AUDIT ASSURANCE AND COMPLIANCE: University Report, Financial Analysis

VerifiedAdded on 2020/03/04

|11

|2662

|206

Report

AI Summary

This report provides a comprehensive analysis of audit assurance and compliance, focusing on the financial statements of DIPL. It begins with an examination of analytical procedures, including ratio analysis of current, profit margin, and solvency ratios, and their impact on audit planning decisions. The report then identifies inherent risks arising from DIPL's business operations, such as complexities in transactions, management integrity, and employee involvement, and discusses how these risks contribute to material misstatements. Finally, it addresses the susceptibility to misstatement due to fraud risk, highlighting vulnerabilities related to employee dissatisfaction, pressure from the board, and issues with financial reporting and accounting system implementation. The analysis emphasizes the importance of mitigating these risks to ensure the accuracy and reliability of financial information.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit assurance and compliance

Name of the student

Name of the university

Author note

Audit assurance and compliance

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

QUESTION 1.............................................................................................................................2

QUESTION 2.............................................................................................................................4

QUESTION 3.............................................................................................................................7

Reference....................................................................................................................................9

Table of Contents

QUESTION 1.............................................................................................................................2

QUESTION 2.............................................................................................................................4

QUESTION 3.............................................................................................................................7

Reference....................................................................................................................................9

2AUDIT ASSURANCE AND COMPLIANCE

QUESTION 1

Analytical procedures of the financial statement are among the various financial audit

procedure that help the auditor to understand the business and any changes in the business of

the client and to recognize the potential risk sectors for planning the other audit procedures.

The analytical procedures also include the analysis of financial information. The auditor will

apply the analytical approach with regard to the financial statement of DIPL to break down

the problems into the components required for solving it (Arens et al. 2016). The analytical

approach that will be applied by the auditor will be same like the formal analysis. The

analysis procedures can be performed through utilization of various strategies and

approaches. However, the use of analytical procedure for the analysis of financial statement

various financial analyst as well as the various accountant interpret the information in

different way to arrive at the major business decisions (Cannon and Bedard 2016).

The analytical approach assists in comparing the annual statements of the

organization for different periods or the comparison among different organization. To

compare the financial statement, the analyst can take various items from the statement and

can analyse their reporting methods. For instance, the analyst can select the current liabilities

and current assets to analyse the liquidity position of the company or can select the any other

item like inventory to analyse its reporting method and the deviation, if any. Further, the audit

plan can be analysed through using the analytical procedure benchmark (Ruhnke and Schmidt

2014). Thereafter, the variance from the actual benchmark will assist in identifying the

difference and evaluations of the cause dedicated to the resulted variance. Apart from this, the

analysis of various ratios can be used as an appropriate approach that may be used for the

comparison of the information included in the financial statement and accordingly plan for

the audit.

QUESTION 1

Analytical procedures of the financial statement are among the various financial audit

procedure that help the auditor to understand the business and any changes in the business of

the client and to recognize the potential risk sectors for planning the other audit procedures.

The analytical procedures also include the analysis of financial information. The auditor will

apply the analytical approach with regard to the financial statement of DIPL to break down

the problems into the components required for solving it (Arens et al. 2016). The analytical

approach that will be applied by the auditor will be same like the formal analysis. The

analysis procedures can be performed through utilization of various strategies and

approaches. However, the use of analytical procedure for the analysis of financial statement

various financial analyst as well as the various accountant interpret the information in

different way to arrive at the major business decisions (Cannon and Bedard 2016).

The analytical approach assists in comparing the annual statements of the

organization for different periods or the comparison among different organization. To

compare the financial statement, the analyst can take various items from the statement and

can analyse their reporting methods. For instance, the analyst can select the current liabilities

and current assets to analyse the liquidity position of the company or can select the any other

item like inventory to analyse its reporting method and the deviation, if any. Further, the audit

plan can be analysed through using the analytical procedure benchmark (Ruhnke and Schmidt

2014). Thereafter, the variance from the actual benchmark will assist in identifying the

difference and evaluations of the cause dedicated to the resulted variance. Apart from this, the

analysis of various ratios can be used as an appropriate approach that may be used for the

comparison of the information included in the financial statement and accordingly plan for

the audit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT ASSURANCE AND COMPLIANCE

