth alternate financing strategy.

Where the organization receives some alternative investment, check the meeting minutes for

evidence of fresh equity injections or new credit arrangement at the meeting of the Board

(Noor and Mansor, 2020). Examine the shareholder communications to see whether any

shareholders have shown an interest in increasing their stake.

Page | 7

There is a possibility that because of financial problems, the company may have to postpone

or pause the schedule for developing new goods.

5. Over the course of the year, the overdraft of John and Jane Co has risen considerably and

will be renewed next month. This shows that the company was mostly dependent on the

overdraft (Kahyaoglu and Caliyurt, 2018). If the banking firm may not resume the overdraft

and the company may not secure substitute financing, it will not be possible for John and

Jane to begin trading.

6. The cash flow forecast for John and Jane reveals a considerably deteriorating position over

the next 12 months. This shows that the cash inflow of John and Jane Co to fund the

everyday costs will not be accessible. In addition, the company could have insufficient capital

to service its obligations and contribute to liquidation according to the Section X Companies

Act 2016 (Kahyaoglu and Caliyurt, 2018).

(c) Description of audit procedures which one should consider to assess the concern

of John and Jane Co.

1. Discuss and assess the corporate future management strategy. Discuss if the firm won any

new customers to offset the lost customer, with the financial officer.

2. Discuss and review Management plans for properly hiring expert developers to ensure

John and Jane Co's capacity to deliver new products in a competitive way (Martínez-Ferrero

and García-Sánchez, 2018). If the company's recruitment is ongoing, Review Board Meetings

of progress on hiring developers to substitute those left to Drum.

3. Discuss and assess the management plan to make the latest provider accessible. If there is

no other supplier on the market, the ongoing issue appraisal can be affected. If the

competition is open to other suppliers, check the offer from the latest supplier to evaluate the

rationality of John and Jane's cash flow to keep the price quoted (Martínez-Ferrero and

García-Sánchez, 2018).

4. Discuss and review management's proposed product growth alternate financing strategy.

Where the organization receives some alternative investment, check the meeting minutes for

evidence of fresh equity injections or new credit arrangement at the meeting of the Board

(Noor and Mansor, 2020). Examine the shareholder communications to see whether any

shareholders have shown an interest in increasing their stake.

Page | 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Examine overdraft arrangements to see if any covenants have been broken, and examine

communications with the bank to see if the overdraft service can be renewed.

6. Get the cash balance estimate from John and Jane and check in and out of cash flows.

Evaluate the presumption of rationality and analyze the results with management to

understand whether there are enough cash flows for the business.

(d) Impact on the auditor’s report of John and Jane Co

1. If the auditor knows the material uncertainties of events or conditions that might give

significant doubts about the ability of the entity to continue as an ongoing concern, the

financial statements shall make those uncertainties known. “Material uncertainty related to

going concern paragraph” (Shalimova and Androshchuk, 2018). The opinion of the auditor

relies on the effectiveness of the management's disclosure.

2. The auditor's report would remain unchanged and unskilled if the disclosures provided by

management are satisfactory. Following the paragraph Basic of Opinion, material uncertainty

relating to the subject matter would be addressed (Shalimova and Androshchuk, 2018).

3. Whether there is not enough transparency, the auditor's report may be changed, unless

there is a material error. This would be either a competent or an adverse opinion, depending

on the materiality of the issue.

4. In relation to current concerns, the reports in the financial statements shall be defined as

material uncertainty. It explains that material uncertainty exists, the existence of uncertainty

is defined and the management refers to the disclosure notice. It would come after the

paragraphs on the opinion and the basis for the opinion.

Question 3

(a) Audit Risk and the Components of Audit Risk

The risk of audit risk is that if the financial statement is substantially misstated the auditor

holds an incorrect audit opinion. The probability of audit often depends on the chances of

content mistakes and the risk of identification.

Audit risk consists of three elements. They consist of “Inherent risk” “Control risk” and

“Detection risk” (Shalimova and Androshchuk, 2018).

