ACC518 Audit Assignment 1: Review of Accounting Standards & News

VerifiedAdded on 2023/06/04

|16

|3576

|420

Report

AI Summary

This report analyzes a news article concerning companies' reporting of climate risks, highlighting the need for environmental disclosures and the implications of fragmented information on investors. It also delves into accounting policies and theories guiding environmental disclosures, such as materiality and Corporate Social Responsibility (CSR). The report further discusses an exposure draft related to IAS 8, focusing on the distinction between accounting policies and accounting estimates, and examines various comments on the draft, providing a comprehensive overview of the issues and stakeholder perspectives. This document is available on Desklib, where students can find more solved assignments and past papers.

Audit Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 20th Sep 2018.

1 | P a g e

By student name

Professor

University

Date: 20th Sep 2018.

1 | P a g e

2

Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................6

References........................................................................................................................................4

2 | P a g e

Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................6

References........................................................................................................................................4

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Question 1

Introduction

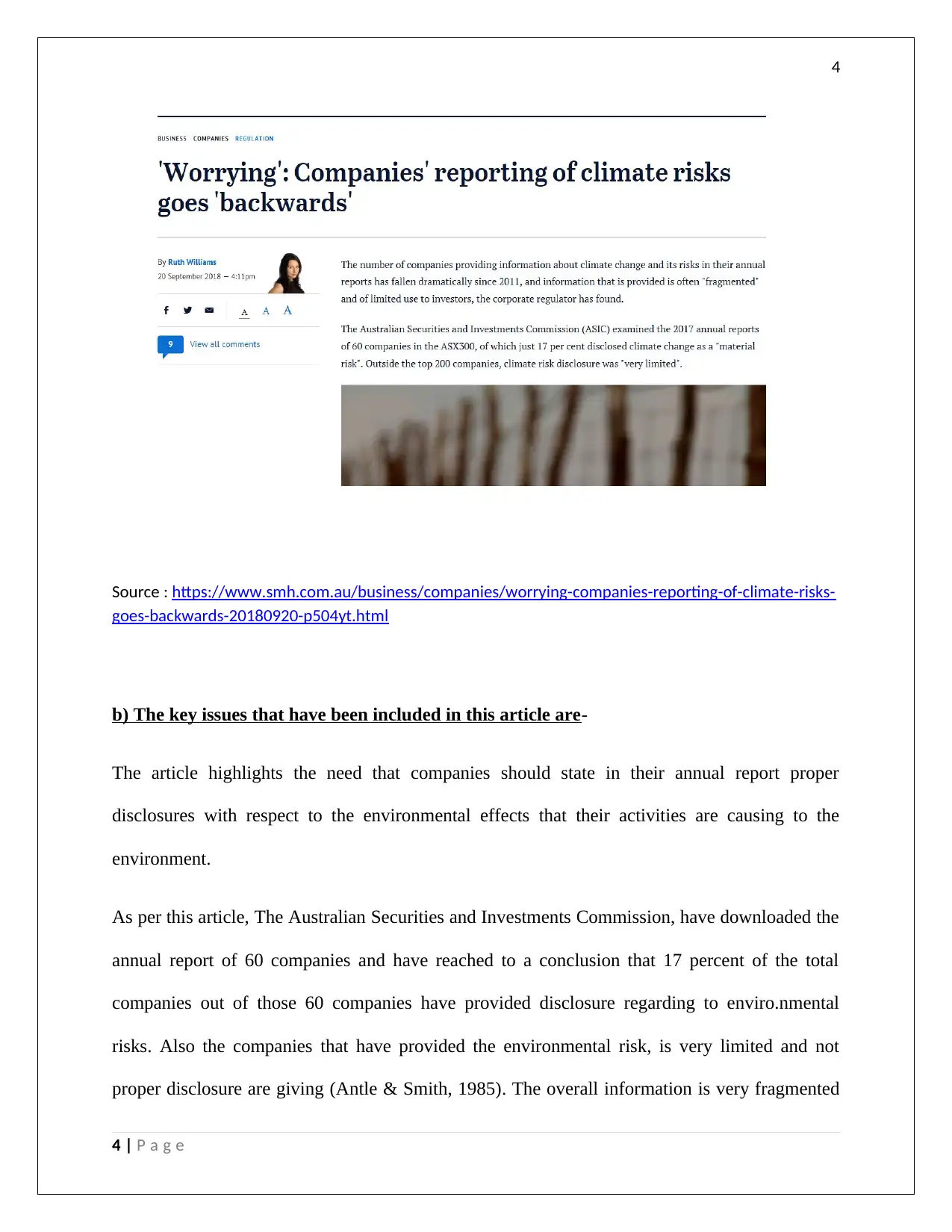

In the given assignment a news article has been selected to be presented in front of the

team to put their opinions on the same. The article that has been selected is “'Worrying':

