Audit, Assurance, and Compliance: Financial Report Analysis for DIPL

VerifiedAdded on 2020/03/04

|11

|2662

|37

Report

AI Summary

This report provides a detailed analysis of the audit, assurance, and compliance practices of Double Pink Printers Limited (DIPL). It begins by highlighting the importance of analytical methods, such as ratio analysis and benchmarking, in developing an effective audit plan. The report then delves into the identification of various risk factors within DIPL, including those related to management failures, inexperienced staff, and CEO succession issues. Furthermore, it explores different types of risks, specifically fraud risk and risks associated with financial reporting, providing insights into their potential causes and impacts. The report examines the financial performance of the company through ratio analysis, revealing trends in current, profit margin, and solvency ratios. It also discusses the challenges faced by DIPL, such as the lack of raw material valuation based on current costs. The report concludes by emphasizing the importance of addressing these risks to ensure the company's financial stability and integrity. This comprehensive analysis is valuable for understanding the complexities of audit, assurance, and compliance in a real-world business context.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................4

Answer to Question 3......................................................................................................................6

Answer to Part A.........................................................................................................................6

Answer to Part B..........................................................................................................................8

References........................................................................................................................................9

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................4

Answer to Question 3......................................................................................................................6

Answer to Part A.........................................................................................................................6

Answer to Part B..........................................................................................................................8

References........................................................................................................................................9

2AUDIT, ASSURANCE AND COMPLIANCE

Answer to Question 1

Analytical method has utmost significance for the analysis and evaluation of the financial

information of the companions from the financial reports. At the time of developing the audit,

plan for the Double Pink Printers Limited (DIPL), the analytical method of financial information

is considered as most valuable aspect. It needs to be mentioned that the audit plan of the

companies provides necessary direction or path to the auditors at the time of audit process. On a

more specific note, audit plan helps the auditors to maintain the audit cost in order to avoid

misunderstanding with the audit clients (Anandarajan, Anandarajan and Srinivasan 2012). The

analytical approach of the financial information of the DIPL refers to the process of spreading

the financial information from different kinds of financial declaration of the company. It can be

seen that there are different kinds of mechanism that help to carry on the analytical process of

financial information. With the assistance of analytical methods for the assessment of financial

information, the financial managers and accountants of the company use this information in

order to take different kinds of financial and accounting decisions. In addition, with the help of

common size analytical approach of financial information, the financial managers of the

companies become able to dissect the financial declaration of the company from different

financial perceptions. One of the major benefits of this is that it helps to provide support in the

development of financial reports and compare the financial reports of the companies for different

financial years (Healy and Palepu 2012).

With the help of analytical methods, the financial managers of the companies can use

various financial items from the financial report and they can verify the process of financial

reporting of those items. For example, the financial reporting process of net liabilities and

owner’s equity can be considered in this regard along with the digression of these items. It needs

Answer to Question 1

Analytical method has utmost significance for the analysis and evaluation of the financial

information of the companions from the financial reports. At the time of developing the audit,

plan for the Double Pink Printers Limited (DIPL), the analytical method of financial information

is considered as most valuable aspect. It needs to be mentioned that the audit plan of the

companies provides necessary direction or path to the auditors at the time of audit process. On a

more specific note, audit plan helps the auditors to maintain the audit cost in order to avoid

misunderstanding with the audit clients (Anandarajan, Anandarajan and Srinivasan 2012). The

analytical approach of the financial information of the DIPL refers to the process of spreading

the financial information from different kinds of financial declaration of the company. It can be

seen that there are different kinds of mechanism that help to carry on the analytical process of

financial information. With the assistance of analytical methods for the assessment of financial

information, the financial managers and accountants of the company use this information in

order to take different kinds of financial and accounting decisions. In addition, with the help of

common size analytical approach of financial information, the financial managers of the

companies become able to dissect the financial declaration of the company from different

financial perceptions. One of the major benefits of this is that it helps to provide support in the

development of financial reports and compare the financial reports of the companies for different

financial years (Healy and Palepu 2012).

