Analysis of Audit, Assurance, and Compliance in AZN Banking

VerifiedAdded on 2023/06/05

|13

|3807

|424

Report

AI Summary

This report provides an in-depth analysis of audit, assurance, and compliance within the context of financial reporting, specifically using AZN Banking as a case study. It examines the importance of audit reporting quality and the adherence to accounting standards to provide assurance to financial information users. The report highlights the auditor's independence, emphasizing objectivity and integrity, and details the key roles and responsibilities of the audit committee, including its structure and functions. Various audit procedures, such as tests of controls, substantive tests of detail, and analytical procedures, are discussed to demonstrate how auditors provide assurance. Furthermore, the report analyzes the auditor's opinion, the roles of management and directors in financial reporting, and elements that indicate the effectiveness of an audit report, covering audit fees and remuneration. This report provides a comprehensive overview of audit processes, compliance requirements, and the significance of assurance in ensuring the reliability and transparency of financial statements.

Running head: AUDIT, ASSURANCE AND COMPLIANCE 1

Audit, Assurance and Compliance

Student’s Name

Institution Affiliate

Date

Audit, Assurance and Compliance

Student’s Name

Institution Affiliate

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE 2

Executive Summary

The quality of audit reporting is a fundamental issue in every company. The auditors are

all expected to comply with the various accounting standards when preparing their audit report,

and this is to provide assurance to the users of the financial information. This report aims at

highlighting some of the key issues undertaken during the auditing work to provide effective

material information which is beneficial to the company. The report has illustrated the

independence requirements of an audit report such as objectivity and integrity. Further, the

key roles and responsibilities of the audit committee have also been highlighted in the paper. The

various audit procedures have also been highlighted in the report such as the substantive detail

testing of the financial statements. Lastly, the report has explained the elements which typically

indicates the effectiveness of a particular audit report and all of the above issues have been

discussed in the paper below.

Introduction

Audit reports generally must give an assurance to the managers and directors of a

company a clear view of the financial position of such a fimr.There are therefore certain aspects

which have to be taken into considerations such as the audit procedures, various audit opinions,

existence of audit committee and factors which makes an audit report to be effective. Audit

assurance focuses on evaluating financial statements while compliance on the other hand focuses

on adherence to the laws, regulations and standards. This paper will focus on some of the above

mentioned aspects of audit, assurance and compliance.

Audit, Assurance, and Compliance

The company selected in the ASX is AZN Banking. Based on the assessment of the

auditors' section including the other areas of the auditors there are a number of an issue which

Executive Summary

The quality of audit reporting is a fundamental issue in every company. The auditors are

all expected to comply with the various accounting standards when preparing their audit report,

and this is to provide assurance to the users of the financial information. This report aims at

highlighting some of the key issues undertaken during the auditing work to provide effective

material information which is beneficial to the company. The report has illustrated the

independence requirements of an audit report such as objectivity and integrity. Further, the

key roles and responsibilities of the audit committee have also been highlighted in the paper. The

various audit procedures have also been highlighted in the report such as the substantive detail

testing of the financial statements. Lastly, the report has explained the elements which typically

indicates the effectiveness of a particular audit report and all of the above issues have been

discussed in the paper below.

Introduction

Audit reports generally must give an assurance to the managers and directors of a

company a clear view of the financial position of such a fimr.There are therefore certain aspects

which have to be taken into considerations such as the audit procedures, various audit opinions,

existence of audit committee and factors which makes an audit report to be effective. Audit

assurance focuses on evaluating financial statements while compliance on the other hand focuses

on adherence to the laws, regulations and standards. This paper will focus on some of the above

mentioned aspects of audit, assurance and compliance.

Audit, Assurance, and Compliance

The company selected in the ASX is AZN Banking. Based on the assessment of the

auditors' section including the other areas of the auditors there are a number of an issue which

AUDIT, ASSURANCE AND COMPLIANCE 3

has been noted. For example, the auditor has complied with the independence requirements. One

of the requirements of an auditor’s independence is that the auditor must hold the highest levels

of integrity and this was displayed in the auditor’s report. The auditor expressed the highest

levels of integrity by being honest while carrying out his duties (Church, Jenkins & Stanley,

2018). Additionally, the auditor was objective while carrying out the audit work and this

typically forms one of the key requirements for independence of an auditor. The audit report also

indicated more disclosure of information and also an increased communication with the

management.

