University Audit, Assurance and Compliance Report Analysis

VerifiedAdded on 2020/03/04

|14

|3469

|46

Report

AI Summary

This report provides a comprehensive analysis of an audit, assurance, and compliance case study, focusing on Double Ink Printers Limited (DIPL). It begins with an examination of the audit plan, emphasizing the importance of financial data analysis techniques, such as benchmarking and ratio analysis, to assess DIPL's financial performance and identify potential issues. The report then delves into the identification of inherent risks, including inventory risk and acquisition risk, detailing their causes and potential impacts on financial statements. Furthermore, it addresses fraud risks, outlining potential fraudulent activities and their audit implications. The report also includes clarifications on financial ratios and explanations of audit impacts, providing a detailed understanding of the audit process and the challenges faced by DIPL. Finally, it examines the fraud risks and their audit implications, offering insights into mitigating these risks. Overall, the report provides a thorough assessment of the audit, assurance, and compliance aspects of DIPL, offering valuable insights into financial analysis and risk management.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................5

Clarification:................................................................................................................................8

Reply to Question 3:........................................................................................................................8

Answer to Part A:........................................................................................................................8

Answer to Part B:.......................................................................................................................12

Reference List................................................................................................................................14

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................5

Clarification:................................................................................................................................8

Reply to Question 3:........................................................................................................................8

Answer to Part A:........................................................................................................................8

Answer to Part B:.......................................................................................................................12

Reference List................................................................................................................................14

2AUDIT, ASSURANCE AND COMPLIANCE

Answer to Question 1:

In the technique for setting up the audit plan of Double Ink Printers Limited (DIPL), the

investigative strategy related with financial data gives gigantic esteem. Actually, audit plan

conveys the required bearings and rules to the evaluators amid the audit operations. Exactly,

audit plan empowers the evaluators in keeping up the cost of audit in a specific point of

confinement for anticipating misconception with the audit customers (Alam 2014). The logical

approach identified with the financial data of DIPL indicates the technique for spreading

financial data from the different financial assertions of the organization. The strategy for

breaking down the financial data of the organizations could be brought out through a few

systems.

With the assistance of diagnostic approach for evaluating the financial data, the

accountants and financial investigators of the organization s could use such data for undertaking

distinctive financial and accounting choices (Baylis et al. 2017). The normal size explanatory

approach empowers in the strategy for dismembering the financial presentation of the

organizations from the regular perspectives. One of the essential advantages is that it helps in

expanding support in differentiating the financial reports from different financial courses of

events.

The accountants and financial experts could use diverse lines of things from the financial

reports and they could confirm their base of planning for the organizations. For example, the

enlistment methodology of various financial and accounting things in the financial reports, for

example, net liabilities, resources, proprietor's value and others could be viewed as combined

with appraisal of straying from the typical situation (Brawley et al. 2015).

Answer to Question 1:

In the technique for setting up the audit plan of Double Ink Printers Limited (DIPL), the

investigative strategy related with financial data gives gigantic esteem. Actually, audit plan

conveys the required bearings and rules to the evaluators amid the audit operations. Exactly,

audit plan empowers the evaluators in keeping up the cost of audit in a specific point of

confinement for anticipating misconception with the audit customers (Alam 2014). The logical

approach identified with the financial data of DIPL indicates the technique for spreading

financial data from the different financial assertions of the organization. The strategy for

breaking down the financial data of the organizations could be brought out through a few

systems.

With the assistance of diagnostic approach for evaluating the financial data, the

accountants and financial investigators of the organization s could use such data for undertaking

distinctive financial and accounting choices (Baylis et al. 2017). The normal size explanatory

approach empowers in the strategy for dismembering the financial presentation of the

organizations from the regular perspectives. One of the essential advantages is that it helps in

expanding support in differentiating the financial reports from different financial courses of

events.

The accountants and financial experts could use diverse lines of things from the financial

reports and they could confirm their base of planning for the organizations. For example, the

enlistment methodology of various financial and accounting things in the financial reports, for

example, net liabilities, resources, proprietor's value and others could be viewed as combined

with appraisal of straying from the typical situation (Brawley et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

