ACC3AUD Assignment: Detailed Audit and Assurance Report on AMP Limited

VerifiedAdded on 2022/09/02

|12

|2100

|23

Report

AI Summary

This report provides a comprehensive audit and assurance analysis of AMP Ltd, a financial services company operating in Australia and New Zealand, specializing in superannuation, investments, advisory, and banking services. The report examines AMP Ltd's areas of operation, key competitors like CommBank, Westpac, ANZ, and NAB, and relevant legal regulations such as the Competition and Consumer Act 2010, Corporations Amendment Act 2012, Anti-Money Laundering Act 2006, and ASIC Act 2001. It identifies key business risks, including environmental sustainability issues, ineffective internal controls, regulatory changes, and market risks. Furthermore, the report assesses account risks and key assertions for life insurance contract claims, investments in financial assets, intangible assets, and interest-bearing liabilities. Finally, it discusses corporate governance principles and the acceptance of the audit based on AMP Ltd's reporting framework and proactive approach to risk management. The report is based on the 2018 annual report of AMP Limited.

Running head: AUDIT AND ASSURANCE

Audit and Assurance

Name of the Student:

Name of the University:

Author’s Note

Audit and Assurance

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT AND ASSURANCE

Table of Contents

Executive Summary.........................................................................................................................2

Discussion........................................................................................................................................3

Areas of Operations.....................................................................................................................3

Competitors of the Business........................................................................................................3

Legal Regulations Applicable to the Company...........................................................................3

Business Risks of AMP ltd..........................................................................................................4

Account Risks and Key Assertions..............................................................................................5

Corporate Governance Principles and Recommendations..........................................................9

Acceptance of Audit....................................................................................................................9

Reference.......................................................................................................................................10

AUDIT AND ASSURANCE

Table of Contents

Executive Summary.........................................................................................................................2

Discussion........................................................................................................................................3

Areas of Operations.....................................................................................................................3

Competitors of the Business........................................................................................................3

Legal Regulations Applicable to the Company...........................................................................3

Business Risks of AMP ltd..........................................................................................................4

Account Risks and Key Assertions..............................................................................................5

Corporate Governance Principles and Recommendations..........................................................9

Acceptance of Audit....................................................................................................................9

Reference.......................................................................................................................................10

2

AUDIT AND ASSURANCE

Executive Summary

The focus of the assessment is to understand the operations of AMP ltd which is engaged

in providing financial services. The financial services which is provided by a business is of the

nature of superannuation products and investments products which contribute to the revenue

which is generated by the business. The assessment would be focusing on the primary activities

which assist the business to generate revenue and also the main competitors of the business in the

market. The assessment would also be showing the four accounts which are susceptible to risks

in a business and also the key assertions which are associated with the same. The analysis would

be further be showing all applicable laws and regulations which are applicable to the company

and whether the managers of the entity complies with the same or not.

Discussion

Areas of Operations

The business of AMP ltd is engaged in providing financial services to the clients of

Australia and New Zealand. The company specialises in providing products of superannuation

and investments. In addition to this, the business also provides advisory services and banking

services to the clients especially loans such as home loans and saving accounts. The business

operations of AMP ltd in Australia is the largest provider of life insurance and superannuation

(AMP Ltd 2020). As per the annual report for the business, the four major activities of AMP are

Advisory and Banking services, Insurance and Superannuation, Customer Solutions and AMP

Capital.

Competitors of the Business

AUDIT AND ASSURANCE

Executive Summary

The focus of the assessment is to understand the operations of AMP ltd which is engaged

in providing financial services. The financial services which is provided by a business is of the

nature of superannuation products and investments products which contribute to the revenue

which is generated by the business. The assessment would be focusing on the primary activities

which assist the business to generate revenue and also the main competitors of the business in the

market. The assessment would also be showing the four accounts which are susceptible to risks

in a business and also the key assertions which are associated with the same. The analysis would

be further be showing all applicable laws and regulations which are applicable to the company

and whether the managers of the entity complies with the same or not.

