HI6026 Audit, Assurance and Compliance Report on BHP Billiton 2018

VerifiedAdded on 2023/06/05

|14

|3283

|163

Report

AI Summary

This report provides a detailed analysis of the audit, assurance, and compliance aspects of BHP Billiton, focusing on the HI6026 course. It begins with an executive summary highlighting the audit report's focus on auditor responsibilities, independence, and the audit opinion. The introduction sets the stage by emphasizing the role of auditors and the International Auditing and Assurance Board's guidelines. The report then delves into auditor independence, non-audit services provided by KPMG, and auditor remuneration, including a breakdown of fees. Key audit matters are examined, including audit procedures and classifications, and the audit committee structure, functions, and responsibilities are outlined. The report also compares the responsibilities of management and auditors, discusses material subsequent events, and concludes with a summary of the findings. References support the analysis of the audit report and annual report of the company.

HI6026 Audit, Assurance and Compliance

Trimester 2 2018

1

Trimester 2 2018

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report emphasises upon the audit report and auditor’s responsibilities, their

independences, opinion and audit activities and audit program undertaken by the auditors.

BHP Billiton Company has been chosen for this assignment to prepare the report on the audit

opinion and their responsibilities towards the stakeholders. Each and every company needs to

take audit report of their prepared financial statements before filing it with the financial

authority. There are several auditing and non-auditing services have been given by the

auditors to company. This report explained the role of the auditors, responsibilities and their

opinion given to company on the basis of the audit performed on the annual report of

company.

2

This report emphasises upon the audit report and auditor’s responsibilities, their

independences, opinion and audit activities and audit program undertaken by the auditors.

BHP Billiton Company has been chosen for this assignment to prepare the report on the audit

opinion and their responsibilities towards the stakeholders. Each and every company needs to

take audit report of their prepared financial statements before filing it with the financial

authority. There are several auditing and non-auditing services have been given by the

auditors to company. This report explained the role of the auditors, responsibilities and their

opinion given to company on the basis of the audit performed on the annual report of

company.

2

Table of Contents

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................3

AUDITOR’S INDEPENDENCE...............................................................................................3

PROVISION OF NON-AUDIT SERVICES.............................................................................3

AUDITER REMUNERATION.................................................................................................4

KEY AUDIT MATTERS..........................................................................................................4

AUDIT COMMITTEE & AUDIT CHARTER.........................................................................6

STRUCTURE............................................................................................................................6

FUNCTIONS.............................................................................................................................6

RESPONSIBILITIES.................................................................................................................6

AUDIT OPINION......................................................................................................................7

DIFFERENCE BETWEEN THE RESPONSIBILITIES OF MANAGEMENT AND

AUDITOR..................................................................................................................................7

MATERIAL SUBSEQUENT EVENTS....................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................8

3

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................3

AUDITOR’S INDEPENDENCE...............................................................................................3

PROVISION OF NON-AUDIT SERVICES.............................................................................3

AUDITER REMUNERATION.................................................................................................4

KEY AUDIT MATTERS..........................................................................................................4

AUDIT COMMITTEE & AUDIT CHARTER.........................................................................6

STRUCTURE............................................................................................................................6

FUNCTIONS.............................................................................................................................6

RESPONSIBILITIES.................................................................................................................6

AUDIT OPINION......................................................................................................................7

DIFFERENCE BETWEEN THE RESPONSIBILITIES OF MANAGEMENT AND

AUDITOR..................................................................................................................................7

MATERIAL SUBSEQUENT EVENTS....................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................8

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

This report emphasises upon the auditing requirement and role played by auditors in

organization. The international auditing assurance board have been several audit assurance

program which needs to be followed by auditors while preparing the financial statements.

This report reveals the declaration for the auditor’s independence, auditor’s roles and given

audit services. The audit report analysis of the BHP Billiton is done by evaluating the audit

report and annual report of company. This report assists in evaluating the audit program and

disclaimer given by auditors in its audit report. In addition to this, auditors need to comply

with the certain audit rules and regulations while auditing the financial statements of

company. In context with the further details of company it is analyzed that the outgoing

chairman of the company is Jac Nasser and the incoming chairman is Ken Mackenzie and the

chief executive officer of the company Andrew Mackenzie (BHP Billiton Company. 2016).

In this report, the main detail explained the role of the auditors, responsibilities and their

opinion given to company on the basis of the audit performed on the annual report of

company.

AUDITOR’S INDEPENDENCE

It is analyzed that auditor’s independence is based on the several factors such as their

relation with company and time they have spent while auditing the financial statement of

particular company Auditors who are auditing the financial statement of company should not

be having any pecuniary relation with the company in any manner. Currently, the financial

statement of company is audited by the biggest audit firm named KPMG. However, in future,

EY will be hired as new auditors to audit to financial statement of company (BHP Billiton

Company. 2016).

It is analyzed that audit committee should also be convinced by auditors that the auditors are

independents in their operations will be allowed to check the financial statements. However,

in this case, in order to justify the auditor’s independence auditors needs to give declaration

regarding with the independence in written. In this written declaration, they will state that

they are not having any sort of pecuniary relation with the company. Nonetheless, it is

considered that auditors are in the fiduciary position of company and takes all the required

actions in the best interest of the stakeholders. Therefore, they should be having no relation

with the company and independently audit the financial statement of company so that it could

4

This report emphasises upon the auditing requirement and role played by auditors in

organization. The international auditing assurance board have been several audit assurance

program which needs to be followed by auditors while preparing the financial statements.

This report reveals the declaration for the auditor’s independence, auditor’s roles and given

audit services. The audit report analysis of the BHP Billiton is done by evaluating the audit

report and annual report of company. This report assists in evaluating the audit program and

disclaimer given by auditors in its audit report. In addition to this, auditors need to comply

with the certain audit rules and regulations while auditing the financial statements of

company. In context with the further details of company it is analyzed that the outgoing

chairman of the company is Jac Nasser and the incoming chairman is Ken Mackenzie and the

chief executive officer of the company Andrew Mackenzie (BHP Billiton Company. 2016).

