HI6026: Audit, Assurance and Compliance - CSR Limited Report Analysis

VerifiedAdded on 2023/06/04

|16

|3887

|59

Report

AI Summary

This report provides a comprehensive analysis of the 2018 annual report of CSR Limited, focusing on its audit, assurance, and compliance aspects. It examines the company's adherence to auditing standards, including APES 110, Australian standards for auditing, IFRS, IASB, and Corporations Act 2001. The report assesses the independence of Deloitte, the auditing firm, and evaluates non-audit services provided, along with the auditor's remuneration. Key audit matters, such as product liability provisions and asset valuation, are analyzed in detail, including the audit processes and the auditor's approach to addressing these issues. The role of the audit committee and its oversight of financial reporting are also discussed. Furthermore, the report highlights the variations between the accountabilities of management, directors, and auditors. The report identifies material subsequent events and evaluates the appropriateness of material information. This analysis aims to provide a thorough understanding of CSR Limited's financial reporting practices and the effectiveness of its audit processes.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Executive Summary:

The current paper would try to evaluate the latest annual report of CSR Limited based on

the various auditing features of the operating statements. CSR Limited is a famous

Australian industrial company engaged in manufacturing building products. The members of

Deloitte involved in audit work of CSR Limited have made thorough analysis of material

information of the organisation in the most responsible manner. They have conformed to

the necessary standards mentioned in APES 110, Australian standards for auditing, IFRS,

IASB, Corporations Act 2001 and others. Two material subsequent events are deemed to be

identified from the annual report of CSR Limited. One of them is sale of a surplus asset and

another is associated with declaration of dividend. As per the latest annual report of CSR

Limited, Deloitte has performed all the necessary functions needed to analyse the material

aspects as well other information that have the possibility of developing material

misstatement risk in terms of financial reporting.

Executive Summary:

The current paper would try to evaluate the latest annual report of CSR Limited based on

the various auditing features of the operating statements. CSR Limited is a famous

Australian industrial company engaged in manufacturing building products. The members of

Deloitte involved in audit work of CSR Limited have made thorough analysis of material

information of the organisation in the most responsible manner. They have conformed to

the necessary standards mentioned in APES 110, Australian standards for auditing, IFRS,

IASB, Corporations Act 2001 and others. Two material subsequent events are deemed to be

identified from the annual report of CSR Limited. One of them is sale of a surplus asset and

another is associated with declaration of dividend. As per the latest annual report of CSR

Limited, Deloitte has performed all the necessary functions needed to analyse the material

aspects as well other information that have the possibility of developing material

misstatement risk in terms of financial reporting.

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Introduction:..............................................................................................................................3

Compliance with the independence requirement of the auditor:............................................3

Non-audit services:....................................................................................................................4

Analysis of the auditor’s remuneration:....................................................................................5

Key audit matters:......................................................................................................................5

Audit committee:.......................................................................................................................8

Audit opinion:.............................................................................................................................8

Variations between accountabilities of the management, directors and auditors:..................9

Material subsequent events:...................................................................................................10

Appropriateness of material information:...............................................................................10

Missing or undisclosed material information:.........................................................................11

Follow-up questions:................................................................................................................11

Conclusion:...............................................................................................................................12

References and Bibliographies:................................................................................................13

Table of Contents

Introduction:..............................................................................................................................3

Compliance with the independence requirement of the auditor:............................................3

Non-audit services:....................................................................................................................4

Analysis of the auditor’s remuneration:....................................................................................5

Key audit matters:......................................................................................................................5

Audit committee:.......................................................................................................................8

Audit opinion:.............................................................................................................................8

Variations between accountabilities of the management, directors and auditors:..................9

Material subsequent events:...................................................................................................10

Appropriateness of material information:...............................................................................10

Missing or undisclosed material information:.........................................................................11

Follow-up questions:................................................................................................................11

Conclusion:...............................................................................................................................12

References and Bibliographies:................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

Introduction:

Auditing could be explained as an aim related examination and evaluation of the

operating statement of a company in order to assure the honest and appropriate recording

of the transactions claimed. Therefore, it is the liability for the auditors to enhance the

quality of the audit report by disclosing all vital data related to the material characteristics

of the financial statements (Kush et al. 2017). Such information requires to be presented to

the stakeholders of the company in a clarified and simple language. In the modern era,

various actions are attempted by the audit committees in order to assure that the quality of

the audit reports gets improved. The current study would try to evaluate the latest annual

report of CSR Limited based on the various auditing features of the operating statements.