Discussion

Areas of Operations

The business of AMP ltd is engaged in providing financial services to the clients of

Australia and New Zealand. The company specialises in providing products of superannuation

and investments. In addition to this, the business also provides advisory services and banking

services to the clients especially loans such as home loans and saving accounts. The business

operations of AMP ltd in Australia is the largest provider of life insurance and superannuation

(AMP Ltd 2020). As per the annual report for the business, the four major activities of AMP are

Advisory and Banking services, Insurance and Superannuation, Customer Solutions and AMP

Capital.

Competitors of the Business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT AND ASSURANCE

The level of competition in the market of financial products is comparatively high as

more and more finance-based companies are coming up providing the same products. The top

four competitors of AMP ltd which can be identified are CommBank, Westpac, ANZ and NAB.

All these banks operate in the market and is well recognised so naturally the level of competition

in the market is quite high.

Legal Regulations Applicable to the Company

The business of AMP ltd also needs to adhere to certain legal regulations so that the

business can operate in an efficient environment. The management of the company needs to

appropriately identify the relevant legislations which are applicable on the company and take

step so that the business does not attract any penalty or fines due to violation of regulations

(Mock and Fukukawa 2015). Some of the regulations which are applicable in the business of

AMP ltd are listed below in details:

Competition and Consumer Act 2010: The competition and consumer Act of 2010 was

introduced by the parliament of Australia and it was earlier known as Trade Practices Act

1974. The regulation aimed to promote fair practices in competition and also ensure that

the interests of the consumers are well protected.

Corporations Amendment (Future of Financial Advice) Act 2012: These are referred

to as an amendment which was made to Corporation Act 2001 which required financial

advisors to act in the best interests of the clients and even put forward the interest of the

clients ahead of his self-interests.

Anti-Money Laundering and Counter-Terrorism Financing Act 2006: The main

purpose of this regulation is to prevent excessive laundering of money and also stop

AUDIT AND ASSURANCE

The level of competition in the market of financial products is comparatively high as

more and more finance-based companies are coming up providing the same products. The top

four competitors of AMP ltd which can be identified are CommBank, Westpac, ANZ and NAB.

All these banks operate in the market and is well recognised so naturally the level of competition

in the market is quite high.

Legal Regulations Applicable to the Company

The business of AMP ltd also needs to adhere to certain legal regulations so that the

business can operate in an efficient environment. The management of the company needs to

appropriately identify the relevant legislations which are applicable on the company and take

step so that the business does not attract any penalty or fines due to violation of regulations

(Mock and Fukukawa 2015). Some of the regulations which are applicable in the business of

AMP ltd are listed below in details:

Competition and Consumer Act 2010: The competition and consumer Act of 2010 was

introduced by the parliament of Australia and it was earlier known as Trade Practices Act

1974. The regulation aimed to promote fair practices in competition and also ensure that

the interests of the consumers are well protected.

Corporations Amendment (Future of Financial Advice) Act 2012: These are referred

to as an amendment which was made to Corporation Act 2001 which required financial

advisors to act in the best interests of the clients and even put forward the interest of the

clients ahead of his self-interests.

Anti-Money Laundering and Counter-Terrorism Financing Act 2006: The main

purpose of this regulation is to prevent excessive laundering of money and also stop

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT AND ASSURANCE

illegal financing of terrorism activities. The regulation puts an obligation on the financial

sector to take steps in this respect and stay proactive in the operations of the finances.

ASIC Act 2001: This act enforces the ASIC to act as an regulator in the finance markets

and ensure that finance corporations acts in the best interests of the clients and ensure that

the operations of the business are ethically managed.

Business Risks of AMP ltd

The business risks are risk which states that the profitability of a business might be

affected due to such risks and therefore the management needs to take appropriate steps to

reduce such types of risks. In the case of AMP ltd, the business faces risks which has a direct

impact on the profits of the business. One of the risks which can be identified is of related to

environmental and sustainability risks for which the management of AMP ltd has taken active

steps so that the business can prevent emission of carbon and thereby protect the environment.

The company has been facing sustainability issues and the same is covered in the annual report

of the business.

Another business risk which can be identified which impacts the operations of AMP ltd is

the ineffective internal control of the management (Munteanu 2015). This is one of the primary

reason that the costs of the business are high and the same leaves the company also susceptible to

frauds which might be concealed easily. The management of the company needs to take

appropriate steps so that the risks can be managed in an effective manner.