Page | 8

communications with the bank to see if the overdraft service can be renewed.

6. Get the cash balance estimate from John and Jane and check in and out of cash flows.

Evaluate the presumption of rationality and analyze the results with management to

understand whether there are enough cash flows for the business.

(d) Impact on the auditor’s report of John and Jane Co

1. If the auditor knows the material uncertainties of events or conditions that might give

significant doubts about the ability of the entity to continue as an ongoing concern, the

financial statements shall make those uncertainties known. “Material uncertainty related to

going concern paragraph” (Shalimova and Androshchuk, 2018). The opinion of the auditor

relies on the effectiveness of the management's disclosure.

2. The auditor's report would remain unchanged and unskilled if the disclosures provided by

management are satisfactory. Following the paragraph Basic of Opinion, material uncertainty

relating to the subject matter would be addressed (Shalimova and Androshchuk, 2018).

3. Whether there is not enough transparency, the auditor's report may be changed, unless

there is a material error. This would be either a competent or an adverse opinion, depending

on the materiality of the issue.

4. In relation to current concerns, the reports in the financial statements shall be defined as

material uncertainty. It explains that material uncertainty exists, the existence of uncertainty

is defined and the management refers to the disclosure notice. It would come after the

paragraphs on the opinion and the basis for the opinion.

Question 3

(a) Audit Risk and the Components of Audit Risk

The risk of audit risk is that if the financial statement is substantially misstated the auditor

holds an incorrect audit opinion. The probability of audit often depends on the chances of

content mistakes and the risk of identification.

Audit risk consists of three elements. They consist of “Inherent risk” “Control risk” and

“Detection risk” (Shalimova and Androshchuk, 2018).

Page | 8

The inherent risk is the vulnerability, either separately or in combination with other mistakes,

of assumptions regarding a class of transactions, account balance or declaration of a

misstatement prior to consideration of any associated controls (Shalimova and Androshchuk,

2018).

Control risk is a possibility of not preventing, detecting and correcting an abnormality in a

claim regarding a class of transaction, balance or declaration and it may be information either

separately or when combined with other abnormalities in a timely manner by the internal

control of an entity (Shalimova and Androshchuk, 2018).

Detection risks are the possibility that an error that occurs which may be material, whether

internally or when combined with more abuse is detected in the auditor's procedures for

reducing an audit risk to an acceptably low amount.

