HI6026 Audit Assurance & Compliance: Auditor Reporting in Australia

VerifiedAdded on 2023/06/04

|16

|3754

|461

Report

AI Summary

This report provides a detailed analysis of the audit of Life Style Communities Limited, focusing on Pitcher Partners' audit work and compliance with Australian auditing standards. It covers the auditor's declaration of independence, the independent auditor's report and opinion, non-audit services performed, and an analysis of auditor remuneration. Key audit matters, particularly the valuation of investment properties, are discussed, along with the role of the audit committee and the responsibilities of directors and management. The report also addresses subsequent events and the effectiveness of information reported in audit reports. Desklib offers a wealth of similar solved assignments and past papers for students.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

Name of the Student:

Name of the University:

Authors Note:

Audit Assurance and Compliance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT ASSURANCE AND COMPLIANCE

Executive Summary:

Stakeholders of an entity are those people that have direct or indirect interests in the

entity and its operations. Most of the stakeholders’ only means of information to assess the

financial state of an entity and its functions is the annual report of the entity that it issues

annually. Annual reports contain financial as well as non-financial information about an entity

and the auditor’s report. Independent audit report included in the annual report of the company

provides the stakeholders independent views on the nature of the financial information contained

in the annual report. It is important that the audit report includes all necessary aspects of an

effective audit and a valid opinion on the financial information of the entity in plain and simple

English. It is specifically important because the users of financial statements are not supposed to

have technical knowledge and skills to understand complex accounting and financial terms.

Thus, the audit report should be such to easily elaborate on different aspects of financial

reporting and their nature. This document would be helpful to the readers to understand different

aspects associated with an audit that an auditor must take into consideration during the course of

audit.

AUDIT ASSURANCE AND COMPLIANCE

Executive Summary:

Stakeholders of an entity are those people that have direct or indirect interests in the

entity and its operations. Most of the stakeholders’ only means of information to assess the

financial state of an entity and its functions is the annual report of the entity that it issues

annually. Annual reports contain financial as well as non-financial information about an entity

and the auditor’s report. Independent audit report included in the annual report of the company

provides the stakeholders independent views on the nature of the financial information contained

in the annual report. It is important that the audit report includes all necessary aspects of an

effective audit and a valid opinion on the financial information of the entity in plain and simple

English. It is specifically important because the users of financial statements are not supposed to

have technical knowledge and skills to understand complex accounting and financial terms.

Thus, the audit report should be such to easily elaborate on different aspects of financial

reporting and their nature. This document would be helpful to the readers to understand different

aspects associated with an audit that an auditor must take into consideration during the course of

audit.

2

AUDIT ASSURANCE AND COMPLIANCE

Contents

Executive Summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Declaration of independence by the auditor:...................................................................................3

Independent auditor’s report:...........................................................................................................4

Non-audit services performed by the auditor:.................................................................................4

Analysis and comparison of auditor’s remuneration:......................................................................5

Audit committee:.............................................................................................................................7

Audit opinion:..................................................................................................................................8

Responsibilities of directors and management differs from that of the auditor:.............................8

Subsequent events:...........................................................................................................................8

Information reported in the audit reports and effectiveness of the same:........................................9

Material information missing:.......................................................................................................10

Follow up question:.......................................................................................................................10

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

AUDIT ASSURANCE AND COMPLIANCE

Contents

Executive Summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Declaration of independence by the auditor:...................................................................................3

Independent auditor’s report:...........................................................................................................4

Non-audit services performed by the auditor:.................................................................................4

Analysis and comparison of auditor’s remuneration:......................................................................5

Audit committee:.............................................................................................................................7

Audit opinion:..................................................................................................................................8

Responsibilities of directors and management differs from that of the auditor:.............................8

Subsequent events:...........................................................................................................................8

Information reported in the audit reports and effectiveness of the same:........................................9

Material information missing:.......................................................................................................10

Follow up question:.......................................................................................................................10

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT ASSURANCE AND COMPLIANCE

Introduction:

Life Style Communities Limited is an Australia based company that provides top quality

facilities to the citizens of the country for building and developing suitable communities. The

company provides working, semi-working and retired people with opportunities to live luxury

life at affordable prices. The company operates as land lease communities and since its formation

has made a niche place in the community building and development market. In this document a

detailed discussion on the audit of the company shall be made. The objective is to independently

appraisal the audit work Pitcher Partners in relation to the audit of the company.

