Audit, Assurance and Compliance Report

VerifiedAdded on 2020/02/24

|20

|2902

|437

Report

AI Summary

This report delves into the audit, assurance, and compliance processes for Double Ink Printers Limited (DIPL). It includes a thorough analysis of financial ratios such as profitability, liquidity, efficiency, and solvency over three years. The report identifies key risk factors affecting financial reporting and discusses the implications of these risks on audit planning. It emphasizes the importance of analytical procedures in evaluating the financial health of DIPL and highlights the need for proper controls to mitigate risks associated with financial misstatements.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Question 1........................................................................................................................................2

Part A...............................................................................................................................................2

Explanation of analytical procedures that is important for preparation of financial reports of

DIPL................................................................................................................................................2

Profitability Ratio............................................................................................................................2

Gross Profit Ratio........................................................................................................................2

Net Profit ratio.............................................................................................................................4

Return on assets...........................................................................................................................5

Return on Equity..........................................................................................................................6

Liquidity ratio..................................................................................................................................7

Current ratio.................................................................................................................................7

Quick ratio...................................................................................................................................8

Efficiency ratio................................................................................................................................9

Inventory turnover ratio...............................................................................................................9

Solvency Ratio...............................................................................................................................11

Debt to Equity Ratio..................................................................................................................11

Part B.............................................................................................................................................12

Impact of analytical review on audit planning for the year ending 30th of June 2015...................12

Question 2......................................................................................................................................13

Table of Contents

Question 1........................................................................................................................................2

Part A...............................................................................................................................................2

Explanation of analytical procedures that is important for preparation of financial reports of

DIPL................................................................................................................................................2

Profitability Ratio............................................................................................................................2

Gross Profit Ratio........................................................................................................................2

Net Profit ratio.............................................................................................................................4

Return on assets...........................................................................................................................5

Return on Equity..........................................................................................................................6

Liquidity ratio..................................................................................................................................7

Current ratio.................................................................................................................................7

Quick ratio...................................................................................................................................8

Efficiency ratio................................................................................................................................9

Inventory turnover ratio...............................................................................................................9

Solvency Ratio...............................................................................................................................11

Debt to Equity Ratio..................................................................................................................11

Part B.............................................................................................................................................12

Impact of analytical review on audit planning for the year ending 30th of June 2015...................12

Question 2......................................................................................................................................13

3AUDIT, ASSURANCE AND COMPLIANCE

Classification of inherent risk factors based on nature of business operations of DIPL...............13

Question 3......................................................................................................................................14

Part A.............................................................................................................................................14

Identification of key risk factors that relates to misstatement of financial reporting....................14

Part B.............................................................................................................................................15

Effect of risk factors on audit conduct...........................................................................................15

Reference List................................................................................................................................16

Classification of inherent risk factors based on nature of business operations of DIPL...............13

Question 3......................................................................................................................................14

Part A.............................................................................................................................................14

Identification of key risk factors that relates to misstatement of financial reporting....................14

Part B.............................................................................................................................................15

Effect of risk factors on audit conduct...........................................................................................15

Reference List................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDIT, ASSURANCE AND COMPLIANCE

Question 1

Part A

Explanation of analytical procedures that is important for preparation of financial reports

of DIPL

Ratio analysis is the most widespread tools used by companies for analyzing a business

financial standing (William, Glover and Prawitt 2016). This analysis is very easy to understand

and compute that makes it so famous than any other accounting measurement tools. It is used by

large and small companies for comparing their financial information. This ratio does not take

into account the company size or the industry. This analysis is just a raw computation of

financial position as well as performance of any business enterprise irrespective of nature and

size of operations. In similar ways, this study uses ratio analysis measurement tool for predicting

the financial performance of Double Ink Printers Limited. The study had used four broad

categories of ratio analysis such as profitability ratio, liquidity ratio, efficiency ratio and

solvency ratio (Simnett, Carson and Vanstraelen 2016).

Profitability Ratio

Gross Profit Ratio

Double Ink Printers Limited

2013 2014 2015

Gross Profit 17.55085935 16.126208 15.1969075

Question 1

Part A

Explanation of analytical procedures that is important for preparation of financial reports

of DIPL

Ratio analysis is the most widespread tools used by companies for analyzing a business

financial standing (William, Glover and Prawitt 2016). This analysis is very easy to understand

and compute that makes it so famous than any other accounting measurement tools. It is used by

large and small companies for comparing their financial information. This ratio does not take

into account the company size or the industry. This analysis is just a raw computation of

financial position as well as performance of any business enterprise irrespective of nature and

size of operations. In similar ways, this study uses ratio analysis measurement tool for predicting

the financial performance of Double Ink Printers Limited. The study had used four broad

categories of ratio analysis such as profitability ratio, liquidity ratio, efficiency ratio and

solvency ratio (Simnett, Carson and Vanstraelen 2016).