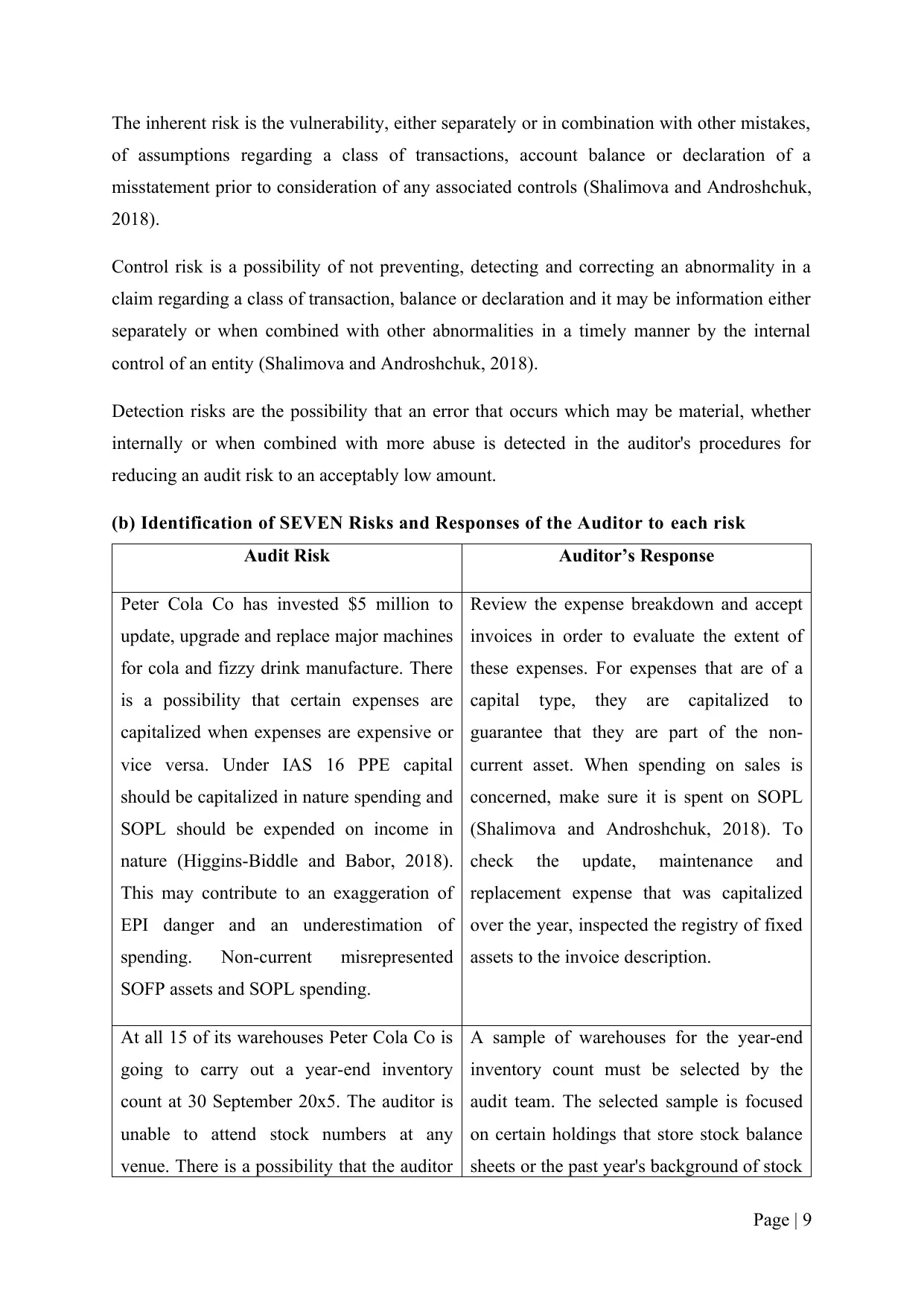

(b) Identification of SEVEN Risks and Responses of the Auditor to each risk

Audit Risk Auditor’s Response

Peter Cola Co has invested $5 million to

update, upgrade and replace major machines

for cola and fizzy drink manufacture. There

is a possibility that certain expenses are

capitalized when expenses are expensive or

vice versa. Under IAS 16 PPE capital

should be capitalized in nature spending and

SOPL should be expended on income in

nature (Higgins-Biddle and Babor, 2018).

This may contribute to an exaggeration of

EPI danger and an underestimation of

spending. Non-current misrepresented

SOFP assets and SOPL spending.

Review the expense breakdown and accept

invoices in order to evaluate the extent of

these expenses. For expenses that are of a

capital type, they are capitalized to

guarantee that they are part of the non-

current asset. When spending on sales is

concerned, make sure it is spent on SOPL

(Shalimova and Androshchuk, 2018). To

check the update, maintenance and

replacement expense that was capitalized

over the year, inspected the registry of fixed

assets to the invoice description.

At all 15 of its warehouses Peter Cola Co is

going to carry out a year-end inventory

count at 30 September 20x5. The auditor is

unable to attend stock numbers at any

venue. There is a possibility that the auditor

A sample of warehouses for the year-end

inventory count must be selected by the

audit team. The selected sample is focused

on certain holdings that store stock balance

sheets or the past year's background of stock

Page | 9

of assumptions regarding a class of transactions, account balance or declaration of a

misstatement prior to consideration of any associated controls (Shalimova and Androshchuk,

2018).

Control risk is a possibility of not preventing, detecting and correcting an abnormality in a

claim regarding a class of transaction, balance or declaration and it may be information either

separately or when combined with other abnormalities in a timely manner by the internal

control of an entity (Shalimova and Androshchuk, 2018).