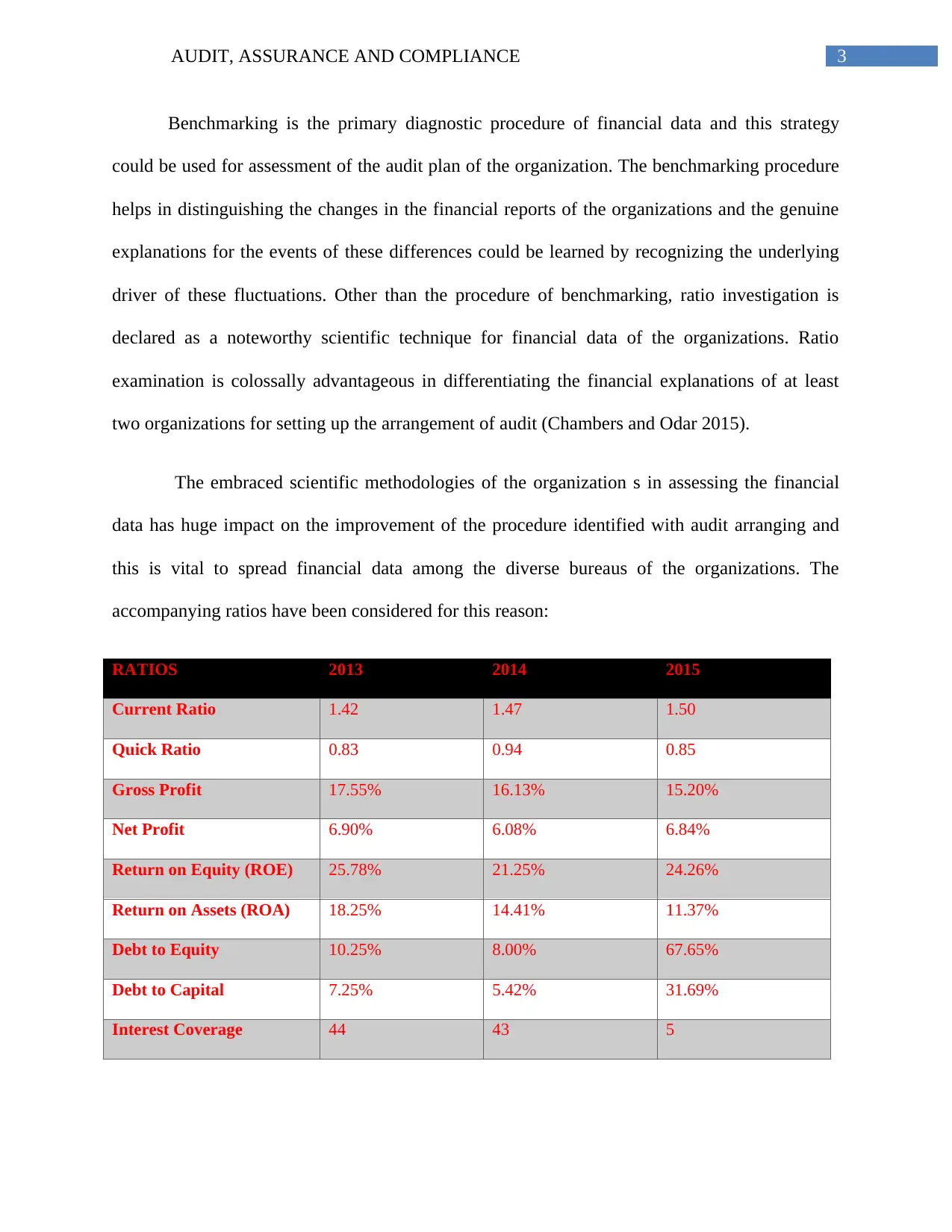

Benchmarking is the primary diagnostic procedure of financial data and this strategy

could be used for assessment of the audit plan of the organization. The benchmarking procedure

helps in distinguishing the changes in the financial reports of the organizations and the genuine

explanations for the events of these differences could be learned by recognizing the underlying

driver of these fluctuations. Other than the procedure of benchmarking, ratio investigation is

declared as a noteworthy scientific technique for financial data of the organizations. Ratio

examination is colossally advantageous in differentiating the financial explanations of at least

two organizations for setting up the arrangement of audit (Chambers and Odar 2015).

The embraced scientific methodologies of the organization s in assessing the financial

data has huge impact on the improvement of the procedure identified with audit arranging and

this is vital to spread financial data among the diverse bureaus of the organizations. The

accompanying ratios have been considered for this reason:

RATIOS 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Gross Profit 17.55% 16.13% 15.20%

Net Profit 6.90% 6.08% 6.84%

Return on Equity (ROE) 25.78% 21.25% 24.26%

Return on Assets (ROA) 18.25% 14.41% 11.37%

Debt to Equity 10.25% 8.00% 67.65%

Debt to Capital 7.25% 5.42% 31.69%

Interest Coverage 44 43 5

Benchmarking is the primary diagnostic procedure of financial data and this strategy

could be used for assessment of the audit plan of the organization. The benchmarking procedure

helps in distinguishing the changes in the financial reports of the organizations and the genuine

explanations for the events of these differences could be learned by recognizing the underlying

driver of these fluctuations. Other than the procedure of benchmarking, ratio investigation is

declared as a noteworthy scientific technique for financial data of the organizations. Ratio

examination is colossally advantageous in differentiating the financial explanations of at least

two organizations for setting up the arrangement of audit (Chambers and Odar 2015).

