Comprehensive Audit, Assurance, and Compliance Report

VerifiedAdded on 2023/01/06

|14

|3719

|49

Report

AI Summary

This report delves into the core principles of audit, assurance, and compliance. It begins by defining the role of audit and assurance in maintaining business accountability, and ensuring adherence to regulations and standards. The report then explores key concepts such as reasonable assurance and professional skepticism. It analyzes an ethical dilemma related to timely payment of audit fees and proposes steps for resolution. The determination of materiality is examined as a matter of auditor judgment, alongside the impact of qualitative factors on materiality assessments. The report also addresses the auditor's responsibilities concerning going concern assumptions and identifies significant events. Finally, it justifies specific accounting treatments and concludes by emphasizing the importance of audit and assurance in maintaining financial integrity.

Audit, Assurance and

Compliance

Compliance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

(a). Write a letter to Nayan explaining the concept of reasonable assurance...........................................3

(b). Explain in the letter to Nayan the concept of 'professional scepticism’.............................................4

QUESTION 2.................................................................................................................................................5

(a). Explain the ethical problem and why it is a problem.........................................................................5

(b) What can be done about it..................................................................................................................5

QUESTION 3.................................................................................................................................................6

(a). Explain why determination of materiality is a matter of auditor judgment........................................6

(b). Explain whether the information provided impacts on the auditor's assessment of preliminary

materiality................................................................................................................................................6

QUESTION 4.................................................................................................................................................7

(a). Explain the auditor's responsibilities for 'going concern assumptions...............................................7

(b). Identify any significant events or conditions.....................................................................................8

QUESTION 5.................................................................................................................................................9

(a). Justify the events and accounting treatment......................................................................................9

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................11

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

(a). Write a letter to Nayan explaining the concept of reasonable assurance...........................................3

(b). Explain in the letter to Nayan the concept of 'professional scepticism’.............................................4

QUESTION 2.................................................................................................................................................5

(a). Explain the ethical problem and why it is a problem.........................................................................5

(b) What can be done about it..................................................................................................................5

QUESTION 3.................................................................................................................................................6

(a). Explain why determination of materiality is a matter of auditor judgment........................................6

(b). Explain whether the information provided impacts on the auditor's assessment of preliminary

materiality................................................................................................................................................6

QUESTION 4.................................................................................................................................................7

(a). Explain the auditor's responsibilities for 'going concern assumptions...............................................7

(b). Identify any significant events or conditions.....................................................................................8

QUESTION 5.................................................................................................................................................9

(a). Justify the events and accounting treatment......................................................................................9

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Audit & Assurance Compliances serves to maintain an overview of how businesses adhere

to Taxation Operating & Legal compliance requirements and ensure accountability in company

activities to meet the requirements of all shareholders. There is a need for assurance only occurs

when a party intends to take happiness in an issue formulated by a second player, and

confirmation is supplied and when an autonomous point of view can be services of a third party.

An audit is the review of an entity's financial statements of somebody outside of that entity, as

described in the financial statement (Brenninkmeijer and et.al, 2017). A balance sheet, an income

statement, a statement of adjustments in equity, an income statement and documents containing a

description of relevant accounting practices and other supplementary documents are contained in

the financial report. The aim of the audit is to determine if the data contained in the financial

report, taking in its entirety, represents the company's monetary condition. This evaluation

addresses many subjects that are mostly about the audit and auditors, and how they work in each

event-related organisation. The objective of this review is to ensure that business statements are

accurate and fair; all operations should also be carried out in accordance with regulations and

practices.

QUESTION 1

(a). Write a letter to Nayan explaining the concept of reasonable assurance

To: Nayan

Subject: Explaining the concept of reasonable assurance

Dear Nayan,

I hope you doing well and in good health. I am enjoying my new job and environment of

business. Thanks for your letter and it was great to hear from you. You asked me to tell you

about reasonable assurance. It requires for better understanding that there is still a potential

probability of not eliminating or finding material defects on a periodic basis. It needs a greater

understanding there is still a possible possibility that material defects will not be removed or

detected on a recurring basis (Davis, 2017). Similar assurance, if not total faith, is indeed a high

degree of certainty. There is a discrepancy between the requirements of the NGA (National

Audit & Assurance Compliances serves to maintain an overview of how businesses adhere

to Taxation Operating & Legal compliance requirements and ensure accountability in company

activities to meet the requirements of all shareholders. There is a need for assurance only occurs

when a party intends to take happiness in an issue formulated by a second player, and

confirmation is supplied and when an autonomous point of view can be services of a third party.

An audit is the review of an entity's financial statements of somebody outside of that entity, as

described in the financial statement (Brenninkmeijer and et.al, 2017). A balance sheet, an income

statement, a statement of adjustments in equity, an income statement and documents containing a

description of relevant accounting practices and other supplementary documents are contained in

the financial report. The aim of the audit is to determine if the data contained in the financial

report, taking in its entirety, represents the company's monetary condition. This evaluation

addresses many subjects that are mostly about the audit and auditors, and how they work in each

event-related organisation. The objective of this review is to ensure that business statements are

accurate and fair; all operations should also be carried out in accordance with regulations and

practices.