One of the major business risks which has affected the company significantly risks is the

regulatory changes on the operations (ABC News. 2019). The senior executives of the company

have faced charges for a scandal which was committed by them. The scandal was that company

AUDIT AND ASSURANCE

illegal financing of terrorism activities. The regulation puts an obligation on the financial

sector to take steps in this respect and stay proactive in the operations of the finances.

ASIC Act 2001: This act enforces the ASIC to act as an regulator in the finance markets

and ensure that finance corporations acts in the best interests of the clients and ensure that

the operations of the business are ethically managed.

Business Risks of AMP ltd

The business risks are risk which states that the profitability of a business might be

affected due to such risks and therefore the management needs to take appropriate steps to

reduce such types of risks. In the case of AMP ltd, the business faces risks which has a direct

impact on the profits of the business. One of the risks which can be identified is of related to

environmental and sustainability risks for which the management of AMP ltd has taken active

steps so that the business can prevent emission of carbon and thereby protect the environment.

The company has been facing sustainability issues and the same is covered in the annual report

of the business.

Another business risk which can be identified which impacts the operations of AMP ltd is

the ineffective internal control of the management (Munteanu 2015). This is one of the primary

reason that the costs of the business are high and the same leaves the company also susceptible to

frauds which might be concealed easily. The management of the company needs to take

appropriate steps so that the risks can be managed in an effective manner.

One of the major business risks which has affected the company significantly risks is the

regulatory changes on the operations (ABC News. 2019). The senior executives of the company

have faced charges for a scandal which was committed by them. The scandal was that company

5

AUDIT AND ASSURANCE

has charged million of fees from clients for no services and therefore for such a scandal the

company has to face cases lodged by ASIC. This would affect the reputation of company in the

market and impact the revenue which is generated by the company and also impact the ability of

the business to attract more clients to the operations of the business.

One of the most common risks which impacts the operations of the business is the market

risk. The business of AMP ltd is engaged in financial operations and provides financial products

and services (Huang, Lin and Raghunandan 2015). It is therefore for this reason that the business

is most susceptible to market risks as there is change of fluctuations. The business of AMP ltd

has diversified operations and therefore the same is volatile in nature.