Profitability Ratio

Gross Profit Ratio

Double Ink Printers Limited

2013 2014 2015

Gross Profit 17.55085935 16.126208 15.1969075

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDIT, ASSURANCE AND COMPLIANCE

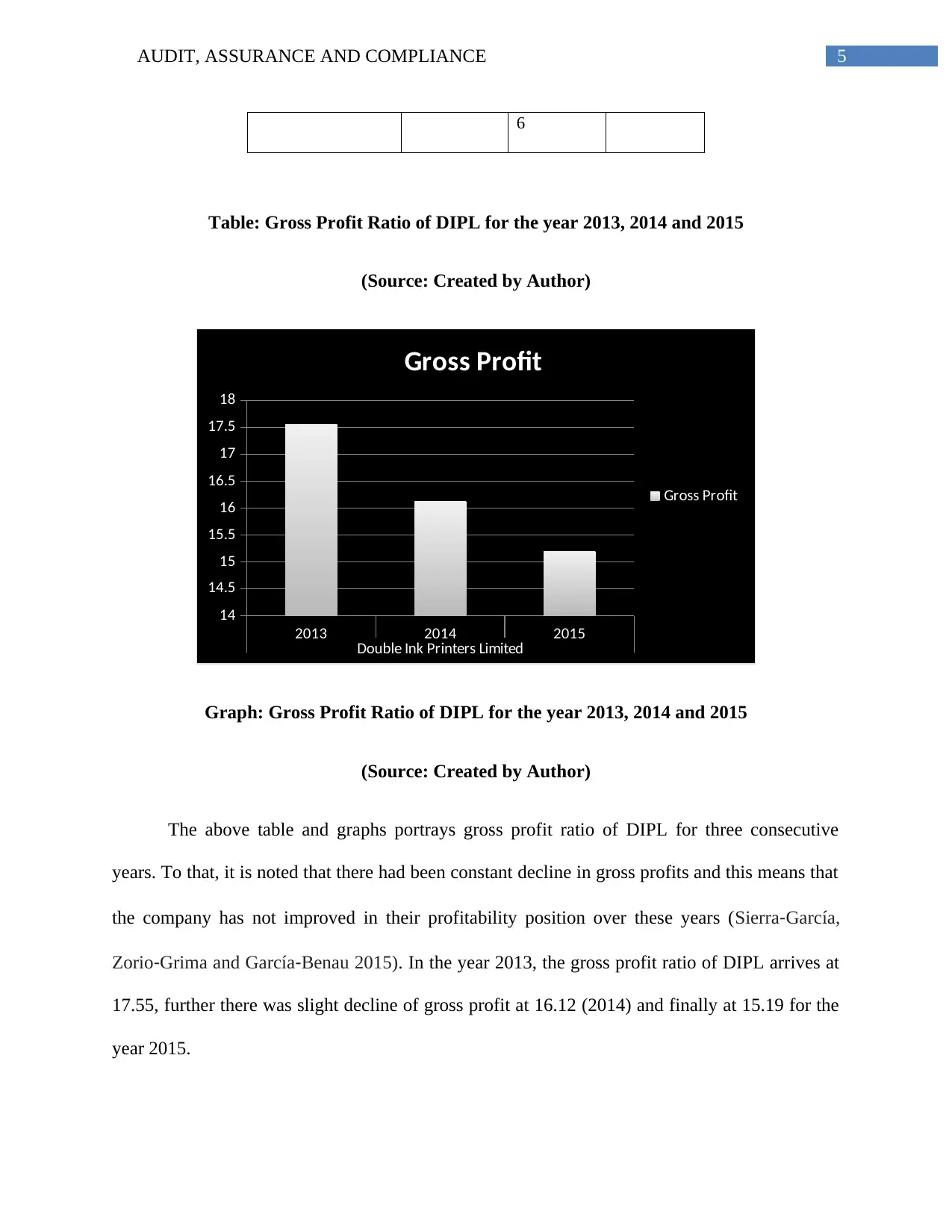

6

Table: Gross Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

14

14.5

15

15.5

16

16.5

17

17.5

18

Gross Profit

Gross Profit

Graph: Gross Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays gross profit ratio of DIPL for three consecutive

years. To that, it is noted that there had been constant decline in gross profits and this means that

the company has not improved in their profitability position over these years (Sierra‐García,

Zorio‐Grima and García‐Benau 2015). In the year 2013, the gross profit ratio of DIPL arrives at

17.55, further there was slight decline of gross profit at 16.12 (2014) and finally at 15.19 for the

year 2015.

6

Table: Gross Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

14

14.5

15

15.5

16

16.5

17

17.5

18

Gross Profit

Gross Profit

Graph: Gross Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays gross profit ratio of DIPL for three consecutive

years. To that, it is noted that there had been constant decline in gross profits and this means that

the company has not improved in their profitability position over these years (Sierra‐García,

Zorio‐Grima and García‐Benau 2015). In the year 2013, the gross profit ratio of DIPL arrives at

17.55, further there was slight decline of gross profit at 16.12 (2014) and finally at 15.19 for the

year 2015.