With the help of analytical methods, the financial managers of the companies can use

various financial items from the financial report and they can verify the process of financial

reporting of those items. For example, the financial reporting process of net liabilities and

owner’s equity can be considered in this regard along with the digression of these items. It needs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

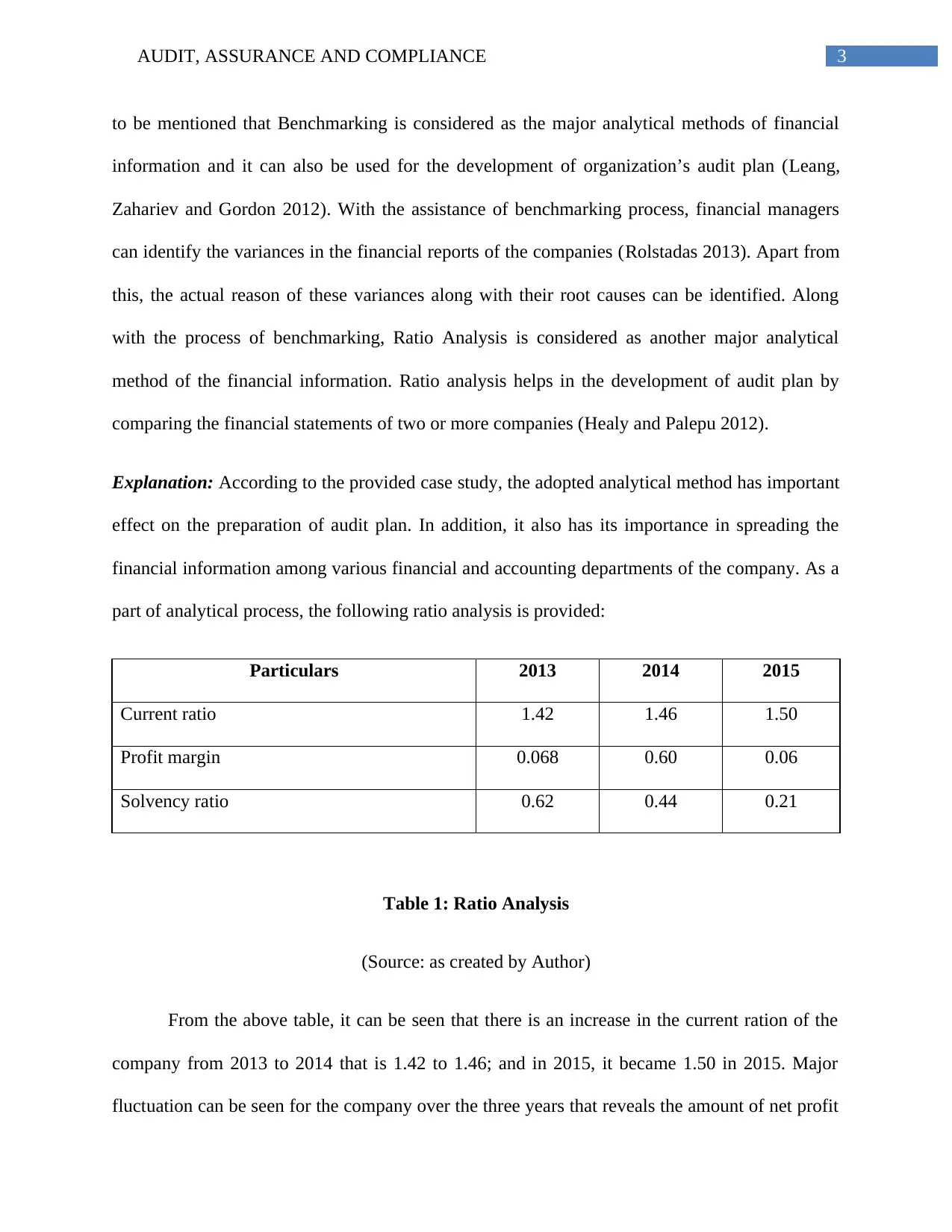

to be mentioned that Benchmarking is considered as the major analytical methods of financial

information and it can also be used for the development of organization’s audit plan (Leang,

Zahariev and Gordon 2012). With the assistance of benchmarking process, financial managers

can identify the variances in the financial reports of the companies (Rolstadas 2013). Apart from

this, the actual reason of these variances along with their root causes can be identified. Along

with the process of benchmarking, Ratio Analysis is considered as another major analytical

method of the financial information. Ratio analysis helps in the development of audit plan by

comparing the financial statements of two or more companies (Healy and Palepu 2012).