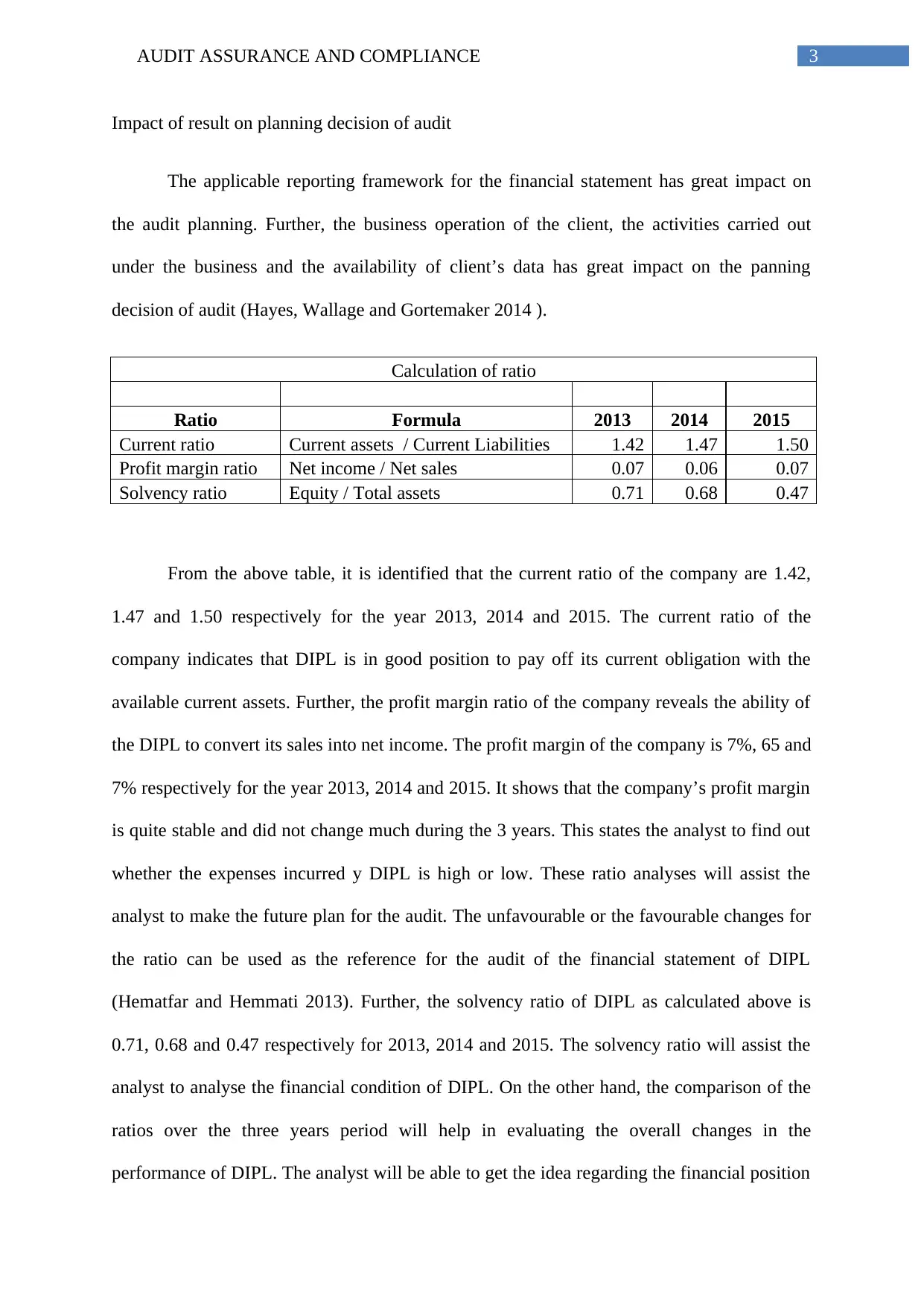

Impact of result on planning decision of audit

The applicable reporting framework for the financial statement has great impact on

the audit planning. Further, the business operation of the client, the activities carried out

under the business and the availability of client’s data has great impact on the panning

decision of audit (Hayes, Wallage and Gortemaker 2014 ).

