Audit, Assurance and Compliance Report: DIPL, Finance Report

VerifiedAdded on 2020/03/02

|10

|2178

|469

Report

AI Summary

This report analyzes an audit, assurance, and compliance case study of Double Pink Printers Limited (DIPL). It examines the application of analytical methods, such as ratio analysis and benchmarking, in evaluating DIPL's financial performance. The report assesses current, profit margin, and solvency ratios, highlighting trends and implications for financial stability. It identifies inherent risk factors, including employee errors, inefficient workforce, and management issues, which contribute to fraud and financial reporting risks. Furthermore, the report discusses the types of risks, including fraud and financial reporting risks, and their explanations within the context of DIPL. The analysis emphasizes the importance of effective financial strategies and risk management to address identified issues and improve DIPL's financial health and compliance.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................4

Answer to Question 3......................................................................................................................6

References........................................................................................................................................8

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................4

Answer to Question 3......................................................................................................................6

References........................................................................................................................................8

2AUDIT, ASSURANCE AND COMPLIANCE

Answer to Question 1

Analytical method is considered as one of the major tools for the analysis and evaluation

of different kinds of accounting and financial documents of the business organizations like

balance sheet, income statements and many others. Analytical method of accounting and

financial information is considered as a major valuable approach at the time to prepare the audit

reports of Double Pink Printers Limited (DIPL). With the assistance of audit plan, the auditors of

the companies use to set the definite path of the audit operations. In addition, with the assistance

of audit plan, the auditors become able to control the audit cost so that misunderstanding with the

audit parties can be minimized. The financial managers of the companies become able to spread

the required accounting and financial information in the organizations with the help of analytical

method of financial information. In this process, the financial managers can take the assistance of

different methods of analytical approaches of the financial information. All these mechanisms of

analytical methods help the financial managers of the companies in taking effective and

appropriate financial decisions. In addition, the common sizing analytical approach provide great

assistance to the financial managers of the companies in anatomizing the financial information

from different point of views. Apart from this, at the time of preparing the financial statements of

the organizations, the financial managers get great supports these analytical approaches (Healy

and Palepu 2012).

In order to verify the reporting process of the different kinds of items in the financial

statements, different process of analytical methods plays an integral part. For example, it can be

said that the financial reporting process of shareholder’s equity is very different from the

reporting process of inventories and this can be determined with the help of analytical

approaches. In this regard, the process of Benchmarking is considered as an important tool as the

Answer to Question 1

Analytical method is considered as one of the major tools for the analysis and evaluation

of different kinds of accounting and financial documents of the business organizations like

balance sheet, income statements and many others. Analytical method of accounting and

financial information is considered as a major valuable approach at the time to prepare the audit

reports of Double Pink Printers Limited (DIPL). With the assistance of audit plan, the auditors of

the companies use to set the definite path of the audit operations. In addition, with the assistance

of audit plan, the auditors become able to control the audit cost so that misunderstanding with the

audit parties can be minimized. The financial managers of the companies become able to spread

the required accounting and financial information in the organizations with the help of analytical

method of financial information. In this process, the financial managers can take the assistance of

different methods of analytical approaches of the financial information. All these mechanisms of

analytical methods help the financial managers of the companies in taking effective and

appropriate financial decisions. In addition, the common sizing analytical approach provide great

assistance to the financial managers of the companies in anatomizing the financial information

from different point of views. Apart from this, at the time of preparing the financial statements of

the organizations, the financial managers get great supports these analytical approaches (Healy

and Palepu 2012).

In order to verify the reporting process of the different kinds of items in the financial

statements, different process of analytical methods plays an integral part. For example, it can be

said that the financial reporting process of shareholder’s equity is very different from the

reporting process of inventories and this can be determined with the help of analytical

approaches. In this regard, the process of Benchmarking is considered as an important tool as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