Explanation: According to the provided case study, the adopted analytical method has important

effect on the preparation of audit plan. In addition, it also has its importance in spreading the

financial information among various financial and accounting departments of the company. As a

part of analytical process, the following ratio analysis is provided:

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

From the above table, it can be seen that there is an increase in the current ration of the

company from 2013 to 2014 that is 1.42 to 1.46; and in 2015, it became 1.50 in 2015. Major

fluctuation can be seen for the company over the three years that reveals the amount of net profit

to be mentioned that Benchmarking is considered as the major analytical methods of financial

information and it can also be used for the development of organization’s audit plan (Leang,

Zahariev and Gordon 2012). With the assistance of benchmarking process, financial managers

can identify the variances in the financial reports of the companies (Rolstadas 2013). Apart from

this, the actual reason of these variances along with their root causes can be identified. Along

with the process of benchmarking, Ratio Analysis is considered as another major analytical

method of the financial information. Ratio analysis helps in the development of audit plan by

comparing the financial statements of two or more companies (Healy and Palepu 2012).

Explanation: According to the provided case study, the adopted analytical method has important

effect on the preparation of audit plan. In addition, it also has its importance in spreading the

financial information among various financial and accounting departments of the company. As a

part of analytical process, the following ratio analysis is provided:

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

From the above table, it can be seen that there is an increase in the current ration of the

company from 2013 to 2014 that is 1.42 to 1.46; and in 2015, it became 1.50 in 2015. Major

fluctuation can be seen for the company over the three years that reveals the amount of net profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

of the company from net sales. Apart from this, with the help of profitability analysis of the

company, the financial managers get insight about the expenditures of the company. Most

importantly, with the help of this analysis, the financial managers can get the insight about the

effectiveness of the company’s budget along with the diversification needs of the businesses

(Higgins 2012).

The auditors of DIPL can get an idea about the current financial position of the company

by observing the ratios and financial difficulties. From the above table, it can be seen that there is

a decrease in solvency ratio of the company from 2013 to 2015. This particular trend in solvency

ratio can helps the financial managers in the determination of financial performance of the

company. With the help of this ratio analysis, the financial managers can ascertain the amount of

cash flows in order to meet both long-term and short-term obligations of the company (Brigham

and Houston 2012). Moreover, it can be said that the evaluation and comparison of the

company’s performance and ratios make the financial managers enable to determine the financial

performance and position of the company overt the period of three years. Apart from this, the

financial managers can ascertain whether the current financial position of the company is

favorable or not. In case the situation is not favorable, the financial managers of the companies

need to take corrective measures to revive the financial position of the company. Thus, based on

the above analysis, it can be said that the analytical methods of financial information has major

values for the companies (Brigham and Ehrhardt 2013).

Answer to Question 2

In the current business operations of DIPL, it can be seen that there are certain risk

factors. According to the provided case study, it can be seen that the management of DIPL has

of the company from net sales. Apart from this, with the help of profitability analysis of the

company, the financial managers get insight about the expenditures of the company. Most

importantly, with the help of this analysis, the financial managers can get the insight about the

effectiveness of the company’s budget along with the diversification needs of the businesses

(Higgins 2012).

The auditors of DIPL can get an idea about the current financial position of the company

by observing the ratios and financial difficulties. From the above table, it can be seen that there is

a decrease in solvency ratio of the company from 2013 to 2015. This particular trend in solvency

ratio can helps the financial managers in the determination of financial performance of the

company. With the help of this ratio analysis, the financial managers can ascertain the amount of

cash flows in order to meet both long-term and short-term obligations of the company (Brigham

and Houston 2012). Moreover, it can be said that the evaluation and comparison of the

company’s performance and ratios make the financial managers enable to determine the financial

performance and position of the company overt the period of three years. Apart from this, the

financial managers can ascertain whether the current financial position of the company is

favorable or not. In case the situation is not favorable, the financial managers of the companies

need to take corrective measures to revive the financial position of the company. Thus, based on

the above analysis, it can be said that the analytical methods of financial information has major

values for the companies (Brigham and Ehrhardt 2013).