6AUDIT, ASSURANCE AND COMPLIANCE

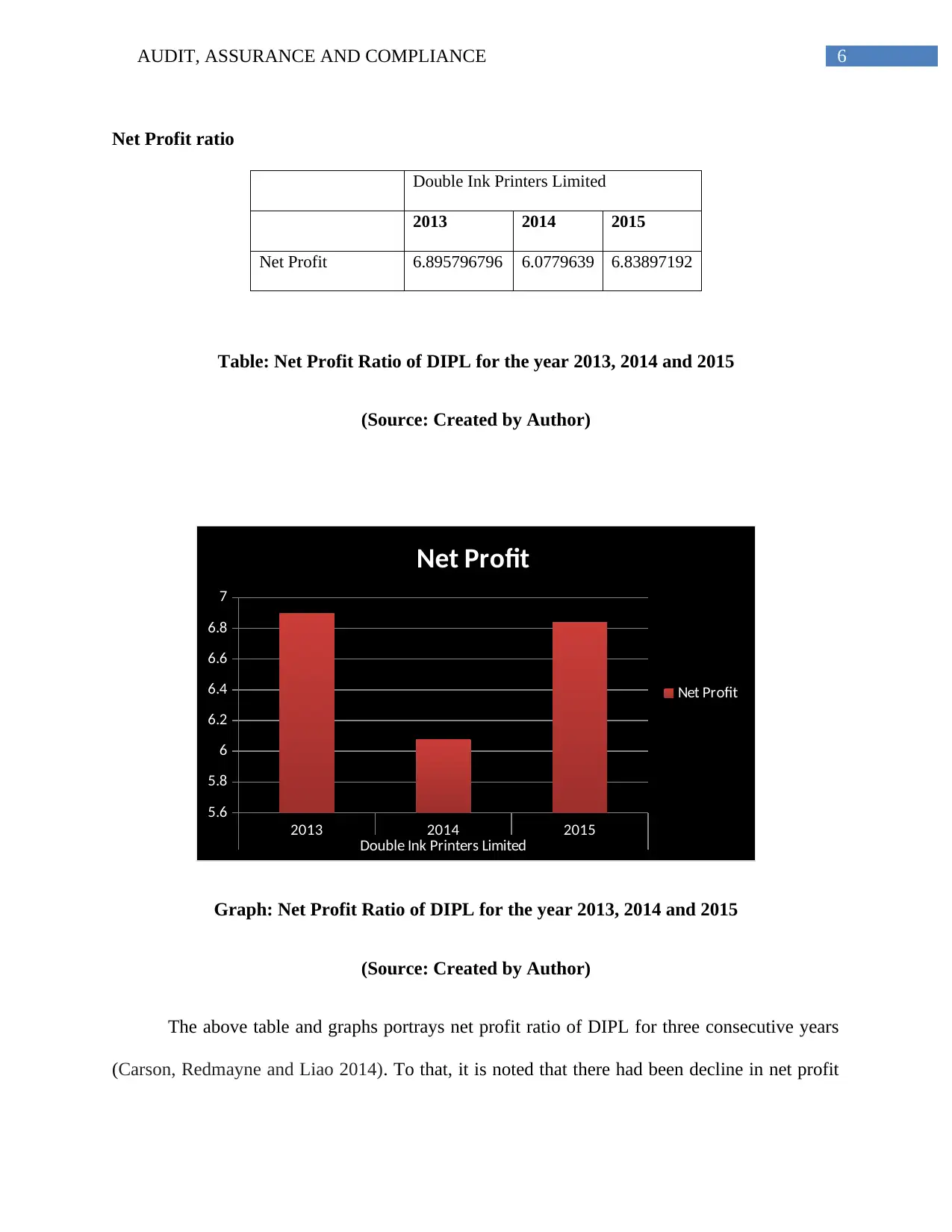

Net Profit ratio

Double Ink Printers Limited

2013 2014 2015

Net Profit 6.895796796 6.0779639 6.83897192

Table: Net Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

5.6

5.8

6

6.2

6.4

6.6

6.8

7

Net Profit

Net Profit

Graph: Net Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays net profit ratio of DIPL for three consecutive years

(Carson, Redmayne and Liao 2014). To that, it is noted that there had been decline in net profit

Net Profit ratio

Double Ink Printers Limited

2013 2014 2015

Net Profit 6.895796796 6.0779639 6.83897192

Table: Net Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

5.6

5.8

6

6.2

6.4

6.6

6.8

7

Net Profit

Net Profit

Graph: Net Profit Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays net profit ratio of DIPL for three consecutive years

(Carson, Redmayne and Liao 2014). To that, it is noted that there had been decline in net profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDIT, ASSURANCE AND COMPLIANCE

from 2013 to 2014 and then there was increase in net profit for the year 2015. In the year 2013,

the net profit ratio of DIPL arrives at 6.89, further there was slight decline of net profit at 6.077

(2014) and finally increase at 6.83 for the year 2015.