Detection risks are the possibility that an error that occurs which may be material, whether

internally or when combined with more abuse is detected in the auditor's procedures for

reducing an audit risk to an acceptably low amount.

(b) Identification of SEVEN Risks and Responses of the Auditor to each risk

Audit Risk Auditor’s Response

Peter Cola Co has invested $5 million to

update, upgrade and replace major machines

for cola and fizzy drink manufacture. There

is a possibility that certain expenses are

capitalized when expenses are expensive or

vice versa. Under IAS 16 PPE capital

should be capitalized in nature spending and

SOPL should be expended on income in

nature (Higgins-Biddle and Babor, 2018).

This may contribute to an exaggeration of

EPI danger and an underestimation of

spending. Non-current misrepresented

SOFP assets and SOPL spending.

Review the expense breakdown and accept

invoices in order to evaluate the extent of

these expenses. For expenses that are of a

capital type, they are capitalized to

guarantee that they are part of the non-

current asset. When spending on sales is

concerned, make sure it is spent on SOPL

(Shalimova and Androshchuk, 2018). To

check the update, maintenance and

replacement expense that was capitalized

over the year, inspected the registry of fixed

assets to the invoice description.

At all 15 of its warehouses Peter Cola Co is

going to carry out a year-end inventory

count at 30 September 20x5. The auditor is

unable to attend stock numbers at any

venue. There is a possibility that the auditor

A sample of warehouses for the year-end

inventory count must be selected by the

audit team. The selected sample is focused

on certain holdings that store stock balance

sheets or the past year's background of stock

Page | 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will not be able to provide adequate and

adequate proof of internal management

exercise and efficacy in the count (Tang and

Karim, 2019). The inventory could be

misunderstood. Both stock numbers, if not,

are precise.

figures (Tang and Karim, 2019).