Answer to Question 2

In the current business operations of DIPL, it can be seen that there are certain risk

factors. According to the provided case study, it can be seen that the management of DIPL has

5AUDIT, ASSURANCE AND COMPLIANCE

failed in entering certain financial transactions of the company. As per the observation this

omitting mistakes of the management has direct connection with ineffective and inconsistent

planning of various marketing and sales activities of the company. As per the total financial

analysis of DIPL, the failure of the company to achieve the targeted profit margin out of the total

sales of the company can be seen. The ineffectiveness and inefficiency of the management team

regarding business operations of the company can be held responsible for this. Hence, it can be

observe that the management of the company has totally failed to foresee or gauge the effects of

various macro and micro factors on the business operations of DIPL; some of these factors are

political factors, economic factors, social factors and others. Thus, based on the above

discussion, it can be said that lower profit marking along with lower revenue of the company

contributes to the birth of inherent risks in the company (Grant 2016).

From the provided case study, it can be seen that the number of staffs in the company has

increase, the workforce of the company is inexperienced, and they lack professionalism. Thus,

this lack of experience and professionalism of the employees of DIPL leads to the birth of

inherent risks in the company. It is a universal fact that the success of any business largely

depends on the employees of those companies. As the employees of the company lack

experience and efficiency, it is natural that they will make mistakes during their jobs and this

process leads to the inherent risks of the companies. Apart from this issue, the case study of

DIPL also indicates that there are some major issues in the company regarding the succession of

the CEO of the company. This issue around the succession of CEO is a major influencer behind

the development of inherent risks in the company. Thus, the ineffective method of selecting the

CEO of the company also leads to the inherent risks. In addition, it can be seen that DIPL does

not have enough employees or staffs for properly carrying on the business operations of the

failed in entering certain financial transactions of the company. As per the observation this

omitting mistakes of the management has direct connection with ineffective and inconsistent

planning of various marketing and sales activities of the company. As per the total financial

analysis of DIPL, the failure of the company to achieve the targeted profit margin out of the total

sales of the company can be seen. The ineffectiveness and inefficiency of the management team

regarding business operations of the company can be held responsible for this. Hence, it can be

observe that the management of the company has totally failed to foresee or gauge the effects of

various macro and micro factors on the business operations of DIPL; some of these factors are

political factors, economic factors, social factors and others. Thus, based on the above

discussion, it can be said that lower profit marking along with lower revenue of the company

contributes to the birth of inherent risks in the company (Grant 2016).

From the provided case study, it can be seen that the number of staffs in the company has

increase, the workforce of the company is inexperienced, and they lack professionalism. Thus,

this lack of experience and professionalism of the employees of DIPL leads to the birth of

inherent risks in the company. It is a universal fact that the success of any business largely

depends on the employees of those companies. As the employees of the company lack

experience and efficiency, it is natural that they will make mistakes during their jobs and this

process leads to the inherent risks of the companies. Apart from this issue, the case study of

DIPL also indicates that there are some major issues in the company regarding the succession of

the CEO of the company. This issue around the succession of CEO is a major influencer behind

the development of inherent risks in the company. Thus, the ineffective method of selecting the

CEO of the company also leads to the inherent risks. In addition, it can be seen that DIPL does

not have enough employees or staffs for properly carrying on the business operations of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

company. This reason also contributes to the development of inherent risk factors in the business

operations of DIPL. Thus, based on the above discussion, it can be seen that the above discussed

reasons are the major reasons that are contributing towards the development of inherent risk

factors in the company (Weil, Schipper and Francis 2013).