Calculation of ratio

Ratio Formula 2013 2014 2015

Current ratio Current assets / Current Liabilities 1.42 1.47 1.50

Profit margin ratio Net income / Net sales 0.07 0.06 0.07

Solvency ratio Equity / Total assets 0.71 0.68 0.47

From the above table, it is identified that the current ratio of the company are 1.42,

1.47 and 1.50 respectively for the year 2013, 2014 and 2015. The current ratio of the

company indicates that DIPL is in good position to pay off its current obligation with the

available current assets. Further, the profit margin ratio of the company reveals the ability of

the DIPL to convert its sales into net income. The profit margin of the company is 7%, 65 and

7% respectively for the year 2013, 2014 and 2015. It shows that the company’s profit margin

is quite stable and did not change much during the 3 years. This states the analyst to find out

whether the expenses incurred y DIPL is high or low. These ratio analyses will assist the

analyst to make the future plan for the audit. The unfavourable or the favourable changes for

the ratio can be used as the reference for the audit of the financial statement of DIPL

(Hematfar and Hemmati 2013). Further, the solvency ratio of DIPL as calculated above is

0.71, 0.68 and 0.47 respectively for 2013, 2014 and 2015. The solvency ratio will assist the

analyst to analyse the financial condition of DIPL. On the other hand, the comparison of the

ratios over the three years period will help in evaluating the overall changes in the

performance of DIPL. The analyst will be able to get the idea regarding the financial position

Impact of result on planning decision of audit

The applicable reporting framework for the financial statement has great impact on

the audit planning. Further, the business operation of the client, the activities carried out

under the business and the availability of client’s data has great impact on the panning

decision of audit (Hayes, Wallage and Gortemaker 2014 ).

Calculation of ratio

Ratio Formula 2013 2014 2015

Current ratio Current assets / Current Liabilities 1.42 1.47 1.50

Profit margin ratio Net income / Net sales 0.07 0.06 0.07

Solvency ratio Equity / Total assets 0.71 0.68 0.47

From the above table, it is identified that the current ratio of the company are 1.42,

1.47 and 1.50 respectively for the year 2013, 2014 and 2015. The current ratio of the

company indicates that DIPL is in good position to pay off its current obligation with the

available current assets. Further, the profit margin ratio of the company reveals the ability of

the DIPL to convert its sales into net income. The profit margin of the company is 7%, 65 and

7% respectively for the year 2013, 2014 and 2015. It shows that the company’s profit margin

is quite stable and did not change much during the 3 years. This states the analyst to find out

whether the expenses incurred y DIPL is high or low. These ratio analyses will assist the

analyst to make the future plan for the audit. The unfavourable or the favourable changes for

the ratio can be used as the reference for the audit of the financial statement of DIPL

(Hematfar and Hemmati 2013). Further, the solvency ratio of DIPL as calculated above is

0.71, 0.68 and 0.47 respectively for 2013, 2014 and 2015. The solvency ratio will assist the

analyst to analyse the financial condition of DIPL. On the other hand, the comparison of the

ratios over the three years period will help in evaluating the overall changes in the

performance of DIPL. The analyst will be able to get the idea regarding the financial position

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT ASSURANCE AND COMPLIANCE

trend of the company and analyse whether the position of the company is favourable or

unfavourable.

QUESTION 2

Identification of inherent risk arise from the business operation of DIPL

Inherent risk is that risk which is posed by omission or error in the financial statement

owing to the factor except the control failure. Under the financial audit, the inherent risk

expected to take place when the nature of transaction is complex or under the circumstance

where the situation demands for high level of judgement with regard to the financial

estimations. This kind of risk is worst of the kind as it cannot be controlled through the

defined measures. The inherent risk is the risk that must be looked in depth while the

financial statements are reviewed by the analysts or auditors. When carrying out the audit or

the business is analyzed the analyst or the auditor shall try to understand the business nature

while the internal risk or inherent risks are examined. If the control risk or the inherent risk

are considered as high, the auditor shall set the level of detection risk as higher for maintain

the overall audit risk at the reasonable level.

As per the given case study, there are various transactions those were not taken into

account while the financial statements were prepared either intentionally or by mistake by the

accountant or the management of DIPL. This will lead to the inconsistencies with regard to

the inefficient planning specifically with regard to the marketing as well as the sales

activities. Further, it is also identified from the financial statement that the company failed to

achieve the target profit level as compared to the level of sales. The reason behind this is that

the failure on the part of the management with regard to the identification of specific items

and fulfilment of consequent requirement (Knechel and Salterio 2016). Therefore, it can be

stated that DIPL has failed in analysing various macro as well as micro-economic objectives

trend of the company and analyse whether the position of the company is favourable or

unfavourable.