In this report, the main detail explained the role of the auditors, responsibilities and their

opinion given to company on the basis of the audit performed on the annual report of

company.

AUDITOR’S INDEPENDENCE

It is analyzed that auditor’s independence is based on the several factors such as their

relation with company and time they have spent while auditing the financial statement of

particular company Auditors who are auditing the financial statement of company should not

be having any pecuniary relation with the company in any manner. Currently, the financial

statement of company is audited by the biggest audit firm named KPMG. However, in future,

EY will be hired as new auditors to audit to financial statement of company (BHP Billiton

Company. 2016).

It is analyzed that audit committee should also be convinced by auditors that the auditors are

independents in their operations will be allowed to check the financial statements. However,

in this case, in order to justify the auditor’s independence auditors needs to give declaration

regarding with the independence in written. In this written declaration, they will state that

they are not having any sort of pecuniary relation with the company. Nonetheless, it is

considered that auditors are in the fiduciary position of company and takes all the required

actions in the best interest of the stakeholders. Therefore, they should be having no relation

with the company and independently audit the financial statement of company so that it could

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

showcase the true and fair views to the stakeholders. Under section 307C of the Australian

corporation act 2001 the auditor's independence declared by KPMG. Under International

Financial Reporting Standards (IFRS's) the consolidated financial statements are prepared as

issued by the International accounting standard board (IASB). The directors are responsible

for the activities which are performed in the annual report (BHP Billiton Company. 2016).

PROVISION OF NON-AUDIT SERVICES

There are several audit services given by auditors to company. These non-audit

services are given to clients in addition to the audit services. However, auditors take

additional compensation for their non-audit services given to clients. These audit services are

given under the corporation act 2001 and only these services could be offered by clients to its

stakeholders. It is analyzed that if in any case, if these non-audit services offered by auditors

hamper the independence of the auditors then it should be deeply analysed by the directors

and would be disclosed in the annual report of company. In the financial statement of

company, it is showcased that the auditors offered tax compliance and setting up

harmonization in its domestic and international reporting to company and for the

consideration it has taken consideration worth $ 23 million from the company. Furthermore,

other non-audit services provided by KPMG to BHP Billiton are legal compliance program

for increasing the effectiveness of the financial statements, complying with the accounting

standards without hampering the prepared accounts (BHP Billiton Company. 2017) The main

consideration point is that every listed company needs to disclose in its annual report

whatever amount of consideration is given to auditors. Some non-audit services were

provided by the external auditors and their objectivity is they are free and safe through

restrictions on provision of these services. If there is the approval of Risk and Audit

committee (RAC)then such type of other than non-audit service are given by the auditors

otherwise the services are not undertaken at all (BHP Billiton Company. 2016). It is analyzed