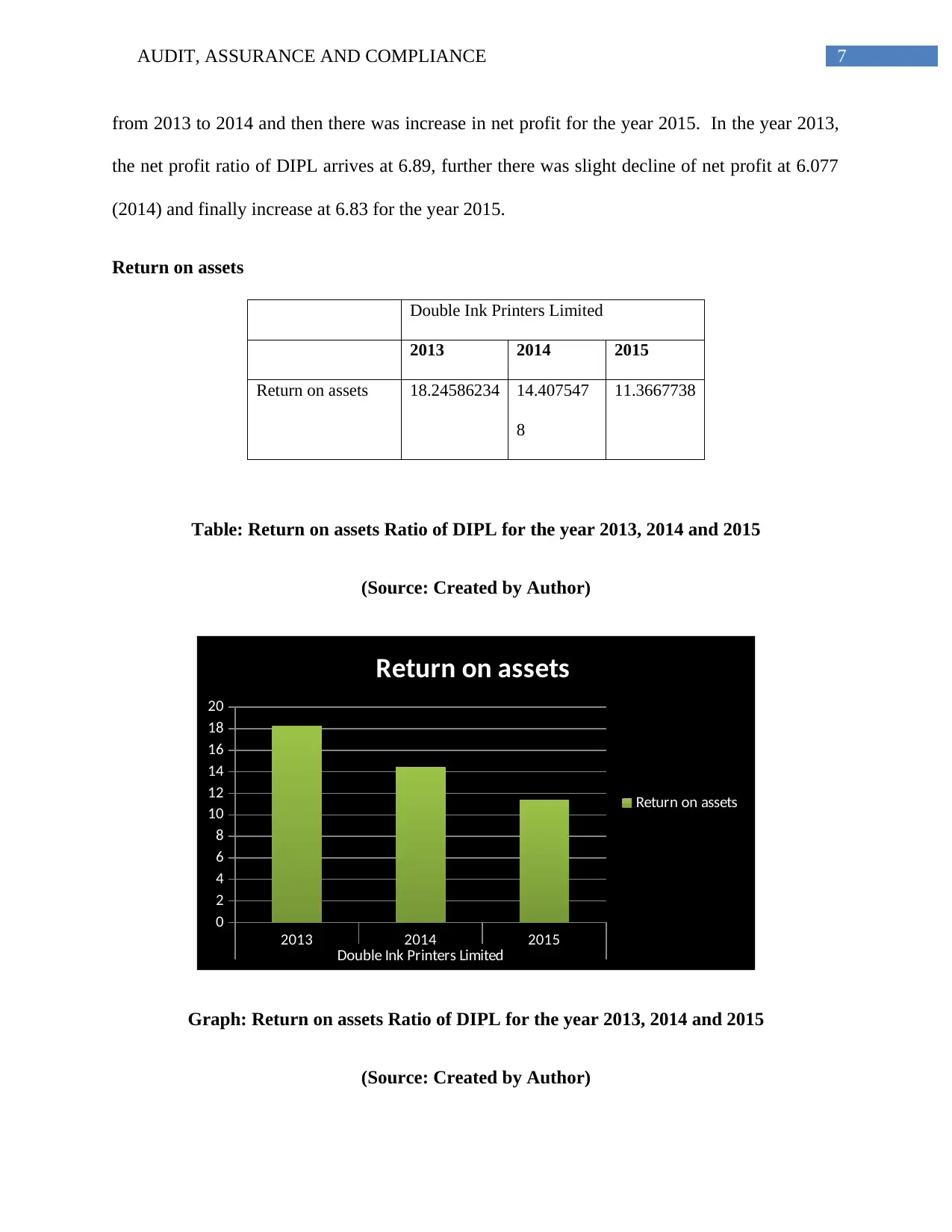

Return on assets

Double Ink Printers Limited

2013 2014 2015

Return on assets 18.24586234 14.407547

8

11.3667738

Table: Return on assets Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0

2

4

6

8

10

12

14

16

18

20

Return on assets

Return on assets

Graph: Return on assets Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

from 2013 to 2014 and then there was increase in net profit for the year 2015. In the year 2013,

the net profit ratio of DIPL arrives at 6.89, further there was slight decline of net profit at 6.077

(2014) and finally increase at 6.83 for the year 2015.

Return on assets

Double Ink Printers Limited

2013 2014 2015

Return on assets 18.24586234 14.407547

8

11.3667738

Table: Return on assets Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0

2

4

6

8

10

12

14

16

18

20

Return on assets

Return on assets

Graph: Return on assets Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDIT, ASSURANCE AND COMPLIANCE

The above table and graphs portrays return on assets ratio of DIPL for three consecutive

years. To that, it is noted that there had been constant decline in return on assets and this means

that the company has not improved in their profitability position over these years (Cohen and

Simnett 2014). In the year 2013, the return on assets ratio of DIPL arrives at 18.24, further there

was slight decline of return on assets at 14.40 (2014) and finally at 11.36 for the year 2015.