Declaration of independence by the auditor:

Pitcher Partners is the auditor of Life Style Communities Limited and has the responsibility to

independently verify the financial information and make a report on the findings of the audit at

the end of the audit. The corporations and entities operating in Australia are governed by the

provisions of Corporations Act, 2001, to be referred to as the act only in this document

(Woiwode et. al. 2016). The act requires (s307C, of the act to be specific) an auditor to

compulsorily make a declaration of independence before proceeding to conduct audit on the

financial statements of an entity in the country. In the annual report 2018 of the company, Pitcher

Partners have complied with the requirements of s307C of the act by providing a declaration of

independence. In the declaration of independence statement the auditor has clearly mentioned

that in relation to the audit of the company for the year ending on 30th June, 2018 the auditor has

not contravened with any of the requirements of independence and the audit has been conducted

in accordance with the APES 110, code of ethics for professional accountant (Knechel and

Salterio, 2016).

AUDIT ASSURANCE AND COMPLIANCE

Introduction:

Life Style Communities Limited is an Australia based company that provides top quality

facilities to the citizens of the country for building and developing suitable communities. The

company provides working, semi-working and retired people with opportunities to live luxury

life at affordable prices. The company operates as land lease communities and since its formation

has made a niche place in the community building and development market. In this document a

detailed discussion on the audit of the company shall be made. The objective is to independently

appraisal the audit work Pitcher Partners in relation to the audit of the company.

Declaration of independence by the auditor:

Pitcher Partners is the auditor of Life Style Communities Limited and has the responsibility to

independently verify the financial information and make a report on the findings of the audit at

the end of the audit. The corporations and entities operating in Australia are governed by the

provisions of Corporations Act, 2001, to be referred to as the act only in this document

(Woiwode et. al. 2016). The act requires (s307C, of the act to be specific) an auditor to

compulsorily make a declaration of independence before proceeding to conduct audit on the

financial statements of an entity in the country. In the annual report 2018 of the company, Pitcher

Partners have complied with the requirements of s307C of the act by providing a declaration of

independence. In the declaration of independence statement the auditor has clearly mentioned

that in relation to the audit of the company for the year ending on 30th June, 2018 the auditor has

not contravened with any of the requirements of independence and the audit has been conducted

in accordance with the APES 110, code of ethics for professional accountant (Knechel and

Salterio, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT ASSURANCE AND COMPLIANCE

Independent auditor’s report:

Corporations Act, 2001 and Australian Standards on Auditing (ASAs) guide a

professional accountant to conduct an in audit in accordance with the applicable provisions to

effectively discharge his duties as an auditor. An auditor must provide an independent audit

report at the end of the audit to the company. In the independent audit report the auditor discloses

how the audit has been conducted along with key audit matters. The report also explains the

responsibility of the auditor and the opinion of the auditor on the financial statements prepared

by the company (Ahmed Haji and Anifowose, 2016).

Opinion on financial information of the company:

The auditor has expressed an unqualified opinion on the financial reports of the company.

According to the auditor the accompanying financial reports of the company has been prepared

in accordance with the provision of Corporations Act, 2001 and these report show the true and

fair picture of the company’s financial performance and position. The auditor has also mentioned

that the financial reports have been prepared in accordance with the Australian Accounting

Standards (AASBs) (Alzeban and Sawan, 2015).

Non-audit services performed by the auditor:

One of the yardsticks used to determine whether an auditor has violated any of the independence

requirements is the non-audit services. The auditors are not allowed to provide certain types of

non-audit services such as book keeping services, consultancy for management of internal

security and controls, internal audit services, consultancy on day to day to business matters and

managerial services. Apart from that an auditor can provide non-audit services without violating

the requirements of independence (Heenetigala et. al. 2016).

