ACCT20075: Audit and Ethics Report on Flight Centre Travel Group

VerifiedAdded on 2022/10/02

|12

|2680

|474

Report

AI Summary

This report presents an audit and ethics analysis of Flight Centre Travel Group's 2018 annual report, focusing on materiality, audit procedures, and financial statement analysis. The report examines the concept of materiality, assessing its application and impact on the financial statements. It reviews key disclosures, including dividends, business combinations, and post-balance sheet events. The analysis extends to the application of analytical procedures, using ratio analysis to evaluate the company's performance and identify potential misstatements. Furthermore, the report analyzes the cash flow statement, highlighting the inflow and outflow of cash from operating, investing, and financing activities. The report also reviews the audit report, summarizing the auditor's opinion and key audit matters. The report concludes that the financial statements present a true and fair view of the company's financial position and performance.

Running head: AUDIT AND ETHICS

Audit and Ethics

Name of the Student

Name of the University

Author Note

Audit and Ethics

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT AND ETHICS

Table of Contents

Section: 1....................................................................................................................................2

Concept of Materiality and Scope for Audit..........................................................................2

Review of Draft and Disclosures...........................................................................................3

Section: 2....................................................................................................................................5

Application to Analytical Procedure......................................................................................5

Section: 3....................................................................................................................................8

Analysis of Cash Flow Statement..........................................................................................8

Review of Audit Report.............................................................................................................9

References................................................................................................................................10

Table of Contents

Section: 1....................................................................................................................................2

Concept of Materiality and Scope for Audit..........................................................................2

Review of Draft and Disclosures...........................................................................................3

Section: 2....................................................................................................................................5

Application to Analytical Procedure......................................................................................5

Section: 3....................................................................................................................................8

Analysis of Cash Flow Statement..........................................................................................8

Review of Audit Report.............................................................................................................9

References................................................................................................................................10

2AUDIT AND ETHICS

Section: 1

Concept of Materiality and Scope for Audit

The aim of making this report is to assessing the business through its annual report. It

focuses mainly on the concept of materiality been used and assessed in the business. The

company here chosen for making this audit report is Flight Centre Travel Group. The study of

financial report of the company has critically analyzed to check any material misstatement

reported or not in the financial statement. It is very necessary for the auditor to go through the

material misstatement if any, by the company to take a proper decision against it. If the

auditors sight of such statement then he/she is liable to collect evidences for the same while

going through a specific procedure for it. This report has considered the disclosed items in the

annual report of 2018 of the company Flight Centre Travel Group (FCTG) that is one of the

world’s largest travel agency group, providing travels services in Australia (Flight Centre

Travel Group, 2019).

It becomes one of the most important for the auditors to audit Materiality. The

concept of materiality results in misstatements when the company’s financial statements

includes any omission or irrelevant data that affect the economic decisions of the users Lai,

Melloni & Stacchezzini, 2017). The materiality concept considers both quantitative as well as

qualitative aspect. This concept helps the auditors to determine a true and fair view of the

data provided by the company (Legoria, Melendrez & Reynolds, 2013). The auditor while

assessing the statement of the company has to keep in mind to thoroughly investigate each

items mentioned in the company’s annual report. The first step taken by the auditors is in

quantitative aspect to set a preliminary judgment that includes the planning stage of audit and

a thumb rule to check either the normalized net income or total assets. The planning

materiality considers the highest value mentioned in the total assets of the company in its

Section: 1

Concept of Materiality and Scope for Audit

The aim of making this report is to assessing the business through its annual report. It

focuses mainly on the concept of materiality been used and assessed in the business. The

company here chosen for making this audit report is Flight Centre Travel Group. The study of

financial report of the company has critically analyzed to check any material misstatement

reported or not in the financial statement. It is very necessary for the auditor to go through the

material misstatement if any, by the company to take a proper decision against it. If the

auditors sight of such statement then he/she is liable to collect evidences for the same while

going through a specific procedure for it. This report has considered the disclosed items in the

annual report of 2018 of the company Flight Centre Travel Group (FCTG) that is one of the

world’s largest travel agency group, providing travels services in Australia (Flight Centre

Travel Group, 2019).