QUESTION 2

Identification of inherent risk arise from the business operation of DIPL

Inherent risk is that risk which is posed by omission or error in the financial statement

owing to the factor except the control failure. Under the financial audit, the inherent risk

expected to take place when the nature of transaction is complex or under the circumstance

where the situation demands for high level of judgement with regard to the financial

estimations. This kind of risk is worst of the kind as it cannot be controlled through the

defined measures. The inherent risk is the risk that must be looked in depth while the

financial statements are reviewed by the analysts or auditors. When carrying out the audit or

the business is analyzed the analyst or the auditor shall try to understand the business nature

while the internal risk or inherent risks are examined. If the control risk or the inherent risk

are considered as high, the auditor shall set the level of detection risk as higher for maintain

the overall audit risk at the reasonable level.

As per the given case study, there are various transactions those were not taken into

account while the financial statements were prepared either intentionally or by mistake by the

accountant or the management of DIPL. This will lead to the inconsistencies with regard to

the inefficient planning specifically with regard to the marketing as well as the sales

activities. Further, it is also identified from the financial statement that the company failed to

achieve the target profit level as compared to the level of sales. The reason behind this is that

the failure on the part of the management with regard to the identification of specific items

and fulfilment of consequent requirement (Knechel and Salterio 2016). Therefore, it can be

stated that DIPL has failed in analysing various macro as well as micro-economic objectives

5AUDIT ASSURANCE AND COMPLIANCE

that should have been considered in form of social, economic or political factors. This can be

identified from the poor sales figure of DIPL which in turn exposes the company to various

inherent risks.

In addition to above mentioned facts, it was also found that the employees from DIPL

also involved in increasing the inherent risk of the company. Moreover, other considerable

facts that exposed the company towards the inherent risks are classified under various

segments. To be more specific, the external factors as well as the material misstatement,

environmental factors and true and for view approach also contributed to the inherent risk for

the business of DIPL. From the analysis of the given case study of DIPL it is identified that

difficulties and complexities involved in the process of appointment of the CEO also led to

exposure to inherent risk. Generally, the appointment of the CEO is considered as different as

he is a distinct individual. Furthermore, various inherent risks that were involved in the

appointment procedure of the CEO, transition procedure for the previous CEO, Ms. Rebecca

Styles and the commencement of activities by Mr. William Jackson are involved with various

inherent risk as the mentioned procedure were not complied with the required strategies.

Further, the processes were initiated late and moreover, the lower level of involvement by the

CEO in the procedures and leaving of the employees may also expose the company to the

inherent risks.

Another risk statement was that associated with the maintenance of records with

regard to the receipts of cash by the cashier, Mr Judy Bones. Generally, most of the payments

by DIPL are received through electronic transfer of fund (Cipriano, Hamilton and

Vandervelde 2016). Thereafter, maintaining the receipt copy after downloading it from the

mail and reconciling the total batch posting are done by Mr. Judy only. However, the bank

reconciliation statement is prepared by the assistant accountant, Mr Body Roger at the closing

of every month. It is suggested that the reconciliation statement shall be prepared more

that should have been considered in form of social, economic or political factors. This can be

identified from the poor sales figure of DIPL which in turn exposes the company to various

inherent risks.

In addition to above mentioned facts, it was also found that the employees from DIPL

also involved in increasing the inherent risk of the company. Moreover, other considerable

facts that exposed the company towards the inherent risks are classified under various

segments. To be more specific, the external factors as well as the material misstatement,

environmental factors and true and for view approach also contributed to the inherent risk for

the business of DIPL. From the analysis of the given case study of DIPL it is identified that

difficulties and complexities involved in the process of appointment of the CEO also led to

exposure to inherent risk. Generally, the appointment of the CEO is considered as different as

he is a distinct individual. Furthermore, various inherent risks that were involved in the

appointment procedure of the CEO, transition procedure for the previous CEO, Ms. Rebecca

Styles and the commencement of activities by Mr. William Jackson are involved with various

inherent risk as the mentioned procedure were not complied with the required strategies.

Further, the processes were initiated late and moreover, the lower level of involvement by the

CEO in the procedures and leaving of the employees may also expose the company to the

inherent risks.

