Audit, Assurance and Compliance Case Study: DIPL (Semester 1, 2023)

VerifiedAdded on 2020/03/04

|15

|2820

|183

Case Study

AI Summary

This assignment presents a comprehensive audit case study on Double Ink Printers Ltd. (DIPL), focusing on the application of audit policies and compliances. It begins with an introduction to analytical procedures and their purpose in auditing, followed by the application of these procedures to DIPL's financial data for the year ending June 2015. The study includes a detailed risk assessment of DIPL's business operations, identifying inherent risks such as inventory and financial risks. Furthermore, it explores potential fraud risks related to revenue recognition and CEO incentives, and their impact on audit procedures. The assignment concludes with an analysis of financial ratios and a discussion of how audit strategies should be adapted to address the identified risks and potential misstatements within DIPL's financial statements.

Audit, Assurance and Compliance 1

Audit, Assurance and Compliance

(A case study on Double Ink Printers Ltd)

Audit, Assurance and Compliance

(A case study on Double Ink Printers Ltd)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 2

Table of Contents

Introduction......................................................................................................................................3

Question 1 Applying preliminary analytical procedure for conducting audit.................................4

Question 2: Risk assessment of business operations of DIPL.........................................................9

Question 3:.....................................................................................................................................11

(a) On the basis of background information of DIPL there are two possible risk factors to

generate fraud related to misstatements.....................................................................................11

(b)Direct impact on the audit procedure of company due to risk factors determined in DIPL. 11

Conclusion.....................................................................................................................................13

References:....................................................................................................................................14

Table of Contents

Introduction......................................................................................................................................3

Question 1 Applying preliminary analytical procedure for conducting audit.................................4

Question 2: Risk assessment of business operations of DIPL.........................................................9

Question 3:.....................................................................................................................................11

(a) On the basis of background information of DIPL there are two possible risk factors to

generate fraud related to misstatements.....................................................................................11

(b)Direct impact on the audit procedure of company due to risk factors determined in DIPL. 11

Conclusion.....................................................................................................................................13

References:....................................................................................................................................14

Audit, Assurance and Compliance 3

Introduction

This assignment is undertaken for the purpose of understanding the requirement and compliance

of audit policies for an organization. This whole study is concerned about the audit of Double

Ink Printers Ltd based on the information given in the case study. On the basis of financial

information given in the case study about DIPL an analytical procedure will be applied for

conducting audit. From the results of analytical procedures risk assessment will be completed

and planning will be done for conducting audit for the year ending June 2015 of DIPL. With the

help of audit policies and compliances major risk factors that may causes fraud will be identified.

Introduction

This assignment is undertaken for the purpose of understanding the requirement and compliance

of audit policies for an organization. This whole study is concerned about the audit of Double

Ink Printers Ltd based on the information given in the case study. On the basis of financial

information given in the case study about DIPL an analytical procedure will be applied for

conducting audit. From the results of analytical procedures risk assessment will be completed

and planning will be done for conducting audit for the year ending June 2015 of DIPL. With the

help of audit policies and compliances major risk factors that may causes fraud will be identified.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit, Assurance and Compliance 4

Question 1 Applying preliminary analytical procedure for conducting audit

On the basis of background information and financial report given in the scenario an analytical

procedure is applied for the audit of Double Ink Printers Ltd. DIPL is a printing manufacturing

company which prints advertising materials, books and magazines or journals on the demand of

advertising, publishing and educational institutions. Its whole operation is based on the demand

of customers that how much to produce and how much to supply not on forecasting basis. DIPL

also provide online facility to its readers with the help of DIPL’s website for the purpose of

increasing income.

Definition and purpose of analytical procedures:

Auditing Standard ASA 520 issued by the AUASB (Auditing and Assurance Standards Board)

for Analytical Procedures in perspective of the audit compliance and the strategic planning done

by the auditor. Analytical procedure can be defined as the process of analysis of financial

information and evaluation of historical information based on the financial and non financial

records of a company (Khansalar, et al., 2015). Analytical procedures help the auditor in

assessment of risk and evaluation of financial statement and draw the conclusions at the last

stage of the audit procedure.