It becomes one of the most important for the auditors to audit Materiality. The

concept of materiality results in misstatements when the company’s financial statements

includes any omission or irrelevant data that affect the economic decisions of the users Lai,

Melloni & Stacchezzini, 2017). The materiality concept considers both quantitative as well as

qualitative aspect. This concept helps the auditors to determine a true and fair view of the

data provided by the company (Legoria, Melendrez & Reynolds, 2013). The auditor while

assessing the statement of the company has to keep in mind to thoroughly investigate each

items mentioned in the company’s annual report. The first step taken by the auditors is in

quantitative aspect to set a preliminary judgment that includes the planning stage of audit and

a thumb rule to check either the normalized net income or total assets. The planning

materiality considers the highest value mentioned in the total assets of the company in its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT AND ETHICS

annual report (Eilifsen & Messier, 2014). Planning materiality is to be computed for the year

2018 on the total asset estimated of the company has shown as $3,405,219,000. It has

represented in the equation as shown below:

Planning materiality=Total Assets∗5 %

¿ $ 3,405,219,000∗5 %

= $ 170,260,950

The above computation results the planning materiality of the business. The

performance materiality of the items shown in the annual report is based on this resulted

planning materiality of $ 170,260,950 only. The above figure used by the auditor to find any

misstatement in materiality stated by the company in their report to take a proper decision

against this matter.

Review of Draft and Disclosures

The annual report of the business shows the drafts and disclosures in the section of

notes to account. The notes of account section contains the relevant treatment that have some

impact on point of materiality. Therefore, the auditor needs to go through this section to find

any misstated figures to the concept of materiality to give a fair view on it (Simnett &

Huggins, 2015). Some significant items that are included in the notes to accounting section

has discussed below accordingly:

Dividends

The financial statement of the Flight Centre Group Ltd. shows that the company has

paid significant dividends during this period (Flight Centre Travel Group, 2019). The

management has considered several factors from the section of notes to accounts to determine

dividend returns to the shareholders of the company. The factors that the management

annual report (Eilifsen & Messier, 2014). Planning materiality is to be computed for the year

2018 on the total asset estimated of the company has shown as $3,405,219,000. It has

represented in the equation as shown below:

Planning materiality=Total Assets∗5 %

¿ $ 3,405,219,000∗5 %

= $ 170,260,950

The above computation results the planning materiality of the business. The

performance materiality of the items shown in the annual report is based on this resulted

planning materiality of $ 170,260,950 only. The above figure used by the auditor to find any

misstatement in materiality stated by the company in their report to take a proper decision

against this matter.

Review of Draft and Disclosures

The annual report of the business shows the drafts and disclosures in the section of

notes to account. The notes of account section contains the relevant treatment that have some

impact on point of materiality. Therefore, the auditor needs to go through this section to find

any misstated figures to the concept of materiality to give a fair view on it (Simnett &

Huggins, 2015). Some significant items that are included in the notes to accounting section

has discussed below accordingly:

Dividends

The financial statement of the Flight Centre Group Ltd. shows that the company has

paid significant dividends during this period (Flight Centre Travel Group, 2019). The

management has considered several factors from the section of notes to accounts to determine

dividend returns to the shareholders of the company. The factors that the management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT AND ETHICS

considered includes the anticipated cash requirement so that can help in fund for the growth,

operational plan and future economic conditions. The auditor has to process the substantive

procedure to ascertain the data related to dividends whether the company has accurately

represented or not in their annual report.

Business Combinations

The business combination shows the numerous acquisitions that has made by the

company during the period. It suggests that the item is material. The company has gone with

different acquisitions during the period for which the management of the company has

included all these acquisitions in their report. Therefore, the auditor needs to check all the

figures of the assets of the company whether it has mentioned correctly or not in the annual

report of the company. Further, the management needs to state the purchase consideration

that has paid for the acquisition are accurately shown or not in the annual report of the

business. The auditor has to check both the aspect so that a nature of transparency can

maintain for all in order to take a fruitful decision (Yusoff, Othman & Yatim, (2013).