QUESTION 1

(a). Write a letter to Nayan explaining the concept of reasonable assurance

To: Nayan

Subject: Explaining the concept of reasonable assurance

Dear Nayan,

I hope you doing well and in good health. I am enjoying my new job and environment of

business. Thanks for your letter and it was great to hear from you. You asked me to tell you

about reasonable assurance. It requires for better understanding that there is still a potential

probability of not eliminating or finding material defects on a periodic basis. It needs a greater

understanding there is still a possible possibility that material defects will not be removed or

detected on a recurring basis (Davis, 2017). Similar assurance, if not total faith, is indeed a high

degree of certainty. There is a discrepancy between the requirements of the NGA (National

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Governors Association) and the auditor's level of competence. Reasonable verification is

conducted by audit, not by utter confirmation.

A significant concentration of assurance based on material mistakes, but not an unmitigated

version, is reasonable assurance. Reasonable assurance contains the information that there is still

a faraway probability of not preventing or detecting material mistakes on a periodic manner. The

auditor must get sufficient and acceptable audit proof to increasing the risk to an acceptable level

and achieve fair confirmation. This suggests that there is some doubt resulting through the use of

analysis, since it is likely that a content misrepresentation would be omitted. Not because they

perform collaborations with inadequate caution, but also because constraints intrinsic in the

mechanism hinder the opportunity to offer absolute assurance, auditors are still unable to achieve

absolute assurance. In the behavior of various audit process, the use of research methods.

A high degree of confirmation is reasonable assurance, but just not absolute assurance. It is not a

certainty that financial reports (if either attributable to fraud or mistakes) are safe from across all

material mistakes. They should, even so, include a reasonable assurance that financial statements

as a whole are not substantially misrepresented (Eulerich, Kremin and Wood, 2019). The

external auditor has put an attempt to narrow the information asymmetry between the standards

of assurance that consumers believe an audit report will provide, and the success of a project that

it actually delivers. In order to provide further clear feedback, it has modified legal requirements

and, in accordance with regulatory agencies, presented more active supervision and delivered

with more disciplinary actions for the issuance of inaccurate findings.

(b). Explain in the letter to Nayan the concept of 'professional scepticism’

To: Nayan

Subject: Explaining the concept of professional Scepticism

Dear Nayan,

I hope you understand the importance of reasonable assurance and in this letter I want to disuses

about professional scepticism. Professional scepticism is a mindset that encompasses a

challenging mind, remaining responsive to complications whereby can signal suspected

conducted by audit, not by utter confirmation.

A significant concentration of assurance based on material mistakes, but not an unmitigated

version, is reasonable assurance. Reasonable assurance contains the information that there is still

a faraway probability of not preventing or detecting material mistakes on a periodic manner. The

auditor must get sufficient and acceptable audit proof to increasing the risk to an acceptable level

and achieve fair confirmation. This suggests that there is some doubt resulting through the use of

analysis, since it is likely that a content misrepresentation would be omitted. Not because they

perform collaborations with inadequate caution, but also because constraints intrinsic in the

mechanism hinder the opportunity to offer absolute assurance, auditors are still unable to achieve

absolute assurance. In the behavior of various audit process, the use of research methods.

A high degree of confirmation is reasonable assurance, but just not absolute assurance. It is not a

certainty that financial reports (if either attributable to fraud or mistakes) are safe from across all

material mistakes. They should, even so, include a reasonable assurance that financial statements

as a whole are not substantially misrepresented (Eulerich, Kremin and Wood, 2019). The

external auditor has put an attempt to narrow the information asymmetry between the standards

of assurance that consumers believe an audit report will provide, and the success of a project that

it actually delivers. In order to provide further clear feedback, it has modified legal requirements

and, in accordance with regulatory agencies, presented more active supervision and delivered

with more disciplinary actions for the issuance of inaccurate findings.

(b). Explain in the letter to Nayan the concept of 'professional scepticism’

To: Nayan

Subject: Explaining the concept of professional Scepticism

Dear Nayan,

I hope you understand the importance of reasonable assurance and in this letter I want to disuses

about professional scepticism. Professional scepticism is a mindset that encompasses a

challenging mind, remaining responsive to complications whereby can signal suspected

misstatement attributed to negligence or fraud, and a reasonable consideration of audit proof. It is

a pillar of the audit committees that we'll need to preserve and develop to help the auditor of the

potential. Professional scepticism has been used to years of knowledge thru the pointed

questions, structure consisting of corroboration, and awareness to warning signs and

discrepancies (Ji, Lu and Qu, 2018).

The degree to which professional scepticism is being used has attracted a lot of scrutiny recently.

In particular, regulatory authorities contend that, in performing its duties, inspectors are not

adequately sceptical. An auditor should have the sceptic mindset that will allow him sensitive for

the circumstances to avoid fraudulent activity. He needs to be careful about the risks of mistakes.

Some inspectors with competent scepticism skills should be present in addition to making the

financial reports straightforward, thereby shielding the report from all sorts of mistakes.

Technical scepticism is often the strength acquired from continued preparation and knowledge.