The main purpose behind the use of analytical procedures is that data should be interrelated to

each other and relationship between information of two years should exist in future irrespective

of the contrary situation (Knechel and Salterio, 2016). Along with this there are three main

purposes behind the use of analytical procedures are as follows:

1. Analytical review at preliminary level: In this stage analytical reviews are executed to

get an understanding of the environment and operation of DIPL. With the help of this review risk

Question 1 Applying preliminary analytical procedure for conducting audit

On the basis of background information and financial report given in the scenario an analytical

procedure is applied for the audit of Double Ink Printers Ltd. DIPL is a printing manufacturing

company which prints advertising materials, books and magazines or journals on the demand of

advertising, publishing and educational institutions. Its whole operation is based on the demand

of customers that how much to produce and how much to supply not on forecasting basis. DIPL

also provide online facility to its readers with the help of DIPL’s website for the purpose of

increasing income.

Definition and purpose of analytical procedures:

Auditing Standard ASA 520 issued by the AUASB (Auditing and Assurance Standards Board)

for Analytical Procedures in perspective of the audit compliance and the strategic planning done

by the auditor. Analytical procedure can be defined as the process of analysis of financial

information and evaluation of historical information based on the financial and non financial

records of a company (Khansalar, et al., 2015). Analytical procedures help the auditor in

assessment of risk and evaluation of financial statement and draw the conclusions at the last

stage of the audit procedure.

The main purpose behind the use of analytical procedures is that data should be interrelated to

each other and relationship between information of two years should exist in future irrespective

of the contrary situation (Knechel and Salterio, 2016). Along with this there are three main

purposes behind the use of analytical procedures are as follows:

1. Analytical review at preliminary level: In this stage analytical reviews are executed to

get an understanding of the environment and operation of DIPL. With the help of this review risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 5

assessment will be done by auditor in order to find out the timing, process of audit and strategy

for future audit.

2. Analytical procedure at substantial level:

This procedure is useful for the further assessment when audit is conducted at more effective

level in DIPL. This method is useful to reduce the error in financial statement and risk level.

3. Analytical review at final level:

Overall analysis of financial statement is conducted at the closing stage of the audit process to

evaluate whether the information is reliable with the nature and operation of DIPL (Plumlee, et

al., 2014). This process is applied when any indiscretions or dissimilarities are found in the

financial statement.

Planning and strategy for audit for the year ending June 2015 on the basis of analytical

procedures

The main objective behind the application of analytical procedures is to develop the strategy and

planning process for audit. It helps in find out the time for audit and facts, figures required for

risk assessment. To avoid the misappropriation in results of the given financial information

various step are required for effective audit.

Know about the client and identify audit planning at initial level: On the basis of given

information audit is conducted for the Double Ink Printers Ltd. All the information should be

disclosed in front of auditor about the business (Jans, et al., 2014). An engagement will be signed

from the client to develop the understanding between both. The main reason of conducting audit

is new CEO is appointed in the DIPL and set up a new department for internal audit and external

audit.

assessment will be done by auditor in order to find out the timing, process of audit and strategy

for future audit.

2. Analytical procedure at substantial level:

This procedure is useful for the further assessment when audit is conducted at more effective

level in DIPL. This method is useful to reduce the error in financial statement and risk level.

3. Analytical review at final level:

Overall analysis of financial statement is conducted at the closing stage of the audit process to

evaluate whether the information is reliable with the nature and operation of DIPL (Plumlee, et

al., 2014). This process is applied when any indiscretions or dissimilarities are found in the

financial statement.

Planning and strategy for audit for the year ending June 2015 on the basis of analytical

procedures

The main objective behind the application of analytical procedures is to develop the strategy and

planning process for audit. It helps in find out the time for audit and facts, figures required for

risk assessment. To avoid the misappropriation in results of the given financial information

various step are required for effective audit.

Know about the client and identify audit planning at initial level: On the basis of given

information audit is conducted for the Double Ink Printers Ltd. All the information should be

disclosed in front of auditor about the business (Jans, et al., 2014). An engagement will be signed

from the client to develop the understanding between both. The main reason of conducting audit

is new CEO is appointed in the DIPL and set up a new department for internal audit and external

audit.