Events occurs after date of Balance Sheet

It happens sometime that some events in the business occurs after maintaining the

balance sheet but the same also needs to be mention in the financial statement the business

made (Al Nawaiseh & Jaber, 2015). The annual report of this business shows that there is an

acquisition, which has made after the reporting period but the same, has to add in the

financial statement of the company relating to the relevant accounting standard. The auditor

has to check whether it has mentioned in the statements or not.

considered includes the anticipated cash requirement so that can help in fund for the growth,

operational plan and future economic conditions. The auditor has to process the substantive

procedure to ascertain the data related to dividends whether the company has accurately

represented or not in their annual report.

Business Combinations

The business combination shows the numerous acquisitions that has made by the

company during the period. It suggests that the item is material. The company has gone with

different acquisitions during the period for which the management of the company has

included all these acquisitions in their report. Therefore, the auditor needs to check all the

figures of the assets of the company whether it has mentioned correctly or not in the annual

report of the company. Further, the management needs to state the purchase consideration

that has paid for the acquisition are accurately shown or not in the annual report of the

business. The auditor has to check both the aspect so that a nature of transparency can

maintain for all in order to take a fruitful decision (Yusoff, Othman & Yatim, (2013).

Events occurs after date of Balance Sheet

It happens sometime that some events in the business occurs after maintaining the

balance sheet but the same also needs to be mention in the financial statement the business

made (Al Nawaiseh & Jaber, 2015). The annual report of this business shows that there is an

acquisition, which has made after the reporting period but the same, has to add in the

financial statement of the company relating to the relevant accounting standard. The auditor

has to check whether it has mentioned in the statements or not.