that the

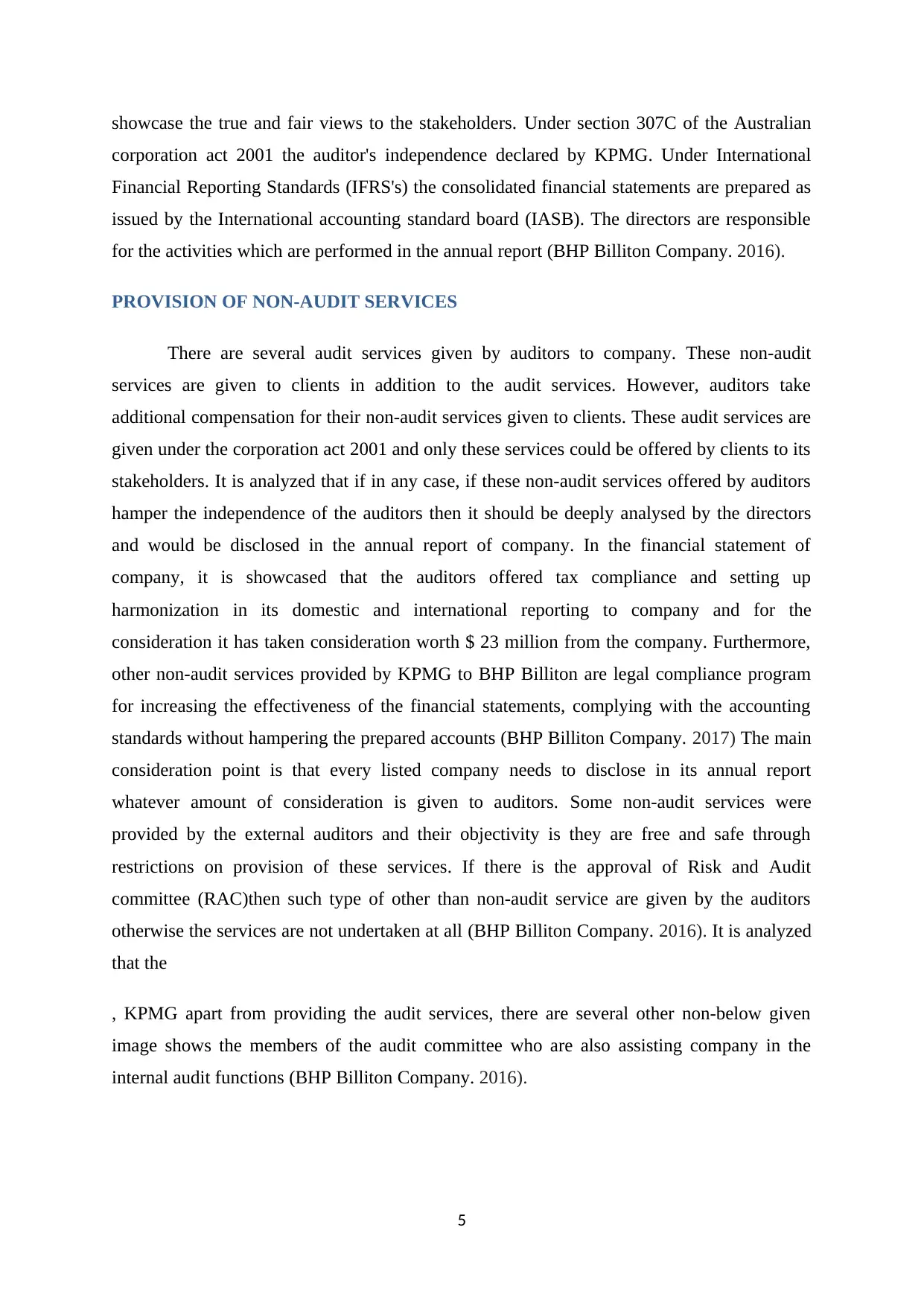

, KPMG apart from providing the audit services, there are several other non-below given

image shows the members of the audit committee who are also assisting company in the

internal audit functions (BHP Billiton Company. 2016).

5

corporation act 2001 the auditor's independence declared by KPMG. Under International

Financial Reporting Standards (IFRS's) the consolidated financial statements are prepared as

issued by the International accounting standard board (IASB). The directors are responsible

for the activities which are performed in the annual report (BHP Billiton Company. 2016).

PROVISION OF NON-AUDIT SERVICES

There are several audit services given by auditors to company. These non-audit

services are given to clients in addition to the audit services. However, auditors take

additional compensation for their non-audit services given to clients. These audit services are

given under the corporation act 2001 and only these services could be offered by clients to its

stakeholders. It is analyzed that if in any case, if these non-audit services offered by auditors

hamper the independence of the auditors then it should be deeply analysed by the directors

and would be disclosed in the annual report of company. In the financial statement of

company, it is showcased that the auditors offered tax compliance and setting up

harmonization in its domestic and international reporting to company and for the

consideration it has taken consideration worth $ 23 million from the company. Furthermore,

other non-audit services provided by KPMG to BHP Billiton are legal compliance program

for increasing the effectiveness of the financial statements, complying with the accounting

standards without hampering the prepared accounts (BHP Billiton Company. 2017) The main

consideration point is that every listed company needs to disclose in its annual report

whatever amount of consideration is given to auditors. Some non-audit services were

provided by the external auditors and their objectivity is they are free and safe through

restrictions on provision of these services. If there is the approval of Risk and Audit

committee (RAC)then such type of other than non-audit service are given by the auditors

otherwise the services are not undertaken at all (BHP Billiton Company. 2016). It is analyzed

that the

, KPMG apart from providing the audit services, there are several other non-below given

image shows the members of the audit committee who are also assisting company in the

internal audit functions (BHP Billiton Company. 2016).

5

(BHP Billiton Company. 2016).