AUDIT ASSURANCE AND COMPLIANCE

Independent auditor’s report:

Corporations Act, 2001 and Australian Standards on Auditing (ASAs) guide a

professional accountant to conduct an in audit in accordance with the applicable provisions to

effectively discharge his duties as an auditor. An auditor must provide an independent audit

report at the end of the audit to the company. In the independent audit report the auditor discloses

how the audit has been conducted along with key audit matters. The report also explains the

responsibility of the auditor and the opinion of the auditor on the financial statements prepared

by the company (Ahmed Haji and Anifowose, 2016).

Opinion on financial information of the company:

The auditor has expressed an unqualified opinion on the financial reports of the company.

According to the auditor the accompanying financial reports of the company has been prepared

in accordance with the provision of Corporations Act, 2001 and these report show the true and

fair picture of the company’s financial performance and position. The auditor has also mentioned

that the financial reports have been prepared in accordance with the Australian Accounting

Standards (AASBs) (Alzeban and Sawan, 2015).

Non-audit services performed by the auditor:

One of the yardsticks used to determine whether an auditor has violated any of the independence

requirements is the non-audit services. The auditors are not allowed to provide certain types of

non-audit services such as book keeping services, consultancy for management of internal

security and controls, internal audit services, consultancy on day to day to business matters and

managerial services. Apart from that an auditor can provide non-audit services without violating

the requirements of independence (Heenetigala et. al. 2016).

5

AUDIT ASSURANCE AND COMPLIANCE

Pitcher Partners have not provided any of the non-audit services that are in contravention with

the requirements of independence as pert the provisions of the Corporations Act, 2001. Apart

from the auditing services as required for the audit of the company the auditor has only provided

consultancy and advice on general tax and GST related matters to help the company to comply

with taxation laws and provisions better (Christopher, 2015).