5AUDIT AND ETHICS

Section: 2

Application to Analytical Procedure

Section: 2

Application to Analytical Procedure

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT AND ETHICS

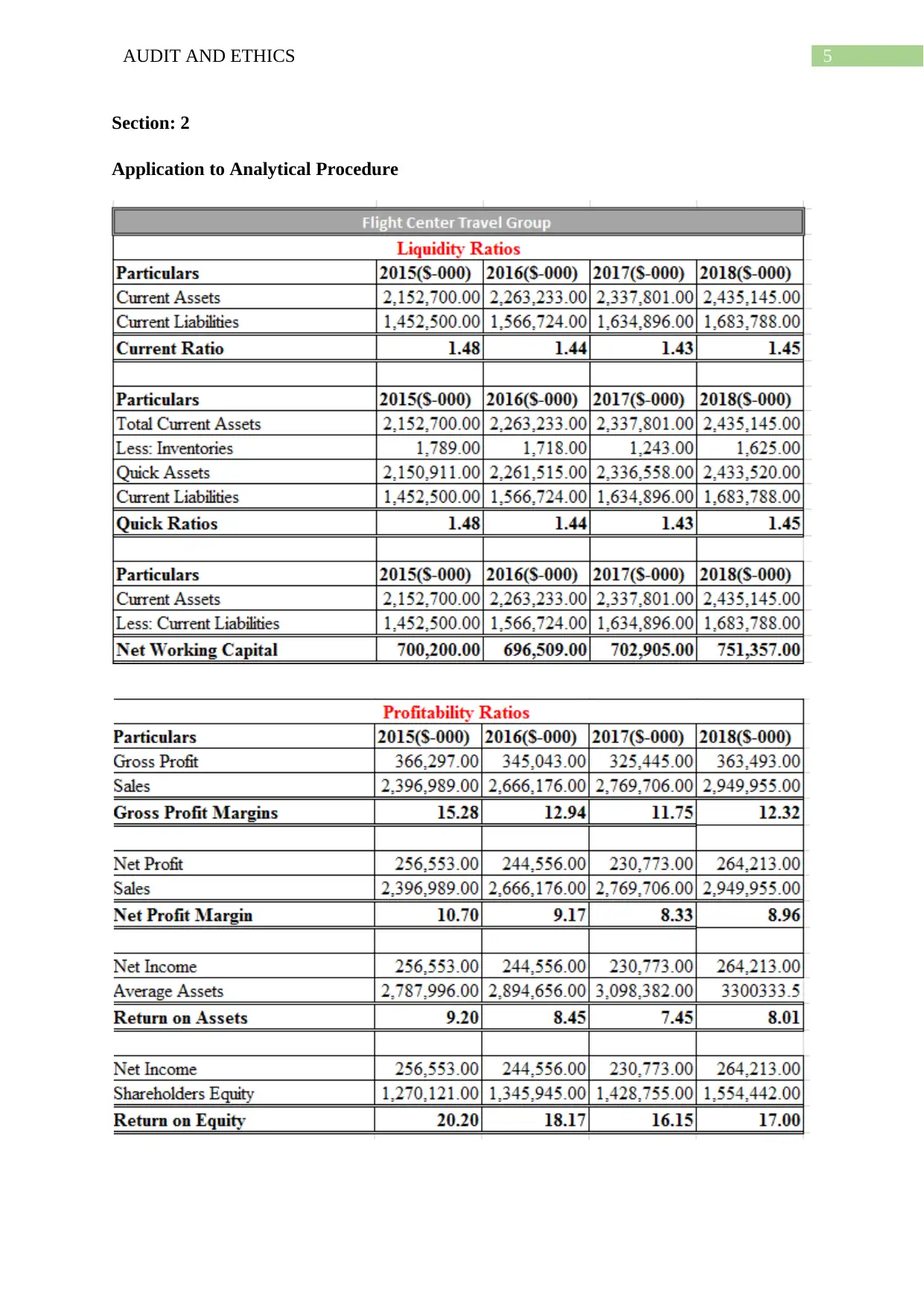

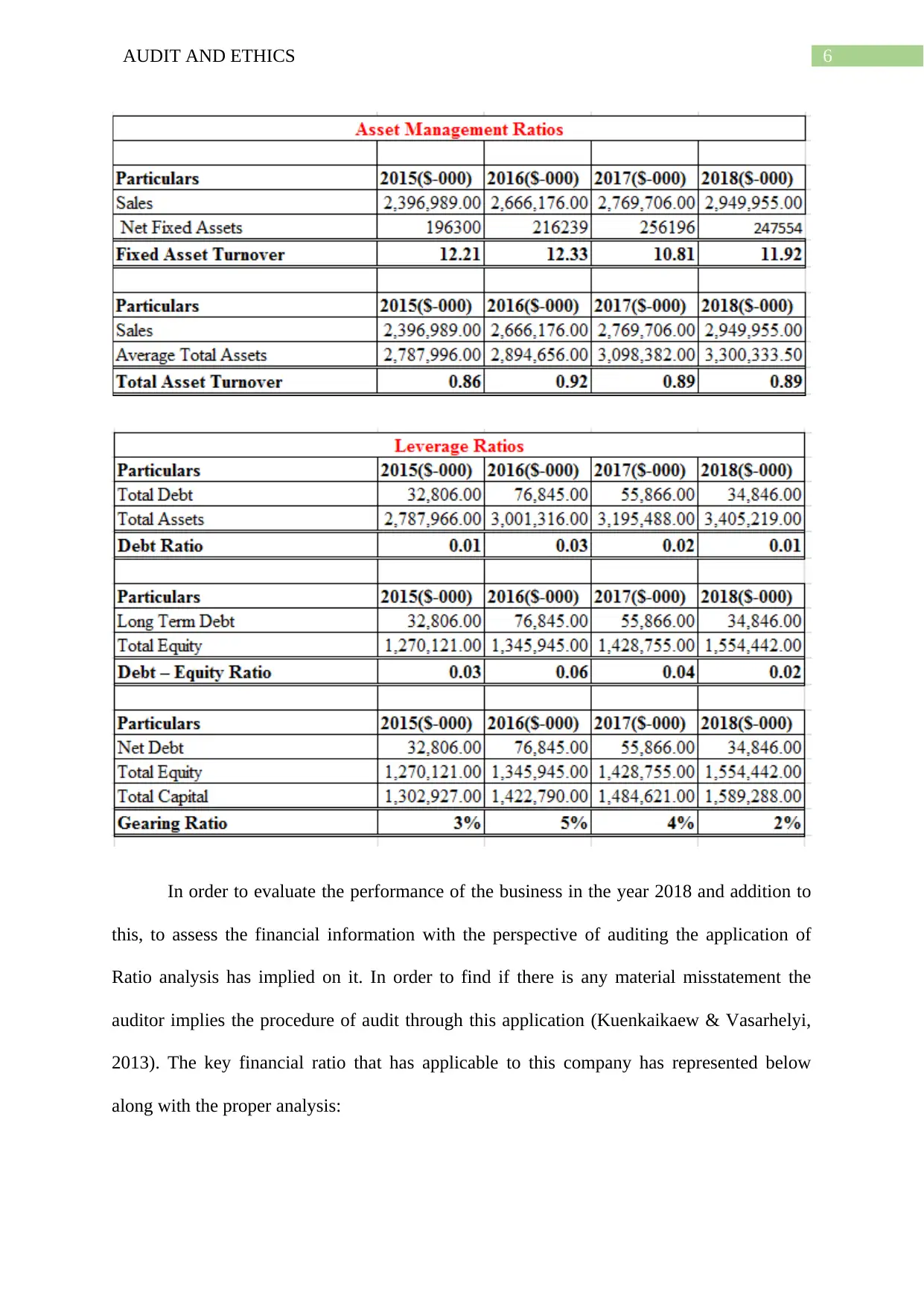

In order to evaluate the performance of the business in the year 2018 and addition to

this, to assess the financial information with the perspective of auditing the application of

Ratio analysis has implied on it. In order to find if there is any material misstatement the

auditor implies the procedure of audit through this application (Kuenkaikaew & Vasarhelyi,

2013). The key financial ratio that has applicable to this company has represented below

along with the proper analysis:

In order to evaluate the performance of the business in the year 2018 and addition to

this, to assess the financial information with the perspective of auditing the application of

Ratio analysis has implied on it. In order to find if there is any material misstatement the

auditor implies the procedure of audit through this application (Kuenkaikaew & Vasarhelyi,

2013). The key financial ratio that has applicable to this company has represented below

along with the proper analysis:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT AND ETHICS

The above figure reflects that the funds in respect of the cash that is available with the

Flight Central Group Ltd. is in favorable condition. As per the same shows the positive result

of increase in comparison of previous two consecutive years. This increase in the cash

position reflects a positive image of the company in terms of liquidity position of the

business. As the liquidity position of the business shows that, the company is in position to

overcome with any liability. Thus, the position is in their hand to take care of any of its

liability. The Net Debt of the company is in an appropriate position as it is reflecting that the

company has well placed in terms of debt that has taken by them. Still it shows the positive

condition of debt of the business. The gearing ratio of the company has declined in the

current year that shows the company has tried to reduce its total debt. The decline in the

gearing ratio reflects the management of the company has tried to reduce the risks associated

with the company (Omar et al.,2014).

The above figure in respect of the key financial ratios used in the company Flight

Central Group Ltd. represents the shareholder’s ratio and profitability ratios of the business.

The liquidity estimates which are covered for the business during the years shows appropriate

liquidity position for the business and shows that the business has appropriate cash for

meeting the current obligations of the business. This reflects the Income margin of the

business has decreased slightly in the previous year that suggests the company to improve the

profitability of the business to avoid any negative situation to face by the company. The

EBITDA of the business reflects the increase in the earnings of the business (Kamath &

Desai, 2014). It shows clearly that the company has achieved efficiency in the operational

process. The data also shows the earning per share of the company has increased during the

period that indicates a positive situation for the company. It shows that the company has tried

to increase their shareholder’s wealth.