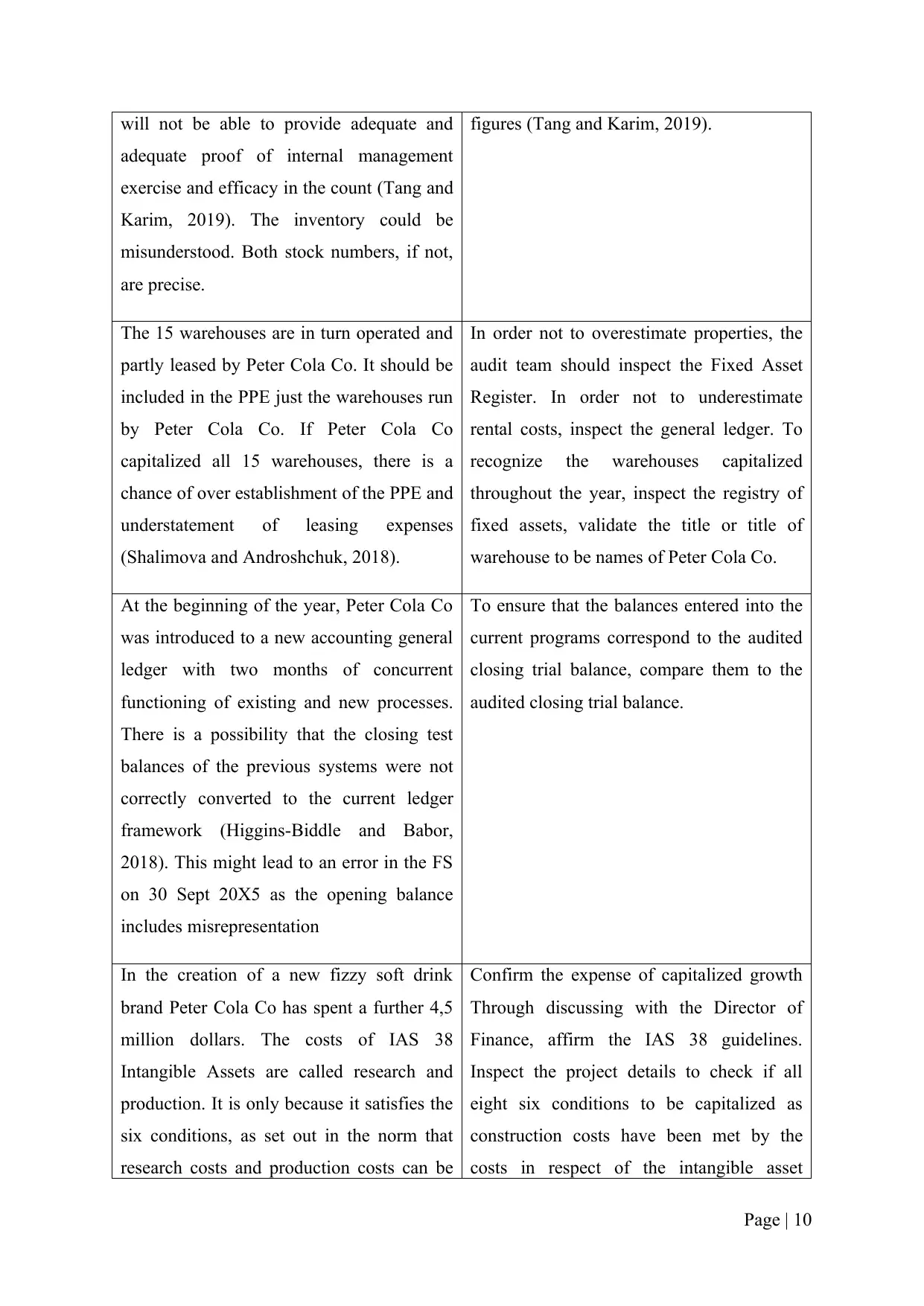

The 15 warehouses are in turn operated and

partly leased by Peter Cola Co. It should be

included in the PPE just the warehouses run

by Peter Cola Co. If Peter Cola Co

capitalized all 15 warehouses, there is a

chance of over establishment of the PPE and

understatement of leasing expenses

(Shalimova and Androshchuk, 2018).

In order not to overestimate properties, the

audit team should inspect the Fixed Asset

Register. In order not to underestimate

rental costs, inspect the general ledger. To

recognize the warehouses capitalized

throughout the year, inspect the registry of

fixed assets, validate the title or title of

warehouse to be names of Peter Cola Co.

At the beginning of the year, Peter Cola Co

was introduced to a new accounting general

ledger with two months of concurrent

functioning of existing and new processes.

There is a possibility that the closing test

balances of the previous systems were not

correctly converted to the current ledger

framework (Higgins-Biddle and Babor,

2018). This might lead to an error in the FS

on 30 Sept 20X5 as the opening balance

includes misrepresentation

To ensure that the balances entered into the

current programs correspond to the audited

closing trial balance, compare them to the

audited closing trial balance.

In the creation of a new fizzy soft drink

brand Peter Cola Co has spent a further 4,5

million dollars. The costs of IAS 38

Intangible Assets are called research and

production. It is only because it satisfies the

six conditions, as set out in the norm that

research costs and production costs can be

Confirm the expense of capitalized growth

Through discussing with the Director of

Finance, affirm the IAS 38 guidelines.

Inspect the project details to check if all

eight six conditions to be capitalized as

construction costs have been met by the

costs in respect of the intangible asset

Page | 10

adequate proof of internal management

exercise and efficacy in the count (Tang and

Karim, 2019). The inventory could be

misunderstood. Both stock numbers, if not,

are precise.

figures (Tang and Karim, 2019).

The 15 warehouses are in turn operated and

partly leased by Peter Cola Co. It should be

included in the PPE just the warehouses run

by Peter Cola Co. If Peter Cola Co

capitalized all 15 warehouses, there is a

chance of over establishment of the PPE and

understatement of leasing expenses

(Shalimova and Androshchuk, 2018).

In order not to overestimate properties, the

audit team should inspect the Fixed Asset

Register. In order not to underestimate

rental costs, inspect the general ledger. To

recognize the warehouses capitalized

throughout the year, inspect the registry of

fixed assets, validate the title or title of

warehouse to be names of Peter Cola Co.