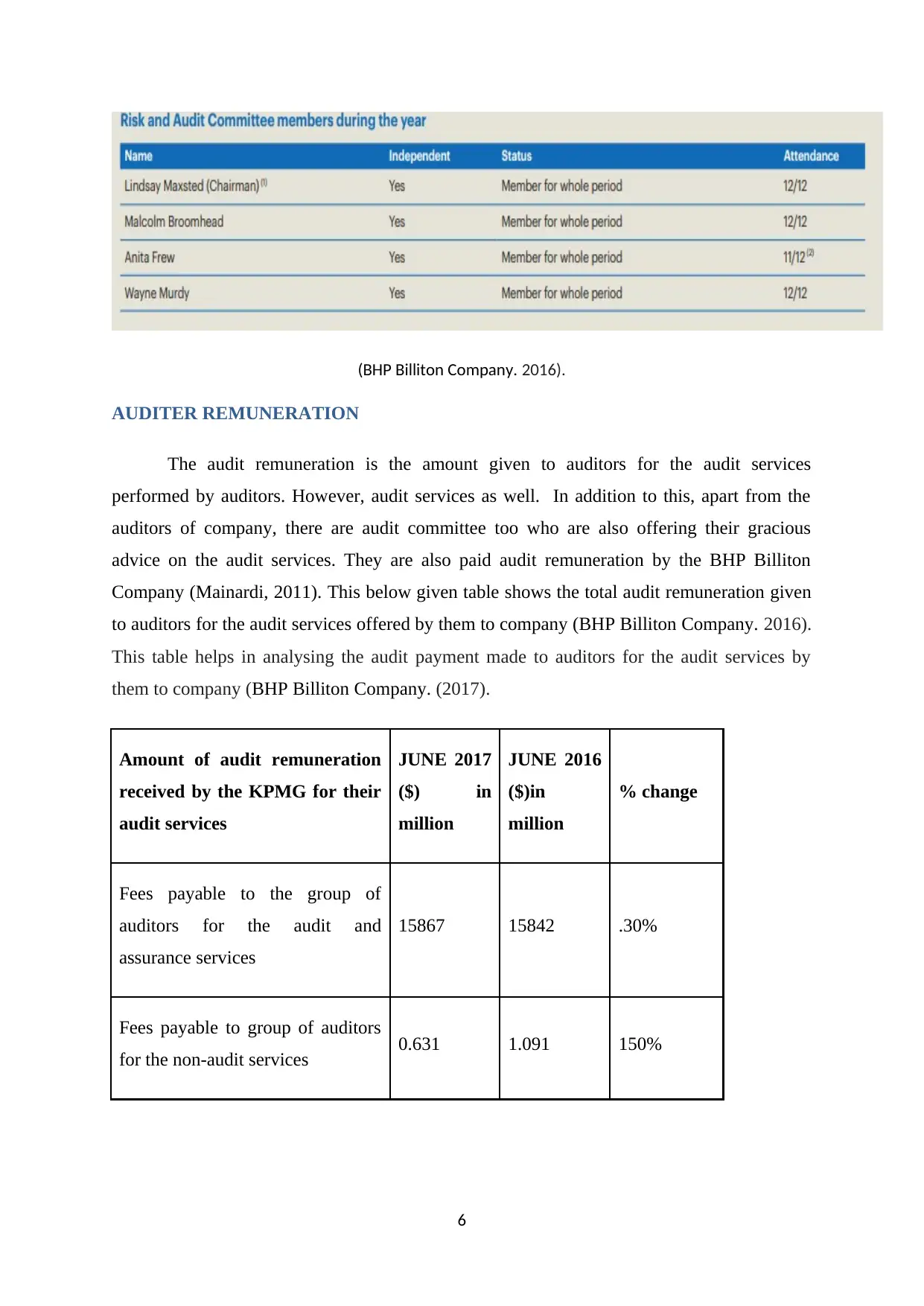

AUDITER REMUNERATION

The audit remuneration is the amount given to auditors for the audit services

performed by auditors. However, audit services as well. In addition to this, apart from the

auditors of company, there are audit committee too who are also offering their gracious

advice on the audit services. They are also paid audit remuneration by the BHP Billiton

Company (Mainardi, 2011). This below given table shows the total audit remuneration given

to auditors for the audit services offered by them to company (BHP Billiton Company. 2016).

This table helps in analysing the audit payment made to auditors for the audit services by

them to company (BHP Billiton Company. (2017).

Amount of audit remuneration

received by the KPMG for their

audit services

JUNE 2017

($) in

million

JUNE 2016

($)in

million

% change

Fees payable to the group of

auditors for the audit and

assurance services

15867 15842 .30%

Fees payable to group of auditors

for the non-audit services 0.631 1.091 150%

6

AUDITER REMUNERATION

The audit remuneration is the amount given to auditors for the audit services

performed by auditors. However, audit services as well. In addition to this, apart from the

auditors of company, there are audit committee too who are also offering their gracious

advice on the audit services. They are also paid audit remuneration by the BHP Billiton

Company (Mainardi, 2011). This below given table shows the total audit remuneration given

to auditors for the audit services offered by them to company (BHP Billiton Company. 2016).

This table helps in analysing the audit payment made to auditors for the audit services by

them to company (BHP Billiton Company. (2017).

Amount of audit remuneration

received by the KPMG for their

audit services

JUNE 2017

($) in

million

JUNE 2016

($)in

million

% change

Fees payable to the group of

auditors for the audit and

assurance services

15867 15842 .30%

Fees payable to group of auditors

for the non-audit services 0.631 1.091 150%

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The audit remunerations have been given to auditors for their audit and non-audit services.

However, the main issue arise due to the changes in exchange rate as the contract entered at

different exchange rate (BHP Billiton Company. 2016).

