HI6026 Audit & Assurance: Enhanced Reporting - ADX Energy Limited

VerifiedAdded on 2023/06/04

|15

|3523

|102

Report

AI Summary

This report provides an analysis of audit and assurance matters related to ADX Energy Limited, an Australian entity involved in oil, gas, and metal exploration. It assesses the auditor's independence, noting their compliance with relevant standards and the absence of non-audit services provided. The report examines auditor remuneration over two years and highlights key audit matters (KAM), specifically cash components. It also points out the absence of an audit committee within the company. The auditor issued an unqualified opinion on the financial statements, emphasizing the directors' responsibility for their preparation and presentation. Furthermore, the report identifies subsequent events and concludes that the auditor effectively disclosed material information relevant to external stakeholders. Desklib provides access to similar reports and study tools for students.

Running Head: Audit, Assurance and Compliance

Auditing and Assurance

Auditing and Assurance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 2

Executive summary

This report presents the audit and assurance related matters related to an Australian entity

named as ADX Energy Limited. The company deals in oil, gases and metal exploration

operations. The report covers discusses about the degree of independence exercised by the

company’s auditor and it has been found that the auditors has independently provided the

audit opinion on company’s financial performance. Apart from providing the audit opinion,

the auditor has not provided any non-audit services to ADX Ltd. The report further provides

insights on the auditor’s remuneration in the last two years and discusses the key audit

matters (KAM) identified by them during the financial year. The auditor has reported cash

component as the KAM. Further, it has been observed that company has no audit committee.

The basic objective of appointment of auditor is to enable him to provide an opinion on

company’s financial statements and auditor has issued unqualified opinion about entity’s

financial statements. However, it is the responsibility of directors to prepare and present the

financial statements. Therefore, auditor cannot be expected to find all the misstatements

contained in the financial statements. Further, the report has identified certain subsequent

events which have occurred after balance sheet but before the approval of financial accounts

of company. After reviewing the audit report, it has been found that the auditor has

effectively disclosed the material information as relevant to the external stakeholders.

Executive summary

This report presents the audit and assurance related matters related to an Australian entity

named as ADX Energy Limited. The company deals in oil, gases and metal exploration

operations. The report covers discusses about the degree of independence exercised by the

company’s auditor and it has been found that the auditors has independently provided the

audit opinion on company’s financial performance. Apart from providing the audit opinion,

the auditor has not provided any non-audit services to ADX Ltd. The report further provides

insights on the auditor’s remuneration in the last two years and discusses the key audit

matters (KAM) identified by them during the financial year. The auditor has reported cash

component as the KAM. Further, it has been observed that company has no audit committee.

The basic objective of appointment of auditor is to enable him to provide an opinion on

company’s financial statements and auditor has issued unqualified opinion about entity’s

financial statements. However, it is the responsibility of directors to prepare and present the

financial statements. Therefore, auditor cannot be expected to find all the misstatements

contained in the financial statements. Further, the report has identified certain subsequent

events which have occurred after balance sheet but before the approval of financial accounts

of company. After reviewing the audit report, it has been found that the auditor has

effectively disclosed the material information as relevant to the external stakeholders.

Audit, Assurance and Compliance 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit, Assurance and Compliance 4

Table of Contents

Executive summary...............................................................................................................................2

Introduction:..........................................................................................................................................5

Auditor’s Independence:........................................................................................................................5

Non-audit services by auditor:...............................................................................................................5

Auditor’s remuneration:........................................................................................................................6

Key audit matters reporting by auditor:.................................................................................................7

Audit Committee:..................................................................................................................................8

Auditor’s Opinion:.................................................................................................................................9

Difference in the responsibility of directors and auditors of the company in respect of annual reports: 9

Director’s Responsibility:................................................................................................................10

Auditor’s Responsibility:.................................................................................................................10

Subsequent Events:............................................................................................................................11

Disclosure of material information by auditor:....................................................................................12

Conclusion:..........................................................................................................................................13

References:..........................................................................................................................................14

Table of Contents

Executive summary...............................................................................................................................2

Introduction:..........................................................................................................................................5

Auditor’s Independence:........................................................................................................................5

Non-audit services by auditor:...............................................................................................................5

Auditor’s remuneration:........................................................................................................................6