Audit, Assurance and Compliance 6

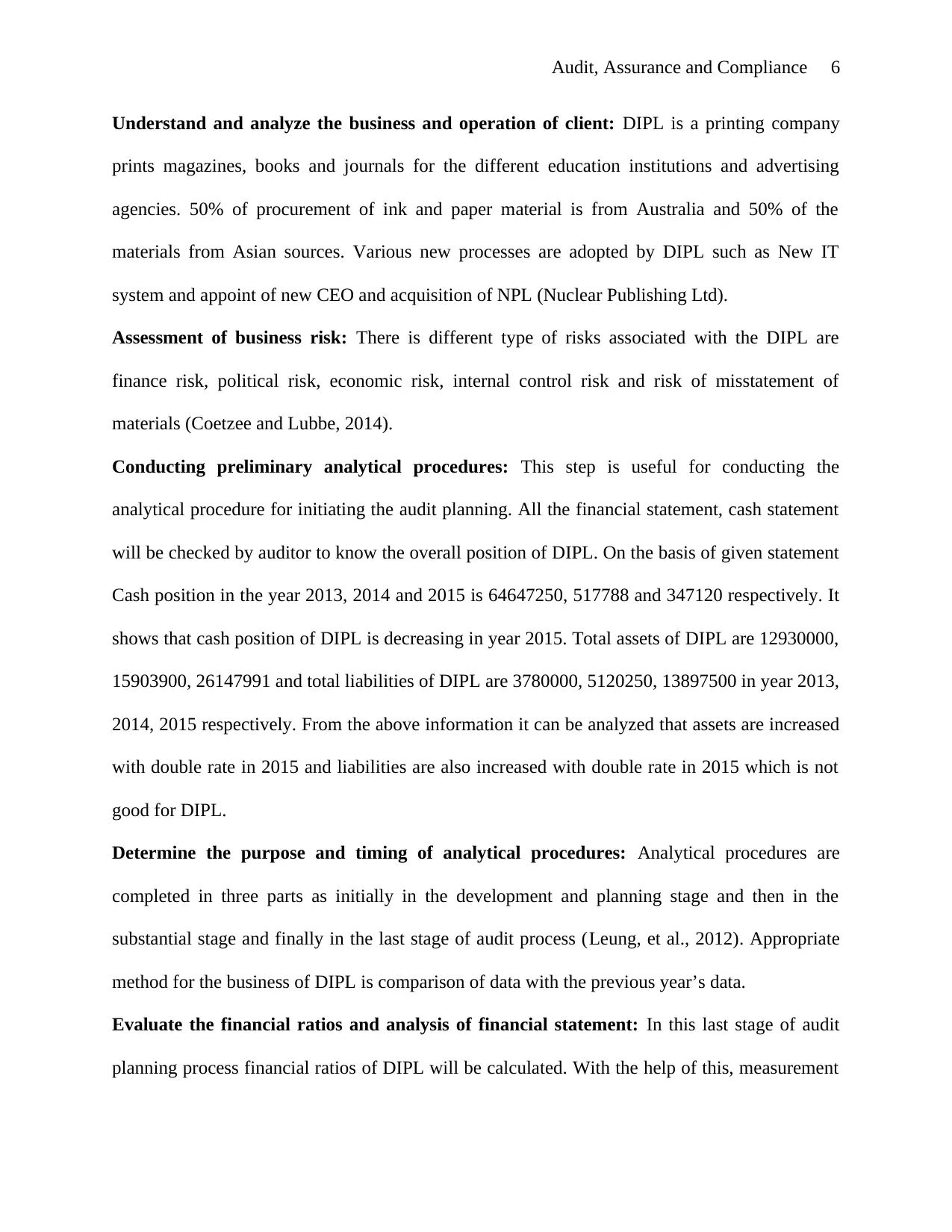

Understand and analyze the business and operation of client: DIPL is a printing company

prints magazines, books and journals for the different education institutions and advertising

agencies. 50% of procurement of ink and paper material is from Australia and 50% of the

materials from Asian sources. Various new processes are adopted by DIPL such as New IT

system and appoint of new CEO and acquisition of NPL (Nuclear Publishing Ltd).

Assessment of business risk: There is different type of risks associated with the DIPL are

finance risk, political risk, economic risk, internal control risk and risk of misstatement of

materials (Coetzee and Lubbe, 2014).

Conducting preliminary analytical procedures: This step is useful for conducting the

analytical procedure for initiating the audit planning. All the financial statement, cash statement

will be checked by auditor to know the overall position of DIPL. On the basis of given statement

Cash position in the year 2013, 2014 and 2015 is 64647250, 517788 and 347120 respectively. It

shows that cash position of DIPL is decreasing in year 2015. Total assets of DIPL are 12930000,

15903900, 26147991 and total liabilities of DIPL are 3780000, 5120250, 13897500 in year 2013,

2014, 2015 respectively. From the above information it can be analyzed that assets are increased

with double rate in 2015 and liabilities are also increased with double rate in 2015 which is not

good for DIPL.