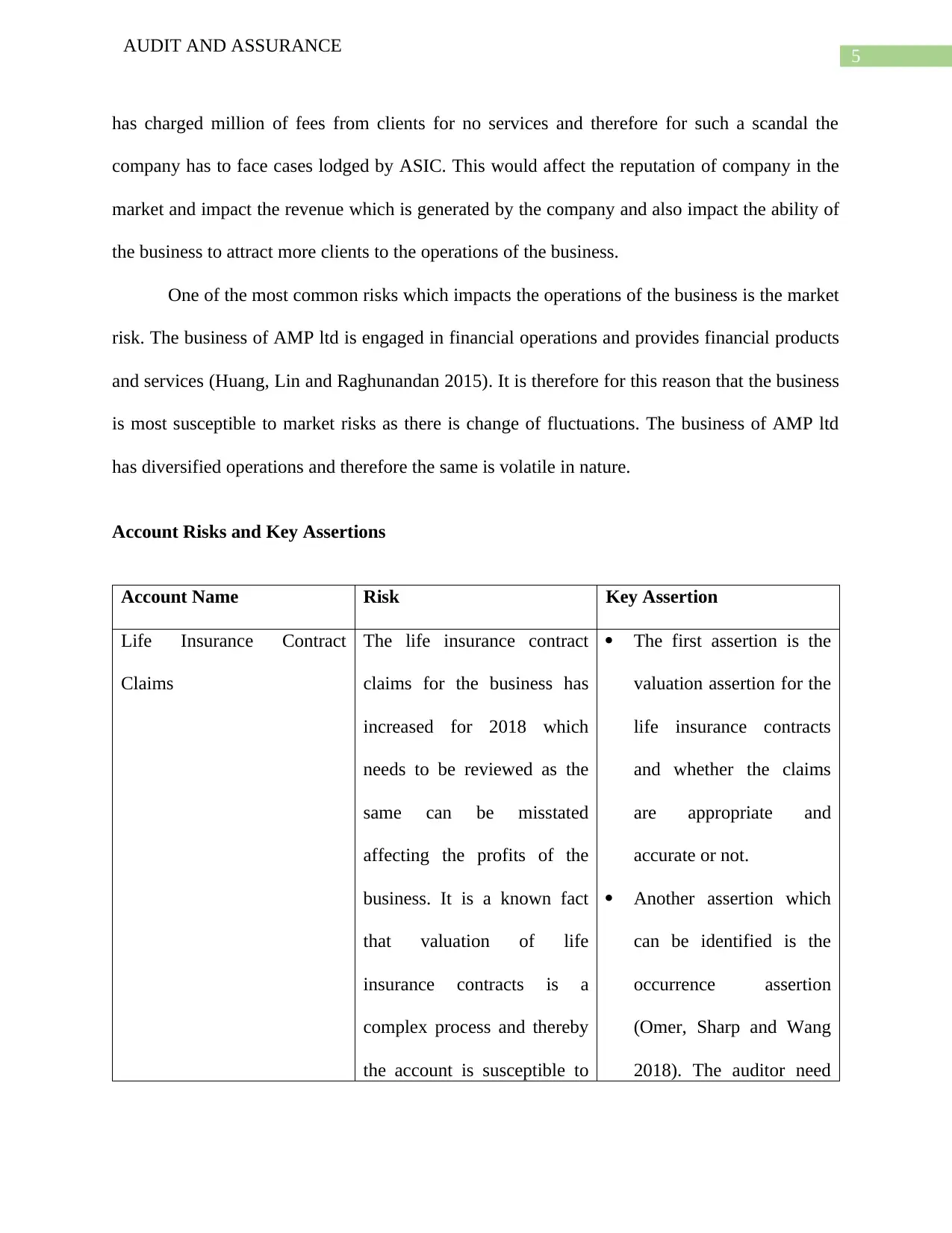

Account Risks and Key Assertions

Account Name Risk Key Assertion

Life Insurance Contract

Claims

The life insurance contract

claims for the business has

increased for 2018 which

needs to be reviewed as the

same can be misstated

affecting the profits of the

business. It is a known fact

that valuation of life

insurance contracts is a

complex process and thereby

the account is susceptible to

The first assertion is the

valuation assertion for the

life insurance contracts

and whether the claims

are appropriate and

accurate or not.

Another assertion which

can be identified is the

occurrence assertion

(Omer, Sharp and Wang

2018). The auditor need

AUDIT AND ASSURANCE

has charged million of fees from clients for no services and therefore for such a scandal the

company has to face cases lodged by ASIC. This would affect the reputation of company in the

market and impact the revenue which is generated by the company and also impact the ability of

the business to attract more clients to the operations of the business.

One of the most common risks which impacts the operations of the business is the market

risk. The business of AMP ltd is engaged in financial operations and provides financial products

and services (Huang, Lin and Raghunandan 2015). It is therefore for this reason that the business

is most susceptible to market risks as there is change of fluctuations. The business of AMP ltd

has diversified operations and therefore the same is volatile in nature.

Account Risks and Key Assertions

Account Name Risk Key Assertion

Life Insurance Contract

Claims

The life insurance contract

claims for the business has

increased for 2018 which

needs to be reviewed as the

same can be misstated

affecting the profits of the

business. It is a known fact

that valuation of life

insurance contracts is a

complex process and thereby

the account is susceptible to

The first assertion is the

valuation assertion for the

life insurance contracts

and whether the claims

are appropriate and

accurate or not.

Another assertion which

can be identified is the

occurrence assertion

(Omer, Sharp and Wang

2018). The auditor need

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT AND ASSURANCE

risks. to check if the life

insurance claim has

actually matured or not.