Companies' reporting of climate risks goes 'backwards', this article highlights the needs of

disclosures that the companies make with relation to environmental issues that occur because of

their activities and what are the steps that they are taking to take care of that (Abdullah & Said,

2017). The article is discussing an important topic of corporate social responsibility that occurs

due to increased dependence of the companies with relation to the various stakeholders that are

dependent on the company in some way or the other. The companies have some important

responsibility towards the environment in which they are functioning and thus it is important that

proper disclosures are being made with relation to that. It has also highlighted how companies

have reduced providing proper disclosures with relation to environmental effects that they are

making. The article highlights how the annual reports of various companies have been

downloaded and making sure that how they have changed with relation to environmental

disclosures that they are making in their annual report (Alexander, 2016). It has also shown how

the investors are being affected with the fragmented information that they have provided in their

annual report with relation to environmental disclosures. It thus raises an important point how

accounting standards and regulations are there that are guiding how companies should fulfil their

responsibility that they have towards the stakeholders.

A copy of the news article has been given below:

3 | P a g e

Question 1

Introduction

In the given assignment a news article has been selected to be presented in front of the

team to put their opinions on the same. The article that has been selected is “'Worrying':

Companies' reporting of climate risks goes 'backwards', this article highlights the needs of

disclosures that the companies make with relation to environmental issues that occur because of

their activities and what are the steps that they are taking to take care of that (Abdullah & Said,

2017). The article is discussing an important topic of corporate social responsibility that occurs

due to increased dependence of the companies with relation to the various stakeholders that are

dependent on the company in some way or the other. The companies have some important

responsibility towards the environment in which they are functioning and thus it is important that

proper disclosures are being made with relation to that. It has also highlighted how companies

have reduced providing proper disclosures with relation to environmental effects that they are

making. The article highlights how the annual reports of various companies have been

downloaded and making sure that how they have changed with relation to environmental

disclosures that they are making in their annual report (Alexander, 2016). It has also shown how

the investors are being affected with the fragmented information that they have provided in their

annual report with relation to environmental disclosures. It thus raises an important point how

accounting standards and regulations are there that are guiding how companies should fulfil their

responsibility that they have towards the stakeholders.

A copy of the news article has been given below:

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Source : https://www.smh.com.au/business/companies/worrying-companies-reporting-of-climate-risks-

goes-backwards-20180920-p504yt.html

b) The key issues that have been included in this article are-

The article highlights the need that companies should state in their annual report proper

disclosures with respect to the environmental effects that their activities are causing to the

environment.

As per this article, The Australian Securities and Investments Commission, have downloaded the

annual report of 60 companies and have reached to a conclusion that 17 percent of the total

companies out of those 60 companies have provided disclosure regarding to enviro.nmental

risks. Also the companies that have provided the environmental risk, is very limited and not

proper disclosure are giving (Antle & Smith, 1985). The overall information is very fragmented

4 | P a g e

Source : https://www.smh.com.au/business/companies/worrying-companies-reporting-of-climate-risks-

goes-backwards-20180920-p504yt.html

b) The key issues that have been included in this article are-

The article highlights the need that companies should state in their annual report proper

disclosures with respect to the environmental effects that their activities are causing to the

environment.