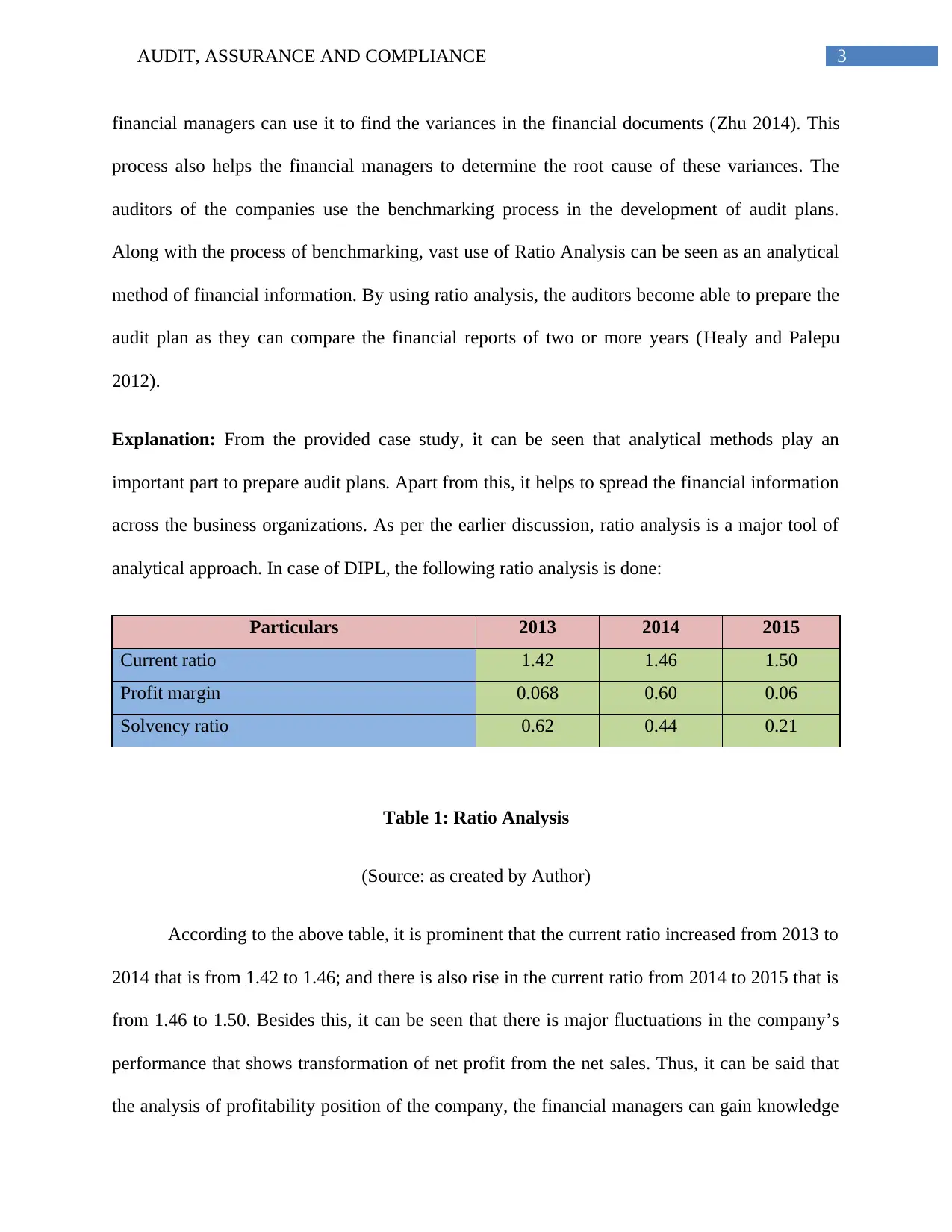

financial managers can use it to find the variances in the financial documents (Zhu 2014). This

process also helps the financial managers to determine the root cause of these variances. The

auditors of the companies use the benchmarking process in the development of audit plans.

Along with the process of benchmarking, vast use of Ratio Analysis can be seen as an analytical

method of financial information. By using ratio analysis, the auditors become able to prepare the

audit plan as they can compare the financial reports of two or more years (Healy and Palepu

2012).

Explanation: From the provided case study, it can be seen that analytical methods play an

important part to prepare audit plans. Apart from this, it helps to spread the financial information

across the business organizations. As per the earlier discussion, ratio analysis is a major tool of

analytical approach. In case of DIPL, the following ratio analysis is done:

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

According to the above table, it is prominent that the current ratio increased from 2013 to

2014 that is from 1.42 to 1.46; and there is also rise in the current ratio from 2014 to 2015 that is

from 1.46 to 1.50. Besides this, it can be seen that there is major fluctuations in the company’s

performance that shows transformation of net profit from the net sales. Thus, it can be said that

the analysis of profitability position of the company, the financial managers can gain knowledge

financial managers can use it to find the variances in the financial documents (Zhu 2014). This

process also helps the financial managers to determine the root cause of these variances. The

auditors of the companies use the benchmarking process in the development of audit plans.