Explanation: From the provided case study, it can be seen that there is a huge amount of work

pressure on the employees of DIPL. As a result of this excessive workload, inefficiency can be

seen in the process of bookkeeping of the company. This poor process of bookkeeping leads to

different kinds of issues like issues regarding cash flows, issues regarding the solvency and

liquidity of the company and many others. Apart from this, there is a major negative effect of

the financial errors of the company one the financial reports as this process lacks effective

interpretation. Thus, the management of the company needs to play an important role in order to

solve these issues in the company (Arens, Elder and Mark 2012). According to the provided case

study, it can also be seen that the management of DIPL largely lacks integrity and honesty and

for this reason, there is a possibility that the company may lose its reputation in the market. As

DIPL has great incentive structure for its management, the management of the company is under

massive pressure for performance. Thus, all these processes lead to the material misstatement of

the financial reports.

Answer to Question 3

Answer to Part A

Types of Risk Identification and Details

Fraud Risk According to the provided case study of DIPL, it can be seen that the main

risk of fraudulent is involved with the employees of the company, as they

company. This reason also contributes to the development of inherent risk factors in the business

operations of DIPL. Thus, based on the above discussion, it can be seen that the above discussed

reasons are the major reasons that are contributing towards the development of inherent risk

factors in the company (Weil, Schipper and Francis 2013).

Explanation: From the provided case study, it can be seen that there is a huge amount of work

pressure on the employees of DIPL. As a result of this excessive workload, inefficiency can be

seen in the process of bookkeeping of the company. This poor process of bookkeeping leads to

different kinds of issues like issues regarding cash flows, issues regarding the solvency and

liquidity of the company and many others. Apart from this, there is a major negative effect of

the financial errors of the company one the financial reports as this process lacks effective

interpretation. Thus, the management of the company needs to play an important role in order to

solve these issues in the company (Arens, Elder and Mark 2012). According to the provided case

study, it can also be seen that the management of DIPL largely lacks integrity and honesty and

for this reason, there is a possibility that the company may lose its reputation in the market. As

DIPL has great incentive structure for its management, the management of the company is under

massive pressure for performance. Thus, all these processes lead to the material misstatement of

the financial reports.

Answer to Question 3

Answer to Part A

Types of Risk Identification and Details

Fraud Risk According to the provided case study of DIPL, it can be seen that the main

risk of fraudulent is involved with the employees of the company, as they

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

can be involved in the fraudulent activities. The main reason behind this risk

is major dissatisfaction among the employees of the company. As per the

provide case study of DIPL, it can be seen that there is massive pressure on

the employees from the end of the boars in order to adopt the new

accounting system. As the adoption of this accounting system creates

massive pressure on the employees, there is high risk that the employees

may be involved in fraudulent activities. Thus, in order to cope up with the

process of reconciliation, the employee of the company may take the way of

fraudulent and this process leads to the material misstatement of the

financial statements. As per the provide case study, due to the ineffective

implementation of the new accounting software, the accountants of the

company failed to correctly record some of the primary accounting and

financial transactions for the financial year. As a result of the inexperienced

and inefficient employees of the company, there is a high chance of fraud

risk. It is expected that the employees of the company will make mistakes in

their jobs that will lead to fraud risk of the company. Apart from this, fraud

risk can also be found in the process to select the succession of CEO of the

company. As a result of this process, there can be high chance of inherent

risks in the company (William Jr, Glover and Prawitt 2016).

Risk in

Financial

Reporting

In case of the business operations of DIPL, another major risk can be seen in

the process of financial reporting of the company. In case the stakeholders

of the company have major financial expectation from the company’s

financial performance, there is a high chance of frauds in the financial

can be involved in the fraudulent activities. The main reason behind this risk

is major dissatisfaction among the employees of the company. As per the

provide case study of DIPL, it can be seen that there is massive pressure on

the employees from the end of the boars in order to adopt the new

accounting system. As the adoption of this accounting system creates

massive pressure on the employees, there is high risk that the employees

may be involved in fraudulent activities. Thus, in order to cope up with the

process of reconciliation, the employee of the company may take the way of

fraudulent and this process leads to the material misstatement of the

financial statements. As per the provide case study, due to the ineffective

implementation of the new accounting software, the accountants of the

company failed to correctly record some of the primary accounting and

financial transactions for the financial year. As a result of the inexperienced

and inefficient employees of the company, there is a high chance of fraud

risk. It is expected that the employees of the company will make mistakes in

their jobs that will lead to fraud risk of the company. Apart from this, fraud

risk can also be found in the process to select the succession of CEO of the

company. As a result of this process, there can be high chance of inherent

risks in the company (William Jr, Glover and Prawitt 2016).