As per this article, The Australian Securities and Investments Commission, have downloaded the

annual report of 60 companies and have reached to a conclusion that 17 percent of the total

companies out of those 60 companies have provided disclosure regarding to enviro.nmental

risks. Also the companies that have provided the environmental risk, is very limited and not

proper disclosure are giving (Antle & Smith, 1985). The overall information is very fragmented

4 | P a g e

5

and not proper and not valid at times, thus investors are not able to make an opinion on how the

companies are making proper disclosure with respect to that. The ASIC has also downloaded the

annual report of 1500 companies and have analyzed their past six years and based on that they

can see that from the past 2011 to 2014, there has been an overall reduction of 22 percent in the

total disclosure that has been made. As per the ASIC, it has been stated that this reduction was

due to the fact that repeal of the Gillard-era emissions trading scheme legislation (Belton, 2017).

It can also be seen that the disclosure provided are very fragmented and not clear and not precise.

Also if 100 companies have provided their disclosure, then that is also not clear and proper. In

this article the ASIC has urged the companies that they should follow proper disclosure policies

and state the same in their annual report under proper headings (Bouret, 2017). It has also urged

the investors that they should focus more in this repsect and see that companies are able to put

their stand in a proper way. . This ramped up the guidelines that were issued by the G20

taskforce, known as TCFD, that was anchored on the fact that the Paris agreement had pledged to

keep the global warming below 2 degrees. It has also stated that companies in New Zealand and

Australia that are having funds that are more than $2 trillion funds for management, then with

respect to that they should make proper disclosure as that might affect their capital credibility of

the company. It is evident that the overall reporting that has been down by the companies have

gone “backward” and they need to make sure that they are changing this scenario and take this

situation seriously.

c) There are various accounting policies and theories that guides the environmental disclosures

that companies need to do with respect to the environmental damage that they might do. In past

there have been serious cases of air pollution and global warming that has affected the

environment a lot and most of them have been caused because companies were not able to install

5 | P a g e

and not proper and not valid at times, thus investors are not able to make an opinion on how the

companies are making proper disclosure with respect to that. The ASIC has also downloaded the

annual report of 1500 companies and have analyzed their past six years and based on that they

can see that from the past 2011 to 2014, there has been an overall reduction of 22 percent in the

total disclosure that has been made. As per the ASIC, it has been stated that this reduction was

due to the fact that repeal of the Gillard-era emissions trading scheme legislation (Belton, 2017).

It can also be seen that the disclosure provided are very fragmented and not clear and not precise.

Also if 100 companies have provided their disclosure, then that is also not clear and proper. In

this article the ASIC has urged the companies that they should follow proper disclosure policies

and state the same in their annual report under proper headings (Bouret, 2017). It has also urged

the investors that they should focus more in this repsect and see that companies are able to put

their stand in a proper way. . This ramped up the guidelines that were issued by the G20

taskforce, known as TCFD, that was anchored on the fact that the Paris agreement had pledged to

keep the global warming below 2 degrees. It has also stated that companies in New Zealand and

Australia that are having funds that are more than $2 trillion funds for management, then with

respect to that they should make proper disclosure as that might affect their capital credibility of

the company. It is evident that the overall reporting that has been down by the companies have

gone “backward” and they need to make sure that they are changing this scenario and take this

situation seriously.

c) There are various accounting policies and theories that guides the environmental disclosures

that companies need to do with respect to the environmental damage that they might do. In past

there have been serious cases of air pollution and global warming that has affected the

environment a lot and most of them have been caused because companies were not able to install

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

proper equipment’s and meet proper safety standards (Charles H, Giovanna, Dennis M, & Robin

W, 2015). Because of this there were situations in which the companies lost their license and the

management were held guilty and were punished very badly. Because of this the investors had to

lose a lot of money. Then there were serious guidelines that stated that if companies are not

meeting safety standards or are involved in such type of industry then they should disclose the

same in them annul reports and follow accounting policies with that respect. But now it can be

seen that this has reduced a lot and companies have taken it very lightly. The same has been

highlighted in this article (Coate & Mitschow, 2017).

ii) The theory of materiality can be linked to this policy of accounting disclosure with respect to

environmental issues that the causes. Materiality as a concept refers to the fact that any event,

transaction or activity that might affect the position of the company financially and can affect its

going concern policies then it should be stated and disclosed. In case of environmental risks

companies never considered it to be material enough that they need to give disclosure with

respect to that. But it can be seen that with changing times, the effect that activities that the

companies were doing was affecting the environment very badly and thus on that note there was

a lot of harm caused and thus it was important that companies should state this in their annual

report (Eddy, Filip,R, & Warlop, 2004). Corporate Social Responsibility is a model that frame

rules and regulations that helps companies in taking care of all the stakeholders that are

dependent on them in some way or the other. There are many cases where companies need to

balance the interest of all one stakeholder in pursuance of another and in this case, we see that