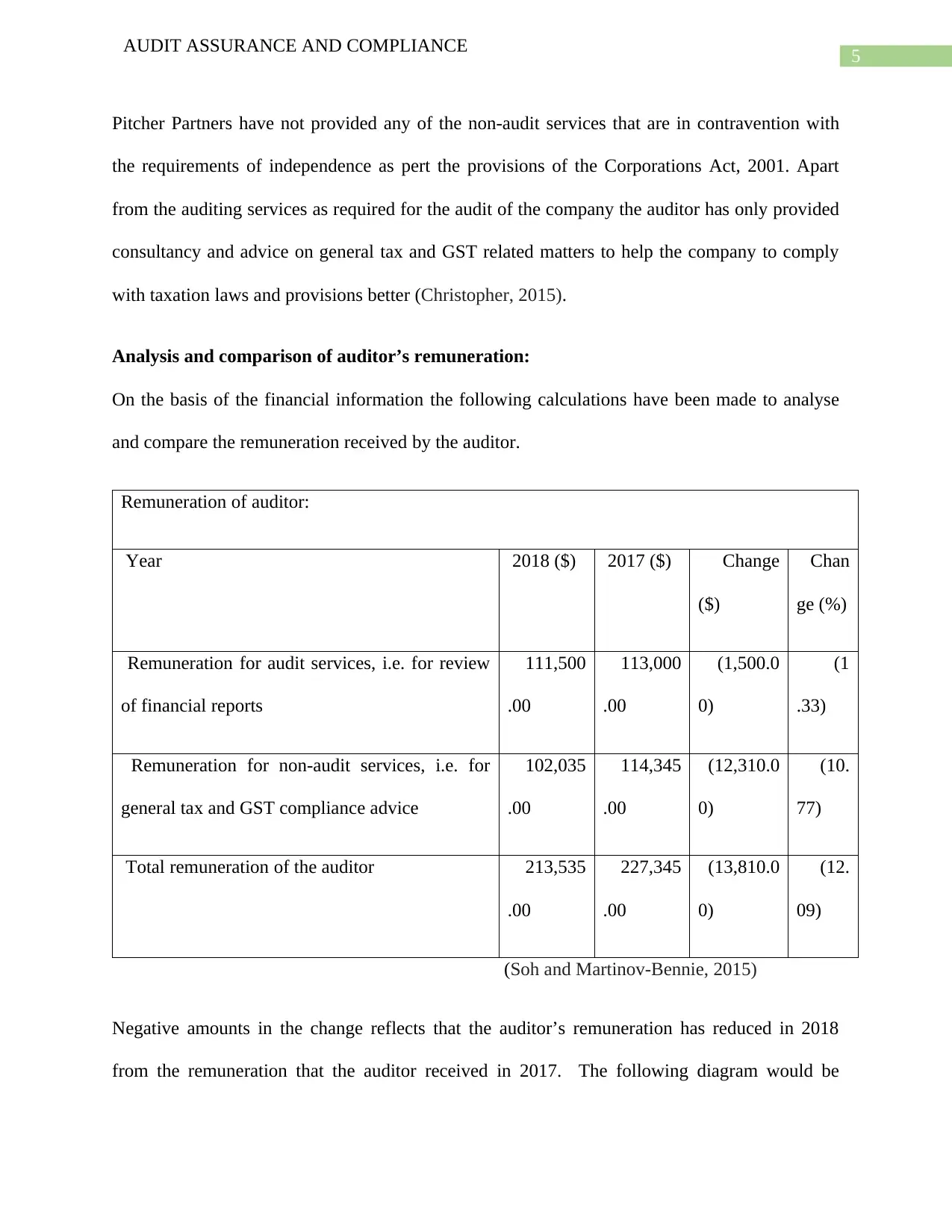

Analysis and comparison of auditor’s remuneration:

On the basis of the financial information the following calculations have been made to analyse

and compare the remuneration received by the auditor.

Remuneration of auditor:

Year 2018 ($) 2017 ($) Change

($)

Chan

ge (%)

Remuneration for audit services, i.e. for review

of financial reports

111,500

.00

113,000

.00

(1,500.0

0)

(1

.33)

Remuneration for non-audit services, i.e. for

general tax and GST compliance advice

102,035

.00

114,345

.00

(12,310.0

0)

(10.

77)

Total remuneration of the auditor 213,535

.00

227,345

.00

(13,810.0

0)

(12.

09)

(Soh and Martinov-Bennie, 2015)

Negative amounts in the change reflects that the auditor’s remuneration has reduced in 2018

from the remuneration that the auditor received in 2017. The following diagram would be

AUDIT ASSURANCE AND COMPLIANCE

Pitcher Partners have not provided any of the non-audit services that are in contravention with

the requirements of independence as pert the provisions of the Corporations Act, 2001. Apart

from the auditing services as required for the audit of the company the auditor has only provided

consultancy and advice on general tax and GST related matters to help the company to comply

with taxation laws and provisions better (Christopher, 2015).

Analysis and comparison of auditor’s remuneration:

On the basis of the financial information the following calculations have been made to analyse

and compare the remuneration received by the auditor.

Remuneration of auditor:

Year 2018 ($) 2017 ($) Change

($)

Chan

ge (%)

Remuneration for audit services, i.e. for review

of financial reports

111,500

.00

113,000

.00

(1,500.0

0)

(1

.33)

Remuneration for non-audit services, i.e. for

general tax and GST compliance advice

102,035

.00

114,345

.00

(12,310.0

0)

(10.

77)

Total remuneration of the auditor 213,535

.00

227,345

.00

(13,810.0

0)

(12.

09)

(Soh and Martinov-Bennie, 2015)

Negative amounts in the change reflects that the auditor’s remuneration has reduced in 2018

from the remuneration that the auditor received in 2017. The following diagram would be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT ASSURANCE AND COMPLIANCE

helpful to understand the differences between the remuneration received by the auditor in 2017

and in 2018.

-

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

Remneration of auditor

2018 ($) 2017 ($)

In 2018 the auditor has received $111,500 for review and verification of financial reports and

$102,035 for taxation consultancy services totalling to $213,535. In 2017 the auditor’s

remuneration totalled to $227,345. Both remuneration for audit services and non-audit services

have decreased in 2018 (Bepari and Mollik, 2016).

Key audit matters:

The auditor has disclosed key audit matters (KAM) that he believed influences the financial

performance and position of the company. According to the auditor the following are the KAM

for the audit of the company (Lisic et. al. 2016).

Investment properties: The value of investment properties as per the valuation method used by

the company is $303.6 million. In order to verify the balance of investment properties reported in

AUDIT ASSURANCE AND COMPLIANCE

helpful to understand the differences between the remuneration received by the auditor in 2017

and in 2018.