QUESTION 2

(a). Explain the ethical problem and why it is a problem

According to the situation, a dispute with the basic values of a community is generated by

situations or actions and ethical problems arise. Both people and organizations may be

influenced by these disputes, as all their actions can be challenged from an ethical perspective. In

this situation, it is discussed that the ethical dilemma of the retailer does not reimburse

examination rates on time and time. While the auditor could not publish an audit opinion on the

impact of the management team in a straightforward way, it is considered to become an ethical

issue. Most law specifies that deals need to be reached once counseling starts, so that consumers

are it's what everyone wants (Maroun, 2017).

(b) What can be done about it

The steps involved in resolving the ethical problems are:

1. Lay the actual information down:

2. Recognize the legal challenges that are concerned:

3. Describe the basic values that are under attack:

a pillar of the audit committees that we'll need to preserve and develop to help the auditor of the

potential. Professional scepticism has been used to years of knowledge thru the pointed

questions, structure consisting of corroboration, and awareness to warning signs and

discrepancies (Ji, Lu and Qu, 2018).

The degree to which professional scepticism is being used has attracted a lot of scrutiny recently.

In particular, regulatory authorities contend that, in performing its duties, inspectors are not

adequately sceptical. An auditor should have the sceptic mindset that will allow him sensitive for

the circumstances to avoid fraudulent activity. He needs to be careful about the risks of mistakes.

Some inspectors with competent scepticism skills should be present in addition to making the

financial reports straightforward, thereby shielding the report from all sorts of mistakes.

Technical scepticism is often the strength acquired from continued preparation and knowledge.

QUESTION 2

(a). Explain the ethical problem and why it is a problem

According to the situation, a dispute with the basic values of a community is generated by

situations or actions and ethical problems arise. Both people and organizations may be

influenced by these disputes, as all their actions can be challenged from an ethical perspective. In

this situation, it is discussed that the ethical dilemma of the retailer does not reimburse

examination rates on time and time. While the auditor could not publish an audit opinion on the

impact of the management team in a straightforward way, it is considered to become an ethical

issue. Most law specifies that deals need to be reached once counseling starts, so that consumers

are it's what everyone wants (Maroun, 2017).

(b) What can be done about it

The steps involved in resolving the ethical problems are:

1. Lay the actual information down:

2. Recognize the legal challenges that are concerned:

3. Describe the basic values that are under attack:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Pinpoint the appropriate possible courses of action for you:

5. Keep comparing and analyze the solutions (the advantages and drawbacks are laid down),

6. Deciding:

In order to solve this problem, it is necessary to notify the consumer that they will not reveal an

audit opinion that has a negative impact on their business if they do not pay on time. As a

consequence, consumers are asking for reimbursement and communicating with people who

would have the authority and strength to address the situation completely (Maroun, 2019).

QUESTION 3

(a). Explain why determination of materiality is a matter of auditor judgment

The determination of materiality by the audit committee is a subject of professional

judgment and is influenced by the inspector's understanding of the consumers of the company's

financial' business information requirements. The duty of the auditors is to evaluate if the

financial reports are significantly mischaracterized. Auditors depend on principles of wisdom

and technical experience to develop a standard of materiality. The number and quality of

misjudgment is also termed by them. The minimum of materiality is commonly expressed as a

generic proportion of a line item of a particular financial statement. ISAs auditing standards to

provide fair confirmation as the criterion for the auditor's judgment over whether the financial

reports of the whole of the free of material mistakes. Consequently, the notion of materiality is

central to the audit.

(b). Explain whether the information provided impacts on the auditor's assessment of preliminary

materiality

Qualitative variables that impact the materiality decision of an auditor include: quantities

involving fraud. Fraud quantities are generally deemed more severe than accidental mistakes of

equivalent amounts of dollars since fraud represents the integrity and competence of the

management or other workers involved (Mendez and Bachtler, 2017). Materiality depends on the

nature and quality of the failure or defect measured in the situation surrounding it. The deciding

factor may be the size or value of the object, or a combination of both. The preliminary

judgments of materiality would be influenced by the planned presentation of the income

statement. Unless the financial reports are widely disseminated to consumers, it is possible that

5. Keep comparing and analyze the solutions (the advantages and drawbacks are laid down),

6. Deciding:

In order to solve this problem, it is necessary to notify the consumer that they will not reveal an

audit opinion that has a negative impact on their business if they do not pay on time. As a

consequence, consumers are asking for reimbursement and communicating with people who

would have the authority and strength to address the situation completely (Maroun, 2019).

QUESTION 3

(a). Explain why determination of materiality is a matter of auditor judgment

The determination of materiality by the audit committee is a subject of professional

judgment and is influenced by the inspector's understanding of the consumers of the company's

financial' business information requirements. The duty of the auditors is to evaluate if the

financial reports are significantly mischaracterized. Auditors depend on principles of wisdom

and technical experience to develop a standard of materiality. The number and quality of

misjudgment is also termed by them. The minimum of materiality is commonly expressed as a

generic proportion of a line item of a particular financial statement. ISAs auditing standards to

provide fair confirmation as the criterion for the auditor's judgment over whether the financial

reports of the whole of the free of material mistakes. Consequently, the notion of materiality is

central to the audit.