At the beginning of the year, Peter Cola Co

was introduced to a new accounting general

ledger with two months of concurrent

functioning of existing and new processes.

There is a possibility that the closing test

balances of the previous systems were not

correctly converted to the current ledger

framework (Higgins-Biddle and Babor,

2018). This might lead to an error in the FS

on 30 Sept 20X5 as the opening balance

includes misrepresentation

To ensure that the balances entered into the

current programs correspond to the audited

closing trial balance, compare them to the

audited closing trial balance.

In the creation of a new fizzy soft drink

brand Peter Cola Co has spent a further 4,5

million dollars. The costs of IAS 38

Intangible Assets are called research and

production. It is only because it satisfies the

six conditions, as set out in the norm that

research costs and production costs can be

Confirm the expense of capitalized growth

Through discussing with the Director of

Finance, affirm the IAS 38 guidelines.

Inspect the project details to check if all

eight six conditions to be capitalized as

construction costs have been met by the

costs in respect of the intangible asset

Page | 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capitalized. The possibility exists that Peter

Cola Co will mis-capitalize the $4.5 million

as intangible asset that will overstate and

underestimate immaterial assets.

(Higgins-Biddle and Babor, 2018). discuss

the 4.5 thousand cost of production with the

Finance Director for clarification and

review the full breakdown of capitalized

development costs to ensure compliance

with definition from the Director

Peter Cola Co's finance manager has

published the opening benefit because he

believes that the allowance must not be

constantly maintained. There is a chance of

overvaluing trade claims. Since a new credit

controller is hired, Peter Cola Co will not be

able to exclude any debtors (Carcello et al.,

2020). Therefore, the provision for

receivables is overvalued if not supplied.

Examine the reasonableness of the

management payment allowance. Check the

accounts for receivable ageing to determine

any remaining balance and to do the cash

receipt examination during year end to

validate the balance that has been collected

after year end. If no, the director suggests

giving the debt credit. their achievement and

the requirement for a receivable’s deduction

(Carcello et al., 2020).

The combining of raw materials during

processing in April was problematic,

leading to a separate catching of a huge

selection of cola goods. The risk of faulty

inventory because of the mixing method

issue would not be deleted from the

inventory closed at year-end. This would

lead to overestimation of inventories and not

lower NRV and expense (Christensen,

Newton and Wilkins, 2020). This leads to a

failure of IAS 2 inventories to comply.

Ask the management why the value of the

affected stock has not been adjusted.

Consider, through administrators, whether

to write or write down and determine the

reasonability by checking the inventory plan

with the appropriate supporting text, the

number of affected inventories. Suggest that

the Finance Manager impair or enter the

NRV warehouse. Explain the effects of non-

adjustment in the auditor's view where the

financial officer refuses.

(c) Identification of the Main Areas Other Than Audit Risks

The main areas other than audit risks are varied, which should be included in the audit

strategy document for Peter Cola Co, in the following evaluation of these areas are

contextualized followed by relevant examples:

Page | 11

Cola Co will mis-capitalize the $4.5 million

as intangible asset that will overstate and

underestimate immaterial assets.

(Higgins-Biddle and Babor, 2018). discuss

the 4.5 thousand cost of production with the

Finance Director for clarification and

review the full breakdown of capitalized

development costs to ensure compliance

with definition from the Director

Peter Cola Co's finance manager has

published the opening benefit because he

believes that the allowance must not be

constantly maintained. There is a chance of

overvaluing trade claims. Since a new credit

controller is hired, Peter Cola Co will not be

able to exclude any debtors (Carcello et al.,

2020). Therefore, the provision for

receivables is overvalued if not supplied.

Examine the reasonableness of the

management payment allowance. Check the

accounts for receivable ageing to determine

any remaining balance and to do the cash

receipt examination during year end to

validate the balance that has been collected

after year end. If no, the director suggests

giving the debt credit. their achievement and

the requirement for a receivable’s deduction

(Carcello et al., 2020).