Key audit matters reporting by auditor:.................................................................................................7

Audit Committee:..................................................................................................................................8

Auditor’s Opinion:.................................................................................................................................9

Difference in the responsibility of directors and auditors of the company in respect of annual reports: 9

Director’s Responsibility:................................................................................................................10

Auditor’s Responsibility:.................................................................................................................10

Subsequent Events:............................................................................................................................11

Disclosure of material information by auditor:....................................................................................12

Conclusion:..........................................................................................................................................13

References:..........................................................................................................................................14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 5

Introduction:

ADX Energy Limited is an Australian company which is listed on the Australian stock

exchange. ADX Limited is headquartered in Perth, Australia. The company operates within

the energy sector of Australian economy. It has been existence since 1987. It is engaged in

the business of oil as well as gas exploration. The company owns four oil and gas permits in

the North African and European Nation. Moreover, it owns interests in the gold and metal

properties in the Australian nation. This report presents the summary of audit report of the

company formulated by its auditor after reviewing the financial statements of the company.

Auditor’s Independence:

According to the audit report of ADX Energy, the auditors have completely complied with

the independence requirement of Corporations Act 2001. They are independent of the group

and have also followed the ethical requirements of Accounting Professional and Ethical

Standards Board's APES 110 Code of Ethics for Professional Accountants (ADX Energy.

2017). All the relevant standards which are applicable to the audit of financial report in

Australia are followed by the auditors of the company. Moreover, auditors confirmed that the

declaration of independence given to the directors would be in the same terms as it was given

at time of the audit report (ADX Energy. 2017).

As per the director’s report, a copy of auditor’s letter has been attached which confirms the

independence of the auditors. It contains the assurance to the alignment of provisions of

section 370C of the Corporations Act 2001.

Non-audit services by auditor:

Non-audit services are the one provided by the qualified accountant during the period of

conducting an audit and which are not related to the audit or the review of financial

Introduction:

ADX Energy Limited is an Australian company which is listed on the Australian stock

exchange. ADX Limited is headquartered in Perth, Australia. The company operates within

the energy sector of Australian economy. It has been existence since 1987. It is engaged in

the business of oil as well as gas exploration. The company owns four oil and gas permits in

the North African and European Nation. Moreover, it owns interests in the gold and metal

properties in the Australian nation. This report presents the summary of audit report of the

company formulated by its auditor after reviewing the financial statements of the company.

Auditor’s Independence:

According to the audit report of ADX Energy, the auditors have completely complied with

the independence requirement of Corporations Act 2001. They are independent of the group

and have also followed the ethical requirements of Accounting Professional and Ethical

Standards Board's APES 110 Code of Ethics for Professional Accountants (ADX Energy.

2017). All the relevant standards which are applicable to the audit of financial report in

Australia are followed by the auditors of the company. Moreover, auditors confirmed that the

declaration of independence given to the directors would be in the same terms as it was given

at time of the audit report (ADX Energy. 2017).

As per the director’s report, a copy of auditor’s letter has been attached which confirms the

independence of the auditors. It contains the assurance to the alignment of provisions of

section 370C of the Corporations Act 2001.

Non-audit services by auditor:

Non-audit services are the one provided by the qualified accountant during the period of

conducting an audit and which are not related to the audit or the review of financial

Audit, Assurance and Compliance 6

statements (Gray and Manson, 2007). Generally, it involves accounting and financial stuff

but is not connected to assurance. As ADX director’s report, there were no non-audit services

provided by the auditors during the last financial year (ADX Energy. 2017).

Auditor’s remuneration:

Auditor’s remuneration is the amount paid by the company to the professional and qualified

accountants or auditors for rendering their audit services. It is basically a fee paid to them in

exchange of performing audit of the company’s financial statements. The amount is fixed by

the directors and according to their remuneration policies (Millichamp, 2002). ADX has

prepared a full detailed report of its remuneration offered to its key management people and

auditors. It contains the policy of remunerating used by the directors and amount rewarded

along with various share based compensation methods.