The embraced scientific methodologies of the organization s in assessing the financial

data has huge impact on the improvement of the procedure identified with audit arranging and

this is vital to spread financial data among the diverse bureaus of the organizations. The

accompanying ratios have been considered for this reason:

RATIOS 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Gross Profit 17.55% 16.13% 15.20%

Net Profit 6.90% 6.08% 6.84%

Return on Equity (ROE) 25.78% 21.25% 24.26%

Return on Assets (ROA) 18.25% 14.41% 11.37%

Debt to Equity 10.25% 8.00% 67.65%

Debt to Capital 7.25% 5.42% 31.69%

Interest Coverage 44 43 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

Clarifications:

RATIOS EXPLANATIONS AUDIT IMPACT

Current

Ratio

Current ratio has demonstrated

upward pattern driven by change

in current resources from FY13

to FY15.

From the DIPL case, there are a ton of things that are to

be viewed as in order to help with settling on arranging

choice for the review. Something that must be

considered is the installment of inventories utilizing the

money of the nation from which the crude materials

have been requested from. There is the danger of

change in so far as freedom of inventories is concerned

on the grounds that every single Asian nation don't

utilize one cash. An arrangement for vacillation should

there be put aside for the other money related year.

Quick

Ratio

This ratio has stayed pretty

much level as the proportionate

changes in both current

resources and liabilities have

been comparative.

The ratio is driven by the estimation of the present

resources and liabilities and as we realize that the

estimation of some present resources is unpredictable

because of market connected esteem or

acknowledgment estimation of the advantages

subsequently the ratio can be controlled.

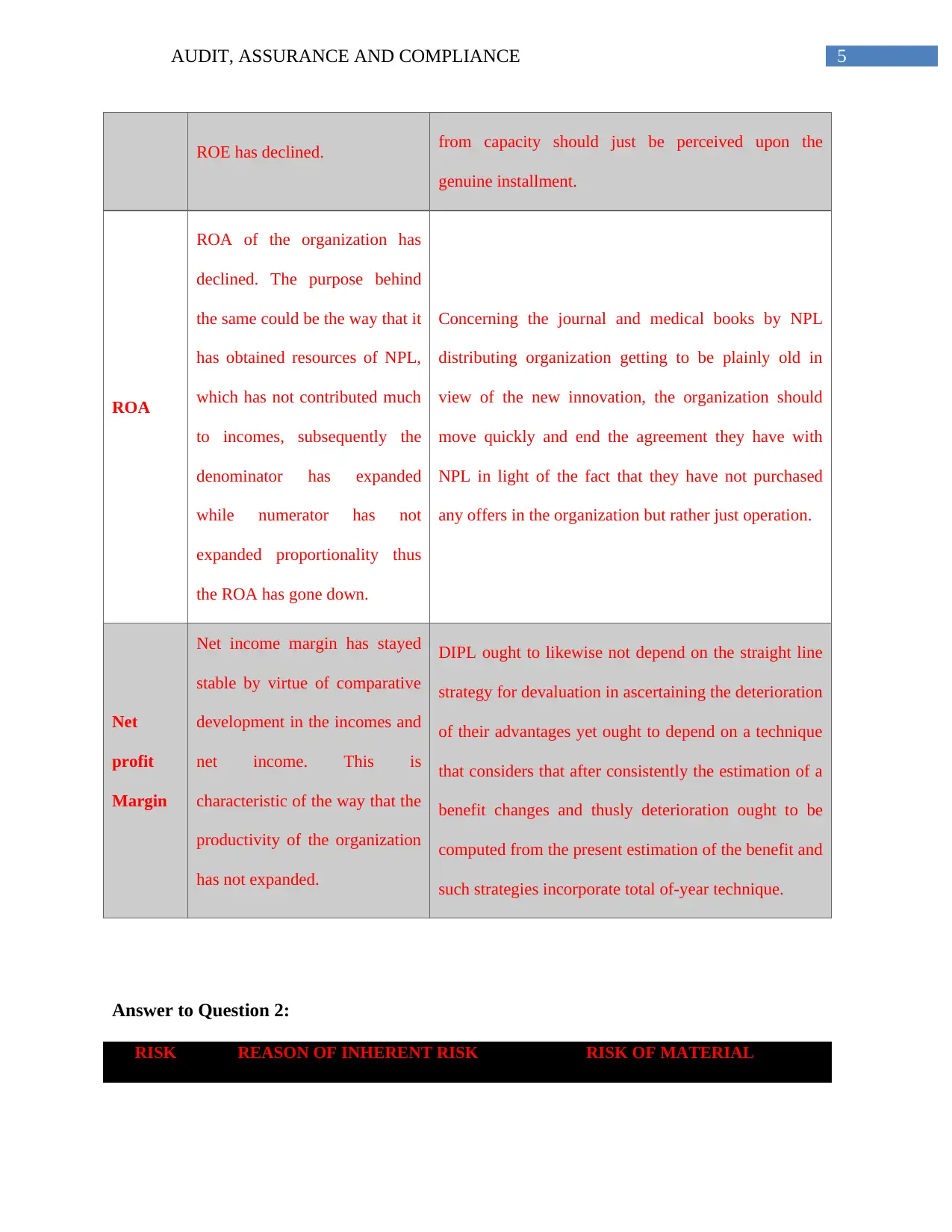

ROE The ratio has declined because

of the way that according to

bookkeeping strategy the net

benefit must be added to the

save of the organization thus

value base has expanded and the

As respects the income that is gotten for capacity of E-

Books, the same ought not be perceived when

solicitations for the charges are sent however when the

same is gotten. This is on account of DIPL dangers

inability to pay inside time by the distributing

organizations. This subsequently implies monies got

Clarifications:

RATIOS EXPLANATIONS AUDIT IMPACT

Current

Ratio

Current ratio has demonstrated

upward pattern driven by change

in current resources from FY13

to FY15.