The combining of raw materials during

processing in April was problematic,

leading to a separate catching of a huge

selection of cola goods. The risk of faulty

inventory because of the mixing method

issue would not be deleted from the

inventory closed at year-end. This would

lead to overestimation of inventories and not

lower NRV and expense (Christensen,

Newton and Wilkins, 2020). This leads to a

failure of IAS 2 inventories to comply.

Ask the management why the value of the

affected stock has not been adjusted.

Consider, through administrators, whether

to write or write down and determine the

reasonability by checking the inventory plan

with the appropriate supporting text, the

number of affected inventories. Suggest that

the Finance Manager impair or enter the

NRV warehouse. Explain the effects of non-

adjustment in the auditor's view where the

financial officer refuses.

(c) Identification of the Main Areas Other Than Audit Risks

The main areas other than audit risks are varied, which should be included in the audit

strategy document for Peter Cola Co, in the following evaluation of these areas are

contextualized followed by relevant examples:

Page | 11

The audit strategy should describe the interaction characteristics (Grosse, Ma and

Scott, 2018). For example, the auditor should define the nature of the corporate

segments of Peter Cola Co and the financial reporting system of Peter Cola Co.

The audit strategy should cover reporting goals, audit scheduling and communications

nature. For example, if consultations with the management of Peter Cola Co and with

others responsible for governance should be held in relation to audit reporting before

dissemination.

The audit strategies should cover the design, pacing and extent of the audit resources

(Lu, Simnett and Zhou, 2019). A range of auditors with common skills and business

experiences as Peter Cola Co for engagement, for example.

The audit strategy should involve key considerations, preliminary collaboration

activities and other commitments. For instance, the number of transactions that will

help to assess Peter Cola Co's audit procedures.