Along with the process of benchmarking, vast use of Ratio Analysis can be seen as an analytical

method of financial information. By using ratio analysis, the auditors become able to prepare the

audit plan as they can compare the financial reports of two or more years (Healy and Palepu

2012).

Explanation: From the provided case study, it can be seen that analytical methods play an

important part to prepare audit plans. Apart from this, it helps to spread the financial information

across the business organizations. As per the earlier discussion, ratio analysis is a major tool of

analytical approach. In case of DIPL, the following ratio analysis is done:

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

According to the above table, it is prominent that the current ratio increased from 2013 to

2014 that is from 1.42 to 1.46; and there is also rise in the current ratio from 2014 to 2015 that is

from 1.46 to 1.50. Besides this, it can be seen that there is major fluctuations in the company’s

performance that shows transformation of net profit from the net sales. Thus, it can be said that

the analysis of profitability position of the company, the financial managers can gain knowledge

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

about the expenditures of the organization. This process is also effective in judging the

effectiveness of the company’s budget making policies and the diversification policies (Weil,

Schipper and Francis 2013).

In case of DIPL, with the help of observation of the financial ratios, the financial

managers and the auditors of the company gain the insight about the financial stability of the

company. It is prominent from the above ratio analysis that there is decrease in solvency ratio

from 2013 to 2014 that is from 0.62 to 0.44; and there is further decrease in it from 2014 to 2015

that is 0.44 to 0.21. Thus, it can be seen that the solvency position of the company is not great as

the company has less current assets to cover the current liabilities of their business. Hence, the

ratio analysis makes the financial managers aware about the amount of cash flows that is needed

in order to meet the short as well as long-term obligations of the company. Ratio analysis makes

the financial managers able to compare the financial performance of the companies for two or

more years and this process is helpful in determining the financial performance of the company.

From this process, the favorableness of the company’s position can be judged. In case the

financial managers find that the financial position of the company is not favorable, they can

develop effective financial strategies to revive the situation (Brigham and Ehrhardt 2013).

Answer to Question 2

Certain risk factors can be seen in the business processes of DIPL. As per the provided

situation of DIPL, the employees of the company have made several errors while recording the

financial transactions of the company. Out of the observation, it can be seen that ineffective and

inconsistent sales and marketing operations of the company have connection with the financial

transaction errors of the company. Thus, it is clear that the management team of the company has

about the expenditures of the organization. This process is also effective in judging the

effectiveness of the company’s budget making policies and the diversification policies (Weil,

Schipper and Francis 2013).

In case of DIPL, with the help of observation of the financial ratios, the financial

managers and the auditors of the company gain the insight about the financial stability of the

company. It is prominent from the above ratio analysis that there is decrease in solvency ratio

from 2013 to 2014 that is from 0.62 to 0.44; and there is further decrease in it from 2014 to 2015

that is 0.44 to 0.21. Thus, it can be seen that the solvency position of the company is not great as

the company has less current assets to cover the current liabilities of their business. Hence, the

ratio analysis makes the financial managers aware about the amount of cash flows that is needed

in order to meet the short as well as long-term obligations of the company. Ratio analysis makes

the financial managers able to compare the financial performance of the companies for two or

more years and this process is helpful in determining the financial performance of the company.

From this process, the favorableness of the company’s position can be judged. In case the

financial managers find that the financial position of the company is not favorable, they can

develop effective financial strategies to revive the situation (Brigham and Ehrhardt 2013).

Answer to Question 2

Certain risk factors can be seen in the business processes of DIPL. As per the provided

situation of DIPL, the employees of the company have made several errors while recording the

financial transactions of the company. Out of the observation, it can be seen that ineffective and

inconsistent sales and marketing operations of the company have connection with the financial

transaction errors of the company. Thus, it is clear that the management team of the company has

5AUDIT, ASSURANCE AND COMPLIANCE

failed to provide effectiveness and efficiency in their job operations. As an effect of this, the

management team has showed is inability to foresee the effects of various macro and micro

economic factors like social factors, policitical factors, economical factors and many others.