CSR Limited is a famous Australian industrial company engaged in manufacturing building

products (Csr.com.au 2018). In this regard, it requires to be mentioned that Deloitte is the

audit partner of the organisation for the year 2018.

Compliance with the independence requirement of the auditor:

According to the annual report of CSR Limited in 2018, no members of Deloitte were

engaged with the business activities of the company. Besides, no specific staff of the audit

group of Deloitte played a significant role in the group audit of CSR Limited for the year,

which is made under a declaration in accordance with “Section 342A of the Corporations

Act 2001”. On the other hand, Deloitte has complied with all the requirements mentioned

under “Section 307C of the Corporations Act 2001” covering the following points:

1. No violations have been there related to the independence needs of the auditor with

respect to audit.

Introduction:

Auditing could be explained as an aim related examination and evaluation of the

operating statement of a company in order to assure the honest and appropriate recording

of the transactions claimed. Therefore, it is the liability for the auditors to enhance the

quality of the audit report by disclosing all vital data related to the material characteristics

of the financial statements (Kush et al. 2017). Such information requires to be presented to

the stakeholders of the company in a clarified and simple language. In the modern era,

various actions are attempted by the audit committees in order to assure that the quality of

the audit reports gets improved. The current study would try to evaluate the latest annual

report of CSR Limited based on the various auditing features of the operating statements.

CSR Limited is a famous Australian industrial company engaged in manufacturing building

products (Csr.com.au 2018). In this regard, it requires to be mentioned that Deloitte is the

audit partner of the organisation for the year 2018.

Compliance with the independence requirement of the auditor:

According to the annual report of CSR Limited in 2018, no members of Deloitte were

engaged with the business activities of the company. Besides, no specific staff of the audit

group of Deloitte played a significant role in the group audit of CSR Limited for the year,

which is made under a declaration in accordance with “Section 342A of the Corporations

Act 2001”. On the other hand, Deloitte has complied with all the requirements mentioned

under “Section 307C of the Corporations Act 2001” covering the following points:

1. No violations have been there related to the independence needs of the auditor with

respect to audit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

2. All relevant codes of professional conduct have been performed regarding the audit and

other related activities of CSR Limited.

Non-audit services:

As stated in the annual report of CSR Limited in 2018, it could be noticed that

Deloitte has performed two types of non-audit services to the company. These services

involve sustainability and carbon related ensuring services and other assurance and advisory

services. For these two non-audit services, CSR Limited has paid $77,108 and $9,000

respectively to Deloitte. This has sum is equal to 10.40% of the overall remuneration of the

auditor (Csr.com.au 2018). On the other hand, sufficient compliance is ensured by both the

auditor and the company while performing and receiving the non-audit services.

As per the written advice of the Risk and Audit Committee, the directors have been

contented that the non-audit services performed by Deloitte have been satisfying to the

general independence status for the auditors implied on the part of the Corporations Act

2001. However, such services are performed by not incorporating with the independent

needs of the auditor of the above-stated standard regarding to materiality of the sum,

service features and the methods invented for supervising auditor independence (Duncan,

and Whittington 2014). Thus, the board of Directors of CSR Limited has assured that the

non-audit services do not include re-assessment of the self-work of the auditor for

undertaking management decisions (Yang et al. 2017). Moreover, the company has taken

into consideration all the rules and regulations regarding the corporate governance for the

non-audit services. Therefore, by taking into consideration all these characteristics, the

independence of the auditor could not be questioned (Marques 2018).

2. All relevant codes of professional conduct have been performed regarding the audit and

other related activities of CSR Limited.

Non-audit services:

As stated in the annual report of CSR Limited in 2018, it could be noticed that

Deloitte has performed two types of non-audit services to the company. These services

involve sustainability and carbon related ensuring services and other assurance and advisory

services. For these two non-audit services, CSR Limited has paid $77,108 and $9,000

respectively to Deloitte. This has sum is equal to 10.40% of the overall remuneration of the

auditor (Csr.com.au 2018). On the other hand, sufficient compliance is ensured by both the

auditor and the company while performing and receiving the non-audit services.