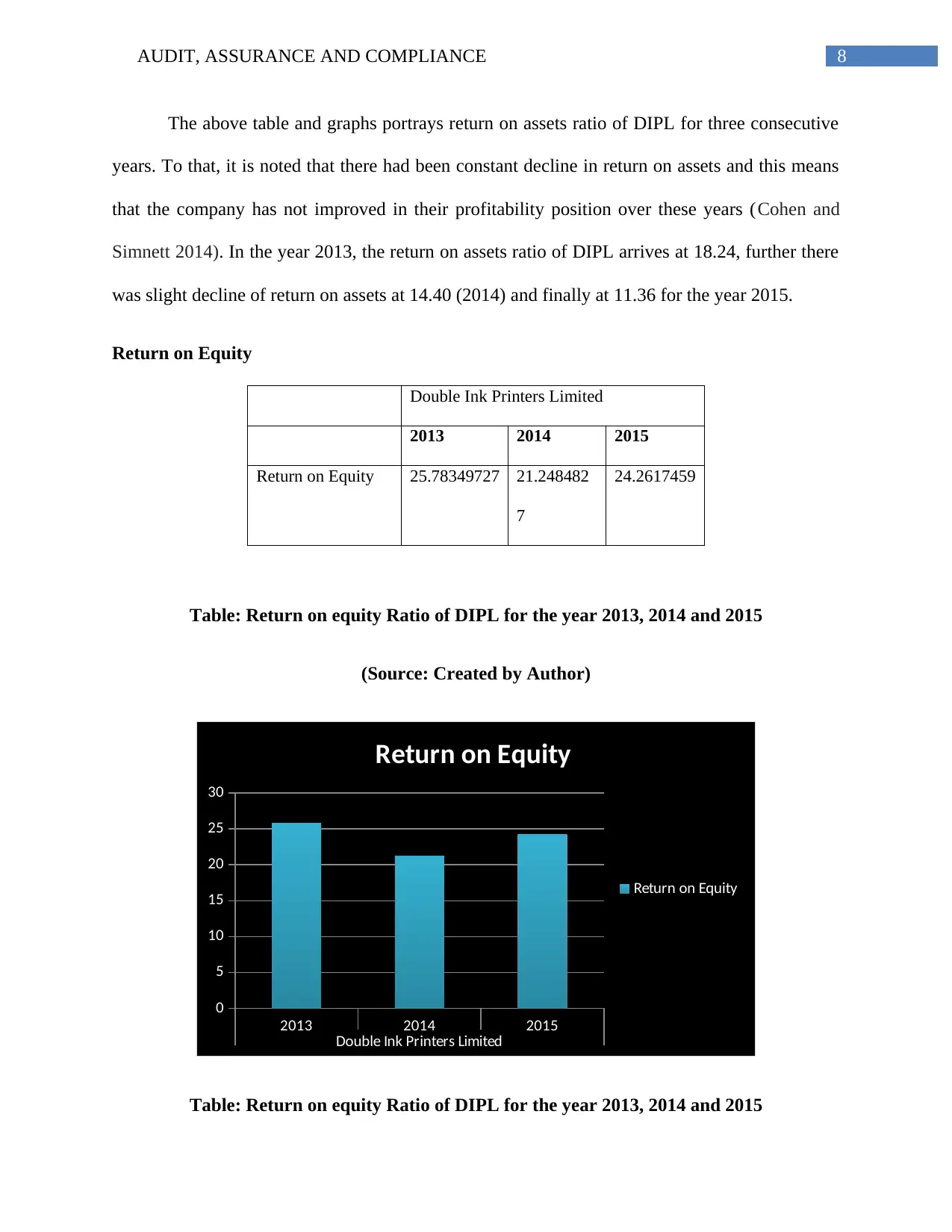

Return on Equity

Double Ink Printers Limited

2013 2014 2015

Return on Equity 25.78349727 21.248482

7

24.2617459

Table: Return on equity Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0

5

10

15

20

25

30

Return on Equity

Return on Equity

Table: Return on equity Ratio of DIPL for the year 2013, 2014 and 2015

The above table and graphs portrays return on assets ratio of DIPL for three consecutive

years. To that, it is noted that there had been constant decline in return on assets and this means

that the company has not improved in their profitability position over these years (Cohen and

Simnett 2014). In the year 2013, the return on assets ratio of DIPL arrives at 18.24, further there

was slight decline of return on assets at 14.40 (2014) and finally at 11.36 for the year 2015.

Return on Equity

Double Ink Printers Limited

2013 2014 2015

Return on Equity 25.78349727 21.248482

7

24.2617459

Table: Return on equity Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0

5

10

15

20

25

30

Return on Equity

Return on Equity

Table: Return on equity Ratio of DIPL for the year 2013, 2014 and 2015

9AUDIT, ASSURANCE AND COMPLIANCE

(Source: Created by Author)

The above table and graphs portrays return on equity ratio of DIPL for three consecutive

years. To that, it is noted that there had been decline in return on equity for the year 2013 and

2014 and then increase in return on equity for the year 2015. In the year 2013, the return on

equity ratio of DIPL arrives at 25.78, further there was slight decline of return on equity at 21.24

(2014) and finally at 24.26 for the year 2015.