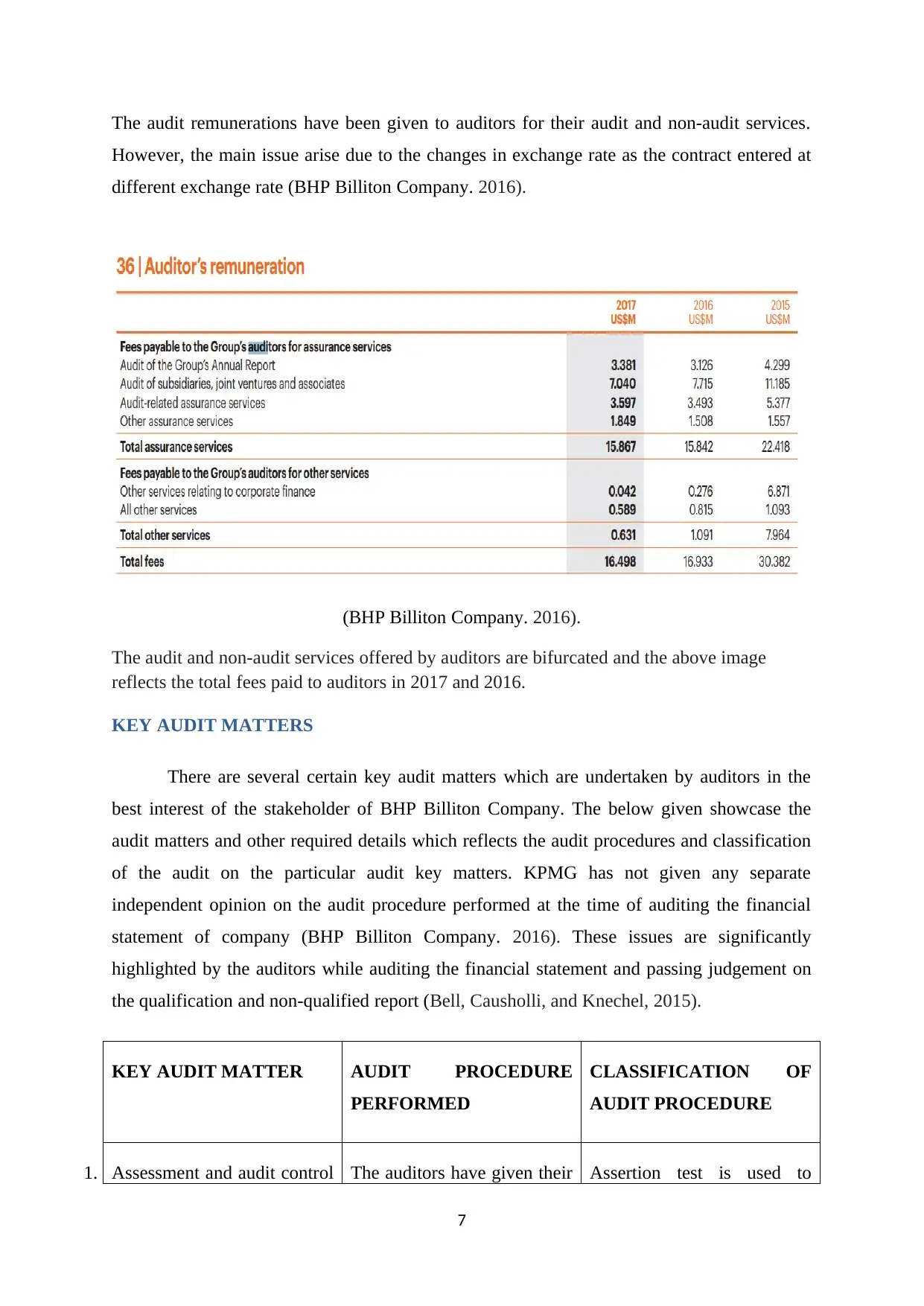

(BHP Billiton Company. 2016).

The audit and non-audit services offered by auditors are bifurcated and the above image

reflects the total fees paid to auditors in 2017 and 2016.

KEY AUDIT MATTERS

There are several certain key audit matters which are undertaken by auditors in the

best interest of the stakeholder of BHP Billiton Company. The below given showcase the

audit matters and other required details which reflects the audit procedures and classification

of the audit on the particular audit key matters. KPMG has not given any separate

independent opinion on the audit procedure performed at the time of auditing the financial

statement of company (BHP Billiton Company. 2016). These issues are significantly

highlighted by the auditors while auditing the financial statement and passing judgement on

the qualification and non-qualified report (Bell, Causholli, and Knechel, 2015).

KEY AUDIT MATTER AUDIT PROCEDURE

PERFORMED

CLASSIFICATION OF

AUDIT PROCEDURE

1. Assessment and audit control The auditors have given their Assertion test is used to

7

However, the main issue arise due to the changes in exchange rate as the contract entered at

different exchange rate (BHP Billiton Company. 2016).

(BHP Billiton Company. 2016).

The audit and non-audit services offered by auditors are bifurcated and the above image

reflects the total fees paid to auditors in 2017 and 2016.

KEY AUDIT MATTERS

There are several certain key audit matters which are undertaken by auditors in the

best interest of the stakeholder of BHP Billiton Company. The below given showcase the

audit matters and other required details which reflects the audit procedures and classification

of the audit on the particular audit key matters. KPMG has not given any separate

independent opinion on the audit procedure performed at the time of auditing the financial

statement of company (BHP Billiton Company. 2016). These issues are significantly

highlighted by the auditors while auditing the financial statement and passing judgement on

the qualification and non-qualified report (Bell, Causholli, and Knechel, 2015).

KEY AUDIT MATTER AUDIT PROCEDURE

PERFORMED

CLASSIFICATION OF

AUDIT PROCEDURE

1. Assessment and audit control The auditors have given their Assertion test is used to

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for the consolidating of the

financial statements

judgement on the basis of the

consolidating of the financial

statement of the other units is

done. They have taken proper

management representation

letter from directors and

management while auditing

the consolidated financial

statement. If any cases, BHP

Billiton made changes in its

accounting statements due to

the compliance with the

accounting standards and

other laws then the same

have been justified by the

directors in their MRL report

(BHP Billiton Company.

2016).

classify the assets.

Audit procedure is based on

the audit test undertaken by

the KMPG in its audit

functions (BHP Billiton

Company. 2016).

2. Undertaken strategic alliance

with other business units

Evaluation of the strategic

alliance with the other

business units is done by

assessing the required details.

Proper assessment is made

on the cash inflow and

outflow of cash from the

busienss. It has made proper

monitoring the financial

statement and recorded

accounts in the books of

Substantive test and

confirmation from the

relative external parties have

also been taken for the audit

evaluation.

8

financial statements

judgement on the basis of the

consolidating of the financial

statement of the other units is

done. They have taken proper

management representation

letter from directors and

management while auditing

the consolidated financial

statement. If any cases, BHP

Billiton made changes in its

accounting statements due to

the compliance with the

accounting standards and

other laws then the same

have been justified by the

directors in their MRL report

(BHP Billiton Company.

2016).

classify the assets.

Audit procedure is based on

the audit test undertaken by

the KMPG in its audit

functions (BHP Billiton

Company. 2016).

2. Undertaken strategic alliance

with other business units

Evaluation of the strategic

alliance with the other

business units is done by

assessing the required details.

Proper assessment is made

on the cash inflow and

outflow of cash from the

busienss. It has made proper

monitoring the financial

statement and recorded

accounts in the books of

Substantive test and

confirmation from the

relative external parties have

also been taken for the audit

evaluation.

8

accounts of company.