Another risk statement was that associated with the maintenance of records with

regard to the receipts of cash by the cashier, Mr Judy Bones. Generally, most of the payments

by DIPL are received through electronic transfer of fund (Cipriano, Hamilton and

Vandervelde 2016). Thereafter, maintaining the receipt copy after downloading it from the

mail and reconciling the total batch posting are done by Mr. Judy only. However, the bank

reconciliation statement is prepared by the assistant accountant, Mr Body Roger at the closing

of every month. It is suggested that the reconciliation statement shall be prepared more

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT ASSURANCE AND COMPLIANCE

frequently and shall not left it for the end of the month. Further, revenue generated by the

company through selling of e-book, reprint of the text books may lead to inherent risks, if the

records are not maintained properly.

Apart from the above mentioned facts, the raw material inventory valuation process at

average cost was not appropriate as the current cost of paper significantly increased from the

presently applied average cost (Burk and Hendry 2014).

How the inherent risk have an impact on the material misstatement

The inherent risk is that risk which leads to material misstatement of the financial

statement that may arise owing to the omission or error as the result of the factors except the

control failure. It leads to material misstatement owing to the lapse or absence of the controls

that are separately controlled in assessing the control risk (William, Glover and Prawitt

2016). The impact of the inherent risk on the material misstatements are as follows –

Integrity of the management – the management level of DIPL will definitely lack the

requirement under the integrity and objectivity which in turn will have an impact on

the status of the company in the long-run

Misrepresentation of the financial statement – the inherent risk will misrepresent the

financial information to the users of the financial statement like stakeholders,

creditors, debtors and the potential investors (Titera 2013.).

Performance of the business – the inherent risk will also misrepresent the growth

status of the business or the performance of the company. It will mislead the

stakeholders, creditors and the investors and the management will not be able to take

important decision within required time period.

frequently and shall not left it for the end of the month. Further, revenue generated by the

company through selling of e-book, reprint of the text books may lead to inherent risks, if the

records are not maintained properly.

Apart from the above mentioned facts, the raw material inventory valuation process at

average cost was not appropriate as the current cost of paper significantly increased from the

presently applied average cost (Burk and Hendry 2014).

How the inherent risk have an impact on the material misstatement

The inherent risk is that risk which leads to material misstatement of the financial

statement that may arise owing to the omission or error as the result of the factors except the

control failure. It leads to material misstatement owing to the lapse or absence of the controls

that are separately controlled in assessing the control risk (William, Glover and Prawitt

2016). The impact of the inherent risk on the material misstatements are as follows –

Integrity of the management – the management level of DIPL will definitely lack the

requirement under the integrity and objectivity which in turn will have an impact on

the status of the company in the long-run

Misrepresentation of the financial statement – the inherent risk will misrepresent the

financial information to the users of the financial statement like stakeholders,

creditors, debtors and the potential investors (Titera 2013.).

Performance of the business – the inherent risk will also misrepresent the growth

status of the business or the performance of the company. It will mislead the

stakeholders, creditors and the investors and the management will not be able to take

important decision within required time period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT ASSURANCE AND COMPLIANCE

QUESTION 3

Susceptibility to misstatement due to fraud risk

A business may lose a considerable amount of its asset owing to fraud. The impact of

fraud can even lead to the closure of the business (Nalewaik and Mills 2016). Thus, the

owner shall take appropriate measures to establish the methods to minimize the level of risk

due to fraud. Number of factors is there that exposes the company to fraud. These risks have

an impact on various factors like value an size of the business, ease of reselling the items and

cash are few to be named.

The biggest risk that DIPL is susceptible to owing to its activities and operation is the

engagement of the workforce in the fraudulent procedure as most of the employees are not

satisfied with the company. As per the given case study of DIPL, there was extreme pressure

from the board of DIPL, owing to which the IT department of the company however

managed to install the new accounting system, irrespective of the fact that the IT manager,

Mr Andy Rogers was not satisfied regarding the installation system of the machine. Further,

he claimed that the excessive pressures were put on the employees for the installation of the

system. However, DIPL did not have sufficient employees to reconcile and test the new

system properly (Louwers et al. 2015). Moreover, the preliminary testing revealed that few

transactions that were carried out at the closing of the year were not properly allocated under

proper period. This procedure may expose DIPL to fraud risk as well as material risk.

Another major risk associated with the operation of DIPL is that reporting of the

financial information. The financial statement has great significance to the external as well as

the internal users of the statement. The financial statement of DIPL revealed that the revenue

of the organization was in increasing trend and both the gross profit as well as the net profit

was in increasing trend. However, it is mentioned in the case study that the company availed

QUESTION 3

Susceptibility to misstatement due to fraud risk

A business may lose a considerable amount of its asset owing to fraud. The impact of

fraud can even lead to the closure of the business (Nalewaik and Mills 2016). Thus, the

owner shall take appropriate measures to establish the methods to minimize the level of risk

due to fraud. Number of factors is there that exposes the company to fraud. These risks have

an impact on various factors like value an size of the business, ease of reselling the items and

cash are few to be named.