The above figure reflects that the funds in respect of the cash that is available with the

Flight Central Group Ltd. is in favorable condition. As per the same shows the positive result

of increase in comparison of previous two consecutive years. This increase in the cash

position reflects a positive image of the company in terms of liquidity position of the

business. As the liquidity position of the business shows that, the company is in position to

overcome with any liability. Thus, the position is in their hand to take care of any of its

liability. The Net Debt of the company is in an appropriate position as it is reflecting that the

company has well placed in terms of debt that has taken by them. Still it shows the positive

condition of debt of the business. The gearing ratio of the company has declined in the

current year that shows the company has tried to reduce its total debt. The decline in the

gearing ratio reflects the management of the company has tried to reduce the risks associated

with the company (Omar et al.,2014).

The above figure in respect of the key financial ratios used in the company Flight

Central Group Ltd. represents the shareholder’s ratio and profitability ratios of the business.

The liquidity estimates which are covered for the business during the years shows appropriate

liquidity position for the business and shows that the business has appropriate cash for

meeting the current obligations of the business. This reflects the Income margin of the

business has decreased slightly in the previous year that suggests the company to improve the

profitability of the business to avoid any negative situation to face by the company. The

EBITDA of the business reflects the increase in the earnings of the business (Kamath &

Desai, 2014). It shows clearly that the company has achieved efficiency in the operational

process. The data also shows the earning per share of the company has increased during the

period that indicates a positive situation for the company. It shows that the company has tried

to increase their shareholder’s wealth.

8AUDIT AND ETHICS

Section: 3

Analysis of Cash Flow Statement

The Cash flow statement is one of the important and necessary statement that

is maintain by the company in the list of their financial statements. The Cash flow statement

effectively shows the inflow and outflow of the cash during an accounting period of the

company. The statement has prepared by the company to show the revenue they have

generated in respect to the company that ultimately reflects the result in inflow and outflow

of the cash in their business (Bepari, Rahman & Taher Mollik, 2013). The annual report of

the business reflects that the company mostly generates the cash through the operating

activities. Thus, the cash from operating activities reflects the positive side of the business. In

the receipts from customer of cash flow of the business, it reflects a cash inflow of the

business is same as shown as $ 2,884,573,000 during the year of 2018 that has relatively

increased from the previous year. This shows that the business is growing and earning more

profit during their process. The cash flow that has recognized from the financial statement

showing the figure of $ 2,480,898,000 that is cash paid to the suppliers and employees of the

company. This cash outflow represents the expenses that has made by the company during

carrying out the operations of the business. The Net Cash from Operating activities has

shown as positive that reflects a favorable condition of the business.

The Cash flow statements represents that the company has taken many decisions

during the accounting period related to acquisitions that has surely affected the investing cash

flow of the business. This has resulted in the decrease in the Net Cash from operating

activities and shown as negative figure during that period.

Addition to the above, the cash from financing activities has also shown as a negative

value. This is due to the company has taken a huge amount of loan that has to pay by them

during the accounting period. The overall repayments of loans and dividend distribution has

Section: 3

Analysis of Cash Flow Statement

The Cash flow statement is one of the important and necessary statement that

is maintain by the company in the list of their financial statements. The Cash flow statement

effectively shows the inflow and outflow of the cash during an accounting period of the

company. The statement has prepared by the company to show the revenue they have

generated in respect to the company that ultimately reflects the result in inflow and outflow

of the cash in their business (Bepari, Rahman & Taher Mollik, 2013). The annual report of

the business reflects that the company mostly generates the cash through the operating

activities. Thus, the cash from operating activities reflects the positive side of the business. In

the receipts from customer of cash flow of the business, it reflects a cash inflow of the

business is same as shown as $ 2,884,573,000 during the year of 2018 that has relatively

increased from the previous year. This shows that the business is growing and earning more

profit during their process. The cash flow that has recognized from the financial statement

showing the figure of $ 2,480,898,000 that is cash paid to the suppliers and employees of the

company. This cash outflow represents the expenses that has made by the company during

carrying out the operations of the business. The Net Cash from Operating activities has

shown as positive that reflects a favorable condition of the business.