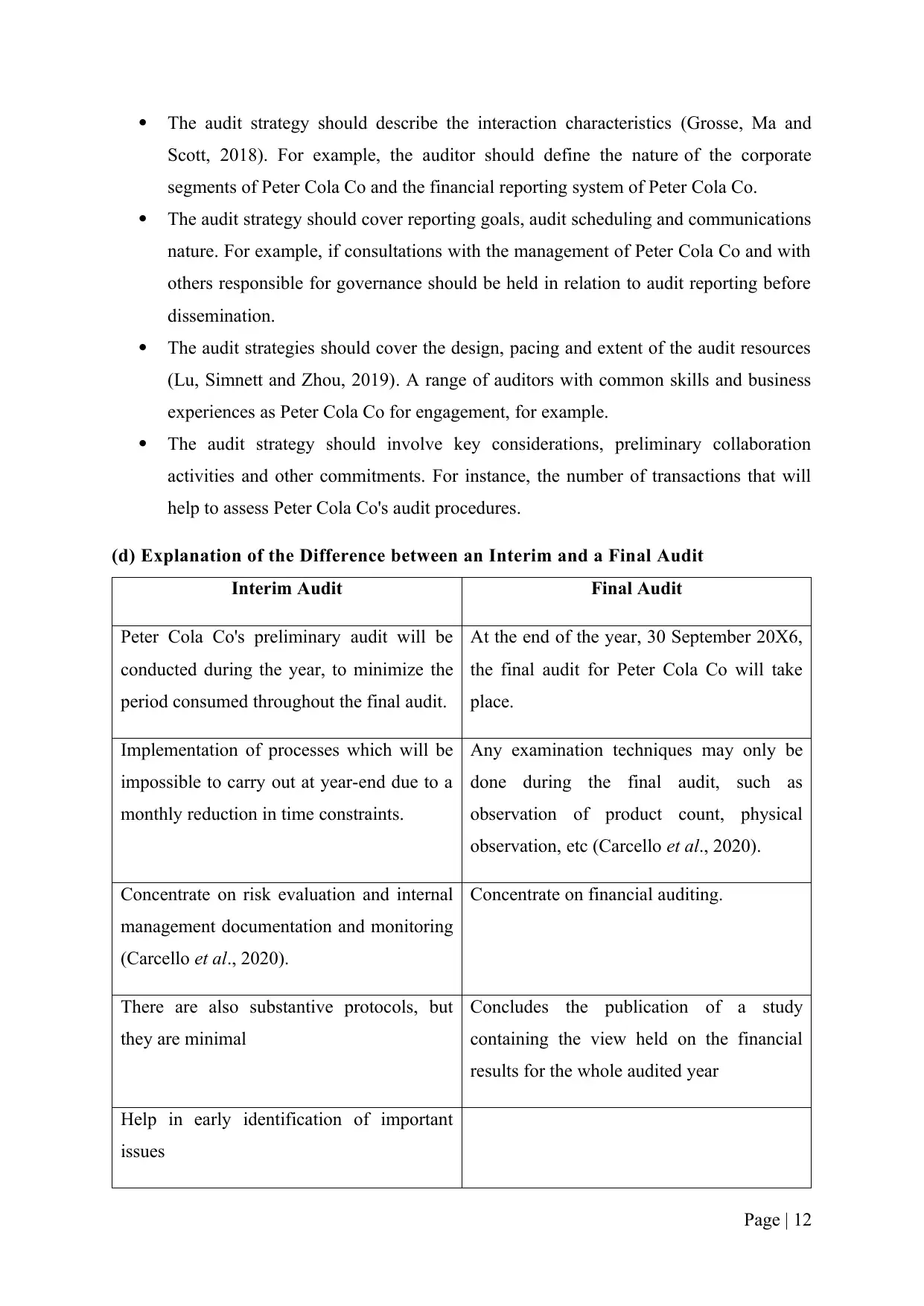

(d) Explanation of the Difference between an Interim and a Final Audit

Interim Audit Final Audit

Peter Cola Co's preliminary audit will be

conducted during the year, to minimize the

period consumed throughout the final audit.

At the end of the year, 30 September 20X6,

the final audit for Peter Cola Co will take

place.

Implementation of processes which will be

impossible to carry out at year-end due to a

monthly reduction in time constraints.

Any examination techniques may only be

done during the final audit, such as

observation of product count, physical

observation, etc (Carcello et al., 2020).

Concentrate on risk evaluation and internal

management documentation and monitoring

(Carcello et al., 2020).

Concentrate on financial auditing.

There are also substantive protocols, but

they are minimal

Concludes the publication of a study

containing the view held on the financial

results for the whole audited year

Help in early identification of important

issues

Page | 12

Scott, 2018). For example, the auditor should define the nature of the corporate

segments of Peter Cola Co and the financial reporting system of Peter Cola Co.

The audit strategy should cover reporting goals, audit scheduling and communications

nature. For example, if consultations with the management of Peter Cola Co and with

others responsible for governance should be held in relation to audit reporting before

dissemination.

The audit strategies should cover the design, pacing and extent of the audit resources

(Lu, Simnett and Zhou, 2019). A range of auditors with common skills and business

experiences as Peter Cola Co for engagement, for example.

The audit strategy should involve key considerations, preliminary collaboration

activities and other commitments. For instance, the number of transactions that will

help to assess Peter Cola Co's audit procedures.

(d) Explanation of the Difference between an Interim and a Final Audit

Interim Audit Final Audit

Peter Cola Co's preliminary audit will be

conducted during the year, to minimize the

period consumed throughout the final audit.

At the end of the year, 30 September 20X6,

the final audit for Peter Cola Co will take

place.

Implementation of processes which will be

impossible to carry out at year-end due to a

monthly reduction in time constraints.

Any examination techniques may only be

done during the final audit, such as

observation of product count, physical

observation, etc (Carcello et al., 2020).

Concentrate on risk evaluation and internal

management documentation and monitoring

(Carcello et al., 2020).

Concentrate on financial auditing.

There are also substantive protocols, but

they are minimal

Concludes the publication of a study

containing the view held on the financial

results for the whole audited year

Help in early identification of important

issues

Page | 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.