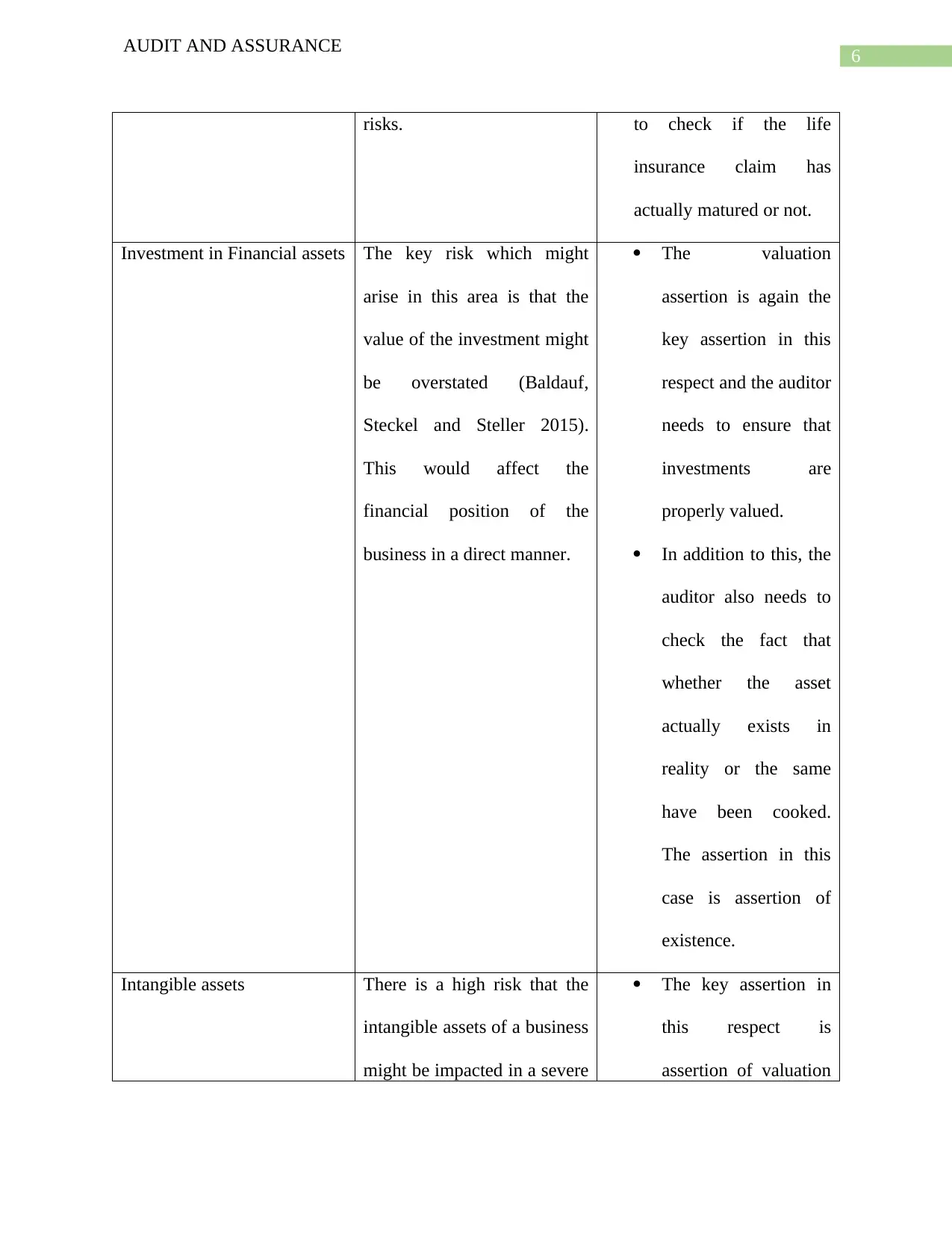

Investment in Financial assets The key risk which might

arise in this area is that the

value of the investment might

be overstated (Baldauf,

Steckel and Steller 2015).

This would affect the

financial position of the

business in a direct manner.

The valuation

assertion is again the

key assertion in this

respect and the auditor

needs to ensure that

investments are

properly valued.

In addition to this, the

auditor also needs to

check the fact that

whether the asset

actually exists in

reality or the same

have been cooked.

The assertion in this

case is assertion of

existence.