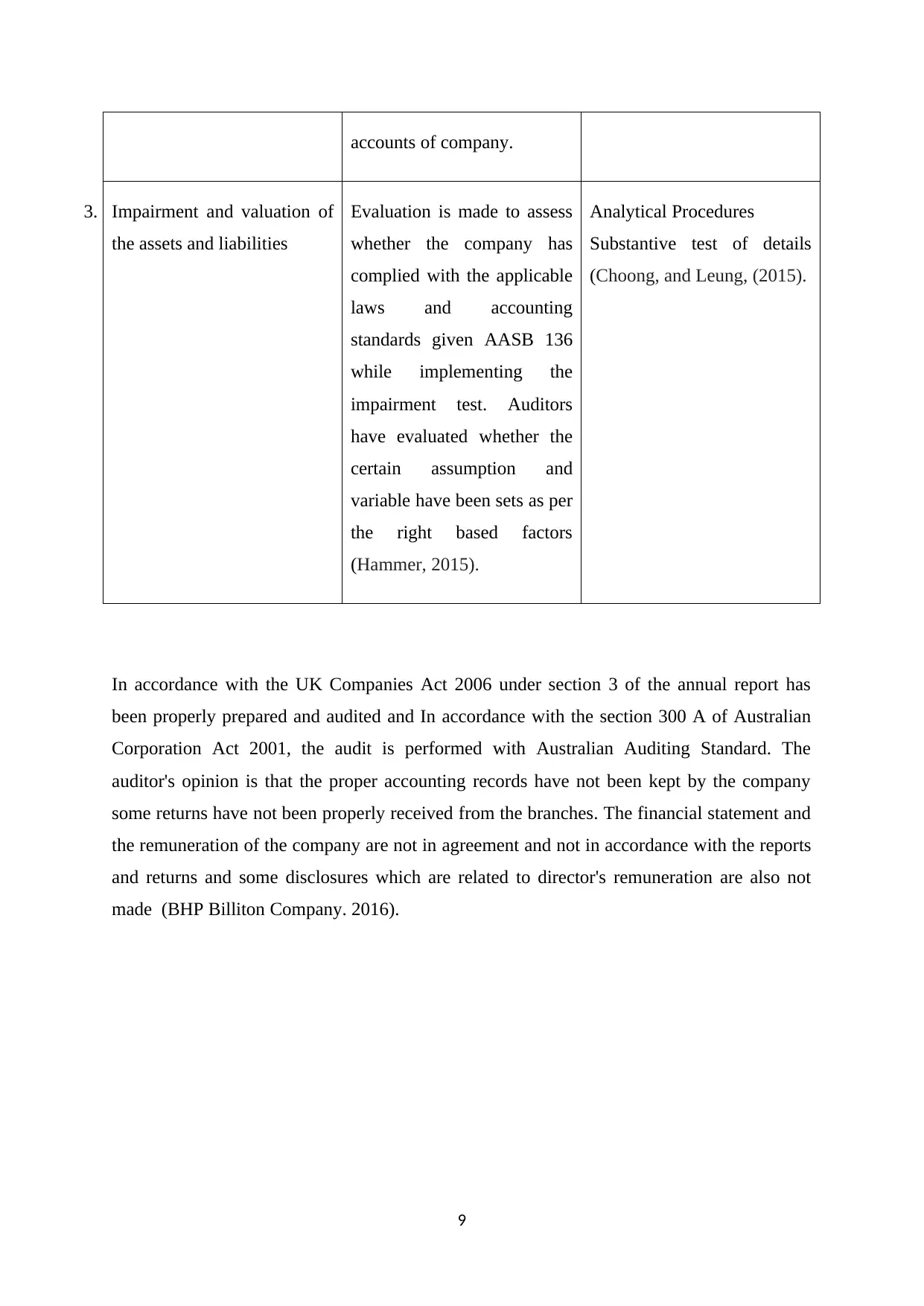

3. Impairment and valuation of

the assets and liabilities

Evaluation is made to assess

whether the company has

complied with the applicable

laws and accounting

standards given AASB 136

while implementing the

impairment test. Auditors

have evaluated whether the

certain assumption and

variable have been sets as per

the right based factors

(Hammer, 2015).

Analytical Procedures

Substantive test of details

(Choong, and Leung, (2015).

In accordance with the UK Companies Act 2006 under section 3 of the annual report has

been properly prepared and audited and In accordance with the section 300 A of Australian

Corporation Act 2001, the audit is performed with Australian Auditing Standard. The

auditor's opinion is that the proper accounting records have not been kept by the company

some returns have not been properly received from the branches. The financial statement and

the remuneration of the company are not in agreement and not in accordance with the reports

and returns and some disclosures which are related to director's remuneration are also not

made (BHP Billiton Company. 2016).

9

3. Impairment and valuation of

the assets and liabilities

Evaluation is made to assess

whether the company has

complied with the applicable

laws and accounting

standards given AASB 136

while implementing the

impairment test. Auditors

have evaluated whether the

certain assumption and

variable have been sets as per

the right based factors

(Hammer, 2015).

Analytical Procedures

Substantive test of details

(Choong, and Leung, (2015).

In accordance with the UK Companies Act 2006 under section 3 of the annual report has

been properly prepared and audited and In accordance with the section 300 A of Australian

Corporation Act 2001, the audit is performed with Australian Auditing Standard. The

auditor's opinion is that the proper accounting records have not been kept by the company

some returns have not been properly received from the branches. The financial statement and

the remuneration of the company are not in agreement and not in accordance with the reports

and returns and some disclosures which are related to director's remuneration are also not

made (BHP Billiton Company. 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