Thus, based on the above discussion, it can be said that low profit, low revenue and

ineffectiveness of the management of the company are responsible for the preparation of inherent

risk factors in the company (Bratten et al. 2013).

From the provided case study of DIPL, it is prominent that DIPL has an inexperienced

and inefficient workforce in the organization. Apart from this, the workforce of the company

massively lacks professionalism. All these factors together increase the inherent risk factor of the

company. One cannot ignore the fact that the success of the businesses depends on the

performance of the employees. Due to be inefficient and not having any experience, the

employees of the company are bound to make mistakes in their work and this process can be

largely held responsible for the development of inherent risks in the company (Knechel et al.

2012).

Explanation: As per the provided case study of DIPL, immense work pressure can be seen on

the employees of the company. Due to this pressure, the employees make several mistakes in the

bookkeeping process that makes the process inefficient. This issue in bookkeeping leads to

various other organizational issues like cash flow issues, solvency issue, liquidity issue and

profitability issue. In addition, it can be seen that there is lack of financial interpretation of the

financial reports and this process creates major negative effect on the financial performance of

the company. In this situation, the management of the company needs to step up and they need to

develop effective strategy to solve these organizational issues. It has also been seen that the

management of the company lacks integrity and honesty in their jobs. Hence, based on the above

failed to provide effectiveness and efficiency in their job operations. As an effect of this, the

management team has showed is inability to foresee the effects of various macro and micro

economic factors like social factors, policitical factors, economical factors and many others.

Thus, based on the above discussion, it can be said that low profit, low revenue and

ineffectiveness of the management of the company are responsible for the preparation of inherent

risk factors in the company (Bratten et al. 2013).

From the provided case study of DIPL, it is prominent that DIPL has an inexperienced

and inefficient workforce in the organization. Apart from this, the workforce of the company

massively lacks professionalism. All these factors together increase the inherent risk factor of the

company. One cannot ignore the fact that the success of the businesses depends on the

performance of the employees. Due to be inefficient and not having any experience, the

employees of the company are bound to make mistakes in their work and this process can be

largely held responsible for the development of inherent risks in the company (Knechel et al.

2012).

Explanation: As per the provided case study of DIPL, immense work pressure can be seen on

the employees of the company. Due to this pressure, the employees make several mistakes in the

bookkeeping process that makes the process inefficient. This issue in bookkeeping leads to

various other organizational issues like cash flow issues, solvency issue, liquidity issue and

profitability issue. In addition, it can be seen that there is lack of financial interpretation of the

financial reports and this process creates major negative effect on the financial performance of

the company. In this situation, the management of the company needs to step up and they need to

develop effective strategy to solve these organizational issues. It has also been seen that the

management of the company lacks integrity and honesty in their jobs. Hence, based on the above

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

discussion, it can be seen that all the above-discussed issues contribute to the material

misstatements of the financial documents (Cao, Chychyla and Stewart 2015).

Answer to Question 3

Types of Risk Explanation

Fraud Risk As per the provided information of DIPL, the employees of the company are

involved in different kinds of fraudulent activities. Thus, out of these fraudulent

activities, the risk of fraud is developed. Major dissatisfaction among the

employees contributes to the development of fraudulent activities among the

employees. As per the provided case study, massive pressure is there on the

employees for the adoption of new accounting system and this pressure comes

from the end of the management of the company. In order to avoid the pressure, the

employees take the way of fraudulent. The employees of the organization may take

the way of fraudulent so that they can easily cope up with the reconciliation

process of the new software. From the provided case study, it can also be seen that

the due to the improper installation of the accounting system, various accounting

transactions are recorded in the wrong way and this process increases the risk of

the company (DeFond and Zhang 2014).

Financial Reporting

Risk

Apart from the above reason, another major risk in DIPL is involved with the

financial reporting of the company. It is a fact that the investor have major

expectations from the companies. In case the investors of the company expect

major financial returns, the company takes the help of financial manipulation. In

order to portray the strong financial position of the company, the management does

many manipulations in the financial statements. This process increase the risk of

fraud in the business organizations and the same concept is applicable for DIPL

also (Arens, Elder and Mark 2012).