CSR policies are very effective. So, they are effective in term of environmental policies also, and

environment is an important stakeholder for the companies, as it is their responsibility to take

care of the society in which they are functioning. Thus, government has set standards of safety

6 | P a g e

proper equipment’s and meet proper safety standards (Charles H, Giovanna, Dennis M, & Robin

W, 2015). Because of this there were situations in which the companies lost their license and the

management were held guilty and were punished very badly. Because of this the investors had to

lose a lot of money. Then there were serious guidelines that stated that if companies are not

meeting safety standards or are involved in such type of industry then they should disclose the

same in them annul reports and follow accounting policies with that respect. But now it can be

seen that this has reduced a lot and companies have taken it very lightly. The same has been

highlighted in this article (Coate & Mitschow, 2017).

ii) The theory of materiality can be linked to this policy of accounting disclosure with respect to

environmental issues that the causes. Materiality as a concept refers to the fact that any event,

transaction or activity that might affect the position of the company financially and can affect its

going concern policies then it should be stated and disclosed. In case of environmental risks

companies never considered it to be material enough that they need to give disclosure with

respect to that. But it can be seen that with changing times, the effect that activities that the

companies were doing was affecting the environment very badly and thus on that note there was

a lot of harm caused and thus it was important that companies should state this in their annual

report (Eddy, Filip,R, & Warlop, 2004). Corporate Social Responsibility is a model that frame

rules and regulations that helps companies in taking care of all the stakeholders that are

dependent on them in some way or the other. There are many cases where companies need to

balance the interest of all one stakeholder in pursuance of another and in this case, we see that

CSR policies are very effective. So, they are effective in term of environmental policies also, and

environment is an important stakeholder for the companies, as it is their responsibility to take

care of the society in which they are functioning. Thus, government has set standards of safety

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

that every company needs to meet and in case they fail, they will be penalized. Not just meeting

the standard is important, giving proper disclosures with respect to this is also important as

investors needs to be aware about the stand that the companies are taking (Ghofiqi, 2018).

Investors are the people who are putting their funds in the company, in case where the company

fails, the investors would be also affected. It has also been highlighted in this article that

companies that are providing disclosure are in a very vague manner, which makes it difficult for

them to are depending on the annual reports. Thus, need arises that there should be clear

disclosures and that should be on point and that should be helpful to the companies in some way

or the other. So, we see that still not many rules are there guiding the principles of environmental

disclosures but whatever is there they seek to spread awareness among the investors, companies,

public that it is the duty of the companies to protect the environment in which they are

functioning, and it is material and hence should be stated in the annual report of the companies

(Ruth, 2018).

Conclusion

Based on the overall analysis it can be said that there have been many changes that have

occurred with respect to environmental disclosures but what is required is that companies should

take their responsibility seriously and put proper information for the investors as the ASIC is

stating in the given article.

7 | P a g e

that every company needs to meet and in case they fail, they will be penalized. Not just meeting

the standard is important, giving proper disclosures with respect to this is also important as

investors needs to be aware about the stand that the companies are taking (Ghofiqi, 2018).

Investors are the people who are putting their funds in the company, in case where the company

fails, the investors would be also affected. It has also been highlighted in this article that

companies that are providing disclosure are in a very vague manner, which makes it difficult for

them to are depending on the annual reports. Thus, need arises that there should be clear

disclosures and that should be on point and that should be helpful to the companies in some way

or the other. So, we see that still not many rules are there guiding the principles of environmental

disclosures but whatever is there they seek to spread awareness among the investors, companies,

public that it is the duty of the companies to protect the environment in which they are

functioning, and it is material and hence should be stated in the annual report of the companies

(Ruth, 2018).

Conclusion

Based on the overall analysis it can be said that there have been many changes that have

occurred with respect to environmental disclosures but what is required is that companies should

take their responsibility seriously and put proper information for the investors as the ASIC is

stating in the given article.