Determine the purpose and timing of analytical procedures: Analytical procedures are

completed in three parts as initially in the development and planning stage and then in the

substantial stage and finally in the last stage of audit process (Leung, et al., 2012). Appropriate

method for the business of DIPL is comparison of data with the previous year’s data.

Evaluate the financial ratios and analysis of financial statement: In this last stage of audit

planning process financial ratios of DIPL will be calculated. With the help of this, measurement

Understand and analyze the business and operation of client: DIPL is a printing company

prints magazines, books and journals for the different education institutions and advertising

agencies. 50% of procurement of ink and paper material is from Australia and 50% of the

materials from Asian sources. Various new processes are adopted by DIPL such as New IT

system and appoint of new CEO and acquisition of NPL (Nuclear Publishing Ltd).

Assessment of business risk: There is different type of risks associated with the DIPL are

finance risk, political risk, economic risk, internal control risk and risk of misstatement of

materials (Coetzee and Lubbe, 2014).

Conducting preliminary analytical procedures: This step is useful for conducting the

analytical procedure for initiating the audit planning. All the financial statement, cash statement

will be checked by auditor to know the overall position of DIPL. On the basis of given statement

Cash position in the year 2013, 2014 and 2015 is 64647250, 517788 and 347120 respectively. It

shows that cash position of DIPL is decreasing in year 2015. Total assets of DIPL are 12930000,

15903900, 26147991 and total liabilities of DIPL are 3780000, 5120250, 13897500 in year 2013,

2014, 2015 respectively. From the above information it can be analyzed that assets are increased

with double rate in 2015 and liabilities are also increased with double rate in 2015 which is not

good for DIPL.

Determine the purpose and timing of analytical procedures: Analytical procedures are

completed in three parts as initially in the development and planning stage and then in the

substantial stage and finally in the last stage of audit process (Leung, et al., 2012). Appropriate

method for the business of DIPL is comparison of data with the previous year’s data.

Evaluate the financial ratios and analysis of financial statement: In this last stage of audit

planning process financial ratios of DIPL will be calculated. With the help of this, measurement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit, Assurance and Compliance 7