The huge disclosure of information and more communication with the management is a

fundamental requirement of an auditor’s independence, and this was exhibited in the financial

statements under the auditors' section, and hence the auditor complied with the auditor’s

independence requirement (Peterson, 2018). Further, there were few cases of conflicts of interest

between the management and the auditor. The few cases of conflict of interest are one of the

critical requirements for an auditor's independence, and thus the auditor had adhered to the

independence requirements. The company also has the audit committee who are responsible for

pre-approval services after an audit report has been submitted to them. Audit committee typically

forms the significant requirements for auditor independence and this, therefore, proves that

indeed the auditors had complied with the independence requirements (Roy & Saha, 2018).

The auditor's section also indicated that the prohibited non-audit services such as

actuarial services, bookkeeping, valuation of services and financial information system design

had not been carried out by the auditor (Carcello, Neal, Reid & Shipman, 2017). The prohibited

non-audit services are one of the essential requirements of an auditor's independence, and this,

has been noted. For example, the auditor has complied with the independence requirements. One

of the requirements of an auditor’s independence is that the auditor must hold the highest levels

of integrity and this was displayed in the auditor’s report. The auditor expressed the highest

levels of integrity by being honest while carrying out his duties (Church, Jenkins & Stanley,

2018). Additionally, the auditor was objective while carrying out the audit work and this

typically forms one of the key requirements for independence of an auditor. The audit report also

indicated more disclosure of information and also an increased communication with the

management.

The huge disclosure of information and more communication with the management is a

fundamental requirement of an auditor’s independence, and this was exhibited in the financial

statements under the auditors' section, and hence the auditor complied with the auditor’s

independence requirement (Peterson, 2018). Further, there were few cases of conflicts of interest

between the management and the auditor. The few cases of conflict of interest are one of the

critical requirements for an auditor's independence, and thus the auditor had adhered to the

independence requirements. The company also has the audit committee who are responsible for

pre-approval services after an audit report has been submitted to them. Audit committee typically

forms the significant requirements for auditor independence and this, therefore, proves that

indeed the auditors had complied with the independence requirements (Roy & Saha, 2018).

The auditor's section also indicated that the prohibited non-audit services such as

actuarial services, bookkeeping, valuation of services and financial information system design

had not been carried out by the auditor (Carcello, Neal, Reid & Shipman, 2017). The prohibited

non-audit services are one of the essential requirements of an auditor's independence, and this,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE 4

therefore, confirmed that the auditor of the company had complied with the independence

requirement.