(b). Explain whether the information provided impacts on the auditor's assessment of preliminary

materiality

Qualitative variables that impact the materiality decision of an auditor include: quantities

involving fraud. Fraud quantities are generally deemed more severe than accidental mistakes of

equivalent amounts of dollars since fraud represents the integrity and competence of the

management or other workers involved (Mendez and Bachtler, 2017). Materiality depends on the

nature and quality of the failure or defect measured in the situation surrounding it. The deciding

factor may be the size or value of the object, or a combination of both. The preliminary

judgments of materiality would be influenced by the planned presentation of the income

statement. Unless the financial reports are widely disseminated to consumers, it is possible that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the preliminary materiality judgment will be set smaller than if it is not anticipated that the

financial statements will be extensively spread. There are mentioned some qualitative factors

which required for auditor’s assessment of preliminary materiality:

The future impact of the misrepresentation on trends, in particular profitability trends.

A error that turns a loss into revenue or vice versa.

The effect of the misrepresentation on sector information , for example, the relevance of

the subject to a specific segment, which is essential for the potential profits of the

business, the omnipresence of the matter on sustainability reports, and the influence of

the subject on developments in sustainability reports, all in addition to the business

certificate verification overall (Mentz, Barac and Odendaal, 2018).

The possible impact of the misrepresentation on the enforcement of the business with

employment contracts, other mutual arrangements and government regulations.

The presence of criteria for legislative or regulatory compliance that influence standards

of materiality. For example, by meeting the conditions for the awarding of incentives or

other types of performance pay, a mistake that has the impact of can organisation’s

remuneration.

Awareness of the conditions underlying the misrepresentation, such as the repercussions

of misrepresentations associated with fraud and alleged criminal activity, breaches of

contract clauses and improprieties.

For instance, the importance of the aspect of the financial report impacted by the error is

an error concerning ongoing income as opposed to one concerning a nonrecurring

expense or credit, including an exceptional object (Robinson and McKee, 2019).

QUESTION 4

(a). Explain the auditor's responsibilities for 'going concern assumptions

The theory of the going concern enables the corporation to delay some of its prepaid costs

until accounting periods. A basic assumption in the preparing the financial statements are the

going concern concept. In the absence of sufficient irrefutable evidence, an individual is believed

to be a continuing concern. In the preparation of financial reports, the principle of current

concern is an implicit presumption, since it is presumed that the company has neither the purpose

nor the need to significantly consolidate or reduce the size of its activities. Another of the basic

financial statements will be extensively spread. There are mentioned some qualitative factors

which required for auditor’s assessment of preliminary materiality:

The future impact of the misrepresentation on trends, in particular profitability trends.

A error that turns a loss into revenue or vice versa.

The effect of the misrepresentation on sector information , for example, the relevance of

the subject to a specific segment, which is essential for the potential profits of the

business, the omnipresence of the matter on sustainability reports, and the influence of

the subject on developments in sustainability reports, all in addition to the business

certificate verification overall (Mentz, Barac and Odendaal, 2018).

The possible impact of the misrepresentation on the enforcement of the business with

employment contracts, other mutual arrangements and government regulations.

The presence of criteria for legislative or regulatory compliance that influence standards

of materiality. For example, by meeting the conditions for the awarding of incentives or

other types of performance pay, a mistake that has the impact of can organisation’s

remuneration.

Awareness of the conditions underlying the misrepresentation, such as the repercussions

of misrepresentations associated with fraud and alleged criminal activity, breaches of

contract clauses and improprieties.

For instance, the importance of the aspect of the financial report impacted by the error is

an error concerning ongoing income as opposed to one concerning a nonrecurring

expense or credit, including an exceptional object (Robinson and McKee, 2019).

QUESTION 4

(a). Explain the auditor's responsibilities for 'going concern assumptions

The theory of the going concern enables the corporation to delay some of its prepaid costs

until accounting periods. A basic assumption in the preparing the financial statements are the

going concern concept. In the absence of sufficient irrefutable evidence, an individual is believed

to be a continuing concern. In the preparation of financial reports, the principle of current

concern is an implicit presumption, since it is presumed that the company has neither the purpose

nor the need to significantly consolidate or reduce the size of its activities. Another of the basic

accounting principles on the grounds where its financial statements are prepared is Going

Concern. Financial statements must be prepared believing that, in the near future, a corporate

organisation can continue to thrive even without manager's need for it desires to consolidate the

organisation or substantially reduce its company's operations (Shahzad, Saeed and Ehsan, 2017).

In the preparation and presentation of financial statement, it is also the duty of the auditor

of a corporation to assess if the going concern assumption is acceptable. Unless the going

concern assumption is found by the administration to be incorrect, the statement of financial

position will have to be updated on end things framework. This implies that the resources will be

recognized at a sum that is supposed to be realized in the normal course of business in its

disposal (net of healthcare distribution) instead of from its continued use. Assets, rather than

their significance as a coordinated team, are valued for their financial value. Liabilities are paid

for in sums which are likely to be resolved. It is not the duty of the auditor to decide whether or

not an organisation should conduct its financial reports and use the accounting basis of the

growing concerns; this is manager's responsibility. However according ISA 570, the auditor 's

duty is to give accurate audit proof as to the advisability of the company's use of the statutory

basis of recent question in the statement of financial position and to determine if there is

considerable difficulty as to the ability of the economy to proceed as an increasing concern

(Shalimova, and Androshchuk, 2018).