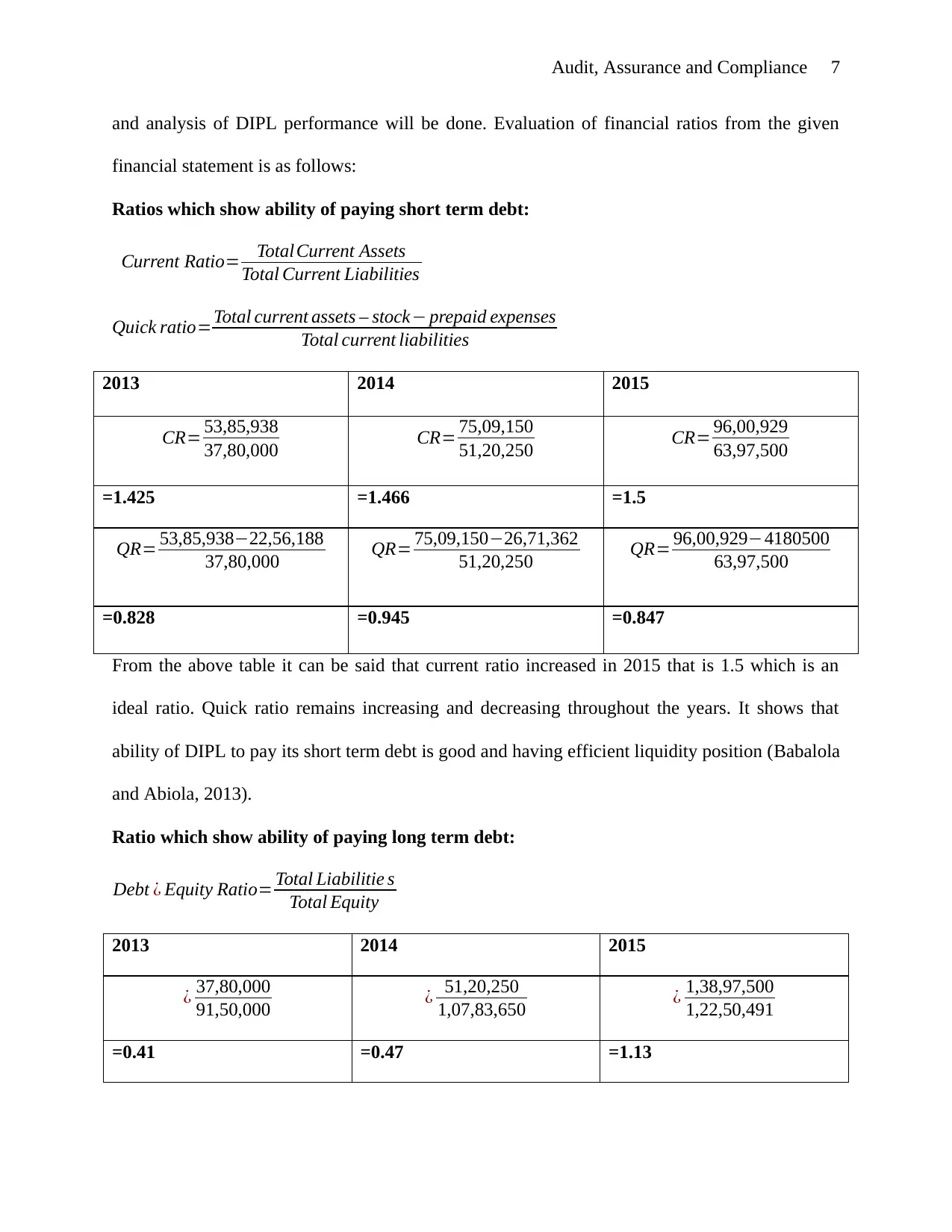

and analysis of DIPL performance will be done. Evaluation of financial ratios from the given

financial statement is as follows:

Ratios which show ability of paying short term debt:

Current Ratio= Total Current Assets

Total Current Liabilities

Quick ratio=Total current assets – stock− prepaid expenses

Total current liabilities

2013 2014 2015

CR= 53,85,938

37,80,000 CR= 75,09,150

51,20,250 CR= 96,00,929

63,97,500

=1.425 =1.466 =1.5

QR= 53,85,938−22,56,188

37,80,000 QR= 75,09,150−26,71,362

51,20,250 QR= 96,00,929−4180500

63,97,500

=0.828 =0.945 =0.847

From the above table it can be said that current ratio increased in 2015 that is 1.5 which is an

ideal ratio. Quick ratio remains increasing and decreasing throughout the years. It shows that

ability of DIPL to pay its short term debt is good and having efficient liquidity position (Babalola

and Abiola, 2013).

Ratio which show ability of paying long term debt:

Debt ¿ Equity Ratio= Total Liabilitie s

Total Equity

2013 2014 2015

¿ 37,80,000

91,50,000 ¿ 51,20,250

1,07,83,650 ¿ 1,38,97,500

1,22,50,491

=0.41 =0.47 =1.13

and analysis of DIPL performance will be done. Evaluation of financial ratios from the given

financial statement is as follows:

Ratios which show ability of paying short term debt:

Current Ratio= Total Current Assets

Total Current Liabilities

Quick ratio=Total current assets – stock− prepaid expenses

Total current liabilities

2013 2014 2015

CR= 53,85,938

37,80,000 CR= 75,09,150

51,20,250 CR= 96,00,929

63,97,500

=1.425 =1.466 =1.5

QR= 53,85,938−22,56,188

37,80,000 QR= 75,09,150−26,71,362

51,20,250 QR= 96,00,929−4180500

63,97,500

=0.828 =0.945 =0.847

From the above table it can be said that current ratio increased in 2015 that is 1.5 which is an

ideal ratio. Quick ratio remains increasing and decreasing throughout the years. It shows that

ability of DIPL to pay its short term debt is good and having efficient liquidity position (Babalola

and Abiola, 2013).