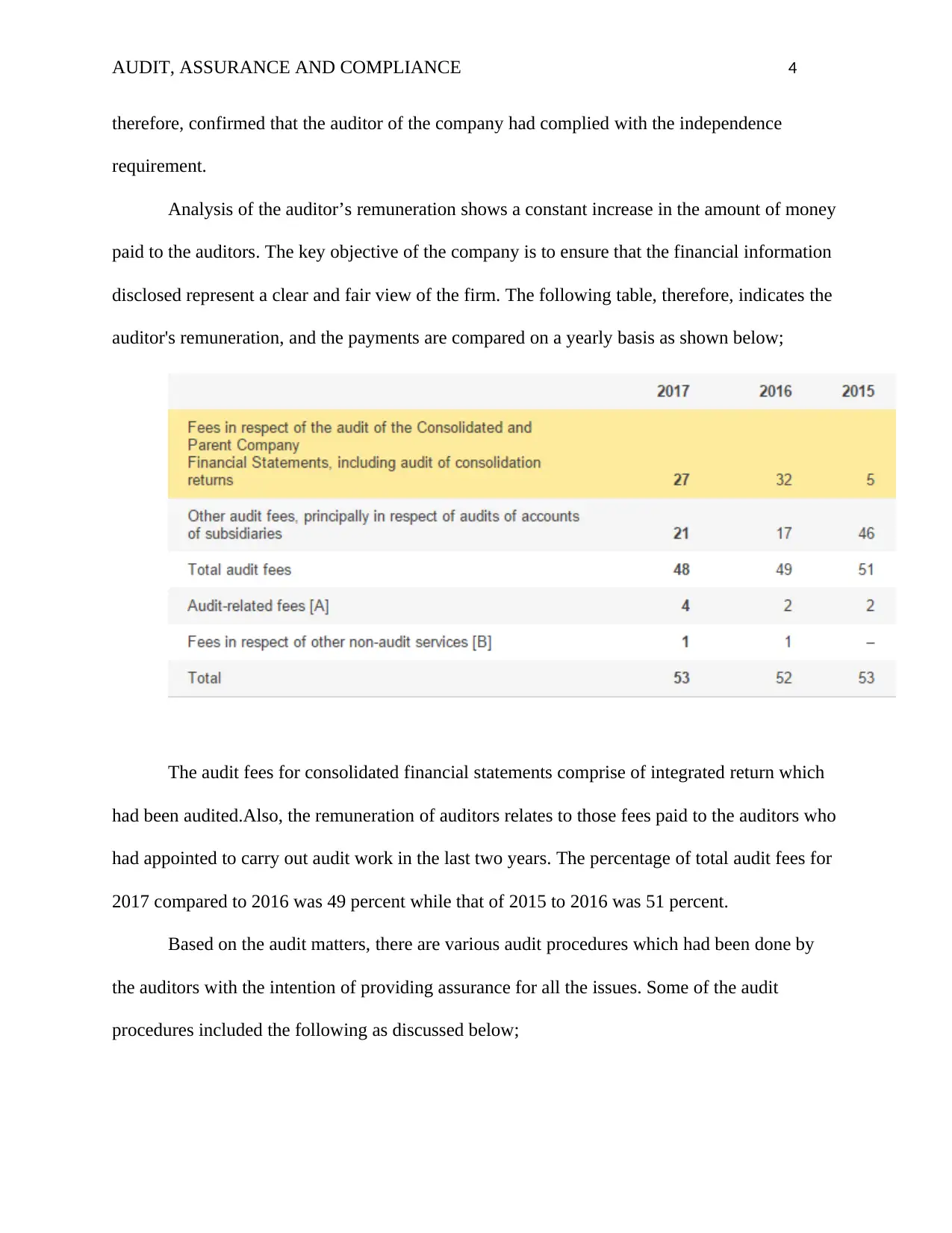

Analysis of the auditor’s remuneration shows a constant increase in the amount of money

paid to the auditors. The key objective of the company is to ensure that the financial information

disclosed represent a clear and fair view of the firm. The following table, therefore, indicates the

auditor's remuneration, and the payments are compared on a yearly basis as shown below;

The audit fees for consolidated financial statements comprise of integrated return which

had been audited.Also, the remuneration of auditors relates to those fees paid to the auditors who

had appointed to carry out audit work in the last two years. The percentage of total audit fees for

2017 compared to 2016 was 49 percent while that of 2015 to 2016 was 51 percent.

Based on the audit matters, there are various audit procedures which had been done by

the auditors with the intention of providing assurance for all the issues. Some of the audit

procedures included the following as discussed below;

therefore, confirmed that the auditor of the company had complied with the independence

requirement.

Analysis of the auditor’s remuneration shows a constant increase in the amount of money

paid to the auditors. The key objective of the company is to ensure that the financial information

disclosed represent a clear and fair view of the firm. The following table, therefore, indicates the

auditor's remuneration, and the payments are compared on a yearly basis as shown below;

The audit fees for consolidated financial statements comprise of integrated return which

had been audited.Also, the remuneration of auditors relates to those fees paid to the auditors who

had appointed to carry out audit work in the last two years. The percentage of total audit fees for

2017 compared to 2016 was 49 percent while that of 2015 to 2016 was 51 percent.

Based on the audit matters, there are various audit procedures which had been done by

the auditors with the intention of providing assurance for all the issues. Some of the audit

procedures included the following as discussed below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE 5

Test of Controls

The above procedure was carried out to determine the effectiveness of the control

measure which was being sued by the management of the company. The procedure helps to

detect any particular material misstatements. There are various categories of a test of controls

which were used by the auditors and such include, an observation which entailed looking at a

variety of business processes and the control elements (Blokdijk, Drieenhuizen, Simunic &

Stein, 2014). The other category of test control which had been used was the inspection where

the auditors inspected different documents for approval such as stamps and signatures, and this

was to ascertain whether the controls had been conducted properly. The last category of tests of

control was reperformance, and this involved the initiation of new transactions in determining

whether the client had applied the controls.