The Cash flow statements represents that the company has taken many decisions

during the accounting period related to acquisitions that has surely affected the investing cash

flow of the business. This has resulted in the decrease in the Net Cash from operating

activities and shown as negative figure during that period.

Addition to the above, the cash from financing activities has also shown as a negative

value. This is due to the company has taken a huge amount of loan that has to pay by them

during the accounting period. The overall repayments of loans and dividend distribution has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT AND ETHICS

affected the Net cash position from the financing activities of the business. The statement

shows that the net cash position of the business has slightly declined but on the other hand it

reflects to be positive that shows a favorable condition for the business.

The fundamental principle of accounting is Principle of Going Concern. The auditor

needs to analyze and report those factors that is affecting the going concern principle of the

business. The auditor has do make a proper assessment of the business and he/she has to find

whether this principle is affected in any way or not (George-Silviu & Melinda-Timea, 2015).

The annual report of the company has shown a significant increase in the profits that result in

the profit for the business. The report has shown its overall cash position reflecting

appropriate liquidity position of the business that seems to be positive factor for the business.

Along with the above all factors the overall debt position of the business has also decreased

that means the company has reduced their risks related to debts to some extent. Thus, the

financial statement of the company has not shown any inappropriate sign that has affected the

going concern principle of the business.

Review of Audit Report

The auditing for this business report has done by Ernst and Young that is consider as

one of the big four firms operating in the field of Audit. According to the auditors, the

financial statement prepared by the company has followed the entire relevant accounting

standard and the provisions of Corporation Act, 2001. Therefore, it states a true and fair view

of the data. Therefore, the auditors has declared that the financial statement is free from any

material misstatement.

The auditors has also recognized certain key audit matters that can affect the financial

position of the business and the same has separately shown in the auditor’s report.

affected the Net cash position from the financing activities of the business. The statement

shows that the net cash position of the business has slightly declined but on the other hand it

reflects to be positive that shows a favorable condition for the business.

The fundamental principle of accounting is Principle of Going Concern. The auditor

needs to analyze and report those factors that is affecting the going concern principle of the

business. The auditor has do make a proper assessment of the business and he/she has to find

whether this principle is affected in any way or not (George-Silviu & Melinda-Timea, 2015).

The annual report of the company has shown a significant increase in the profits that result in

the profit for the business. The report has shown its overall cash position reflecting

appropriate liquidity position of the business that seems to be positive factor for the business.

Along with the above all factors the overall debt position of the business has also decreased

that means the company has reduced their risks related to debts to some extent. Thus, the

financial statement of the company has not shown any inappropriate sign that has affected the

going concern principle of the business.

Review of Audit Report

The auditing for this business report has done by Ernst and Young that is consider as

one of the big four firms operating in the field of Audit. According to the auditors, the

financial statement prepared by the company has followed the entire relevant accounting

standard and the provisions of Corporation Act, 2001. Therefore, it states a true and fair view

of the data. Therefore, the auditors has declared that the financial statement is free from any

material misstatement.

The auditors has also recognized certain key audit matters that can affect the financial

position of the business and the same has separately shown in the auditor’s report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT AND ETHICS

References

Al Nawaiseh, M. A. L., & Jaber, J. (2015). Auditing subsequent events from the

perspective of auditors: study from Jordan. International Journal of Financial

Research, 6(3), 78.

Bepari, K., Rahman, S. F., & Taher Mollik, A. (2013). Value relevance of earnings

and cash flows during the global financial crisis. Review of Accounting and

Finance, 12(3), 226-251.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public

accounting firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Flight Centre Travel Group (2019). About Us - Flight Centre Travel Group. [online]

Flight Centre Travel Group. Available at: http://www.fctgl.com/about-us/

[Accessed 26 Aug. 2019].