(b). Identify any significant events or conditions

Lack of ability to offer distribution analysis

Significant losses or problems with cash flow which have occurred since before the end

of the reporting period

Detrimental important economic ratios

Evidence of removal from the banking or financial organizations of monetary assistance

Negative cash flows for operations

Significant interest payments of debt that the company will not be able to fulfil will fall

due to

Currently awaiting legal and regulatory action against organization, which could result in

charges that are impossible to be settled if approved.

A substantial drop in gross profit. ...

Concern. Financial statements must be prepared believing that, in the near future, a corporate

organisation can continue to thrive even without manager's need for it desires to consolidate the

organisation or substantially reduce its company's operations (Shahzad, Saeed and Ehsan, 2017).

In the preparation and presentation of financial statement, it is also the duty of the auditor

of a corporation to assess if the going concern assumption is acceptable. Unless the going

concern assumption is found by the administration to be incorrect, the statement of financial

position will have to be updated on end things framework. This implies that the resources will be

recognized at a sum that is supposed to be realized in the normal course of business in its

disposal (net of healthcare distribution) instead of from its continued use. Assets, rather than

their significance as a coordinated team, are valued for their financial value. Liabilities are paid

for in sums which are likely to be resolved. It is not the duty of the auditor to decide whether or

not an organisation should conduct its financial reports and use the accounting basis of the

growing concerns; this is manager's responsibility. However according ISA 570, the auditor 's

duty is to give accurate audit proof as to the advisability of the company's use of the statutory

basis of recent question in the statement of financial position and to determine if there is

considerable difficulty as to the ability of the economy to proceed as an increasing concern

(Shalimova, and Androshchuk, 2018).

(b). Identify any significant events or conditions

Lack of ability to offer distribution analysis

Significant losses or problems with cash flow which have occurred since before the end

of the reporting period

Detrimental important economic ratios

Evidence of removal from the banking or financial organizations of monetary assistance

Negative cash flows for operations

Significant interest payments of debt that the company will not be able to fulfil will fall

due to

Currently awaiting legal and regulatory action against organization, which could result in

charges that are impossible to be settled if approved.

A substantial drop in gross profit. ...

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Major Outstanding Debt or Owing Taxes. ...

The rest of the checking account. ...

Complete lack of Fund for Science & Architecture. ...

Lost in Core Management. ...

Cash Flow issues. ...

Lost from the Project Nice (Střihavková, 2018)