As per the written advice of the Risk and Audit Committee, the directors have been

contented that the non-audit services performed by Deloitte have been satisfying to the

general independence status for the auditors implied on the part of the Corporations Act

2001. However, such services are performed by not incorporating with the independent

needs of the auditor of the above-stated standard regarding to materiality of the sum,

service features and the methods invented for supervising auditor independence (Duncan,

and Whittington 2014). Thus, the board of Directors of CSR Limited has assured that the

non-audit services do not include re-assessment of the self-work of the auditor for

undertaking management decisions (Yang et al. 2017). Moreover, the company has taken

into consideration all the rules and regulations regarding the corporate governance for the

non-audit services. Therefore, by taking into consideration all these characteristics, the

independence of the auditor could not be questioned (Marques 2018).

5AUDIT, ASSURANCE AND COMPLIANCE

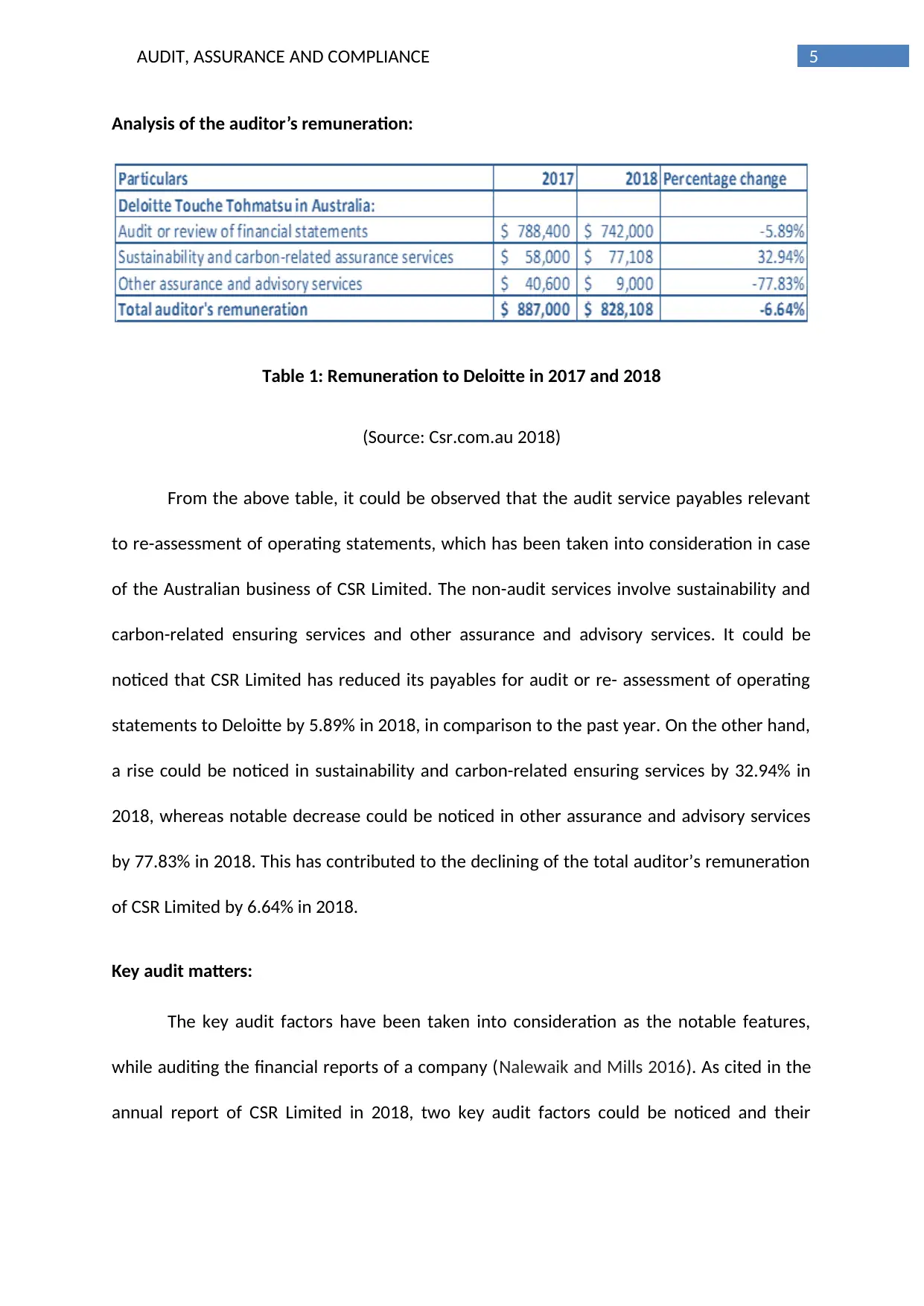

Analysis of the auditor’s remuneration:

Table 1: Remuneration to Deloitte in 2017 and 2018

(Source: Csr.com.au 2018)

From the above table, it could be observed that the audit service payables relevant

to re-assessment of operating statements, which has been taken into consideration in case

of the Australian business of CSR Limited. The non-audit services involve sustainability and

carbon-related ensuring services and other assurance and advisory services. It could be

noticed that CSR Limited has reduced its payables for audit or re- assessment of operating

statements to Deloitte by 5.89% in 2018, in comparison to the past year. On the other hand,

a rise could be noticed in sustainability and carbon-related ensuring services by 32.94% in

2018, whereas notable decrease could be noticed in other assurance and advisory services

by 77.83% in 2018. This has contributed to the declining of the total auditor’s remuneration

of CSR Limited by 6.64% in 2018.

Key audit matters:

The key audit factors have been taken into consideration as the notable features,

while auditing the financial reports of a company (Nalewaik and Mills 2016). As cited in the

annual report of CSR Limited in 2018, two key audit factors could be noticed and their

Analysis of the auditor’s remuneration:

Table 1: Remuneration to Deloitte in 2017 and 2018

(Source: Csr.com.au 2018)

From the above table, it could be observed that the audit service payables relevant

to re-assessment of operating statements, which has been taken into consideration in case

of the Australian business of CSR Limited. The non-audit services involve sustainability and