-

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

Remneration of auditor

2018 ($) 2017 ($)

In 2018 the auditor has received $111,500 for review and verification of financial reports and

$102,035 for taxation consultancy services totalling to $213,535. In 2017 the auditor’s

remuneration totalled to $227,345. Both remuneration for audit services and non-audit services

have decreased in 2018 (Bepari and Mollik, 2016).

Key audit matters:

The auditor has disclosed key audit matters (KAM) that he believed influences the financial

performance and position of the company. According to the auditor the following are the KAM

for the audit of the company (Lisic et. al. 2016).

Investment properties: The value of investment properties as per the valuation method used by

the company is $303.6 million. In order to verify the balance of investment properties reported in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT ASSURANCE AND COMPLIANCE

the financial statements the auditor has used extended substantive procedures on the investment

properties of the company (Cohen, Krishnamoorthy and Wright, 2017).

The amount of investment properties is by far the largest asset in the Balance sheet of the

company. In fact $303.6 million of investment properties approximates to 84.7% of the total

assets of Balance sheet. The auditor has provided significant attention on the valuation method

used by the entity to ensure that investments have been valued appropriately (DeZoort and

Taylor, 2015). Investment has been correctly valued using fair value method. The auditor has

evaluated the report of valuation that the management has obtained from external property

valuation organization. The key inputs used in the valuation has been evaluated by the auditor to

assess whether the inputs are appropriate or not. Apart from that the properties that were nor

subjected to external valuation have also been reviewed and assessed by the auditor. The key

inputs and assumptions have been challenged to evaluate whether these are appropriate to the

particular circumstances (Dhaliwal et. al. 2015).

Audit committee:

The company has as per the recommendation of the auditing and assurance standards board has

constituted an audit committee. The audit committee of the company has been constituted as per

the provisions of the Corporations Act, 2001. The committee is only comprised on non-executive

directors. The Committee has in total 4 members, all of them are non-executive directors of the

company (Tepalagul and Lin, 2015).

Structure, functions and responsibilities of audit committee:

The audit committee is comprises of 4 non-executive members and must meet at-least four times

in a year with not more than 120 days gap between two consecutive meetings of the audit

AUDIT ASSURANCE AND COMPLIANCE

the financial statements the auditor has used extended substantive procedures on the investment

properties of the company (Cohen, Krishnamoorthy and Wright, 2017).

The amount of investment properties is by far the largest asset in the Balance sheet of the

company. In fact $303.6 million of investment properties approximates to 84.7% of the total

assets of Balance sheet. The auditor has provided significant attention on the valuation method

used by the entity to ensure that investments have been valued appropriately (DeZoort and

Taylor, 2015). Investment has been correctly valued using fair value method. The auditor has

evaluated the report of valuation that the management has obtained from external property

valuation organization. The key inputs used in the valuation has been evaluated by the auditor to

assess whether the inputs are appropriate or not. Apart from that the properties that were nor

subjected to external valuation have also been reviewed and assessed by the auditor. The key

inputs and assumptions have been challenged to evaluate whether these are appropriate to the

particular circumstances (Dhaliwal et. al. 2015).

Audit committee:

The company has as per the recommendation of the auditing and assurance standards board has

constituted an audit committee. The audit committee of the company has been constituted as per

the provisions of the Corporations Act, 2001. The committee is only comprised on non-executive

directors. The Committee has in total 4 members, all of them are non-executive directors of the

company (Tepalagul and Lin, 2015).

Structure, functions and responsibilities of audit committee:

The audit committee is comprises of 4 non-executive members and must meet at-least four times

in a year with not more than 120 days gap between two consecutive meetings of the audit

8

AUDIT ASSURANCE AND COMPLIANCE

committee. The audit committee charter of the company states that the members of the audit

committee must meet at regular intervals to discuss and improve the quality of internal controls

and securities. The members of the audit committee is responsible to coordinate with the

members of internal auditing team to discuss the steps to be taken to improve the financial

reporting and operational efficiency within the organization. The audit committee also has the

role to coordinate with the external auditors and ensure that the auditors get all necessary

cooperation from the employees and workers of the company to conduct the audit effectively

(Badolato, Donelson and Ege, 2014).