7 | P a g e

8

Question 2

The second part of the assignment deals with draft exposures that are given for the public on the

specific websites of the accounting standards and policies forming board and the public can

comment on that exposure draft. All the comments are considered and based on that they can

take decision whether they want to pass that accounting standard or policy or not and implement

it. In this assignment one of such exposure draft that have been published on the IASB websites

is discussed and various comments on that are also analyzed and then proper conclusion has been

given (Lepistö & Ihantola, 2018).

Introduction

There are many exposure drafts that are there and people can comment on them whether they

agree to it or not. In the given case the draft exposure is in relation to the IAS 8 Accounting

Policies, Changes in Accounting Estimates and Errors. The article is mainly highlighting the

difference between the accounting policies and accounting estimates. It is very difficult for

accountants and professionals to understand the basic difference between accounting policies and

8 | P a g e

Question 2

The second part of the assignment deals with draft exposures that are given for the public on the

specific websites of the accounting standards and policies forming board and the public can

comment on that exposure draft. All the comments are considered and based on that they can

take decision whether they want to pass that accounting standard or policy or not and implement

it. In this assignment one of such exposure draft that have been published on the IASB websites

is discussed and various comments on that are also analyzed and then proper conclusion has been

given (Lepistö & Ihantola, 2018).

Introduction

There are many exposure drafts that are there and people can comment on them whether they

agree to it or not. In the given case the draft exposure is in relation to the IAS 8 Accounting

Policies, Changes in Accounting Estimates and Errors. The article is mainly highlighting the

difference between the accounting policies and accounting estimates. It is very difficult for

accountants and professionals to understand the basic difference between accounting policies and

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

estimates and this exposure draft aims to make it clear in a better way. It highlights the difference

between the accounting estimates and accounting policies. It is very important that companies

should be aware of this because accounting estimates are those that affects the profit loss and

balance sheet transactions and accounting policies do not impact them (Kusnadi & Wei, 2017).

So, they are materially relevant and affects the financial position of the company in some way or

the other. And thus, they need to understand what are the accounting estimates and accounting

policies are.

An extract of the exposure draft is given below:

Source : https://www.ifrs.org/projects/work-plan/accounting-policies-and-accounting-estimates/

comment-letters-projects/exposure-draft-accounting-policies-and-accounting-estimates/

#consultation

9 | P a g e

estimates and this exposure draft aims to make it clear in a better way. It highlights the difference

between the accounting estimates and accounting policies. It is very important that companies

should be aware of this because accounting estimates are those that affects the profit loss and

balance sheet transactions and accounting policies do not impact them (Kusnadi & Wei, 2017).

So, they are materially relevant and affects the financial position of the company in some way or

the other. And thus, they need to understand what are the accounting estimates and accounting

policies are.

An extract of the exposure draft is given below:

Source : https://www.ifrs.org/projects/work-plan/accounting-policies-and-accounting-estimates/

comment-letters-projects/exposure-draft-accounting-policies-and-accounting-estimates/

#consultation

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

In the above exposure draft it can be seen that the authority have stated the various amendments

that has been made with respect to IAS8. It can be stated that accounting policies are those that

helps in the functioning of the company, they are the rules and regulations that affects the

company. It is inclusive of measured procedure for disclosure of facts that are important to the

company and the stakeholder. On the other hand, accounting estimate is the measurement or

appropriation of the accounts of the companies, and deals with which account needs to debited

and credited and how the books of the company will be affected by the same. It is based on

judgement and knowledge that companies derive from relevant sources and are mostly based on

facts and figure. Few example of accounting estimates are provision for bad and doubtful debts,

provision for debtors, general reserves, measurement of inventories, various types of costing etc

(Iggers, 2018). There are many authorities that decides based on relevant facts of accounting on

how these figures would be calculated and there are specific methods that companies need to

follow for this. In case if the company fails they wont be able to present the correct value of the

elements of the financial statements and that would affect their position financially. Thus we see

that knowing the difference between accounting estimates and accounting policies is so

important. If the accountants are not aware then they wont be able to take correct decisions for

the companies.

Various Comments that have been stated in the exposure drafts.