Substantive Tests of Detail

The substantive testing is also another audit procedure which had been used by the

auditors of the company. The procedure was primarily conducted to assess the financial

statements including the supporting documents to get errors in the annual report. Further, the

audit procedure above was done to ensure that all the financial records were accurate, valid and

complete (Blokdijk et al., 2014). There are a variety of samples in which the tests had been

carried out in, and they included, contact of various clients to validate that the accounts

receivable were accurate. The other test was to ascertain the accuracy of inventory valuation

estimations. Some of the other tests were communication with the suppliers to validate whether

the accounts payable were accurate or not and a bank confirmation was issued to validate the

ending cash balances. During this procedure, the minutes of the board of directors were reviewed

Test of Controls

The above procedure was carried out to determine the effectiveness of the control

measure which was being sued by the management of the company. The procedure helps to

detect any particular material misstatements. There are various categories of a test of controls

which were used by the auditors and such include, an observation which entailed looking at a

variety of business processes and the control elements (Blokdijk, Drieenhuizen, Simunic &

Stein, 2014). The other category of test control which had been used was the inspection where

the auditors inspected different documents for approval such as stamps and signatures, and this

was to ascertain whether the controls had been conducted properly. The last category of tests of

control was reperformance, and this involved the initiation of new transactions in determining

whether the client had applied the controls.

Substantive Tests of Detail

The substantive testing is also another audit procedure which had been used by the

auditors of the company. The procedure was primarily conducted to assess the financial

statements including the supporting documents to get errors in the annual report. Further, the

audit procedure above was done to ensure that all the financial records were accurate, valid and

complete (Blokdijk et al., 2014). There are a variety of samples in which the tests had been

carried out in, and they included, contact of various clients to validate that the accounts

receivable were accurate. The other test was to ascertain the accuracy of inventory valuation

estimations. Some of the other tests were communication with the suppliers to validate whether

the accounts payable were accurate or not and a bank confirmation was issued to validate the

ending cash balances. During this procedure, the minutes of the board of directors were reviewed

AUDIT, ASSURANCE AND COMPLIANCE 6

to check for the presence of dividends which had been approved by the directors of the company

(Graham, Bedard & Dutta, 2018).

Substantive Test of Balances or Analytical Procedures.

The analytical procedure is also one of the audit procedures which had been used by the

auditors of the company. It entailed an assessment of the financial information by evaluating the

relationship between the non-financial and financial data. The key examples of analytical tests

which had been used by the auditors were the regression analysis and trend ratio. Also, the above

audit procedure was used together with the other audit procedures such as the substantive testing.

The primary reason for the integration of the other procedures was to identify the misstatements

in the various account balances (Tricker, 2016). Additionally, the procedure was found to be

more efficient compared to the traditional procedures which often necessitates for a lot of time to

be used for the verification of the various transactions and account balances. The analytical

procedure involved five key steps, and this included, an analysis of the possibility of

misstatement of material, the formation of an independent outcome based on particular account

balances. The other step involved an investigation into the cause of the various financial

discrepancies to typically identify the cause of such deviations in the financial statements. The

variations existing in the reported and estimated amounts were identified. The last step entailed

the ascertainment of the nature of any other auditing procedures (Schreiber, 2017).

The analysis of the audit section in the annual report also shows that there is an audit

committee. The audit committee comprises of five directors. There of the members of the

committee are executive members, and two of them are the non-executive members of the audit

committee (Desai, 2015). The committee is chaired by an independent auditor, and he is not part

of the board. The assessment of the auditors' section also shows that there exists an audit

to check for the presence of dividends which had been approved by the directors of the company

(Graham, Bedard & Dutta, 2018).

Substantive Test of Balances or Analytical Procedures.