Liquidity ratio

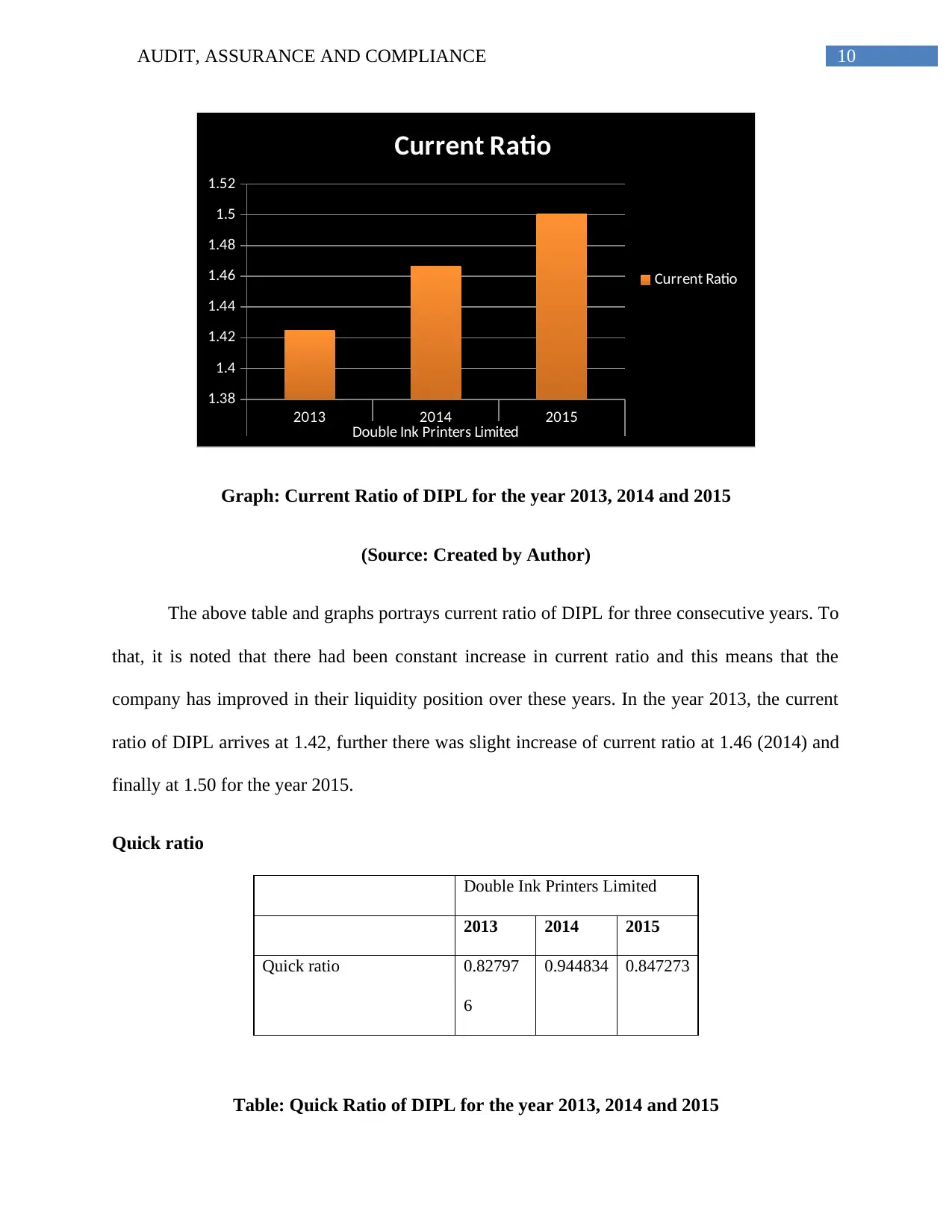

Current ratio

Double Ink Printers Limited

2013 2014 2015

Current Ratio 1.424851 1.466559 1.500731

Table: Current Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

(Source: Created by Author)

The above table and graphs portrays return on equity ratio of DIPL for three consecutive

years. To that, it is noted that there had been decline in return on equity for the year 2013 and

2014 and then increase in return on equity for the year 2015. In the year 2013, the return on

equity ratio of DIPL arrives at 25.78, further there was slight decline of return on equity at 21.24

(2014) and finally at 24.26 for the year 2015.

Liquidity ratio

Current ratio

Double Ink Printers Limited

2013 2014 2015

Current Ratio 1.424851 1.466559 1.500731

Table: Current Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10AUDIT, ASSURANCE AND COMPLIANCE

2013 2014 2015

Double Ink Printers Limited

1.38

1.4

1.42

1.44

1.46

1.48

1.5

1.52

Current Ratio

Current Ratio

Graph: Current Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays current ratio of DIPL for three consecutive years. To

that, it is noted that there had been constant increase in current ratio and this means that the

company has improved in their liquidity position over these years. In the year 2013, the current

ratio of DIPL arrives at 1.42, further there was slight increase of current ratio at 1.46 (2014) and

finally at 1.50 for the year 2015.