Ratio which show ability of paying long term debt:

Debt ¿ Equity Ratio= Total Liabilitie s

Total Equity

2013 2014 2015

¿ 37,80,000

91,50,000 ¿ 51,20,250

1,07,83,650 ¿ 1,38,97,500

1,22,50,491

=0.41 =0.47 =1.13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 8

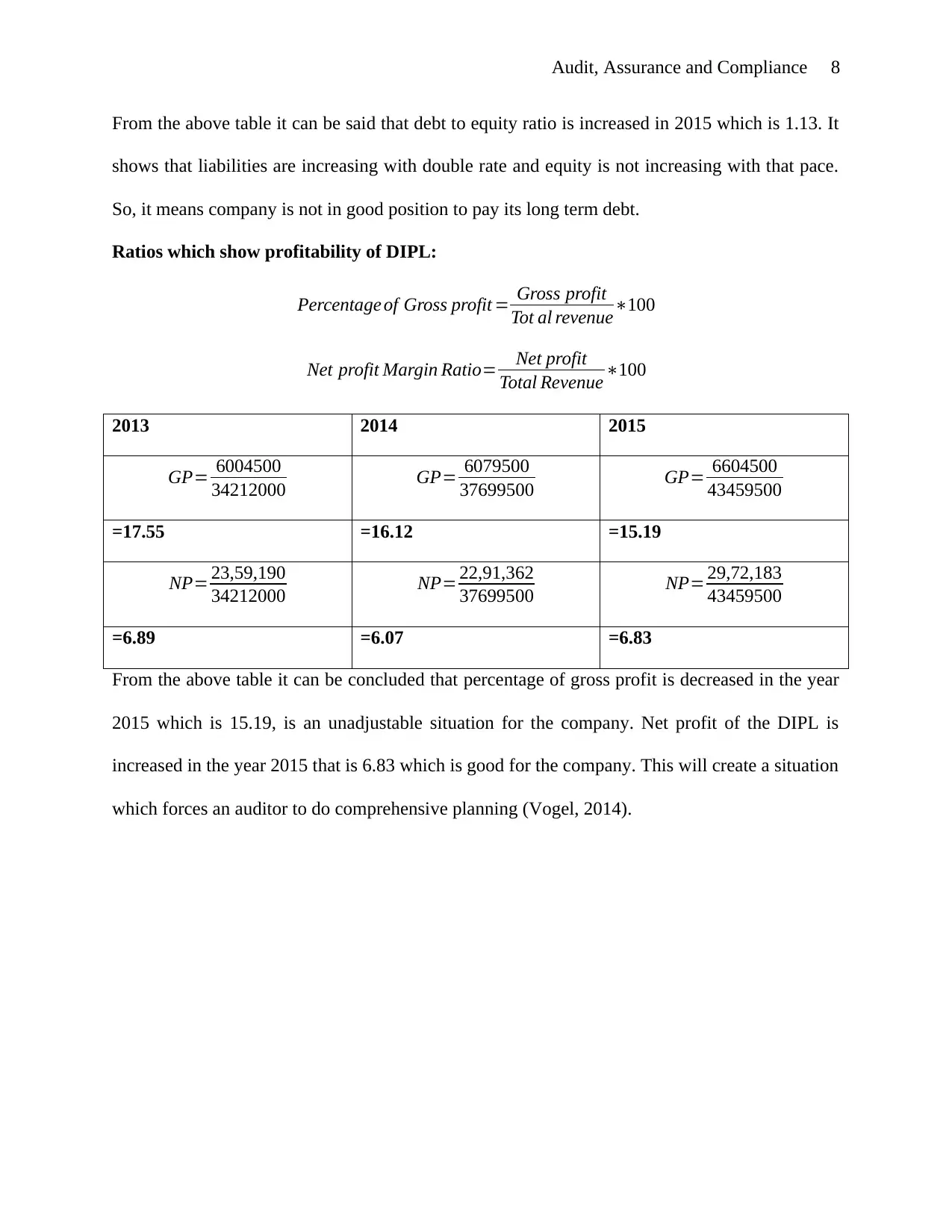

From the above table it can be said that debt to equity ratio is increased in 2015 which is 1.13. It

shows that liabilities are increasing with double rate and equity is not increasing with that pace.

So, it means company is not in good position to pay its long term debt.