QUESTION 5

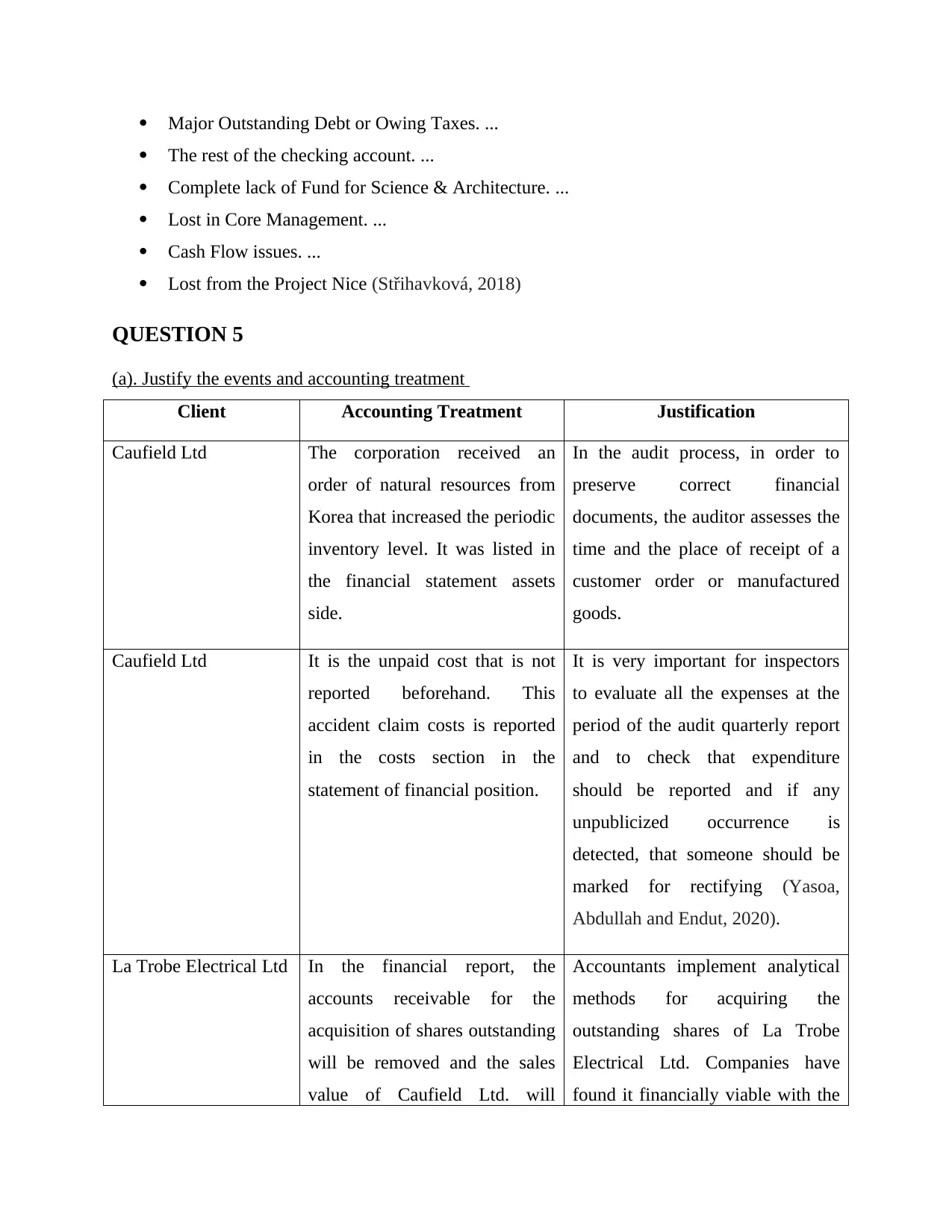

(a). Justify the events and accounting treatment

Client Accounting Treatment Justification

Caufield Ltd The corporation received an

order of natural resources from

Korea that increased the periodic

inventory level. It was listed in

the financial statement assets

side.

In the audit process, in order to

preserve correct financial

documents, the auditor assesses the

time and the place of receipt of a

customer order or manufactured

goods.

Caufield Ltd It is the unpaid cost that is not

reported beforehand. This

accident claim costs is reported

in the costs section in the

statement of financial position.

It is very important for inspectors

to evaluate all the expenses at the

period of the audit quarterly report

and to check that expenditure

should be reported and if any

unpublicized occurrence is

detected, that someone should be

marked for rectifying (Yasoa,

Abdullah and Endut, 2020).

La Trobe Electrical Ltd In the financial report, the

accounts receivable for the

acquisition of shares outstanding

will be removed and the sales

value of Caufield Ltd. will

Accountants implement analytical

methods for acquiring the

outstanding shares of La Trobe

Electrical Ltd. Companies have

found it financially viable with the

The rest of the checking account. ...

Complete lack of Fund for Science & Architecture. ...

Lost in Core Management. ...

Cash Flow issues. ...

Lost from the Project Nice (Střihavková, 2018)

QUESTION 5

(a). Justify the events and accounting treatment

Client Accounting Treatment Justification

Caufield Ltd The corporation received an

order of natural resources from

Korea that increased the periodic

inventory level. It was listed in

the financial statement assets

side.

In the audit process, in order to

preserve correct financial

documents, the auditor assesses the

time and the place of receipt of a

customer order or manufactured

goods.

Caufield Ltd It is the unpaid cost that is not

reported beforehand. This

accident claim costs is reported

in the costs section in the

statement of financial position.

It is very important for inspectors

to evaluate all the expenses at the

period of the audit quarterly report

and to check that expenditure

should be reported and if any

unpublicized occurrence is

detected, that someone should be

marked for rectifying (Yasoa,

Abdullah and Endut, 2020).

La Trobe Electrical Ltd In the financial report, the

accounts receivable for the

acquisition of shares outstanding

will be removed and the sales

value of Caufield Ltd. will

Accountants implement analytical

methods for acquiring the

outstanding shares of La Trobe

Electrical Ltd. Companies have

found it financially viable with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

improve. assistance of the analysis approach,

which is why they buy these share

capital.