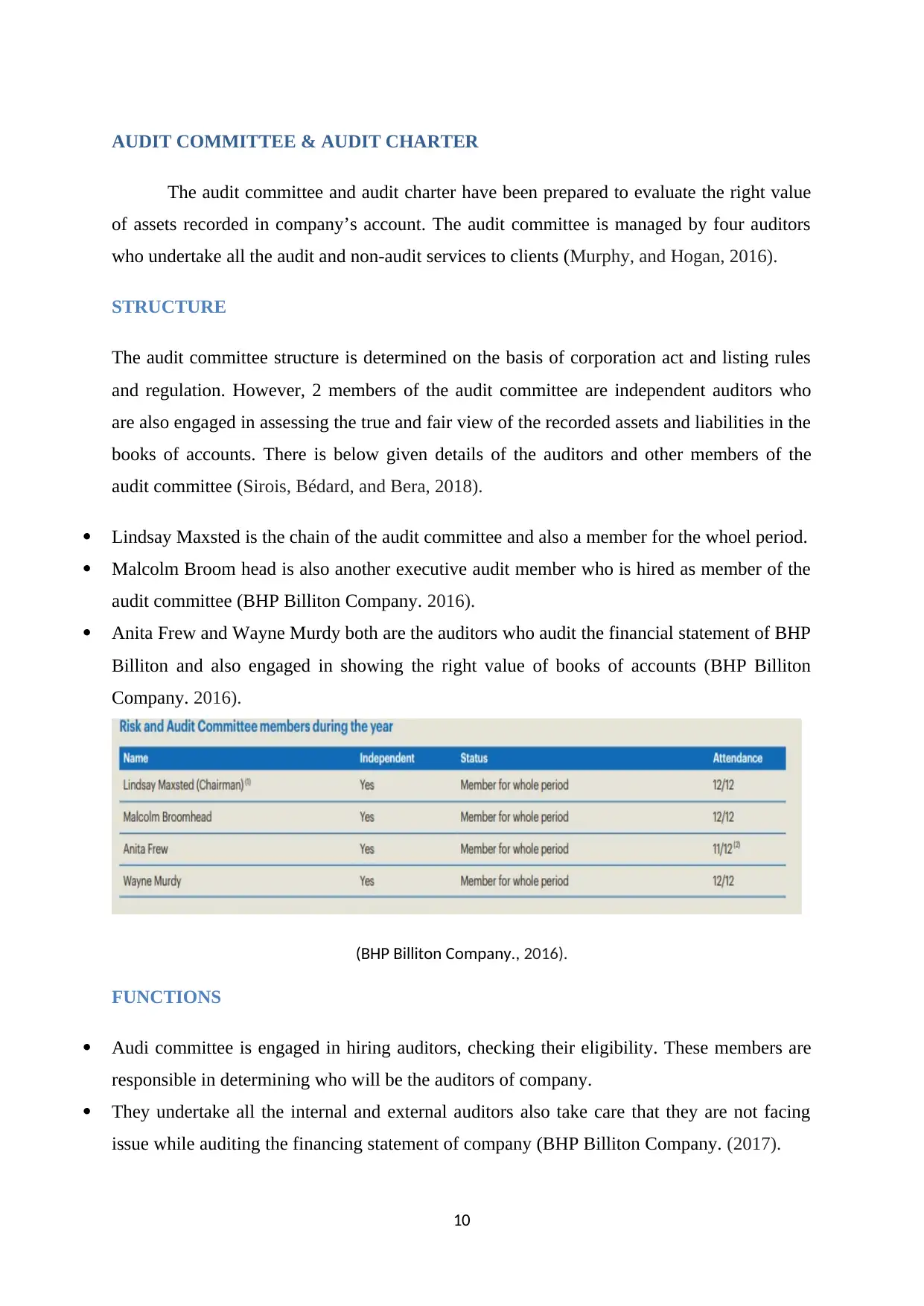

AUDIT COMMITTEE & AUDIT CHARTER

The audit committee and audit charter have been prepared to evaluate the right value

of assets recorded in company’s account. The audit committee is managed by four auditors

who undertake all the audit and non-audit services to clients (Murphy, and Hogan, 2016).

STRUCTURE

The audit committee structure is determined on the basis of corporation act and listing rules

and regulation. However, 2 members of the audit committee are independent auditors who

are also engaged in assessing the true and fair view of the recorded assets and liabilities in the

books of accounts. There is below given details of the auditors and other members of the

audit committee (Sirois, Bédard, and Bera, 2018).

Lindsay Maxsted is the chain of the audit committee and also a member for the whoel period.

Malcolm Broom head is also another executive audit member who is hired as member of the

audit committee (BHP Billiton Company. 2016).

Anita Frew and Wayne Murdy both are the auditors who audit the financial statement of BHP

Billiton and also engaged in showing the right value of books of accounts (BHP Billiton

Company. 2016).

(BHP Billiton Company., 2016).

FUNCTIONS

Audi committee is engaged in hiring auditors, checking their eligibility. These members are

responsible in determining who will be the auditors of company.

They undertake all the internal and external auditors also take care that they are not facing

issue while auditing the financing statement of company (BHP Billiton Company. (2017).

10

The audit committee and audit charter have been prepared to evaluate the right value

of assets recorded in company’s account. The audit committee is managed by four auditors

who undertake all the audit and non-audit services to clients (Murphy, and Hogan, 2016).

STRUCTURE

The audit committee structure is determined on the basis of corporation act and listing rules

and regulation. However, 2 members of the audit committee are independent auditors who

are also engaged in assessing the true and fair view of the recorded assets and liabilities in the

books of accounts. There is below given details of the auditors and other members of the

audit committee (Sirois, Bédard, and Bera, 2018).

Lindsay Maxsted is the chain of the audit committee and also a member for the whoel period.

Malcolm Broom head is also another executive audit member who is hired as member of the

audit committee (BHP Billiton Company. 2016).

Anita Frew and Wayne Murdy both are the auditors who audit the financial statement of BHP

Billiton and also engaged in showing the right value of books of accounts (BHP Billiton

Company. 2016).

(BHP Billiton Company., 2016).

FUNCTIONS

Audi committee is engaged in hiring auditors, checking their eligibility. These members are

responsible in determining who will be the auditors of company.

They undertake all the internal and external auditors also take care that they are not facing

issue while auditing the financing statement of company (BHP Billiton Company. (2017).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These auditors engaged in maintaining the transparency in the busienss (Badolato, Donelson,

and Ege, 2014).

RESPONSIBILITIES

The responsibilities of the auditors is determined on the basis of audit services offered by

auditors to company.

The audit committee is engaged in determining the Director's responsibility is to give the true

and fair view of the financial statement which are related to financial reporting

framework ,execute internal control and free from material misstatement due to fraud and

error. The auditor's responsibility is to obtain the reasonable surety of the financial statement

with its right recorded value due to fraud and error. When material misstatement is not

detected then some irregularities may be happen like forgery, misrepresentation, omission

(Tepalagul, and Lin, 2015).