Flight Centre Travel Group. (2019). About Us - Flight Centre Travel Group.

Retrieved 26 August 2019, from http://www.fctgl.com/about-us/

George-Silviu, C., & Melinda-Timea, F. (2015). New audit reporting challenges:

auditing the going concern basis of accounting. Procedia Economics and

Finance, 32, 216-224.

Kamath, R., & Desai, R. (2014). The Impact of IFRS Adoption on the Financial

Activities of Companies in India: An Empirical Study. IUP Journal of

Accounting Research & Audit Practices, 13(3).

Kuenkaikaew, S., & Vasarhelyi, M. A. (2013). The predictive audit framework. The

International Journal of Digital Accounting Research, 13(19), 37-71.

References

Al Nawaiseh, M. A. L., & Jaber, J. (2015). Auditing subsequent events from the

perspective of auditors: study from Jordan. International Journal of Financial

Research, 6(3), 78.

Bepari, K., Rahman, S. F., & Taher Mollik, A. (2013). Value relevance of earnings

and cash flows during the global financial crisis. Review of Accounting and

Finance, 12(3), 226-251.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public

accounting firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Flight Centre Travel Group (2019). About Us - Flight Centre Travel Group. [online]

Flight Centre Travel Group. Available at: http://www.fctgl.com/about-us/

[Accessed 26 Aug. 2019].

Flight Centre Travel Group. (2019). About Us - Flight Centre Travel Group.

Retrieved 26 August 2019, from http://www.fctgl.com/about-us/

George-Silviu, C., & Melinda-Timea, F. (2015). New audit reporting challenges:

auditing the going concern basis of accounting. Procedia Economics and

Finance, 32, 216-224.

Kamath, R., & Desai, R. (2014). The Impact of IFRS Adoption on the Financial

Activities of Companies in India: An Empirical Study. IUP Journal of

Accounting Research & Audit Practices, 13(3).

Kuenkaikaew, S., & Vasarhelyi, M. A. (2013). The predictive audit framework. The

International Journal of Digital Accounting Research, 13(19), 37-71.

11AUDIT AND ETHICS

Lai, A., Melloni, G., & Stacchezzini, R. (2017). What does materiality mean to

integrated reporting preparers? An empirical exploration. Meditari

Accountancy Research, 25(4), 533-552.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality

and earnings management. Review of Accounting Studies, 18(2), 414-442.

Omar, N., Koya, R. K., Sanusi, Z. M., & Shafie, N. A. (2014). Financial statement

fraud: A case examination using Beneish model and ratio

analysis. International Journal of Trade, Economics and Finance, 5(2), 184.

Simnett, R., & Huggins, A. L. (2015). Integrated reporting and assurance: where can

research add value?. Sustainability Accounting, Management and Policy

Journal, 6(1), 29-53.

Yusoff, H., Othman, R., & Yatim, N. (2013). Environmental reporting practices in

Malaysia and Australia. Journal of Applied Business Research (Jabr), 29(6),

1717-1726.

Lai, A., Melloni, G., & Stacchezzini, R. (2017). What does materiality mean to

integrated reporting preparers? An empirical exploration. Meditari

Accountancy Research, 25(4), 533-552.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality

and earnings management. Review of Accounting Studies, 18(2), 414-442.

Omar, N., Koya, R. K., Sanusi, Z. M., & Shafie, N. A. (2014). Financial statement

fraud: A case examination using Beneish model and ratio

analysis. International Journal of Trade, Economics and Finance, 5(2), 184.

Simnett, R., & Huggins, A. L. (2015). Integrated reporting and assurance: where can

research add value?. Sustainability Accounting, Management and Policy

Journal, 6(1), 29-53.

Yusoff, H., Othman, R., & Yatim, N. (2013). Environmental reporting practices in

Malaysia and Australia. Journal of Applied Business Research (Jabr), 29(6),

1717-1726.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.