From the DIPL case, there are a ton of things that are to

be viewed as in order to help with settling on arranging

choice for the review. Something that must be

considered is the installment of inventories utilizing the

money of the nation from which the crude materials

have been requested from. There is the danger of

change in so far as freedom of inventories is concerned

on the grounds that every single Asian nation don't

utilize one cash. An arrangement for vacillation should

there be put aside for the other money related year.

Quick

Ratio

This ratio has stayed pretty

much level as the proportionate

changes in both current

resources and liabilities have

been comparative.

The ratio is driven by the estimation of the present

resources and liabilities and as we realize that the

estimation of some present resources is unpredictable

because of market connected esteem or

acknowledgment estimation of the advantages

subsequently the ratio can be controlled.

ROE The ratio has declined because

of the way that according to

bookkeeping strategy the net

benefit must be added to the

save of the organization thus

value base has expanded and the

As respects the income that is gotten for capacity of E-

Books, the same ought not be perceived when

solicitations for the charges are sent however when the

same is gotten. This is on account of DIPL dangers

inability to pay inside time by the distributing

organizations. This subsequently implies monies got

5AUDIT, ASSURANCE AND COMPLIANCE

ROE has declined. from capacity should just be perceived upon the

genuine installment.

ROA

ROA of the organization has

declined. The purpose behind

the same could be the way that it

has obtained resources of NPL,

which has not contributed much

to incomes, subsequently the

denominator has expanded

while numerator has not

expanded proportionality thus

the ROA has gone down.

Concerning the journal and medical books by NPL

distributing organization getting to be plainly old in

view of the new innovation, the organization should

move quickly and end the agreement they have with

NPL in light of the fact that they have not purchased

any offers in the organization but rather just operation.

Net

profit

Margin

Net income margin has stayed

stable by virtue of comparative

development in the incomes and

net income. This is

characteristic of the way that the

productivity of the organization

has not expanded.

DIPL ought to likewise not depend on the straight line

strategy for devaluation in ascertaining the deterioration

of their advantages yet ought to depend on a technique

that considers that after consistently the estimation of a

benefit changes and thusly deterioration ought to be

computed from the present estimation of the benefit and

such strategies incorporate total of-year technique.

Answer to Question 2:

RISK REASON OF INHERENT RISK RISK OF MATERIAL

ROE has declined. from capacity should just be perceived upon the

genuine installment.

ROA

ROA of the organization has

declined. The purpose behind

the same could be the way that it

has obtained resources of NPL,

which has not contributed much

to incomes, subsequently the

denominator has expanded

while numerator has not

expanded proportionality thus

the ROA has gone down.

Concerning the journal and medical books by NPL

distributing organization getting to be plainly old in

view of the new innovation, the organization should

move quickly and end the agreement they have with

NPL in light of the fact that they have not purchased

any offers in the organization but rather just operation.

Net

profit

Margin

Net income margin has stayed

stable by virtue of comparative

development in the incomes and

net income. This is

characteristic of the way that the

productivity of the organization

has not expanded.

DIPL ought to likewise not depend on the straight line

strategy for devaluation in ascertaining the deterioration

of their advantages yet ought to depend on a technique

that considers that after consistently the estimation of a

benefit changes and thusly deterioration ought to be

computed from the present estimation of the benefit and

such strategies incorporate total of-year technique.

Answer to Question 2:

RISK REASON OF INHERENT RISK RISK OF MATERIAL

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

MISSTATEMENT

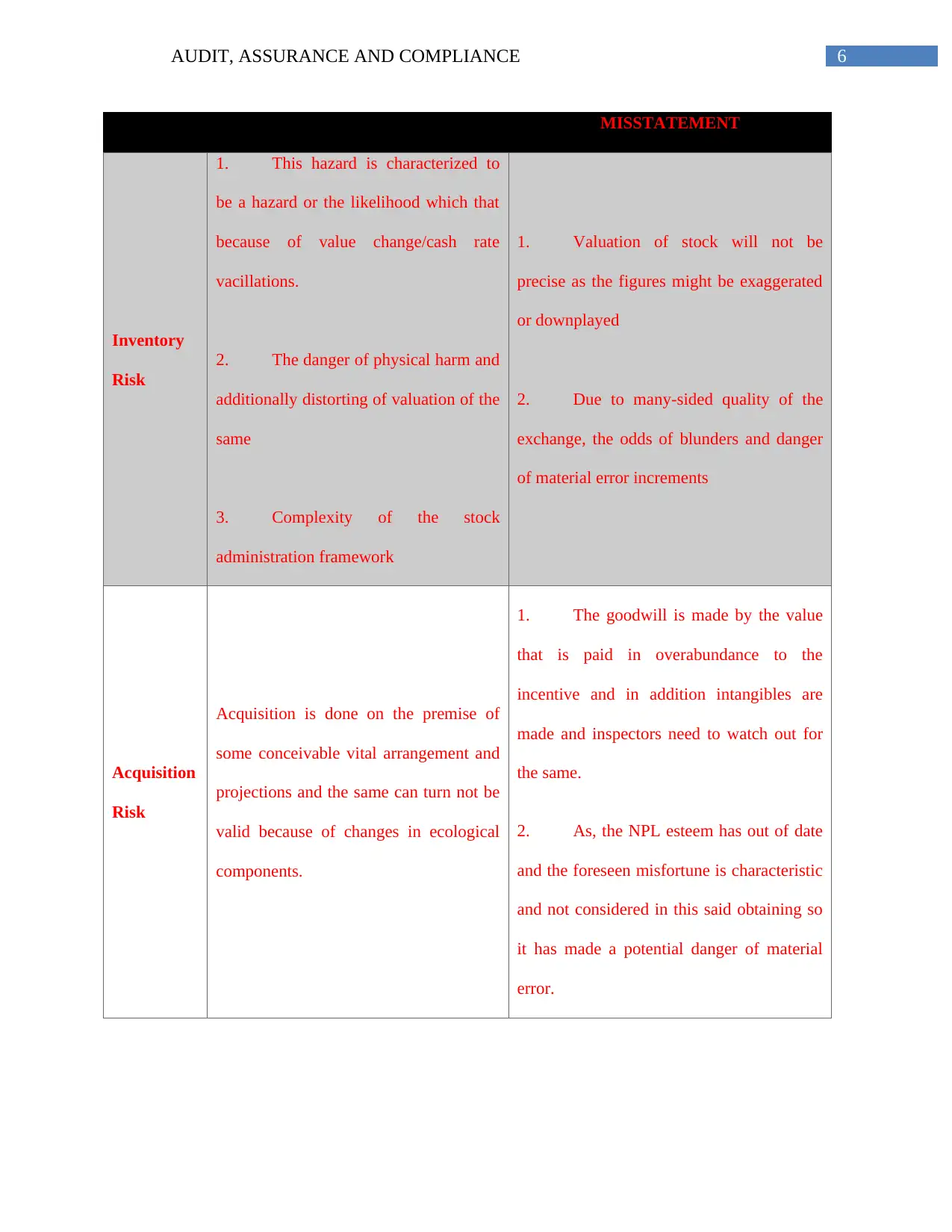

Inventory

Risk

1. This hazard is characterized to

be a hazard or the likelihood which that

because of value change/cash rate

vacillations.

2. The danger of physical harm and

additionally distorting of valuation of the

same

3. Complexity of the stock

administration framework

1. Valuation of stock will not be

precise as the figures might be exaggerated

or downplayed

2. Due to many-sided quality of the

exchange, the odds of blunders and danger

of material error increments

Acquisition

Risk

Acquisition is done on the premise of

some conceivable vital arrangement and

projections and the same can turn not be

valid because of changes in ecological

components.

1. The goodwill is made by the value

that is paid in overabundance to the

incentive and in addition intangibles are

made and inspectors need to watch out for

the same.

2. As, the NPL esteem has out of date

and the foreseen misfortune is characteristic

and not considered in this said obtaining so

it has made a potential danger of material

error.

MISSTATEMENT

Inventory

Risk

1. This hazard is characterized to

be a hazard or the likelihood which that

because of value change/cash rate

vacillations.

2. The danger of physical harm and

additionally distorting of valuation of the

same

3. Complexity of the stock

administration framework

1. Valuation of stock will not be

precise as the figures might be exaggerated

or downplayed

2. Due to many-sided quality of the

exchange, the odds of blunders and danger

of material error increments

Acquisition

Risk

Acquisition is done on the premise of

some conceivable vital arrangement and

projections and the same can turn not be

valid because of changes in ecological

components.

1. The goodwill is made by the value

that is paid in overabundance to the

incentive and in addition intangibles are

made and inspectors need to watch out for

the same.

2. As, the NPL esteem has out of date

and the foreseen misfortune is characteristic

and not considered in this said obtaining so

it has made a potential danger of material

error.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

Certain risk components could be raised from the business operations of DIPL. As per the

contextual investigation, the administration of an organization has neglected to enter different

business exchanges of the organization. This method has coordinate organization with the

irregularities in the arranging of various showcasing and deals exercises of the organization

(Earley et al. 2016). The general financial investigation did with regards to DIPL states that the

organization has neglected to finish the focused on level of benefit from the general deals

income. The essential reason is the insufficiency and wastefulness of the administration of the

organization in business operations. In this manner, it could be watched that the organization has

neglected to gage the impact of various miniaturized scale and full scale financial components

having sway on the business operations of DIPL like political, financial and social elements.