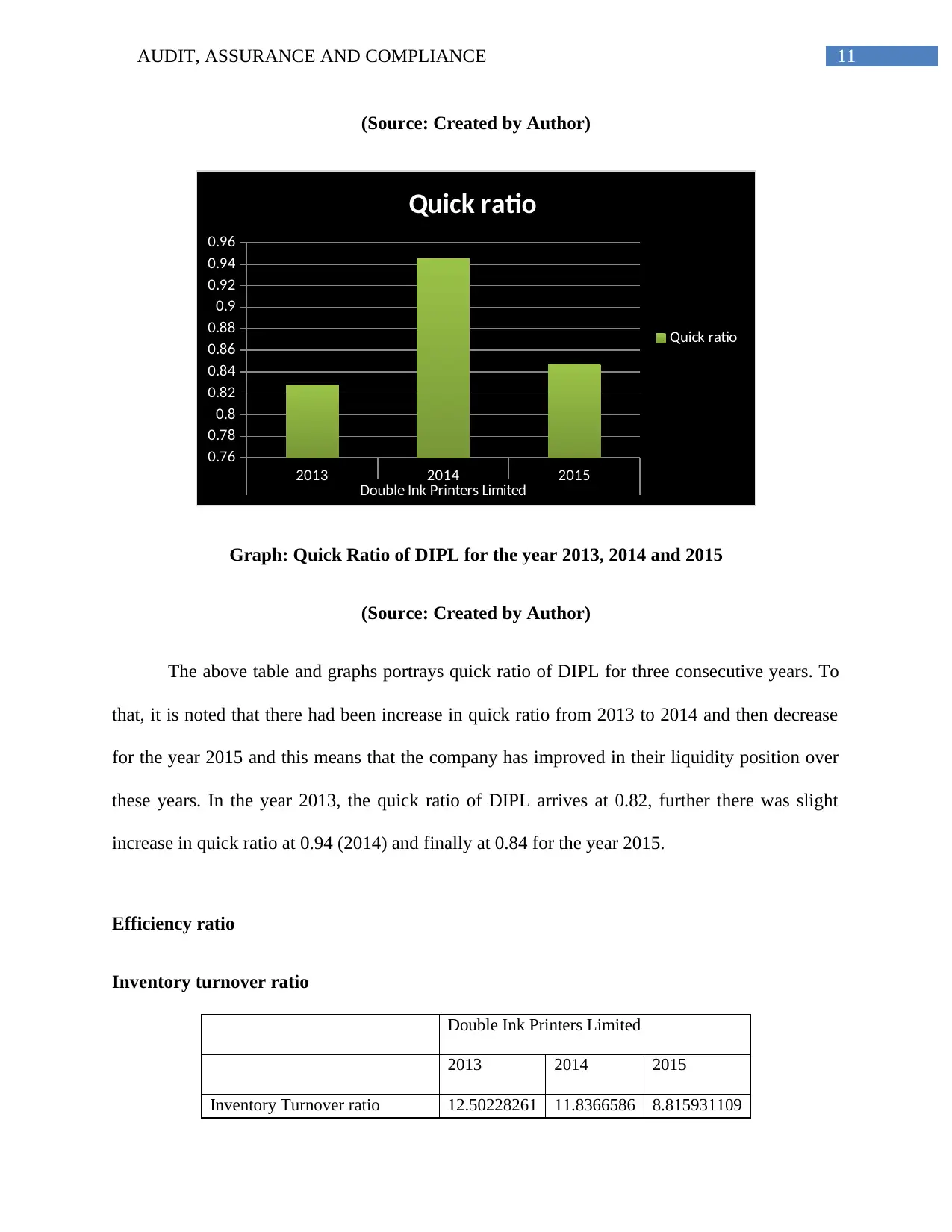

Quick ratio

Double Ink Printers Limited

2013 2014 2015

Quick ratio 0.82797

6

0.944834 0.847273

Table: Quick Ratio of DIPL for the year 2013, 2014 and 2015

2013 2014 2015

Double Ink Printers Limited

1.38

1.4

1.42

1.44

1.46

1.48

1.5

1.52

Current Ratio

Current Ratio

Graph: Current Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays current ratio of DIPL for three consecutive years. To

that, it is noted that there had been constant increase in current ratio and this means that the

company has improved in their liquidity position over these years. In the year 2013, the current

ratio of DIPL arrives at 1.42, further there was slight increase of current ratio at 1.46 (2014) and

finally at 1.50 for the year 2015.

Quick ratio

Double Ink Printers Limited

2013 2014 2015

Quick ratio 0.82797

6

0.944834 0.847273

Table: Quick Ratio of DIPL for the year 2013, 2014 and 2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11AUDIT, ASSURANCE AND COMPLIANCE

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0.76

0.78

0.8

0.82

0.84

0.86

0.88

0.9

0.92

0.94

0.96

Quick ratio

Quick ratio

Graph: Quick Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays quick ratio of DIPL for three consecutive years. To

that, it is noted that there had been increase in quick ratio from 2013 to 2014 and then decrease

for the year 2015 and this means that the company has improved in their liquidity position over

these years. In the year 2013, the quick ratio of DIPL arrives at 0.82, further there was slight

increase in quick ratio at 0.94 (2014) and finally at 0.84 for the year 2015.