The biggest risk that DIPL is susceptible to owing to its activities and operation is the

engagement of the workforce in the fraudulent procedure as most of the employees are not

satisfied with the company. As per the given case study of DIPL, there was extreme pressure

from the board of DIPL, owing to which the IT department of the company however

managed to install the new accounting system, irrespective of the fact that the IT manager,

Mr Andy Rogers was not satisfied regarding the installation system of the machine. Further,

he claimed that the excessive pressures were put on the employees for the installation of the

system. However, DIPL did not have sufficient employees to reconcile and test the new

system properly (Louwers et al. 2015). Moreover, the preliminary testing revealed that few

transactions that were carried out at the closing of the year were not properly allocated under

proper period. This procedure may expose DIPL to fraud risk as well as material risk.

Another major risk associated with the operation of DIPL is that reporting of the

financial information. The financial statement has great significance to the external as well as

the internal users of the statement. The financial statement of DIPL revealed that the revenue

of the organization was in increasing trend and both the gross profit as well as the net profit

was in increasing trend. However, it is mentioned in the case study that the company availed

8AUDIT ASSURANCE AND COMPLIANCE

a loan amounting to 7.5 million during 2015 (Duncan and Whittington 2014). Further, the

current ratio of the company was moving around 1.50 in association with the debt equity of

less than 1. It indicates that the requirement will put pressure on the company to maintain the

financial ratio to improve its liquidity position and avail the loan as per requirement.

Otherwise, they will not be able to avail the loan from BDO Finance.

Identification of risk factors

It is recognized from the case study that the valuation procedure of various raw

material based on the average cost method was not in order. Further, there exist the

fraudulent procedures in implementation of the new IT machine. Moreover, there were non-

compliances in preparation of the financial statement of DIPL.

a loan amounting to 7.5 million during 2015 (Duncan and Whittington 2014). Further, the

current ratio of the company was moving around 1.50 in association with the debt equity of

less than 1. It indicates that the requirement will put pressure on the company to maintain the

financial ratio to improve its liquidity position and avail the loan as per requirement.

Otherwise, they will not be able to avail the loan from BDO Finance.

Identification of risk factors

It is recognized from the case study that the valuation procedure of various raw

material based on the average cost method was not in order. Further, there exist the

fraudulent procedures in implementation of the new IT machine. Moreover, there were non-

compliances in preparation of the financial statement of DIPL.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT ASSURANCE AND COMPLIANCE

Reference

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Burk, J.A. and Hendry, J.A., 2014. Risk-Based Auditing. Professional Safety, 59(6), p.76.

Cannon, N. and Bedard, J.C., 2016. Auditing challenging fair value measurements: Evidence

from the field. The Accounting Review.

Cipriano, M., Hamilton, E.L. and Vandervelde, S.D., 2016. Newport Soup Inc.: An

interactive inherent risk assessment case. Journal of Accounting Education, 37, pp.13-23.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance

and audit: Does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Hayes, R., Wallage, P. and Gortemaker, H., 2014. Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Hematfar, M. and Hemmati, M., 2013. A Comparison of Risk-Based and Traditional

Auditing and their Effect on the Quality of Audit Reports.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of

Audit, Oversight, and Compliance for Project Success. CRC Press.

Reference

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Burk, J.A. and Hendry, J.A., 2014. Risk-Based Auditing. Professional Safety, 59(6), p.76.

Cannon, N. and Bedard, J.C., 2016. Auditing challenging fair value measurements: Evidence

from the field. The Accounting Review.

Cipriano, M., Hamilton, E.L. and Vandervelde, S.D., 2016. Newport Soup Inc.: An

interactive inherent risk assessment case. Journal of Accounting Education, 37, pp.13-23.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance

and audit: Does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Hayes, R., Wallage, P. and Gortemaker, H., 2014. Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Hematfar, M. and Hemmati, M., 2013. A Comparison of Risk-Based and Traditional

Auditing and their Effect on the Quality of Audit Reports.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of

Audit, Oversight, and Compliance for Project Success. CRC Press.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT ASSURANCE AND COMPLIANCE

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), pp.247-269.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), pp.247-269.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.