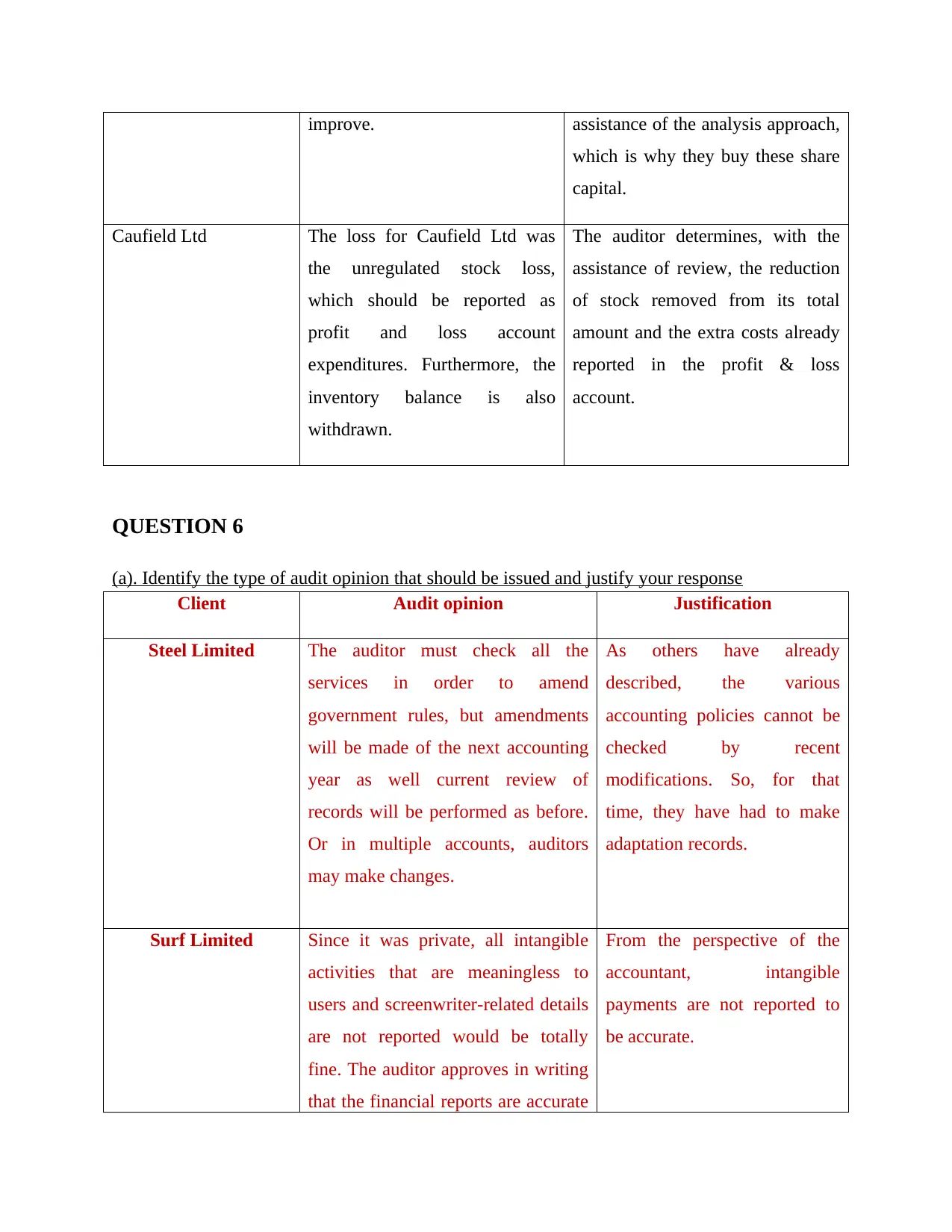

Caufield Ltd The loss for Caufield Ltd was

the unregulated stock loss,

which should be reported as

profit and loss account

expenditures. Furthermore, the

inventory balance is also

withdrawn.

The auditor determines, with the

assistance of review, the reduction

of stock removed from its total

amount and the extra costs already

reported in the profit & loss

account.

QUESTION 6

(a). Identify the type of audit opinion that should be issued and justify your response

Client Audit opinion Justification

Steel Limited The auditor must check all the

services in order to amend

government rules, but amendments

will be made of the next accounting

year as well current review of

records will be performed as before.

Or in multiple accounts, auditors

may make changes.

As others have already

described, the various

accounting policies cannot be

checked by recent

modifications. So, for that

time, they have had to make

adaptation records.

Surf Limited Since it was private, all intangible

activities that are meaningless to

users and screenwriter-related details

are not reported would be totally

fine. The auditor approves in writing

that the financial reports are accurate

From the perspective of the

accountant, intangible

payments are not reported to

be accurate.

which is why they buy these share

capital.

Caufield Ltd The loss for Caufield Ltd was

the unregulated stock loss,

which should be reported as

profit and loss account

expenditures. Furthermore, the

inventory balance is also

withdrawn.

The auditor determines, with the

assistance of review, the reduction

of stock removed from its total

amount and the extra costs already

reported in the profit & loss

account.

QUESTION 6

(a). Identify the type of audit opinion that should be issued and justify your response

Client Audit opinion Justification

Steel Limited The auditor must check all the

services in order to amend

government rules, but amendments

will be made of the next accounting

year as well current review of

records will be performed as before.

Or in multiple accounts, auditors

may make changes.

As others have already

described, the various

accounting policies cannot be

checked by recent

modifications. So, for that

time, they have had to make

adaptation records.

Surf Limited Since it was private, all intangible

activities that are meaningless to

users and screenwriter-related details

are not reported would be totally

fine. The auditor approves in writing

that the financial reports are accurate

From the perspective of the

accountant, intangible

payments are not reported to

be accurate.