Ratios which show profitability of DIPL:

Percentage of Gross profit = Gross profit

Tot al revenue∗100

Net profit Margin Ratio= Net profit

Total Revenue ∗100

2013 2014 2015

GP= 6004500

34212000 GP= 6079500

37699500 GP= 6604500

43459500

=17.55 =16.12 =15.19

NP= 23,59,190

34212000 NP= 22,91,362

37699500 NP= 29,72,183

43459500

=6.89 =6.07 =6.83

From the above table it can be concluded that percentage of gross profit is decreased in the year

2015 which is 15.19, is an unadjustable situation for the company. Net profit of the DIPL is

increased in the year 2015 that is 6.83 which is good for the company. This will create a situation

which forces an auditor to do comprehensive planning (Vogel, 2014).

From the above table it can be said that debt to equity ratio is increased in 2015 which is 1.13. It

shows that liabilities are increasing with double rate and equity is not increasing with that pace.

So, it means company is not in good position to pay its long term debt.

Ratios which show profitability of DIPL:

Percentage of Gross profit = Gross profit

Tot al revenue∗100

Net profit Margin Ratio= Net profit

Total Revenue ∗100

2013 2014 2015

GP= 6004500

34212000 GP= 6079500

37699500 GP= 6604500

43459500

=17.55 =16.12 =15.19

NP= 23,59,190

34212000 NP= 22,91,362

37699500 NP= 29,72,183

43459500

=6.89 =6.07 =6.83

From the above table it can be concluded that percentage of gross profit is decreased in the year

2015 which is 15.19, is an unadjustable situation for the company. Net profit of the DIPL is

increased in the year 2015 that is 6.83 which is good for the company. This will create a situation

which forces an auditor to do comprehensive planning (Vogel, 2014).

Audit, Assurance and Compliance 9

Question 2: Risk assessment of business operations of DIPL

Inherent risk: Inherent risk can be defined as the chances of wrong or deceptive information in

financial statements due to the lack of internal control of management and can be due to various

external factors (Hopkin, 2017). Some examples of inherent risk are such as use of large data

approximation and use of those financial instruments which cannot generate clear picture of

business. Inherent risk is the important part of audit risk which cannot be simply avoided from

the financial statement.

In the DIPL there are two type of inherent risk exist such as inventory risk or financial risk.

Financial risk is the risk because it covers all type risk such as interest rate risk, debt risk etc. In

the financial report it can generate the occurrence of material misstatement as to show the better

finance position of the company (PCAOB, 2017). While calculating the liquidity ratios of the

company it can analyzed that current ratio is 1.5 which shows company have enough fund to pay

its short term debt. But company does not have enough funds to pay its long term debt because

its liabilities are increasing with double rate and equity is not increasing with that pace. So,

company cannot generate enough funds to pay its long term debt and it may show false

information related to equity balance or can manipulate the management to create high liquidity

position in the market and to show the debt to equity ratio of less than 1.

One more risk is arising from the nature of DIPL’s business operations is the inventory risk.

Inventory risk is the major inherent risk for a business operation if its inventory becomes

outdated (PCAOB, 2017). DIPL generally does 50% of procurement of ink and paper material is

from Australia and 50% of the materials from Asian sources. From the given information it can

be analyzed that DIPL valued its raw material at average cost and to cover from the loss of

reduction in value of old inventory an allowance for outdated stock shown in last year account.

Question 2: Risk assessment of business operations of DIPL

Inherent risk: Inherent risk can be defined as the chances of wrong or deceptive information in

financial statements due to the lack of internal control of management and can be due to various

external factors (Hopkin, 2017). Some examples of inherent risk are such as use of large data

approximation and use of those financial instruments which cannot generate clear picture of

business. Inherent risk is the important part of audit risk which cannot be simply avoided from

the financial statement.

In the DIPL there are two type of inherent risk exist such as inventory risk or financial risk.

Financial risk is the risk because it covers all type risk such as interest rate risk, debt risk etc. In

the financial report it can generate the occurrence of material misstatement as to show the better

finance position of the company (PCAOB, 2017). While calculating the liquidity ratios of the

company it can analyzed that current ratio is 1.5 which shows company have enough fund to pay

its short term debt. But company does not have enough funds to pay its long term debt because

its liabilities are increasing with double rate and equity is not increasing with that pace. So,

company cannot generate enough funds to pay its long term debt and it may show false

information related to equity balance or can manipulate the management to create high liquidity

position in the market and to show the debt to equity ratio of less than 1.

One more risk is arising from the nature of DIPL’s business operations is the inventory risk.