Efficiency ratio

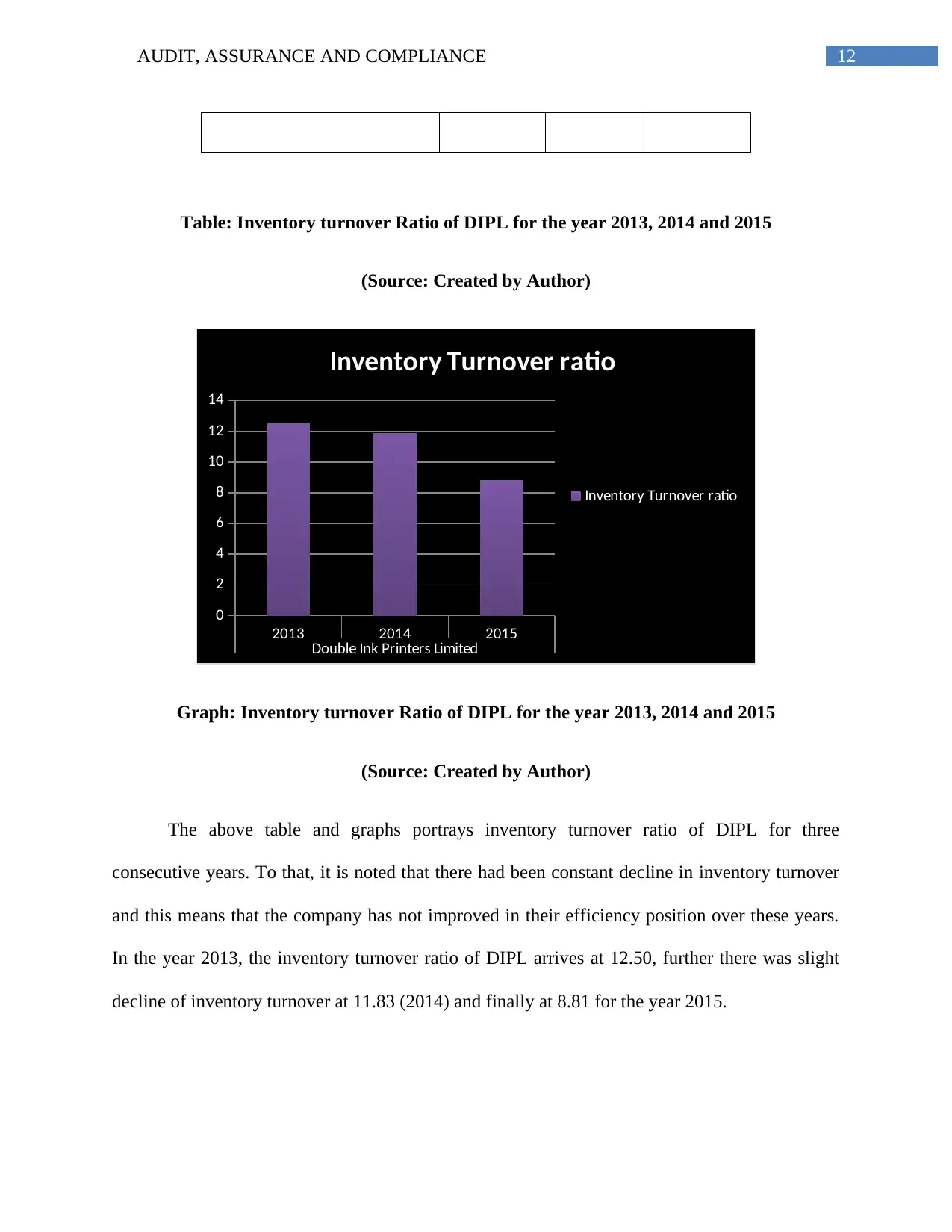

Inventory turnover ratio

Double Ink Printers Limited

2013 2014 2015

Inventory Turnover ratio 12.50228261 11.8366586 8.815931109

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0.76

0.78

0.8

0.82

0.84

0.86

0.88

0.9

0.92

0.94

0.96

Quick ratio

Quick ratio

Graph: Quick Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays quick ratio of DIPL for three consecutive years. To

that, it is noted that there had been increase in quick ratio from 2013 to 2014 and then decrease

for the year 2015 and this means that the company has improved in their liquidity position over

these years. In the year 2013, the quick ratio of DIPL arrives at 0.82, further there was slight

increase in quick ratio at 0.94 (2014) and finally at 0.84 for the year 2015.

Efficiency ratio

Inventory turnover ratio

Double Ink Printers Limited

2013 2014 2015

Inventory Turnover ratio 12.50228261 11.8366586 8.815931109

12AUDIT, ASSURANCE AND COMPLIANCE

Table: Inventory turnover Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0

2

4

6

8

10

12

14

Inventory Turnover ratio

Inventory Turnover ratio

Graph: Inventory turnover Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays inventory turnover ratio of DIPL for three

consecutive years. To that, it is noted that there had been constant decline in inventory turnover

and this means that the company has not improved in their efficiency position over these years.

In the year 2013, the inventory turnover ratio of DIPL arrives at 12.50, further there was slight

decline of inventory turnover at 11.83 (2014) and finally at 8.81 for the year 2015.

Table: Inventory turnover Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

2013 2014 2015

Double Ink Printers Limited

0

2

4

6

8

10

12

14

Inventory Turnover ratio

Inventory Turnover ratio

Graph: Inventory turnover Ratio of DIPL for the year 2013, 2014 and 2015

(Source: Created by Author)

The above table and graphs portrays inventory turnover ratio of DIPL for three

consecutive years. To that, it is noted that there had been constant decline in inventory turnover

and this means that the company has not improved in their efficiency position over these years.

In the year 2013, the inventory turnover ratio of DIPL arrives at 12.50, further there was slight

decline of inventory turnover at 11.83 (2014) and finally at 8.81 for the year 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.