Risk in

Financial

Reporting

In case of the business operations of DIPL, another major risk can be seen in

the process of financial reporting of the company. In case the stakeholders

of the company have major financial expectation from the company’s

financial performance, there is a high chance of frauds in the financial

8AUDIT, ASSURANCE AND COMPLIANCE

reports from the end of the company. It has been seen that the management

of the company manipulates the financial statements of the company so that

the stakeholders can see that the company has financial growth and

performance. Thus, it can be observed that the fraud risk in financial

reporting is one of the major risks in the companies (DeFond and Zhang

2014).

Answer to Part B

According to the provide case study, there is a massive lack in the raw material valuation

of DIPL that is based on the process of average cost. The main reason is that the current cost of

paper is higher than average cost. Thus, it is not en effective process. The primary risk in the

implementation process of the new accounting software can be identified with the help of

monitoring various phases of task in the organization. On the other hand, the analysis and

evaluation of the financial reports of the companies helps the management to detect the fraud

risk related with financial reporting. As per the earlier discussion, the analysis can be done with

the help of various analytical mechanisms that is benchmarking, ratio analysis and others. It is

crucial for the management of DIPL to conduct the analysis and evaluation process on a time

basis (Wang, Li and Li 2012).

reports from the end of the company. It has been seen that the management

of the company manipulates the financial statements of the company so that

the stakeholders can see that the company has financial growth and

performance. Thus, it can be observed that the fraud risk in financial

reporting is one of the major risks in the companies (DeFond and Zhang

2014).

Answer to Part B

According to the provide case study, there is a massive lack in the raw material valuation

of DIPL that is based on the process of average cost. The main reason is that the current cost of

paper is higher than average cost. Thus, it is not en effective process. The primary risk in the

implementation process of the new accounting software can be identified with the help of

monitoring various phases of task in the organization. On the other hand, the analysis and

evaluation of the financial reports of the companies helps the management to detect the fraud

risk related with financial reporting. As per the earlier discussion, the analysis can be done with

the help of various analytical mechanisms that is benchmarking, ratio analysis and others. It is

crucial for the management of DIPL to conduct the analysis and evaluation process on a time

basis (Wang, Li and Li 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

References

Anandarajan, M., Anandarajan, A. and Srinivasan, C.A. eds., 2012. Business intelligence

techniques: a perspective from accounting and finance. Springer Science & Business Media.

Arens, A.A., Elder, R.J. and Mark, B., 2012. Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Leang, S.S., Zahariev, F. and Gordon, M.S., 2012. Benchmarking the performance of time-

dependent density functional methods. The Journal of chemical physics, 136(10), p.104101.

Rolstadas, A. ed., 2013. Benchmarking—theory and practice. Springer.

References

Anandarajan, M., Anandarajan, A. and Srinivasan, C.A. eds., 2012. Business intelligence

techniques: a perspective from accounting and finance. Springer Science & Business Media.

Arens, A.A., Elder, R.J. and Mark, B., 2012. Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Leang, S.S., Zahariev, F. and Gordon, M.S., 2012. Benchmarking the performance of time-

dependent density functional methods. The Journal of chemical physics, 136(10), p.104101.

Rolstadas, A. ed., 2013. Benchmarking—theory and practice. Springer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

Wang, B., Li, B. and Li, H., 2012, June. Oruta: Privacy-preserving public auditing for shared

data in the cloud. In Cloud Computing (CLOUD), 2012 IEEE 5th International Conference

on (pp. 295-302). IEEE.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Wang, B., Li, B. and Li, H., 2012, June. Oruta: Privacy-preserving public auditing for shared

data in the cloud. In Cloud Computing (CLOUD), 2012 IEEE 5th International Conference

on (pp. 295-302). IEEE.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.