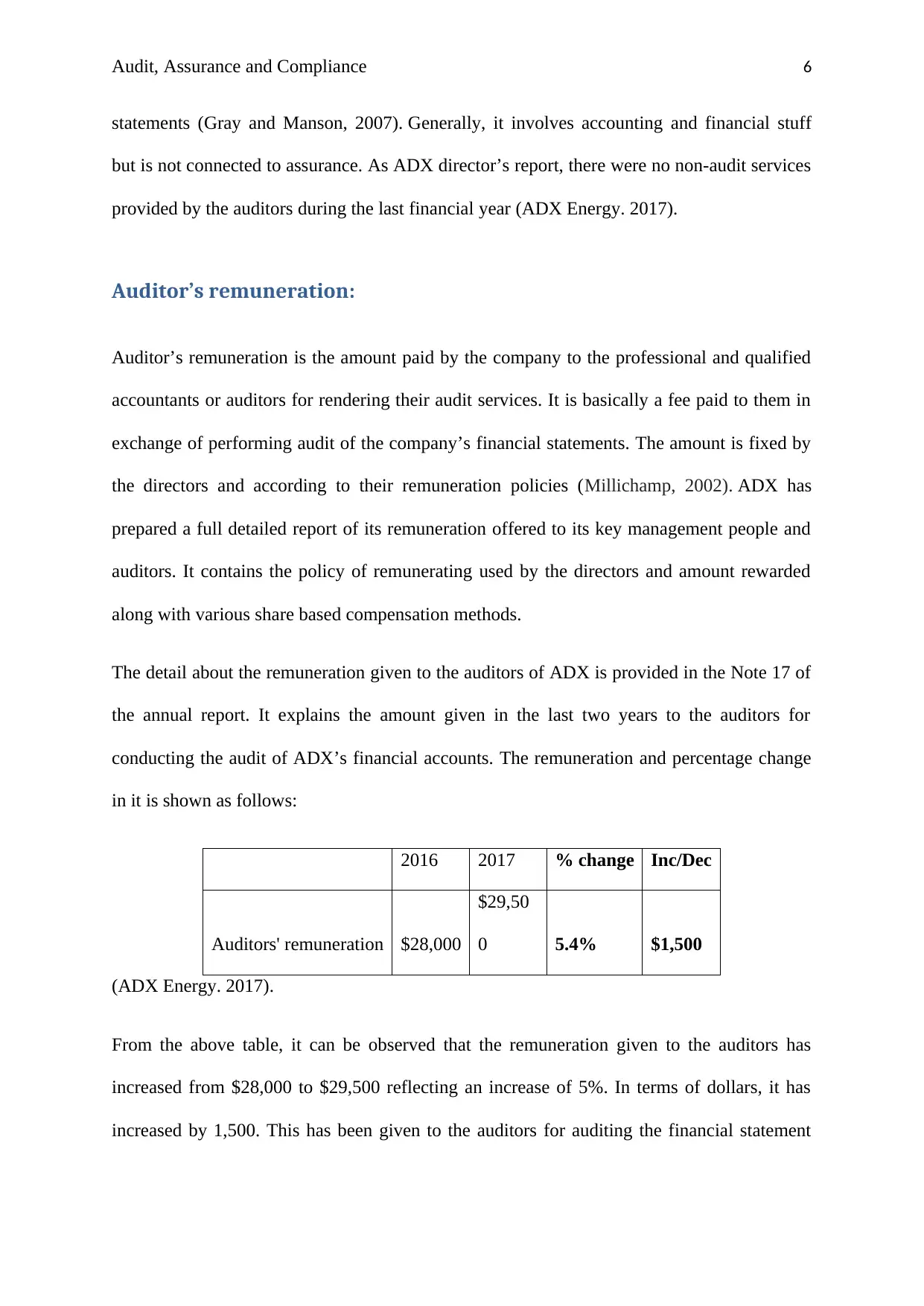

The detail about the remuneration given to the auditors of ADX is provided in the Note 17 of

the annual report. It explains the amount given in the last two years to the auditors for

conducting the audit of ADX’s financial accounts. The remuneration and percentage change

in it is shown as follows:

2016 2017 % change Inc/Dec

Auditors' remuneration $28,000

$29,50

0 5.4% $1,500

(ADX Energy. 2017).

From the above table, it can be observed that the remuneration given to the auditors has

increased from $28,000 to $29,500 reflecting an increase of 5%. In terms of dollars, it has

increased by 1,500. This has been given to the auditors for auditing the financial statement

statements (Gray and Manson, 2007). Generally, it involves accounting and financial stuff

but is not connected to assurance. As ADX director’s report, there were no non-audit services

provided by the auditors during the last financial year (ADX Energy. 2017).