The analytical procedure is also one of the audit procedures which had been used by the

auditors of the company. It entailed an assessment of the financial information by evaluating the

relationship between the non-financial and financial data. The key examples of analytical tests

which had been used by the auditors were the regression analysis and trend ratio. Also, the above

audit procedure was used together with the other audit procedures such as the substantive testing.

The primary reason for the integration of the other procedures was to identify the misstatements

in the various account balances (Tricker, 2016). Additionally, the procedure was found to be

more efficient compared to the traditional procedures which often necessitates for a lot of time to

be used for the verification of the various transactions and account balances. The analytical

procedure involved five key steps, and this included, an analysis of the possibility of

misstatement of material, the formation of an independent outcome based on particular account

balances. The other step involved an investigation into the cause of the various financial

discrepancies to typically identify the cause of such deviations in the financial statements. The

variations existing in the reported and estimated amounts were identified. The last step entailed

the ascertainment of the nature of any other auditing procedures (Schreiber, 2017).

The analysis of the audit section in the annual report also shows that there is an audit

committee. The audit committee comprises of five directors. There of the members of the

committee are executive members, and two of them are the non-executive members of the audit

committee (Desai, 2015). The committee is chaired by an independent auditor, and he is not part

of the board. The assessment of the auditors' section also shows that there exists an audit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE 7

committee charter. The charter highlights the purpose of the committee, the composition of the

audit committee, the roles and responsibilities of the audit committee, the resources of the audit

committee and the various meetings of the audit committee.

Structure of Audit Committee

The audit committee is made up of five directors, and two of the members are non-

executive members. The audit committee has appointed by the board of directors of the

company. Also, the members are mainly independent directors, and this is based on the

regulations made by the Capital Market Supervisory Board. One of the members of the audit

committee has a wide knowledge to ensure that the financial statement and budgets are reliable.

Functions and Responsibilities of the Audit Committee

Sultana, Singh & Van der Zahn (2015), argues that there are various roles played by the

audit committee in the company. For example, the committee determines the internal control of

the company by ensuring that they are effective and this is done on a quarterly basis. The

committee also approves the appointment of the chief audit executive of the company through

voting by the members (Cohen, Krishnamoorthy & Wright, 2017). The committee also assists

the board of directors in oversight roles especially in the risk management systems, financial

reporting, and various audit functions.

Another responsibility of the audit committee is that it monitors and evaluates the

audited financial statements provided by the external auditors. Further, the audit committee plays

a fundamental function in corporate governance, and this relates to the control, accountability,

and directions of the company (Abernathy, Beyer, Masli & Stefaniak, 2015). Another

responsibility of the audit committee is that it oversees the process of disclosure of the AZN

Banking and this is to ensure that there is compliance with the international and local laws. Apart

committee charter. The charter highlights the purpose of the committee, the composition of the

audit committee, the roles and responsibilities of the audit committee, the resources of the audit

committee and the various meetings of the audit committee.

Structure of Audit Committee

The audit committee is made up of five directors, and two of the members are non-

executive members. The audit committee has appointed by the board of directors of the

company. Also, the members are mainly independent directors, and this is based on the

regulations made by the Capital Market Supervisory Board. One of the members of the audit

committee has a wide knowledge to ensure that the financial statement and budgets are reliable.

Functions and Responsibilities of the Audit Committee

Sultana, Singh & Van der Zahn (2015), argues that there are various roles played by the

audit committee in the company. For example, the committee determines the internal control of

the company by ensuring that they are effective and this is done on a quarterly basis. The

committee also approves the appointment of the chief audit executive of the company through

voting by the members (Cohen, Krishnamoorthy & Wright, 2017). The committee also assists

the board of directors in oversight roles especially in the risk management systems, financial

reporting, and various audit functions.

Another responsibility of the audit committee is that it monitors and evaluates the

audited financial statements provided by the external auditors. Further, the audit committee plays

a fundamental function in corporate governance, and this relates to the control, accountability,

and directions of the company (Abernathy, Beyer, Masli & Stefaniak, 2015). Another

responsibility of the audit committee is that it oversees the process of disclosure of the AZN

Banking and this is to ensure that there is compliance with the international and local laws. Apart

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE 8

from the roles mentioned above of the audit committee, they also have a responsibility of

approving the budgets and plans proposed by an external auditor. They have to check the

benefits and costs of administering certain audit duties before carrying out an audit procedure of

the company (Khlif & Samaha, 2016).