Consequently, it could be expressed that the lower income and overall revenue of the

organization has brought about inalienable dangers (Graham 2015).

Additionally, the staffs of DIPL have expanded quickly and thus, the innate risk has

expanded too. The inalienable risk level of the organization rises in view of the absence of

polished skill and experienced capability of the staffs. This is on the grounds that the

accomplishment of a business is dependent to a great extent on the execution of its staffs (Homb

et al. 2014). Because of such naiveté and wastefulness of the workforce of DIPL, there is more

noteworthy possibility of intrinsic dangers, since the representatives will undoubtedly lead

botches. In view of the given instance of DIPL, the issues could be found in the progression

procedure of CEO of the organization. Because of this, such process has brought about ascent in

natural dangers of the organization. The primary intrinsic risk could be seen in the inadequate

strategy for choosing the CEO progression of the organization.

Certain risk components could be raised from the business operations of DIPL. As per the

contextual investigation, the administration of an organization has neglected to enter different

business exchanges of the organization. This method has coordinate organization with the

irregularities in the arranging of various showcasing and deals exercises of the organization

(Earley et al. 2016). The general financial investigation did with regards to DIPL states that the

organization has neglected to finish the focused on level of benefit from the general deals

income. The essential reason is the insufficiency and wastefulness of the administration of the

organization in business operations. In this manner, it could be watched that the organization has

neglected to gage the impact of various miniaturized scale and full scale financial components

having sway on the business operations of DIPL like political, financial and social elements.

Consequently, it could be expressed that the lower income and overall revenue of the

organization has brought about inalienable dangers (Graham 2015).

Additionally, the staffs of DIPL have expanded quickly and thus, the innate risk has

expanded too. The inalienable risk level of the organization rises in view of the absence of

polished skill and experienced capability of the staffs. This is on the grounds that the

accomplishment of a business is dependent to a great extent on the execution of its staffs (Homb

et al. 2014). Because of such naiveté and wastefulness of the workforce of DIPL, there is more

noteworthy possibility of intrinsic dangers, since the representatives will undoubtedly lead

botches. In view of the given instance of DIPL, the issues could be found in the progression

procedure of CEO of the organization. Because of this, such process has brought about ascent in

natural dangers of the organization. The primary intrinsic risk could be seen in the inadequate

strategy for choosing the CEO progression of the organization.

8AUDIT, ASSURANCE AND COMPLIANCE

Other than this, it could be watched that DIPL does not have adequate staffs for dealing

with its business operations. This reason has brought about ascent in characteristic dangers in the

general business working of DIPL. Subsequently, from the above assessment, it could be

watched that these are the essential reasons of the ascent in natural dangers in the business

operations of DIPL (Jones and Beattie 2015).

Clarification:

It has been gathered that there is high measure of workload on the representatives of the

organization. The expanding workload brings about poor accounting of the organization and this

issue additionally brings about various issues of income, insufficient working outcomes

incapable solvency and liquidity position of the organization. Other than this, the danger of

blunder could be portrayed in the financial articulations because of absence of compelling

understanding. In this unique situation, the administration of DIPL needs to assume a compelling

part. It has been watched that the DIPL administration needs responsibility and uprightness and

because of this reason, they are experiencing the worry of losing notoriety in the business group.

The more noteworthy motivating force structure identified with administration shapes extra

weight on administration and it brings about material misquotes in the financial reports (Levy

2015).

Reply to Question 3:

Answer to Part A:

In the present business organizations, extortion risk is pronounced as the primary risk

with regards to the same. Due to the event of such fake risk, the business organizations

frequently acquire serious losses in its business resources (Martin, Sanders and Scalan 2014). In

Other than this, it could be watched that DIPL does not have adequate staffs for dealing

with its business operations. This reason has brought about ascent in characteristic dangers in the

general business working of DIPL. Subsequently, from the above assessment, it could be

watched that these are the essential reasons of the ascent in natural dangers in the business

operations of DIPL (Jones and Beattie 2015).

Clarification:

It has been gathered that there is high measure of workload on the representatives of the

organization. The expanding workload brings about poor accounting of the organization and this

issue additionally brings about various issues of income, insufficient working outcomes

incapable solvency and liquidity position of the organization. Other than this, the danger of

blunder could be portrayed in the financial articulations because of absence of compelling

understanding. In this unique situation, the administration of DIPL needs to assume a compelling

part. It has been watched that the DIPL administration needs responsibility and uprightness and

because of this reason, they are experiencing the worry of losing notoriety in the business group.

The more noteworthy motivating force structure identified with administration shapes extra

weight on administration and it brings about material misquotes in the financial reports (Levy

2015).