Inventory risk is the major inherent risk for a business operation if its inventory becomes

outdated (PCAOB, 2017). DIPL generally does 50% of procurement of ink and paper material is

from Australia and 50% of the materials from Asian sources. From the given information it can

be analyzed that DIPL valued its raw material at average cost and to cover from the loss of

reduction in value of old inventory an allowance for outdated stock shown in last year account.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit, Assurance and Compliance 10

Inventory of DIPL is increased with twice rate and allowance for obsolete inventory is also

increased but written back. So, company can record higher amount of stock to show better

position in the market and can increase the amount of allowance for outdated inventory can be a

part of material misstatement.

Inventory of DIPL is increased with twice rate and allowance for obsolete inventory is also

increased but written back. So, company can record higher amount of stock to show better

position in the market and can increase the amount of allowance for outdated inventory can be a

part of material misstatement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit, Assurance and Compliance 11

Question 3:

(a) On the basis of background information of DIPL there are two possible risk factors to

generate fraud related to misstatements

On the basis of information given in the case study it is identified that for the purpose of

uploading the e-book on the website of DIPL an annual fee is charged by DIPL from its

publishers as a storage fee. This fee payable by the publishers in advance for 12 months but

revenue is recognized and recorded in the books on the date of first book download when fees

are invoiced. Another risk factor identified is that new CEO (chief executive officer) has been

appointed from January 2015. It is remuneration policy of DIPL is that CEO will get

performance bonus on the basis of achieving 10% growth in revenue and net profit after tax.

CEO also recommended for appointing new audit team for DIPL business which directly shows

that any fraudulent or misstatements can occur to get higher bonus

(b)Direct impact on the audit procedure of company due to risk factors determined in

DIPL

Both the fraudulent activities and risk factors identified above will have direct impact on the

audit procedure for business operation of DIPL. To avoid the misappropriation in the results of

given financial information various strategy have to be followed by auditor (Ruhnke and

Schmidt, 2014). Evaluation of financial ratios and analysis of financial statement is required and

proper facts and figures will be analyzed. From the given financial information it can be

analyzed that revenue in 2015 that is 4,34,59,500 increased with double rate as compared to the

increased in 2014. Net profit after deducting taxes also increased with higher rate in 2015 while

it is decreased in 2014. This all facts show that any wrongful information or misstatements

occurred in DIPL business activities to get higher amount of bonus by the CEO. Recording of E-

Question 3:

(a) On the basis of background information of DIPL there are two possible risk factors to

generate fraud related to misstatements

On the basis of information given in the case study it is identified that for the purpose of

uploading the e-book on the website of DIPL an annual fee is charged by DIPL from its

publishers as a storage fee. This fee payable by the publishers in advance for 12 months but

revenue is recognized and recorded in the books on the date of first book download when fees

are invoiced. Another risk factor identified is that new CEO (chief executive officer) has been

appointed from January 2015. It is remuneration policy of DIPL is that CEO will get

performance bonus on the basis of achieving 10% growth in revenue and net profit after tax.

CEO also recommended for appointing new audit team for DIPL business which directly shows

that any fraudulent or misstatements can occur to get higher bonus

(b)Direct impact on the audit procedure of company due to risk factors determined in

DIPL

Both the fraudulent activities and risk factors identified above will have direct impact on the

audit procedure for business operation of DIPL. To avoid the misappropriation in the results of

given financial information various strategy have to be followed by auditor (Ruhnke and

Schmidt, 2014). Evaluation of financial ratios and analysis of financial statement is required and

proper facts and figures will be analyzed. From the given financial information it can be

analyzed that revenue in 2015 that is 4,34,59,500 increased with double rate as compared to the

increased in 2014. Net profit after deducting taxes also increased with higher rate in 2015 while

it is decreased in 2014. This all facts show that any wrongful information or misstatements

occurred in DIPL business activities to get higher amount of bonus by the CEO. Recording of E-

Audit, Assurance and Compliance 12

book storage fees in the month of fees are invoiced not at the time when fees are taken by DIPL

in advance for 12 months. This recording of storage fees also increased with higher rate in 2015.

This all wrongful information required to do proper planning for audit of business activities of

DIPL (Cohen, et al., 2017).

book storage fees in the month of fees are invoiced not at the time when fees are taken by DIPL

in advance for 12 months. This recording of storage fees also increased with higher rate in 2015.

This all wrongful information required to do proper planning for audit of business activities of

DIPL (Cohen, et al., 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.