Intangible assets There is a high risk that the

intangible assets of a business

might be impacted in a severe

The key assertion in

this respect is

assertion of valuation

AUDIT AND ASSURANCE

risks. to check if the life

insurance claim has

actually matured or not.

Investment in Financial assets The key risk which might

arise in this area is that the

value of the investment might

be overstated (Baldauf,

Steckel and Steller 2015).

This would affect the

financial position of the

business in a direct manner.

The valuation

assertion is again the

key assertion in this

respect and the auditor

needs to ensure that

investments are

properly valued.

In addition to this, the

auditor also needs to

check the fact that

whether the asset

actually exists in

reality or the same

have been cooked.

The assertion in this

case is assertion of

existence.

Intangible assets There is a high risk that the

intangible assets of a business

might be impacted in a severe

The key assertion in

this respect is

assertion of valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT AND ASSURANCE

manner and the same can be

misstated. There is a risk that

the management has not

provided impairment charges

appropriately in this respect

which might make a big

difference.

which requires the

auditor to asses if the

value of intangible

assets which includes

goodwill are perfectly

presented.

Another assertion in

this respect would be

assertion of

completeness which

requires the auditor to

check if complete

disclosures are

provided in the annual

reports and there is no

ambiguity (Byrnes et

al. 2015).

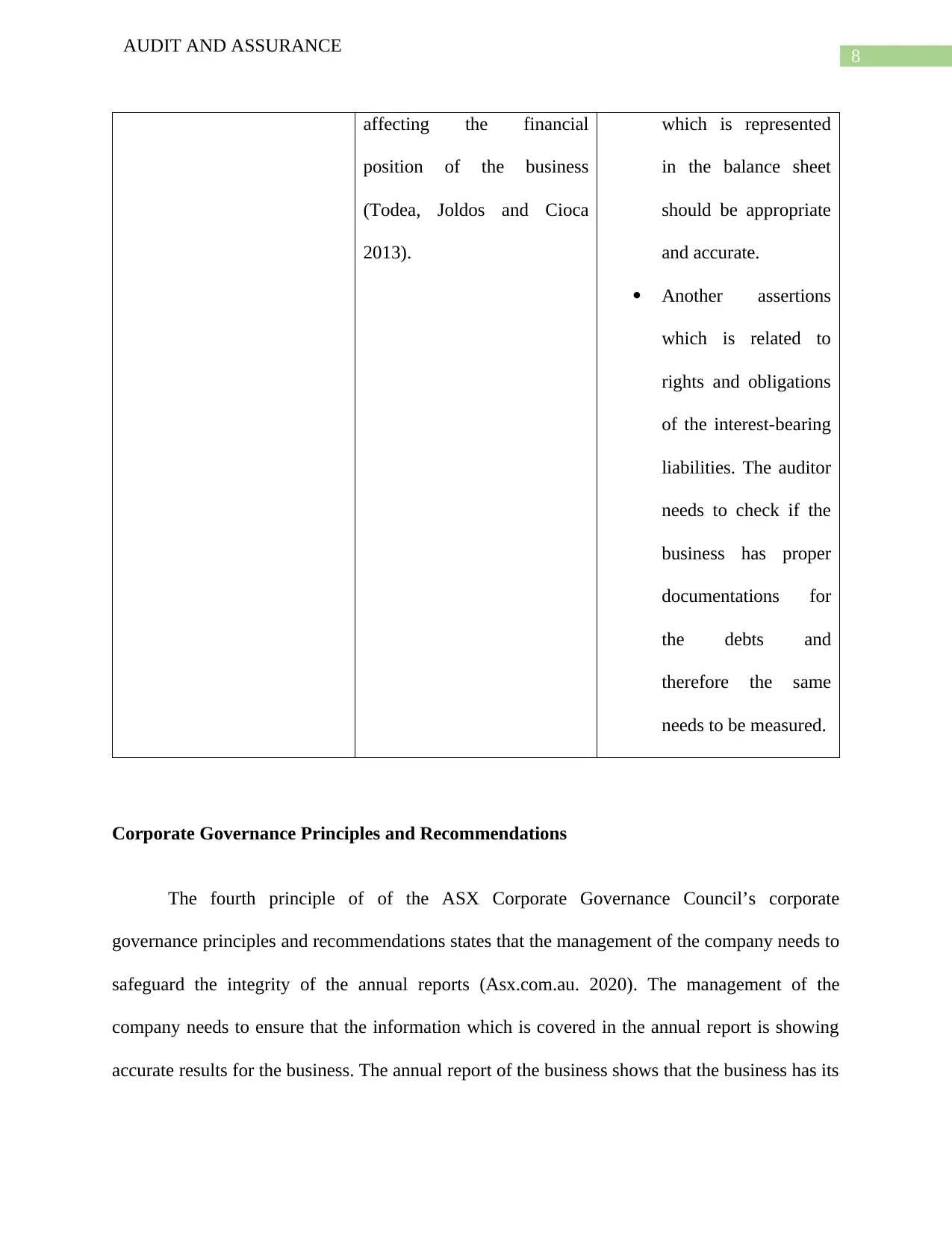

Interest Bearing Liabilities The auditor needs to check

the interest-bearing liabilities

which are shown in the

balance sheet and there is a

risk that the same might be

undervalued which would be

The auditor of the

business would be

considering the

assertion of

completeness which

states that the amount

AUDIT AND ASSURANCE

manner and the same can be

misstated. There is a risk that

the management has not

provided impairment charges

appropriately in this respect

which might make a big

difference.

which requires the

auditor to asses if the

value of intangible

assets which includes

goodwill are perfectly

presented.

Another assertion in

this respect would be

assertion of

completeness which

requires the auditor to

check if complete

disclosures are

provided in the annual

reports and there is no

ambiguity (Byrnes et

al. 2015).

Interest Bearing Liabilities The auditor needs to check

the interest-bearing liabilities

which are shown in the

balance sheet and there is a

risk that the same might be

undervalued which would be