Explanation: According to the provided information, it can be seen that the process of valuation

of raw materials of DIPL is ineffective and inefficient as the present cost of the paper is higher

than the average cost of papers. Hence, this process cannot be considered as an effective process.

discussion, it can be seen that all the above-discussed issues contribute to the material

misstatements of the financial documents (Cao, Chychyla and Stewart 2015).

Answer to Question 3

Types of Risk Explanation

Fraud Risk As per the provided information of DIPL, the employees of the company are

involved in different kinds of fraudulent activities. Thus, out of these fraudulent

activities, the risk of fraud is developed. Major dissatisfaction among the

employees contributes to the development of fraudulent activities among the

employees. As per the provided case study, massive pressure is there on the

employees for the adoption of new accounting system and this pressure comes

from the end of the management of the company. In order to avoid the pressure, the

employees take the way of fraudulent. The employees of the organization may take

the way of fraudulent so that they can easily cope up with the reconciliation

process of the new software. From the provided case study, it can also be seen that

the due to the improper installation of the accounting system, various accounting

transactions are recorded in the wrong way and this process increases the risk of

the company (DeFond and Zhang 2014).

Financial Reporting

Risk

Apart from the above reason, another major risk in DIPL is involved with the

financial reporting of the company. It is a fact that the investor have major

expectations from the companies. In case the investors of the company expect

major financial returns, the company takes the help of financial manipulation. In

order to portray the strong financial position of the company, the management does

many manipulations in the financial statements. This process increase the risk of

fraud in the business organizations and the same concept is applicable for DIPL

also (Arens, Elder and Mark 2012).

Explanation: According to the provided information, it can be seen that the process of valuation

of raw materials of DIPL is ineffective and inefficient as the present cost of the paper is higher

than the average cost of papers. Hence, this process cannot be considered as an effective process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

The mentioned risk in the implementation of new accounting software can be detected with

thorough process of monitoring of the different phrases of tasks. On the other hand, in order to

identify the risks in the financial reporting, the financial managers take the help of analysis and

evaluation of those financial reports. These are the ways to identify the major frauds in the

organization (Grant 2016).

The mentioned risk in the implementation of new accounting software can be detected with

thorough process of monitoring of the different phrases of tasks. On the other hand, in order to

identify the risks in the financial reporting, the financial managers take the help of analysis and

evaluation of those financial reports. These are the ways to identify the major frauds in the

organization (Grant 2016).

8AUDIT, ASSURANCE AND COMPLIANCE

References

Arens, A.A., Elder, R.J. and Mark, B., 2012. Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Bratten, B., Gaynor, L.M., McDaniel, L., Montague, N.R. and Sierra, G.E., 2013. The audit of

fair values and other estimates: The effects of underlying environmental, task, and auditor-

specific factors. Auditing: A Journal of Practice & Theory, 32(sp1), pp.7-44.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), pp.423-429.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Knechel, W.R., Krishnan, G.V., Pevzner, M., Shefchik, L.B. and Velury, U.K., 2012. Audit

quality: Insights from the academic literature. Auditing: A Journal of Practice &

Theory, 32(sp1), pp.385-421.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

References

Arens, A.A., Elder, R.J. and Mark, B., 2012. Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Bratten, B., Gaynor, L.M., McDaniel, L., Montague, N.R. and Sierra, G.E., 2013. The audit of

fair values and other estimates: The effects of underlying environmental, task, and auditor-

specific factors. Auditing: A Journal of Practice & Theory, 32(sp1), pp.7-44.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), pp.423-429.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Knechel, W.R., Krishnan, G.V., Pevzner, M., Shefchik, L.B. and Velury, U.K., 2012. Audit

quality: Insights from the academic literature. Auditing: A Journal of Practice &

Theory, 32(sp1), pp.385-421.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

Zhu, J., 2014. Quantitative models for performance evaluation and benchmarking: data

envelopment analysis with spreadsheets (Vol. 213). Springer.

Zhu, J., 2014. Quantitative models for performance evaluation and benchmarking: data

envelopment analysis with spreadsheets (Vol. 213). Springer.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.