carbon-related ensuring services and other assurance and advisory services. It could be

noticed that CSR Limited has reduced its payables for audit or re- assessment of operating

statements to Deloitte by 5.89% in 2018, in comparison to the past year. On the other hand,

a rise could be noticed in sustainability and carbon-related ensuring services by 32.94% in

2018, whereas notable decrease could be noticed in other assurance and advisory services

by 77.83% in 2018. This has contributed to the declining of the total auditor’s remuneration

of CSR Limited by 6.64% in 2018.

Key audit matters:

The key audit factors have been taken into consideration as the notable features,

while auditing the financial reports of a company (Nalewaik and Mills 2016). As cited in the

annual report of CSR Limited in 2018, two key audit factors could be noticed and their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

elaborated audit process for reduction and classification have been represented in the

following:

Product liability provision:

A liability catering to a sum of $289 million has been identified by CSR Limited at 31st

March 2018. The provision is regarding the declaration and forecasting of the future claims

related to asbestos. This has been assured after considering the suggestion of an external

specialist appointed by the management in Australia and USA. The provision needs

substantial acumen for settling the sums and the possibilities of the future claims. However,

the predictions regarding the foreign exchange rate shifts and rates of discount have

substantial effect on the estimated provision (Paterson et al. 2016). Furthermore, after all

the predictions vary in size and complex in nature, Deloitte has taken into consideration

product liability catering to the form a key audit factor (Pedersen et al. 2016).

For handling with this problem, Deloitte has evaluated the experience as well as

independence of the external specialist and the appropriateness of the predictions and

processes used in the study. This involves analysing the impactful nature of the utilised

process for calculating the provision, standard of the rates of discount and comparison of

the expertise of historical claims to predictions used for projecting future claims (Schmidt,

Wood and Grabski 2016). However, Deloitte has utilised sample testing for accurate

examination and elimination of claims regarding the asbestos in the liability database of the

management. This is vital for the audit processes, after all the provision is constructed on

the basis of the reports. Thus, the auditor has inspected about the external specialist and

the internal and external legal counsel of the company. Lastly, Deloitte has evaluated the

appropriateness of the relevant declarations in the financial reports.

