Audit and Assurance Assignment: DIPL Ltd. Analysis and Audit

VerifiedAdded on 2020/03/04

|9

|2061

|48

Homework Assignment

AI Summary

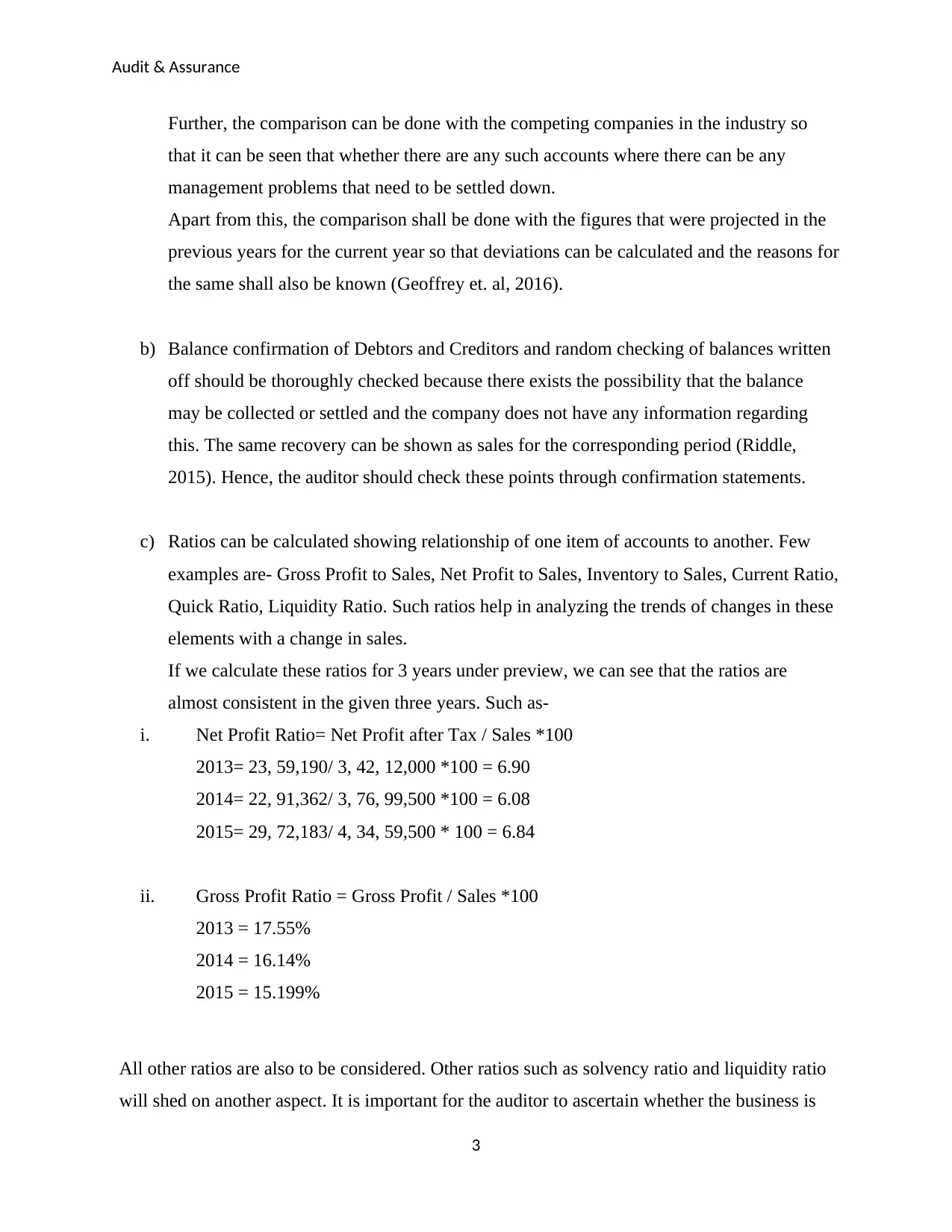

This assignment analyzes the audit and assurance practices applied to DIPL Ltd., focusing on analytical procedures, risk assessment, and potential frauds. The solution begins by outlining various analytical procedures, such as comparing current and previous financial data, industry benchmarks, and projected figures to identify trends and variances. It emphasizes the importance of verifying balance confirmations and calculating financial ratios to assess the company's performance. The assignment then explores inherent risks, including the implications of a new IT system implementation and the appointment of a CEO with financial interests, potentially leading to biased financial reporting. Furthermore, the solution identifies potential fraudulent activities related to unrecorded entries and inflated inventory values, discussing their impact on the auditor's opinion and the misrepresentation of financial statements. The assignment underscores the auditor's responsibility to maintain an unbiased perspective and assess all aspects of the business thoroughly to provide a fair and accurate opinion.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.