The analysis of the auditors' sections shows that the auditor’s opinion was unqualified. It,

therefore, meant that the financial statements of the company are a true view of the position if the

company. Also, the unqualified audit opinion indicated that the Generally Accepted Accounting

Principles were conformed to by the financial statements (Bhasin, 2015). The above opinion was

arrived at by the auditors after getting adequate audit evidence on the financial statements due to

the various audit procedures such as the substantive detail testing of such statements provided by

the management.

The directors and management of the company have varied roles in relation to the

financial report. The main role of the management during the financial reporting is to ensure that

all the financial statements are sufficient and also are disclosed according to the reporting

standards. Also, they have to ensure that all the financial statements contain information which is

truthful and does not ruin the reputation of the company (Badolato, Donelson & Ege, 2014).

Additionally, the management checks the disclosures in the financial reports to ensure that the

available information is accurate, relevant and reliable for the users who will use the information

to make certain viable decisions. The directors, on the other hand, keep proper accounting

records which will be used during the disclosure of financial information in the annual reports.

The directors are also expected to have knowledge in accounting which will enable them to

challenge the assumptions and approximations in the financial reports. Further, the accounting

from the roles mentioned above of the audit committee, they also have a responsibility of

approving the budgets and plans proposed by an external auditor. They have to check the

benefits and costs of administering certain audit duties before carrying out an audit procedure of

the company (Khlif & Samaha, 2016).

The analysis of the auditors' sections shows that the auditor’s opinion was unqualified. It,

therefore, meant that the financial statements of the company are a true view of the position if the

company. Also, the unqualified audit opinion indicated that the Generally Accepted Accounting

Principles were conformed to by the financial statements (Bhasin, 2015). The above opinion was

arrived at by the auditors after getting adequate audit evidence on the financial statements due to

the various audit procedures such as the substantive detail testing of such statements provided by

the management.

The directors and management of the company have varied roles in relation to the

financial report. The main role of the management during the financial reporting is to ensure that

all the financial statements are sufficient and also are disclosed according to the reporting

standards. Also, they have to ensure that all the financial statements contain information which is

truthful and does not ruin the reputation of the company (Badolato, Donelson & Ege, 2014).

Additionally, the management checks the disclosures in the financial reports to ensure that the

available information is accurate, relevant and reliable for the users who will use the information

to make certain viable decisions. The directors, on the other hand, keep proper accounting

records which will be used during the disclosure of financial information in the annual reports.

The directors are also expected to have knowledge in accounting which will enable them to

challenge the assumptions and approximations in the financial reports. Further, the accounting

AUDIT, ASSURANCE AND COMPLIANCE 9

knowledge will enable the auditors to comprehend the substance of various transactions in the

financial reports (Kothari, Mizik & Roychowdhury, 2015).

The roles of the auditors, however, differ from those of the directors and management

during the financial reporting. For example, the auditors only carry out an evaluation of the

financial statements of the company, and this is unlike for the directors and management who

ensure that such financial statements are reported according to the accounting standards. The

work of the auditors is to just examine the documents of the firm (Knechel & Salterio, 2016).

During the financial reporting, the auditors' responsibility is to give details in report form as to

whether there was adequate evidence collected which would allow them to give the assurance

which is reasonable to indicate that such financial statements had been fairly prepared. They also

look at whether there was material misstatement in the documents which would justify that the

report prepared contained certain errors. Based on the above discussion, it is concluded that the

roles played by the directors, management and the auditors differ during the preparation of the

financial reports.

The auditors' section also shows that there were subsequent material events after the

reporting period. The subsequent material events identified were primarily two that is recognized

and non-recognized events. The recognized subsequent events are treated by adjusting the

financial statements in the current financial statements of the company, and this was done issuing

them in the statements of financial position (AICPA, 2017). The non-recognized events,

however, on the other hand, are treated by issuing them in the in the next year financial

statements.

Based on the assessment of the auditor’s report, it can be concluded that material

information reported by the auditor is effective. The report can be considered effective because

knowledge will enable the auditors to comprehend the substance of various transactions in the

financial reports (Kothari, Mizik & Roychowdhury, 2015).