Nandi Uchenna, is a professional from Nigeria and he has stated that he is ok with the overall

amendments that are stated in the proposed draft however he is not in favor of one policy that the

authorities have stated. In his comment he mentions that paragraph 32A and 32B are not

10 | P a g e

In the above exposure draft it can be seen that the authority have stated the various amendments

that has been made with respect to IAS8. It can be stated that accounting policies are those that

helps in the functioning of the company, they are the rules and regulations that affects the

company. It is inclusive of measured procedure for disclosure of facts that are important to the

company and the stakeholder. On the other hand, accounting estimate is the measurement or

appropriation of the accounts of the companies, and deals with which account needs to debited

and credited and how the books of the company will be affected by the same. It is based on

judgement and knowledge that companies derive from relevant sources and are mostly based on

facts and figure. Few example of accounting estimates are provision for bad and doubtful debts,

provision for debtors, general reserves, measurement of inventories, various types of costing etc

(Iggers, 2018). There are many authorities that decides based on relevant facts of accounting on

how these figures would be calculated and there are specific methods that companies need to

follow for this. In case if the company fails they wont be able to present the correct value of the

elements of the financial statements and that would affect their position financially. Thus we see

that knowing the difference between accounting estimates and accounting policies is so

important. If the accountants are not aware then they wont be able to take correct decisions for

the companies.

Various Comments that have been stated in the exposure drafts.

Nandi Uchenna, is a professional from Nigeria and he has stated that he is ok with the overall

amendments that are stated in the proposed draft however he is not in favor of one policy that the

authorities have stated. In his comment he mentions that paragraph 32A and 32B are not

10 | P a g e

11

consistent with each other and are providing contrast opinion on the overall concept of

accounting policy and estimates. In his opinion he states that in case of measurement of

inventories, FIFO or weighted average method can be selected as a process of accounting

estimates and not accounting policy (Johan, 2018).

Mr. Hans Hoogervorst, he is the chairman of the IASB IFRS foundation, he has presented his

opinion on the exposure draft is given below. As per him he states that the various provisions of

the accounting standard with relation to the difference between the accounting policies and

accounting estimates is stated. He has stated only one point as per which it states that the

authorities must frame definite rules and regulations with relation to the specific rules that must

be presented for the overall treatment of the inventories that can be interchanged between

companies.

Segun Adebiyi, who is one more professional and he has stated that he agrees to the overall

amendments that have been made by the authorities except one. He feel that when it comes to

accounting for inventory, the companies should see to it that they are IAS 2 should be treated as

an accounting policy and not an accounting estimates as most of the inventories are brought from

outside and then treated in the store and hence they are also part of interchangebale inventory

and companies should have proper knowledge on how they are going to treat them (Golden,

2006).

The Australian Council of Auditors, have stated in their comment that they are with the

authorities and they feel that the authorities have done full justice and have clearly stated what is

the diffferance between accounting policy and estimates when it comes of treatment of some

specific assets like inventories, intangible assets etc. So in case accountants go through this they

11 | P a g e

consistent with each other and are providing contrast opinion on the overall concept of

accounting policy and estimates. In his opinion he states that in case of measurement of

inventories, FIFO or weighted average method can be selected as a process of accounting

estimates and not accounting policy (Johan, 2018).

Mr. Hans Hoogervorst, he is the chairman of the IASB IFRS foundation, he has presented his

opinion on the exposure draft is given below. As per him he states that the various provisions of

the accounting standard with relation to the difference between the accounting policies and

accounting estimates is stated. He has stated only one point as per which it states that the

authorities must frame definite rules and regulations with relation to the specific rules that must

be presented for the overall treatment of the inventories that can be interchanged between

companies.

Segun Adebiyi, who is one more professional and he has stated that he agrees to the overall

amendments that have been made by the authorities except one. He feel that when it comes to

accounting for inventory, the companies should see to it that they are IAS 2 should be treated as

an accounting policy and not an accounting estimates as most of the inventories are brought from

outside and then treated in the store and hence they are also part of interchangebale inventory

and companies should have proper knowledge on how they are going to treat them (Golden,

2006).

The Australian Council of Auditors, have stated in their comment that they are with the

authorities and they feel that the authorities have done full justice and have clearly stated what is

the diffferance between accounting policy and estimates when it comes of treatment of some

specific assets like inventories, intangible assets etc. So in case accountants go through this they

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.