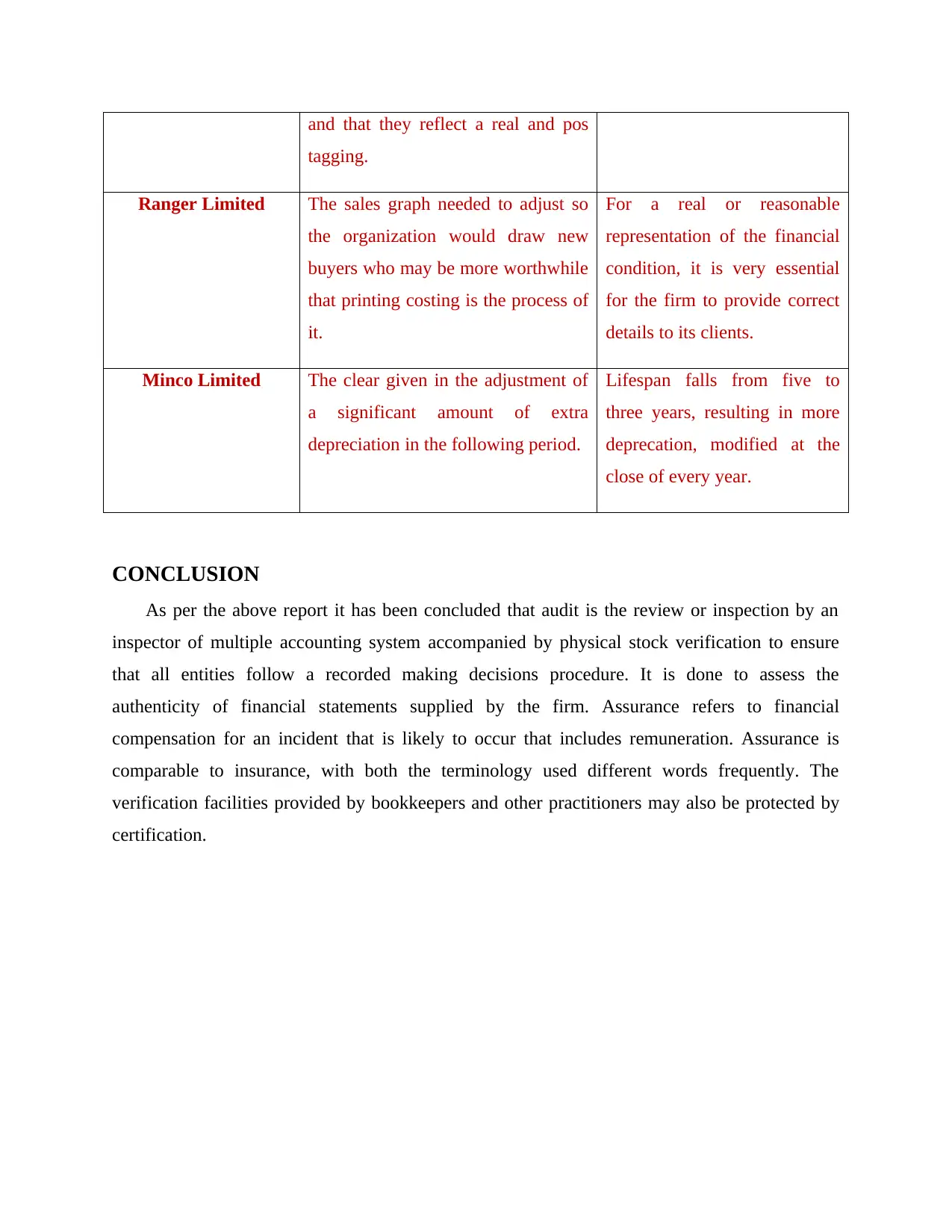

and that they reflect a real and pos

tagging.

Ranger Limited The sales graph needed to adjust so

the organization would draw new

buyers who may be more worthwhile

that printing costing is the process of

it.

For a real or reasonable

representation of the financial

condition, it is very essential

for the firm to provide correct

details to its clients.

Minco Limited The clear given in the adjustment of

a significant amount of extra

depreciation in the following period.

Lifespan falls from five to

three years, resulting in more

deprecation, modified at the

close of every year.

CONCLUSION

As per the above report it has been concluded that audit is the review or inspection by an

inspector of multiple accounting system accompanied by physical stock verification to ensure

that all entities follow a recorded making decisions procedure. It is done to assess the

authenticity of financial statements supplied by the firm. Assurance refers to financial

compensation for an incident that is likely to occur that includes remuneration. Assurance is

comparable to insurance, with both the terminology used different words frequently. The

verification facilities provided by bookkeepers and other practitioners may also be protected by

certification.

tagging.

Ranger Limited The sales graph needed to adjust so

the organization would draw new

buyers who may be more worthwhile

that printing costing is the process of

it.

For a real or reasonable

representation of the financial

condition, it is very essential

for the firm to provide correct

details to its clients.

Minco Limited The clear given in the adjustment of

a significant amount of extra

depreciation in the following period.

Lifespan falls from five to

three years, resulting in more

deprecation, modified at the

close of every year.

CONCLUSION

As per the above report it has been concluded that audit is the review or inspection by an

inspector of multiple accounting system accompanied by physical stock verification to ensure

that all entities follow a recorded making decisions procedure. It is done to assess the

authenticity of financial statements supplied by the firm. Assurance refers to financial

compensation for an incident that is likely to occur that includes remuneration. Assurance is

comparable to insurance, with both the terminology used different words frequently. The

verification facilities provided by bookkeepers and other practitioners may also be protected by

certification.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.