The auditor of the

business would be

considering the

assertion of

completeness which

states that the amount

8

AUDIT AND ASSURANCE

affecting the financial

position of the business

(Todea, Joldos and Cioca

2013).

which is represented

in the balance sheet

should be appropriate

and accurate.

Another assertions

which is related to

rights and obligations

of the interest-bearing

liabilities. The auditor

needs to check if the

business has proper

documentations for

the debts and

therefore the same

needs to be measured.

Corporate Governance Principles and Recommendations

The fourth principle of of the ASX Corporate Governance Council’s corporate

governance principles and recommendations states that the management of the company needs to

safeguard the integrity of the annual reports (Asx.com.au. 2020). The management of the

company needs to ensure that the information which is covered in the annual report is showing

accurate results for the business. The annual report of the business shows that the business has its

AUDIT AND ASSURANCE

affecting the financial

position of the business

(Todea, Joldos and Cioca

2013).

which is represented

in the balance sheet

should be appropriate

and accurate.

Another assertions

which is related to

rights and obligations

of the interest-bearing

liabilities. The auditor

needs to check if the

business has proper

documentations for

the debts and

therefore the same

needs to be measured.

Corporate Governance Principles and Recommendations

The fourth principle of of the ASX Corporate Governance Council’s corporate

governance principles and recommendations states that the management of the company needs to

safeguard the integrity of the annual reports (Asx.com.au. 2020). The management of the

company needs to ensure that the information which is covered in the annual report is showing

accurate results for the business. The annual report of the business shows that the business has its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT AND ASSURANCE

own audit committee and risk management committee so that the reporting framework which is

followed by the business is appropriate.

Acceptance of Audit

The analysis of the annual report of AMP ltd for the year 2018 shows that the reporting

framework is as per the conceptual framework which is universally followed in a business. The

audit for the company would be accepted as the management of AMP ltd is trying to improve the

internal control and the management has been proactive in its approach for managing the

operations of the business.

AUDIT AND ASSURANCE

own audit committee and risk management committee so that the reporting framework which is

followed by the business is appropriate.