Reply to Question 3:

Answer to Part A:

In the present business organizations, extortion risk is pronounced as the primary risk

with regards to the same. Due to the event of such fake risk, the business organizations

frequently acquire serious losses in its business resources (Martin, Sanders and Scalan 2014). In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

greater part of the circumstances, the essential disappointment could be seen among the

workforce and such disappointment frequently constrain them to participate in different sorts of

fakes in organizations. Another essential reason of extortion is the desire of different financial

specialists of the organizations. The organizations regularly make guarantees for accomplishing a

particular financial execution that adds to more prominent misrepresentation level (Nalewaik and

Mills 2016).

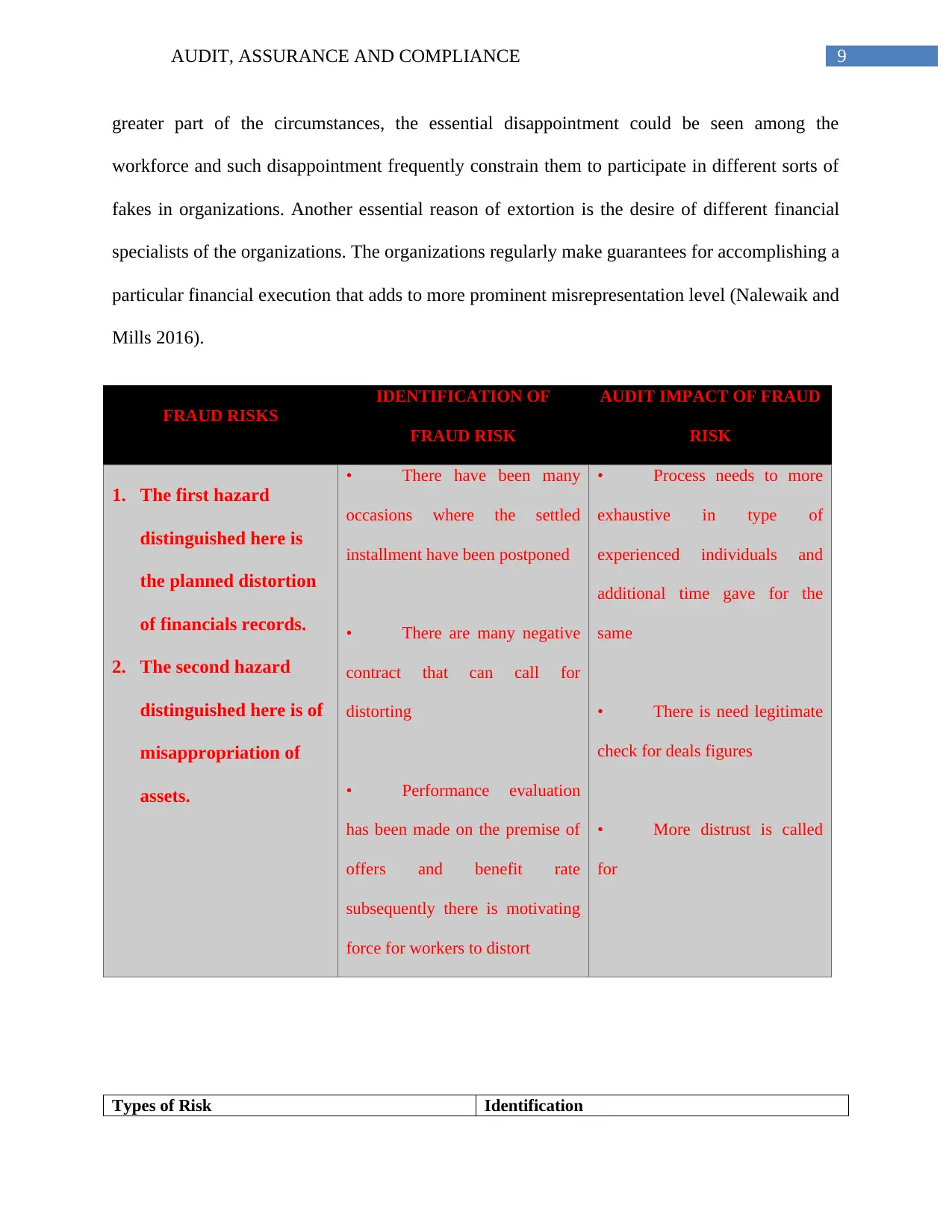

FRAUD RISKS

IDENTIFICATION OF

FRAUD RISK

AUDIT IMPACT OF FRAUD

RISK

1. The first hazard

distinguished here is

the planned distortion

of financials records.

2. The second hazard

distinguished here is of

misappropriation of

assets.