Auditor’s remuneration:

Auditor’s remuneration is the amount paid by the company to the professional and qualified

accountants or auditors for rendering their audit services. It is basically a fee paid to them in

exchange of performing audit of the company’s financial statements. The amount is fixed by

the directors and according to their remuneration policies (Millichamp, 2002). ADX has

prepared a full detailed report of its remuneration offered to its key management people and

auditors. It contains the policy of remunerating used by the directors and amount rewarded

along with various share based compensation methods.

The detail about the remuneration given to the auditors of ADX is provided in the Note 17 of

the annual report. It explains the amount given in the last two years to the auditors for

conducting the audit of ADX’s financial accounts. The remuneration and percentage change

in it is shown as follows:

2016 2017 % change Inc/Dec

Auditors' remuneration $28,000

$29,50

0 5.4% $1,500

(ADX Energy. 2017).

From the above table, it can be observed that the remuneration given to the auditors has

increased from $28,000 to $29,500 reflecting an increase of 5%. In terms of dollars, it has

increased by 1,500. This has been given to the auditors for auditing the financial statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit, Assurance and Compliance 7

and conducting an audit review for ADX Energy. No other services were provided and no

fees have been paid for the same (ADX Energy. 2017).

Key audit matters reporting by auditor:

Key audit matters are those matters which carries high significance in the audit of financial

report. According to the auditors’ professional judgement, these matters are very important to

be considered while conducting the audit of accounts and financials. They are been addressed

in whole detail and assist the auditors in making their opinion (Arens, Elder and Mark,

2012). As per the declaration of ADX’s auditors, they have explained all the key matters and

have not provided a separate opinion on the same. The key audit matters explained are as

follows:

Cash

The amount of cash makes up to 92% of group’s total assets and is considered to be a

essential factor in the operating and exploration activities of the company. Though it is a

liquid asset and cannot be considered at high risk of misstatement but as it holds importance

in context of financial statements, it has to be reviewed properly. Cash is that factor which

can affect the strategy of the group as a whole in respect to the allocation of resources and

completing the audit. It has been reviewed by using following procedures:

The documentation and assessment of processes and controls has been done that are

been used for recording cash transactions.

Agreeing to the cash holdings to the confirmation of third party (ADX Energy. 2017).

Other audit procedure classified as test of controls is used to test the effectiveness of the

controls used by the entity to detect the material misstatements. It also includes analytical

and conducting an audit review for ADX Energy. No other services were provided and no

fees have been paid for the same (ADX Energy. 2017).

Key audit matters reporting by auditor:

Key audit matters are those matters which carries high significance in the audit of financial

report. According to the auditors’ professional judgement, these matters are very important to

be considered while conducting the audit of accounts and financials. They are been addressed

in whole detail and assist the auditors in making their opinion (Arens, Elder and Mark,

2012). As per the declaration of ADX’s auditors, they have explained all the key matters and

have not provided a separate opinion on the same. The key audit matters explained are as

follows:

Cash

The amount of cash makes up to 92% of group’s total assets and is considered to be a

essential factor in the operating and exploration activities of the company. Though it is a

liquid asset and cannot be considered at high risk of misstatement but as it holds importance

in context of financial statements, it has to be reviewed properly. Cash is that factor which

can affect the strategy of the group as a whole in respect to the allocation of resources and

completing the audit. It has been reviewed by using following procedures:

The documentation and assessment of processes and controls has been done that are

been used for recording cash transactions.

Agreeing to the cash holdings to the confirmation of third party (ADX Energy. 2017).

Other audit procedure classified as test of controls is used to test the effectiveness of the

controls used by the entity to detect the material misstatements. It also includes analytical

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 8

procedures which are based on the analysis conducted for the financial statements. The

auditors rely on the ratio analysis of the ADX to make their judgements. In addition, some

substantive procedures are also used which test the completeness, disclosure, existence and

valuation of the assets by providing a conclusive evidence. According to ADX’s auditors,

cash is the most significant item in company’s financial statements which has been properly

reviewed and is separately disclosed in key audit matters. They have collected evidences to

check the existence and validity of the cash balances. The same has been disclosed in their

audit reports (Knapp and Knapp, 2001).