Auditors will have to check whether the dividend of shares is distributed out of the profit

available .Under Australian law, when there is libiliteis and dividend recorded more than its

declared value.

Auditors should take proper management representation letter form the management of

company so that they could state that every details shared by company has been used while

determining the right value of its assets (BHP Billiton Company. 2016).

Auditors will analysis the financial statements and legal accounting standards compliance

program of company while evaluating the books of accounts.

AUDIT OPINION

The auditors of the BHP Billiton company has given non-qualified clean audit report

and stated that company has complied with the all the accounting standards and

laws.Auditors have stated that board has established some committees which helps in

monitoring ,controlling the performance or activities .Committees can use the resources

freely to discharge their responsibilities. In the opinion of the auditors, there is reasonable

ground to believe that the company is able to pay its debts in effective manner (Mohseni,

(2014). Auditor have also taken proper management representation letter from directors and

management while auditing the consolidated financial statement.The audit opinion given by

the auditors showcase that company has complied with the applicable laws. The audit report

also assists in sustainability of company.

11

and Ege, 2014).

RESPONSIBILITIES

The responsibilities of the auditors is determined on the basis of audit services offered by

auditors to company.

The audit committee is engaged in determining the Director's responsibility is to give the true

and fair view of the financial statement which are related to financial reporting

framework ,execute internal control and free from material misstatement due to fraud and

error. The auditor's responsibility is to obtain the reasonable surety of the financial statement

with its right recorded value due to fraud and error. When material misstatement is not

detected then some irregularities may be happen like forgery, misrepresentation, omission

(Tepalagul, and Lin, 2015).

Auditors will have to check whether the dividend of shares is distributed out of the profit

available .Under Australian law, when there is libiliteis and dividend recorded more than its

declared value.

Auditors should take proper management representation letter form the management of

company so that they could state that every details shared by company has been used while

determining the right value of its assets (BHP Billiton Company. 2016).

Auditors will analysis the financial statements and legal accounting standards compliance

program of company while evaluating the books of accounts.

AUDIT OPINION

The auditors of the BHP Billiton company has given non-qualified clean audit report

and stated that company has complied with the all the accounting standards and

laws.Auditors have stated that board has established some committees which helps in

monitoring ,controlling the performance or activities .Committees can use the resources

freely to discharge their responsibilities. In the opinion of the auditors, there is reasonable

ground to believe that the company is able to pay its debts in effective manner (Mohseni,

(2014). Auditor have also taken proper management representation letter from directors and

management while auditing the consolidated financial statement.The audit opinion given by

the auditors showcase that company has complied with the applicable laws. The audit report

also assists in sustainability of company.

11

DIFFERENCE BETWEEN THE RESPONSIBILITIES OF MANAGEMENT AND

AUDITOR

The responsibilities of the management are related to preparing the financial statement as per

the applicable laws and regulations. It is the duty of the management to maintain the

transparency in financial statements. The main role of the auditors is to maintain the

transparency in the prepared financial statement and assure the transparency in the prepared

financial statements. The auditors check the vulnerability and viability of the prepared

financial statements (Porter, Hatherly, and Simon, 2008). The management has to act in the

best interest of organization and auditors have to act for the stakeholders.

MATERIAL SUBSEQUENT EVENTS

There are several material subsequent events such as increased profitability, loss of busienss

and auditors functions. It is analyzed that when comparing the profit or earning with the last

year there is huge difference in profit. There is complete loss of US$ 6.4 billion, and it

includes abnormal loss of US$7.6 billion after tax but this year there is profit of US$5.9

billion and it also add loss of US$842 million after tax. The net operating cash flow of US$

16.8 billion shows that the commodities prices are higher and the further cost efficiency of

cash. The capital gearing ratio is 20.6% with the comparison of financial year 2016 it was

30.3% (Štangová, 2017). This has shown the material subsequent events have shown that

company has complied with the accounting standards and listing rules.

CONCLUSION

The crux of this report is that BHP Billiton Company has to disclose all the

information which is related to their financial performance. The auditors of company have

assisted in increasing the transparency and recording right value of the assets. With the

proper accounting records and auditors report given by auditors, it is easy to say that

company has complied with the applicable laws and regulations. The sustainability of

company is good and company is able to pay off its debts to its stakeholders.

12

AUDITOR

The responsibilities of the management are related to preparing the financial statement as per

the applicable laws and regulations. It is the duty of the management to maintain the

transparency in financial statements. The main role of the auditors is to maintain the

transparency in the prepared financial statement and assure the transparency in the prepared

financial statements. The auditors check the vulnerability and viability of the prepared

financial statements (Porter, Hatherly, and Simon, 2008). The management has to act in the

best interest of organization and auditors have to act for the stakeholders.

MATERIAL SUBSEQUENT EVENTS

There are several material subsequent events such as increased profitability, loss of busienss

and auditors functions. It is analyzed that when comparing the profit or earning with the last

year there is huge difference in profit. There is complete loss of US$ 6.4 billion, and it

includes abnormal loss of US$7.6 billion after tax but this year there is profit of US$5.9

billion and it also add loss of US$842 million after tax. The net operating cash flow of US$

16.8 billion shows that the commodities prices are higher and the further cost efficiency of

cash. The capital gearing ratio is 20.6% with the comparison of financial year 2016 it was

30.3% (Štangová, 2017). This has shown the material subsequent events have shown that

company has complied with the accounting standards and listing rules.

CONCLUSION

The crux of this report is that BHP Billiton Company has to disclose all the

information which is related to their financial performance. The auditors of company have

assisted in increasing the transparency and recording right value of the assets. With the

proper accounting records and auditors report given by auditors, it is easy to say that

company has complied with the applicable laws and regulations. The sustainability of

company is good and company is able to pay off its debts to its stakeholders.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.