The roles of the auditors, however, differ from those of the directors and management

during the financial reporting. For example, the auditors only carry out an evaluation of the

financial statements of the company, and this is unlike for the directors and management who

ensure that such financial statements are reported according to the accounting standards. The

work of the auditors is to just examine the documents of the firm (Knechel & Salterio, 2016).

During the financial reporting, the auditors' responsibility is to give details in report form as to

whether there was adequate evidence collected which would allow them to give the assurance

which is reasonable to indicate that such financial statements had been fairly prepared. They also

look at whether there was material misstatement in the documents which would justify that the

report prepared contained certain errors. Based on the above discussion, it is concluded that the

roles played by the directors, management and the auditors differ during the preparation of the

financial reports.

The auditors' section also shows that there were subsequent material events after the

reporting period. The subsequent material events identified were primarily two that is recognized

and non-recognized events. The recognized subsequent events are treated by adjusting the

financial statements in the current financial statements of the company, and this was done issuing

them in the statements of financial position (AICPA, 2017). The non-recognized events,

however, on the other hand, are treated by issuing them in the in the next year financial

statements.

Based on the assessment of the auditor’s report, it can be concluded that material

information reported by the auditor is effective. The report can be considered effective because

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE 10

the right audit procedures which had been used by the auditor to carry out the audit work. The

audit report can also be said to be effective since it had been carried out by certain competent

auditors of the company (Loughran & McDonald, 2014). Most of the auditing work was done

based on the appointees of the audit committee, and it is expected that any particular auditor of

the firm must have the experience and knowledge to undertake the activity. Additionally, they

have to meet the independent requirements before being allowed to carry out some of the

auditing tasks.

According to Leuz & Wysocki (2016), the other reason which makes the audit report to

be effective is because of the quality control which had been done by the auditors during the

process. All the control systems of the organization had been looked into, and this was done to

identify the strengths and weaknesses of the internal control system of the firm. Lastly, the

information in the audit report was effective due to the quality assurance which was displayed by

the auditors while carrying out their audit work for the company. The factors mentioned above

typically prove that the audit report was effective and hence could be relied on by a variety of

financial users such as the investors, government, employees and the public among others. The

auditing report was found to be effective and hence there no case of missing information in the

report. The level of competency which was applied in the preparation of the audit report resulted

in no missing material information. All the details were fully explained, and hence the

information provided could be relied upon by the different users of the financial information.

Conclusion

In summary, it is evident that the quality and assurance of an audit report is based on a

variety of issues which must be taken into account by auditors. For example, the auditors must

comply with the different accounting standards of auditing. There are also a variety of audit

the right audit procedures which had been used by the auditor to carry out the audit work. The

audit report can also be said to be effective since it had been carried out by certain competent

auditors of the company (Loughran & McDonald, 2014). Most of the auditing work was done

based on the appointees of the audit committee, and it is expected that any particular auditor of

the firm must have the experience and knowledge to undertake the activity. Additionally, they

have to meet the independent requirements before being allowed to carry out some of the

auditing tasks.

According to Leuz & Wysocki (2016), the other reason which makes the audit report to

be effective is because of the quality control which had been done by the auditors during the

process. All the control systems of the organization had been looked into, and this was done to

identify the strengths and weaknesses of the internal control system of the firm. Lastly, the

information in the audit report was effective due to the quality assurance which was displayed by

the auditors while carrying out their audit work for the company. The factors mentioned above

typically prove that the audit report was effective and hence could be relied on by a variety of

financial users such as the investors, government, employees and the public among others. The

auditing report was found to be effective and hence there no case of missing information in the

report. The level of competency which was applied in the preparation of the audit report resulted

in no missing material information. All the details were fully explained, and hence the

information provided could be relied upon by the different users of the financial information.