Audit Committee:

According to the ASX CGC principle number four, all the listed companies should have an

audit committee comprising of three members. All of them should be non-executive directors

and majorly the independent ones. In case if the entity does not have such committee, it

needs to disclose procedures employed by it which safeguards the integrity of financial

reporting (ASX (2018). The corporate governance statement of ADX explains that the firm

does not have any audit committee. As the company is of limited size and have limited

operations and financial affairs, having a separate audit committee is not considered suitable

for ADX. However, it has listed down the accountability of management in the statement that

assures the integrity of reporting. It includes review of the statutory financial statements,

monitoring the compliance with accounting procedures and records, review of audit reports

and many others. All such details are properly disclosed and presented in the CG statement of

the company. As the company does not have any committee, there is no audit charter

explained in the report (ADX Energy. 2017).

procedures which are based on the analysis conducted for the financial statements. The

auditors rely on the ratio analysis of the ADX to make their judgements. In addition, some

substantive procedures are also used which test the completeness, disclosure, existence and

valuation of the assets by providing a conclusive evidence. According to ADX’s auditors,

cash is the most significant item in company’s financial statements which has been properly

reviewed and is separately disclosed in key audit matters. They have collected evidences to

check the existence and validity of the cash balances. The same has been disclosed in their

audit reports (Knapp and Knapp, 2001).

Audit Committee:

According to the ASX CGC principle number four, all the listed companies should have an

audit committee comprising of three members. All of them should be non-executive directors

and majorly the independent ones. In case if the entity does not have such committee, it

needs to disclose procedures employed by it which safeguards the integrity of financial

reporting (ASX (2018). The corporate governance statement of ADX explains that the firm

does not have any audit committee. As the company is of limited size and have limited

operations and financial affairs, having a separate audit committee is not considered suitable

for ADX. However, it has listed down the accountability of management in the statement that

assures the integrity of reporting. It includes review of the statutory financial statements,

monitoring the compliance with accounting procedures and records, review of audit reports

and many others. All such details are properly disclosed and presented in the CG statement of

the company. As the company does not have any committee, there is no audit charter

explained in the report (ADX Energy. 2017).

Audit, Assurance and Compliance 9

On a whole, ADX do comply with the requirements of all the ASX CGC principles and

discloses all the information related to the audit and assurance matters in its annual report as

well as in the statement of corporate governance.

Auditor’s Opinion:

Auditor’s opinion is a kind of feedback which is provided by the auditor after carrying out the

audit in relation to financial statements of the entity. The opinion provided by the auditor

does not judge the financial position of the business of the entity nor does it interpret the

financial data of the entity (Tsipouridou & Spathis, 2014). In general there are four types of

opinions provided by the auditors: Unqualified opinion, qualified opinion, adverse opinion

and disclaimer of opinion. In the present case of ADX Limited, the opinion provided by the

auditor of the company is an unqualified opinion. This has been identified from the

examination of annual report of the company for the year ended 2017. The audit opinion

section of the annual report contains a statement by where audit006Frs have declared that the

financial statements of the company are giving true and fair view of financial position of

ADX Group as at 31st December, 2017 as well as the financial performance for the year

ending on 31st December, 2017. The auditors have stated that the financial statements of the

company are prepared and presented in accordance with the Australian Corporations Act,

2001 as well as the Australian accounting standards. The auditors have stated that necessary

and sufficient audit evidences could be generated to form an audit opinion.

However, along with the clean report, the auditors of the company have disclosed few key

audit matters to drive the attention of the users of the annual report. Although these are those

matters where auditor has provided unqualified form of audit opinion but yet these matters

On a whole, ADX do comply with the requirements of all the ASX CGC principles and

discloses all the information related to the audit and assurance matters in its annual report as

well as in the statement of corporate governance.