Audit opinion:

As already mentioned earlier that the auditor of the company has expressed an unqualified

opinion on the financial information of the company.

Responsibilities of directors and management differs from that of the auditor:

As per s307C an auditor must conduct an independent verification of the financial reports of an

organization with the objectives of expressing an opinion on the quality of financial reporting.

Thus, the auditor is only responsible to verify the financial statements and report on it. However,

the directors and the management of an entity is wholly responsible to maintain books of

accounts and prepare and present financial reports of the entity from the books of accounts in

accordance with the provisions of Corporations Act 2001 and AASBs. Thus, there is a sharp

difference between the responsibilities of the auditor and the management & directors (AICPA,

2017).

AUDIT ASSURANCE AND COMPLIANCE

committee. The audit committee charter of the company states that the members of the audit

committee must meet at regular intervals to discuss and improve the quality of internal controls

and securities. The members of the audit committee is responsible to coordinate with the

members of internal auditing team to discuss the steps to be taken to improve the financial

reporting and operational efficiency within the organization. The audit committee also has the

role to coordinate with the external auditors and ensure that the auditors get all necessary

cooperation from the employees and workers of the company to conduct the audit effectively

(Badolato, Donelson and Ege, 2014).

Audit opinion:

As already mentioned earlier that the auditor of the company has expressed an unqualified

opinion on the financial information of the company.

Responsibilities of directors and management differs from that of the auditor:

As per s307C an auditor must conduct an independent verification of the financial reports of an

organization with the objectives of expressing an opinion on the quality of financial reporting.

Thus, the auditor is only responsible to verify the financial statements and report on it. However,

the directors and the management of an entity is wholly responsible to maintain books of

accounts and prepare and present financial reports of the entity from the books of accounts in

accordance with the provisions of Corporations Act 2001 and AASBs. Thus, there is a sharp

difference between the responsibilities of the auditor and the management & directors (AICPA,

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT ASSURANCE AND COMPLIANCE

Subsequent events:

The company has paid dividend to the shareholders after the end of the financial year. Except

this there has been no subsequent event that has occurred between the periods from end of the

financial year to the date of audit report. The company paid a dividend of $4,181,805 after the

closure of financial year on 30th June, 2018. The company has been quite regular when it comes

to payment of dividend to the shareholders of the company (Byrnes et. al. 2018).

Information reported in the audit reports and effectiveness of the same:

An auditor is appointed by an entity to provide an independent audit report after verifying the

financial information of the entity. The objective of external audit is to provide the entity and its

stakeholders with an independent appraisal report on the financial statements of the entity. Since

most the stakeholders had to rely on the financial reports of an entity to take important decisions

affecting their interests in the entity, it is desirable to have an effective independent audit report

outlining all material information required by the stakeholders to correctly assess the financial

state and performance of the entity (Renzi, Whitaker and Wardle, 2015).

Taking into consideration this it is clear that Pitcher Partners, the auditor of Life Style

Communities Limited, has included all standard information as per the requirements of

Corporations Act, 2001 and the Auditing standards applicable in the country. All the

requirements of material information as per the provisions of the act and the ASAs have been

met by the auditor of the company (Alles et. al. 2018). However, since the stakeholders are

looking to take important decisions in the future thus, it would be very helpful to the

stakeholders if the audit report of an entity contains certain aspects of verification on the future

strategies of the entity and appropriateness of underlying variables and assumptions used by the

entity while providing forecasting future performance. Thus, inclusion of futuristic perspective in

AUDIT ASSURANCE AND COMPLIANCE

Subsequent events:

The company has paid dividend to the shareholders after the end of the financial year. Except

this there has been no subsequent event that has occurred between the periods from end of the

financial year to the date of audit report. The company paid a dividend of $4,181,805 after the

closure of financial year on 30th June, 2018. The company has been quite regular when it comes

to payment of dividend to the shareholders of the company (Byrnes et. al. 2018).