Conclusion

In summary, it is evident that the quality and assurance of an audit report is based on a

variety of issues which must be taken into account by auditors. For example, the auditors must

comply with the different accounting standards of auditing. There are also a variety of audit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE 11

procedures such as substantive detail testing and the analytical procedures and they must be

strictly adhered to when conducting audit work. In the financial reports, under the auditors

section, the company is said to have an audit committee tasked with various responsibilities such

as oversight roles especially in the risk management systems, financial reporting, and various

audit functions. However the responsibilities of the management and auditors differ on the basis

of planning and control. An audit report should also be effective and this is indicated by various

elements such as competency of the auditors among others.

procedures such as substantive detail testing and the analytical procedures and they must be

strictly adhered to when conducting audit work. In the financial reports, under the auditors

section, the company is said to have an audit committee tasked with various responsibilities such

as oversight roles especially in the risk management systems, financial reporting, and various

audit functions. However the responsibilities of the management and auditors differ on the basis

of planning and control. An audit report should also be effective and this is indicated by various

elements such as competency of the auditors among others.

AUDIT, ASSURANCE AND COMPLIANCE 12

References

Abernathy, J. L., Beyer, B., Masli, A., & Stefaniak, C. M. (2015). How the source of audit

committee accounting expertise influences financial reporting timeliness. Current Issues

in Auditing, 9(1), P1-P9.

AICPA. (2017). Statement on Auditing Standards, Number 126: The Auditor's Consideration of

an Entity's Ability to Continue as a Going Concern (No. 126). John Wiley & Sons.

Badolato, P. G., Donelson, D. C., & Ege, M. (2014). Audit committee financial expertise and

earnings management: The role of status. Journal of Accounting and Economics, 58(2-3),

208-230.

Bhasin, M. L. (2015). Audit committee mechanism to improve corporate governance: Evidence

from a developing country.

Blokdijk, H., Drieenhuizen, F., Simunic, D. A., & Stein, M. T. (2014). Determinants of the Mix

of Audit Procedures: Key Factors that Cause Auditors to Change What They Want.

Accessed on 20th December.

Carcello, J. V., Neal, T. L., Reid, L. C., & Shipman, J. E. (2017). Auditor Independence and Fair

Value Accounting: An Examination of Non-Audit Fees and Goodwill Impairments.

Church, B. K., Jenkins, J. G., & Stanley, J. D. (2018). Auditor Independence in the United

States: Cornerstone of the Profession or Thorn in Our Side?. Accounting Horizons.

Cohen, J., Krishnamoorthy, G., & Wright, A. (2017). Enterprise Risk Management and the

Financial Reporting Process: The Experiences of Audit Committee Members, CFO s, and

External Auditors. Contemporary Accounting Research, 34(2), 1178-1209.

Desai, N. (2015). The Effects of Fraud Risk Factors and Client Characteristics on Audit

Procedures.

References

Abernathy, J. L., Beyer, B., Masli, A., & Stefaniak, C. M. (2015). How the source of audit

committee accounting expertise influences financial reporting timeliness. Current Issues

in Auditing, 9(1), P1-P9.

AICPA. (2017). Statement on Auditing Standards, Number 126: The Auditor's Consideration of

an Entity's Ability to Continue as a Going Concern (No. 126). John Wiley & Sons.

Badolato, P. G., Donelson, D. C., & Ege, M. (2014). Audit committee financial expertise and

earnings management: The role of status. Journal of Accounting and Economics, 58(2-3),

208-230.

Bhasin, M. L. (2015). Audit committee mechanism to improve corporate governance: Evidence

from a developing country.

Blokdijk, H., Drieenhuizen, F., Simunic, D. A., & Stein, M. T. (2014). Determinants of the Mix

of Audit Procedures: Key Factors that Cause Auditors to Change What They Want.

Accessed on 20th December.

Carcello, J. V., Neal, T. L., Reid, L. C., & Shipman, J. E. (2017). Auditor Independence and Fair

Value Accounting: An Examination of Non-Audit Fees and Goodwill Impairments.

Church, B. K., Jenkins, J. G., & Stanley, J. D. (2018). Auditor Independence in the United

States: Cornerstone of the Profession or Thorn in Our Side?. Accounting Horizons.

Cohen, J., Krishnamoorthy, G., & Wright, A. (2017). Enterprise Risk Management and the

Financial Reporting Process: The Experiences of Audit Committee Members, CFO s, and

External Auditors. Contemporary Accounting Research, 34(2), 1178-1209.

Desai, N. (2015). The Effects of Fraud Risk Factors and Client Characteristics on Audit

Procedures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.