Auditor’s Opinion:

Auditor’s opinion is a kind of feedback which is provided by the auditor after carrying out the

audit in relation to financial statements of the entity. The opinion provided by the auditor

does not judge the financial position of the business of the entity nor does it interpret the

financial data of the entity (Tsipouridou & Spathis, 2014). In general there are four types of

opinions provided by the auditors: Unqualified opinion, qualified opinion, adverse opinion

and disclaimer of opinion. In the present case of ADX Limited, the opinion provided by the

auditor of the company is an unqualified opinion. This has been identified from the

examination of annual report of the company for the year ended 2017. The audit opinion

section of the annual report contains a statement by where audit006Frs have declared that the

financial statements of the company are giving true and fair view of financial position of

ADX Group as at 31st December, 2017 as well as the financial performance for the year

ending on 31st December, 2017. The auditors have stated that the financial statements of the

company are prepared and presented in accordance with the Australian Corporations Act,

2001 as well as the Australian accounting standards. The auditors have stated that necessary

and sufficient audit evidences could be generated to form an audit opinion.

However, along with the clean report, the auditors of the company have disclosed few key

audit matters to drive the attention of the users of the annual report. Although these are those

matters where auditor has provided unqualified form of audit opinion but yet these matters

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit, Assurance and Compliance 10

requires significant attention of the readers so that they can clearly understand the impact of

such items on the entity’s financial performance.

Difference in the responsibility of directors and auditors of the

company in respect of annual reports:

Director’s Responsibility:

The responsibility of auditors and directors of the company totally differs with respect to the

financial reports of the company. The directors of the ADX Limited have the responsibility of

preparation of company’s financial statements as well as financial reports. They are

responsible for preparation of such financial reports that presents the true and fair view of its

financial position. The directors are responsible to comply with all the Australian accounting

standards and provisions of the Corporations Act, 2001 which are relevant and applicable to

the entity. Also, directors of the company have the pure responsibility to implement a system

of internal control which allows the true and fair view of financial statements by ensuring that

such financial statements are containing any material misstatements due to any kind of error

or fraud by or on the management of the company.

Auditor’s Responsibility:

While undertaking the preparation function of financial reports, it is the core responsibility of

the auditor to assess the ability of entire ADX Group to continue its functions as a going

concern. For this purpose, they are liable to disclose any matter which relates to the going

concern concept. Unless otherwise required, company’s directors are held with the

responsibility of preparing the financial statements on the basis of going concern assumption.

However, auditors are the external independent parties who are not involved in the internal

activities of the company and also they do not participate in the preparatory function of

financial statements as well financial reports. They are merely appointed in the company to

requires significant attention of the readers so that they can clearly understand the impact of

such items on the entity’s financial performance.

Difference in the responsibility of directors and auditors of the

company in respect of annual reports:

Director’s Responsibility:

The responsibility of auditors and directors of the company totally differs with respect to the

financial reports of the company. The directors of the ADX Limited have the responsibility of

preparation of company’s financial statements as well as financial reports. They are

responsible for preparation of such financial reports that presents the true and fair view of its

financial position. The directors are responsible to comply with all the Australian accounting

standards and provisions of the Corporations Act, 2001 which are relevant and applicable to

the entity. Also, directors of the company have the pure responsibility to implement a system

of internal control which allows the true and fair view of financial statements by ensuring that

such financial statements are containing any material misstatements due to any kind of error

or fraud by or on the management of the company.

Auditor’s Responsibility:

While undertaking the preparation function of financial reports, it is the core responsibility of

the auditor to assess the ability of entire ADX Group to continue its functions as a going

concern. For this purpose, they are liable to disclose any matter which relates to the going

concern concept. Unless otherwise required, company’s directors are held with the

responsibility of preparing the financial statements on the basis of going concern assumption.

However, auditors are the external independent parties who are not involved in the internal

activities of the company and also they do not participate in the preparatory function of

financial statements as well financial reports. They are merely appointed in the company to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 11

provide a reasonable assurance about whether the financial statements of the company are

free from any sort material misstatements which could arise due to any frau or errors. The

auditors are responsible to provide an opinion on the truthfulness and fairness of financial

statements. Auditor of ADX Limited can issue any form of audit opinion whether it is

qualified opinion or unqualified opinion or the opinion disclaimer. Along with the audit

opinion auditors are also required to report any key audit matter so as to draw the attention of

users of audit report so that such information could influence their decision making process.

Reasonable assurance is the type of high level assurance which is acceptable by the readers.