Information reported in the audit reports and effectiveness of the same:

An auditor is appointed by an entity to provide an independent audit report after verifying the

financial information of the entity. The objective of external audit is to provide the entity and its

stakeholders with an independent appraisal report on the financial statements of the entity. Since

most the stakeholders had to rely on the financial reports of an entity to take important decisions

affecting their interests in the entity, it is desirable to have an effective independent audit report

outlining all material information required by the stakeholders to correctly assess the financial

state and performance of the entity (Renzi, Whitaker and Wardle, 2015).

Taking into consideration this it is clear that Pitcher Partners, the auditor of Life Style

Communities Limited, has included all standard information as per the requirements of

Corporations Act, 2001 and the Auditing standards applicable in the country. All the

requirements of material information as per the provisions of the act and the ASAs have been

met by the auditor of the company (Alles et. al. 2018). However, since the stakeholders are

looking to take important decisions in the future thus, it would be very helpful to the

stakeholders if the audit report of an entity contains certain aspects of verification on the future

strategies of the entity and appropriateness of underlying variables and assumptions used by the

entity while providing forecasting future performance. Thus, inclusion of futuristic perspective in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT ASSURANCE AND COMPLIANCE

audit report would help the stakeholders of an organization to take important decisions affecting

their interests in the organization (Chan and Vasarhelyi, 2018).

Material information missing:

From a detailed appraisal of the audit procedures performed by the auditor of the company and

verification of the independent audit report it is clear that the independent audit report of the

company includes all information that is material to the assessment of financial performance and

position of the company. No material information is missing in the audit report of the company

as per the requirements of Corporations Act, 2001 and ASAs. However, as mentioned earlier it

would have been great to include assessment of future strategies and forecasting statements of

the company to help the stakeholders to take important decision affecting their interests in the

company. Thus, the auditor has disclosed all material information with necessary explanations in

the independent audit report of the company (Appelbaum, Kogan and Vasarhelyi, 2017).

Follow up question:

Though the auditor has conducted the audit in accordance with the applicable standards on

auditing (ASAs) and provisions of Corporations act, 2001 however, the missing aspect of future

forecasting assessment report is certainly an important consideration. Thus, the follow up

question to be asked to the auditor is as following:

When will the auditing and assurance standards in the country consider including assessment of

forecasting statements of an entity?

Conclusion:

Considering the independent appraisal of audit work performed by Pitcher Partners it is safe to

say that appropriate audit procedures have been performed by the auditor to issue independent

AUDIT ASSURANCE AND COMPLIANCE

audit report would help the stakeholders of an organization to take important decisions affecting

their interests in the organization (Chan and Vasarhelyi, 2018).

Material information missing:

From a detailed appraisal of the audit procedures performed by the auditor of the company and

verification of the independent audit report it is clear that the independent audit report of the

company includes all information that is material to the assessment of financial performance and

position of the company. No material information is missing in the audit report of the company

as per the requirements of Corporations Act, 2001 and ASAs. However, as mentioned earlier it

would have been great to include assessment of future strategies and forecasting statements of

the company to help the stakeholders to take important decision affecting their interests in the

company. Thus, the auditor has disclosed all material information with necessary explanations in

the independent audit report of the company (Appelbaum, Kogan and Vasarhelyi, 2017).

Follow up question:

Though the auditor has conducted the audit in accordance with the applicable standards on

auditing (ASAs) and provisions of Corporations act, 2001 however, the missing aspect of future

forecasting assessment report is certainly an important consideration. Thus, the follow up

question to be asked to the auditor is as following:

When will the auditing and assurance standards in the country consider including assessment of

forecasting statements of an entity?

Conclusion:

Considering the independent appraisal of audit work performed by Pitcher Partners it is safe to

say that appropriate audit procedures have been performed by the auditor to issue independent

11

AUDIT ASSURANCE AND COMPLIANCE

audit report on the quality of financial reporting of the company. Each and every single aspect of

auditing has been documented by the auditor in the audit report to provide the users of financial

statements with substantial information to correctly assess the financial state and performance of

the company.

AUDIT ASSURANCE AND COMPLIANCE

audit report on the quality of financial reporting of the company. Each and every single aspect of

auditing has been documented by the auditor in the audit report to provide the users of financial

statements with substantial information to correctly assess the financial state and performance of

the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.