Audit, Assurance, and Compliance Report: TWE and ASX Principles

VerifiedAdded on 2021/06/14

|20

|3220

|19

Report

AI Summary

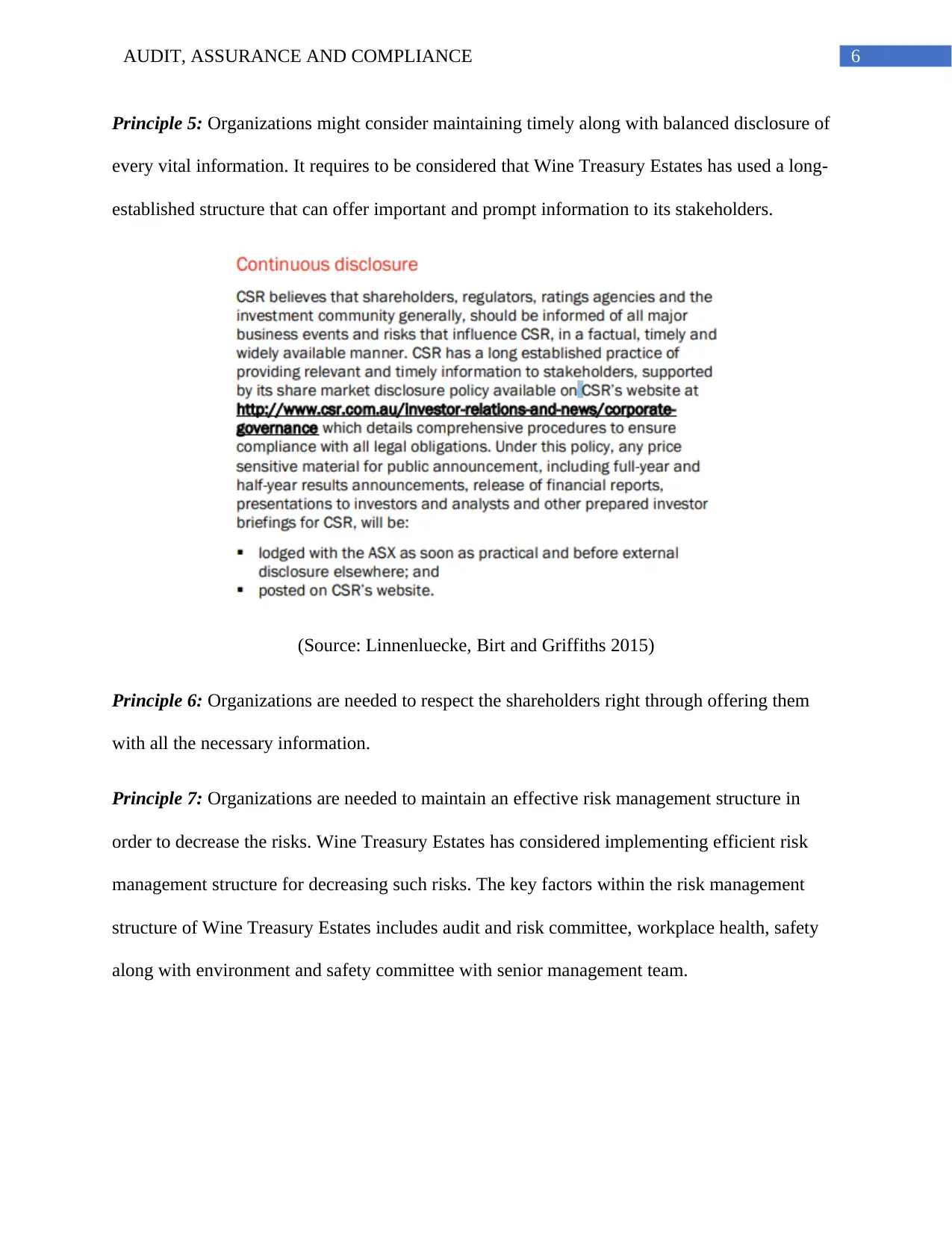

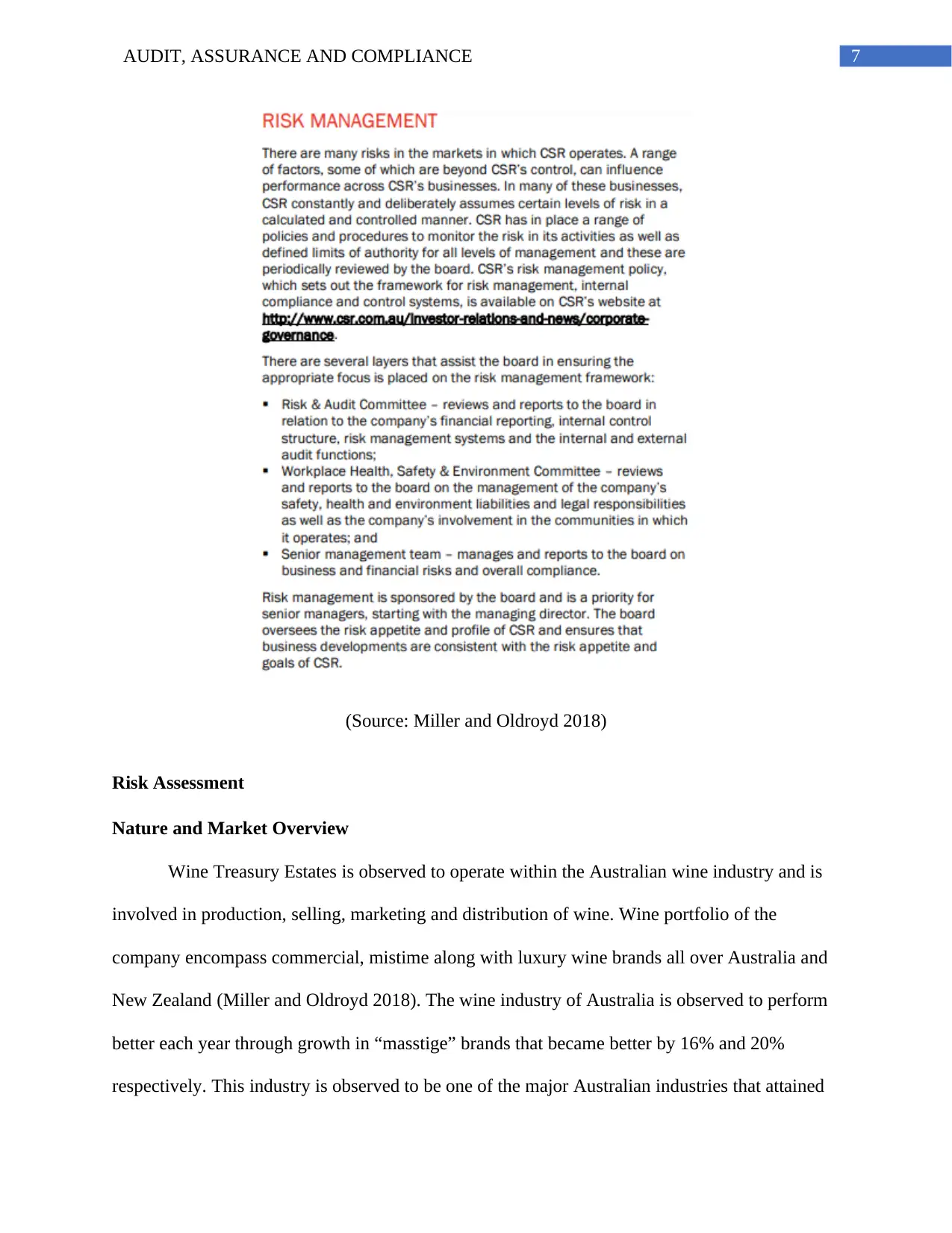

This report provides a comprehensive analysis of the audit, assurance, and compliance practices of Treasury Wine Estates (TWE), focusing on its adherence to the ASX Corporate Governance Council (CGC) principles. The report begins with an introduction to auditing and the importance of corporate governance, followed by an examination of TWE's compliance with each of the seven ASX CGC principles. It assesses TWE's risk management strategies, including its approach to risk assessment, the nature and market overview of the wine industry, regulatory compliance, and the identification of relevant business and financial risks. The report includes financial ratio analysis (profitability, liquidity, efficiency, and solvency) to evaluate TWE's financial performance. Furthermore, it identifies key risks such as currency fluctuations, competitive pressures, and climate change, along with potential steps to mitigate these risks. The report concludes with a summary of findings and recommendations, emphasizing the importance of robust corporate governance and effective risk management in the wine industry. The report highlights the importance of maintaining financial integrity, timely disclosure, and shareholder rights within the context of the ASX guidelines.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.