• There have been many

occasions where the settled

installment have been postponed

• There are many negative

contract that can call for

distorting

• Performance evaluation

has been made on the premise of

offers and benefit rate

subsequently there is motivating

force for workers to distort

• Process needs to more

exhaustive in type of

experienced individuals and

additional time gave for the

same

• There is need legitimate

check for deals figures

• More distrust is called

for

Types of Risk Identification

greater part of the circumstances, the essential disappointment could be seen among the

workforce and such disappointment frequently constrain them to participate in different sorts of

fakes in organizations. Another essential reason of extortion is the desire of different financial

specialists of the organizations. The organizations regularly make guarantees for accomplishing a

particular financial execution that adds to more prominent misrepresentation level (Nalewaik and

Mills 2016).

FRAUD RISKS

IDENTIFICATION OF

FRAUD RISK

AUDIT IMPACT OF FRAUD

RISK

1. The first hazard

distinguished here is

the planned distortion

of financials records.

2. The second hazard

distinguished here is of

misappropriation of

assets.

• There have been many

occasions where the settled

installment have been postponed

• There are many negative

contract that can call for

distorting

• Performance evaluation

has been made on the premise of

offers and benefit rate

subsequently there is motivating

force for workers to distort

• Process needs to more

exhaustive in type of

experienced individuals and

additional time gave for the

same

• There is need legitimate

check for deals figures

• More distrust is called

for

Types of Risk Identification

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

Fraud risk- In the setting of the business operations of

DIPL, the fundamental risk that could happen from

its business exercises is the inclusion of the staffs

in different sorts of fake exercises. This could

happen because of disappointment of the workers.

As per the given instance of DIPL, it could be

watched that there is gigantic weight from the piece

of the leading body of the organization to embrace

another arrangement of accounting. The selection

of this new arrangement of accounting builds up a

substantial weight on the workforce of the

organization and such weight brings about

extortion. Consequently, it could be expressed that

for adapting up to the compromise weight, the

staffs may embrace false exercises, which would

prompt inaccurate treatment of the general system

bringing about material errors.

As per the contextual investigation, it could

be watched that the system of wasteful treatment of

the usage of new data innovation brings about

insufficient treatment of couple of essential

financial and accounting exchanges toward the

complete of the year. This general procedure may

bring about loss of material misquotes and financial

data. Due to such freshness and wastefulness of the

Fraud risk- In the setting of the business operations of

DIPL, the fundamental risk that could happen from

its business exercises is the inclusion of the staffs

in different sorts of fake exercises. This could

happen because of disappointment of the workers.

As per the given instance of DIPL, it could be

watched that there is gigantic weight from the piece

of the leading body of the organization to embrace

another arrangement of accounting. The selection

of this new arrangement of accounting builds up a

substantial weight on the workforce of the

organization and such weight brings about

extortion. Consequently, it could be expressed that

for adapting up to the compromise weight, the

staffs may embrace false exercises, which would

prompt inaccurate treatment of the general system

bringing about material errors.

As per the contextual investigation, it could

be watched that the system of wasteful treatment of

the usage of new data innovation brings about

insufficient treatment of couple of essential

financial and accounting exchanges toward the

complete of the year. This general procedure may

bring about loss of material misquotes and financial

data. Due to such freshness and wastefulness of the

11AUDIT, ASSURANCE AND COMPLIANCE

workforce of DIPL, there is more prominent shot of

innate dangers, since the representatives will

undoubtedly direct oversights. In light of the given

instance of DIPL, the issues could be found in the

progression procedure of CEO of the organization.

Because of this, such process has brought about

ascent in characteristic risks of the organization.

The fundamental inalienable risk could be seen in

the ineffectual strategy for choosing the CEO

progression of the organization. It has been

watched that the DIPL administration needs

responsibility and uprightness and because of this

reason, they are experiencing the worry of losing

disrepute in the business group.

Procedure of financial reporting- Another significant risk is related with the

strategy of financial detailing. The more serious

risk of incapable financial statements could be

seen, if extra financial desires could be seen from

various partners for the financial revelations. This

is valid in instances of declaration from the

administration of the organization to accomplish

specific focus of execution and specific focus of the

destinations for obligation procurement. In light of

the financial reports of DIPL, it could be watched

that there is ascend in income of the organization

from 2013 to 2015. Other than this, there is

workforce of DIPL, there is more prominent shot of

innate dangers, since the representatives will

undoubtedly direct oversights. In light of the given

instance of DIPL, the issues could be found in the

progression procedure of CEO of the organization.

Because of this, such process has brought about

ascent in characteristic risks of the organization.

The fundamental inalienable risk could be seen in

the ineffectual strategy for choosing the CEO

progression of the organization. It has been

watched that the DIPL administration needs

responsibility and uprightness and because of this

reason, they are experiencing the worry of losing

disrepute in the business group.

Procedure of financial reporting- Another significant risk is related with the

strategy of financial detailing. The more serious

risk of incapable financial statements could be

seen, if extra financial desires could be seen from

various partners for the financial revelations. This

is valid in instances of declaration from the

administration of the organization to accomplish

specific focus of execution and specific focus of the

destinations for obligation procurement. In light of

the financial reports of DIPL, it could be watched

that there is ascend in income of the organization

from 2013 to 2015. Other than this, there is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.