However, the reasonable assurance of the auditor does not guarantee that audit engagement

carried by the auditor will always detect each type of errors or frauds since the basic objective

of audit is not to identify any material misstatements arising from any error or fraud in the

audit of financial statements. Even if the audit is carried with due diligence by complying all

the relevant accounting standards, it cannot be expected from the auditor that all the frauds

will be traced by him and all the errors will be identified and corrected by the auditor ((ADX

Energy. 2017).

Subsequent Events:

Yes there were certain events that occurred subsequently after the date on which financial

statements were prepared but before the date of auditor approval the financial statements

(Michels, 2017). These events are:

Issuance of shares:

On 2nd March, 2018: The amounts of these shares were accrued for the month of December

in 2017. Following transactions in respect of shares have been undertaken after the balance

sheet:

provide a reasonable assurance about whether the financial statements of the company are

free from any sort material misstatements which could arise due to any frau or errors. The

auditors are responsible to provide an opinion on the truthfulness and fairness of financial

statements. Auditor of ADX Limited can issue any form of audit opinion whether it is

qualified opinion or unqualified opinion or the opinion disclaimer. Along with the audit

opinion auditors are also required to report any key audit matter so as to draw the attention of

users of audit report so that such information could influence their decision making process.

Reasonable assurance is the type of high level assurance which is acceptable by the readers.

However, the reasonable assurance of the auditor does not guarantee that audit engagement

carried by the auditor will always detect each type of errors or frauds since the basic objective

of audit is not to identify any material misstatements arising from any error or fraud in the

audit of financial statements. Even if the audit is carried with due diligence by complying all

the relevant accounting standards, it cannot be expected from the auditor that all the frauds

will be traced by him and all the errors will be identified and corrected by the auditor ((ADX

Energy. 2017).

Subsequent Events:

Yes there were certain events that occurred subsequently after the date on which financial

statements were prepared but before the date of auditor approval the financial statements

(Michels, 2017). These events are:

Issuance of shares:

On 2nd March, 2018: The amounts of these shares were accrued for the month of December

in 2017. Following transactions in respect of shares have been undertaken after the balance

sheet:

Audit, Assurance and Compliance 12

4330768 shares of the company were issued in pursuance to the director’s share plans

of ADX Limited. This plan was officially signed-off by company shareholders on 31st

May, 2017. These shares were issued to the directors of ADX in return of the amount

waived by them for $ 70100.

1061537 shares were also issued to the company secretaries of ADX Ltd for the

remuneration waived by them for $ 13800.

2562517 shares were issued by the company to its consultants for the advisory

services provided by them against their fees of $ 31841.

On 16th March, 2018:

4380018 shares were issued by the company to its consultants for the advisory

services provided by them against their fees of $ 50000.

On 28th March, 2018:

The company had finalised the agreement with Reabold Resources Plc (Reabold) which was

announced by it on 4th of December, 2017. The agreement was entered into for the investment

of US $ 2 million in the subsidiary of ADX which is named as Danube Petroleum Limited.

The company has adjusted the figures of its share capital value in the exiting financial

statements for the year ended on 31st December, 2017.

There are no other subsequent events taken place in case of ADX Ltd which could

significantly affect the operations or results of the company or the ADX Group as a whole in

the upcoming financial years.

4330768 shares of the company were issued in pursuance to the director’s share plans

of ADX Limited. This plan was officially signed-off by company shareholders on 31st

May, 2017. These shares were issued to the directors of ADX in return of the amount

waived by them for $ 70100.

1061537 shares were also issued to the company secretaries of ADX Ltd for the

remuneration waived by them for $ 13800.

2562517 shares were issued by the company to its consultants for the advisory

services provided by them against their fees of $ 31841.

On 16th March, 2018:

4380018 shares were issued by the company to its consultants for the advisory

services provided by them against their fees of $ 50000.

On 28th March, 2018:

The company had finalised the agreement with Reabold Resources Plc (Reabold) which was

announced by it on 4th of December, 2017. The agreement was entered into for the investment

of US $ 2 million in the subsidiary of ADX which is named as Danube Petroleum Limited.

The company has adjusted the figures of its share capital value in the exiting financial

statements for the year ended on 31st December, 2017.

There are no other subsequent events taken place in case of ADX Ltd which could

significantly affect the operations or results of the company or the ADX Group as a whole in

the upcoming financial years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.