Acceptance of Audit

The analysis of the annual report of AMP ltd for the year 2018 shows that the reporting

framework is as per the conceptual framework which is universally followed in a business. The

audit for the company would be accepted as the management of AMP ltd is trying to improve the

internal control and the management has been proactive in its approach for managing the

operations of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT AND ASSURANCE

Reference

ABC News. (2019). AMP executives facing potential criminal charges. [online] Available at:

https://www.abc.net.au/news/2019-02-08/amp-executives-will-face-criminal-charges/10793402

[Accessed 6 Jan. 2020].

Annualreports.com. (2020). AMP Ltd. - AnnualReports.com. [online] Available at:

http://www.annualreports.com/Company/amp-ltd [Accessed 6 Jan. 2020].

Asx.com.au. (2020). [online] Available at: https://www.asx.com.au/documents/regulation/cgc-

principles-and-recommendations-fourth-edn.pdf [Accessed 6 Jan. 2020].

Baldauf, J., Steckel, R. and Steller, M., 2015. The Influence of Audit Risk and Materiality

Guidelines on Auditor’s Planning Materiality Assessment. Accounting and Finance

Research, 4(4), pp.97-114.

Byrnes, P., Brennan, G., Vasarhelyi, M., Moon, D. and Ghosh, S., 2015. Managing risk and the

audit process in a world of instantaneous change. Audit Analaytics and Continuous Audit:

Looking Toward The Future, pp.129-143.

Huang, H.W., Lin, S. and Raghunandan, K., 2015. The volatility of other comprehensive income

and audit fees. Accounting Horizons, 30(2), pp.195-210.

Mock, T.J. and Fukukawa, H., 2015. Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in A

Munteanu, C.C., 2015. Audit Risk Assessment in the Light of Current European

Regulations. Acta Universitatis Danubius. Œconomica, 11(3), pp.94-105.

AUDIT AND ASSURANCE

Reference

ABC News. (2019). AMP executives facing potential criminal charges. [online] Available at:

https://www.abc.net.au/news/2019-02-08/amp-executives-will-face-criminal-charges/10793402

[Accessed 6 Jan. 2020].

Annualreports.com. (2020). AMP Ltd. - AnnualReports.com. [online] Available at:

http://www.annualreports.com/Company/amp-ltd [Accessed 6 Jan. 2020].

Asx.com.au. (2020). [online] Available at: https://www.asx.com.au/documents/regulation/cgc-

principles-and-recommendations-fourth-edn.pdf [Accessed 6 Jan. 2020].

Baldauf, J., Steckel, R. and Steller, M., 2015. The Influence of Audit Risk and Materiality

Guidelines on Auditor’s Planning Materiality Assessment. Accounting and Finance

Research, 4(4), pp.97-114.

Byrnes, P., Brennan, G., Vasarhelyi, M., Moon, D. and Ghosh, S., 2015. Managing risk and the

audit process in a world of instantaneous change. Audit Analaytics and Continuous Audit:

Looking Toward The Future, pp.129-143.

Huang, H.W., Lin, S. and Raghunandan, K., 2015. The volatility of other comprehensive income

and audit fees. Accounting Horizons, 30(2), pp.195-210.

Mock, T.J. and Fukukawa, H., 2015. Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in A

Munteanu, C.C., 2015. Audit Risk Assessment in the Light of Current European

Regulations. Acta Universitatis Danubius. Œconomica, 11(3), pp.94-105.

11

AUDIT AND ASSURANCE

Omer, T.C., Sharp, N.Y. and Wang, D., 2018. The impact of religion on the going concern

reporting decisions of local audit offices. Journal of Business Ethics, 149(4), pp.811-831.

Todea, N., Joldos, A.M. and Cioca, I.C., 2013. Considerations Regarding Materiality Calculation

and Audit Risk in the Context of the Guidelines for Audit Quality. Anale. Seria Stiinte

Economice. Timisoara, 19, p.728.

AUDIT AND ASSURANCE

Omer, T.C., Sharp, N.Y. and Wang, D., 2018. The impact of religion on the going concern

reporting decisions of local audit offices. Journal of Business Ethics, 149(4), pp.811-831.

Todea, N., Joldos, A.M. and Cioca, I.C., 2013. Considerations Regarding Materiality Calculation

and Audit Risk in the Context of the Guidelines for Audit Quality. Anale. Seria Stiinte

Economice. Timisoara, 19, p.728.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.