elaborated audit process for reduction and classification have been represented in the

following:

Product liability provision:

A liability catering to a sum of $289 million has been identified by CSR Limited at 31st

March 2018. The provision is regarding the declaration and forecasting of the future claims

related to asbestos. This has been assured after considering the suggestion of an external

specialist appointed by the management in Australia and USA. The provision needs

substantial acumen for settling the sums and the possibilities of the future claims. However,

the predictions regarding the foreign exchange rate shifts and rates of discount have

substantial effect on the estimated provision (Paterson et al. 2016). Furthermore, after all

the predictions vary in size and complex in nature, Deloitte has taken into consideration

product liability catering to the form a key audit factor (Pedersen et al. 2016).

For handling with this problem, Deloitte has evaluated the experience as well as

independence of the external specialist and the appropriateness of the predictions and

processes used in the study. This involves analysing the impactful nature of the utilised

process for calculating the provision, standard of the rates of discount and comparison of

the expertise of historical claims to predictions used for projecting future claims (Schmidt,

Wood and Grabski 2016). However, Deloitte has utilised sample testing for accurate

examination and elimination of claims regarding the asbestos in the liability database of the

management. This is vital for the audit processes, after all the provision is constructed on

the basis of the reports. Thus, the auditor has inspected about the external specialist and

the internal and external legal counsel of the company. Lastly, Deloitte has evaluated the

appropriateness of the relevant declarations in the financial reports.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

Asset valuation:

As per the annual report of CSR Limited in 2018, it has been noticed that the

company has goodwill amount of $98.1 million, other intangible assets of $45.8 million and

property, plant and equipment of $834 million that take into account a number of money

producing units. In order to carry out the evaluation of the dissimilarities of these asset

balances, considerable judgement is required. Such acumen involves notable predictions

like inflation, discount tasks, estimation of building cycle changes, growth rates and

assumptions of future cash flows (Shafii, Abidin and Salleh 2015). The management of CSR

Limited has constructed a dissimilarity triggering evaluation for indicating those money

producing units to be taken into consideration for further dissimilarities. It has been

recognised that the Viridian money producing unit requires more dissimilarity assessment.

This is because it has earned diminished return on capital employed (Stafford, Deitz and

2018). This has been taken into consideration as a key audit factor because of the acumen

incorporated with the assumption of future cash flows and chosen estimations.

In order to manage this matter, the auditor has evaluated the management process

of CSR Limited for identifying the cash generating units (CGUs), in which further impairment

evaluation is required. Hence, it has assisted in developing an understanding of the

consistency in segmental reporting, outside market situations, financial health of the year

and apportionment of goodwill to all CGUs for testing impairment. In addition, the

methodology associated with the impairment model as well as assumptions are evaluated

appropriately while bearing in mind various influential dynamics. Furthermore, Deloitte is

observed to use sample testing so that the cash flow models could be checked for accuracy

Asset valuation:

As per the annual report of CSR Limited in 2018, it has been noticed that the

company has goodwill amount of $98.1 million, other intangible assets of $45.8 million and

property, plant and equipment of $834 million that take into account a number of money

producing units. In order to carry out the evaluation of the dissimilarities of these asset

balances, considerable judgement is required. Such acumen involves notable predictions

like inflation, discount tasks, estimation of building cycle changes, growth rates and

assumptions of future cash flows (Shafii, Abidin and Salleh 2015). The management of CSR

Limited has constructed a dissimilarity triggering evaluation for indicating those money

producing units to be taken into consideration for further dissimilarities. It has been

recognised that the Viridian money producing unit requires more dissimilarity assessment.

This is because it has earned diminished return on capital employed (Stafford, Deitz and

2018). This has been taken into consideration as a key audit factor because of the acumen

incorporated with the assumption of future cash flows and chosen estimations.

In order to manage this matter, the auditor has evaluated the management process

of CSR Limited for identifying the cash generating units (CGUs), in which further impairment

evaluation is required. Hence, it has assisted in developing an understanding of the

consistency in segmental reporting, outside market situations, financial health of the year

and apportionment of goodwill to all CGUs for testing impairment. In addition, the

methodology associated with the impairment model as well as assumptions are evaluated

appropriately while bearing in mind various influential dynamics. Furthermore, Deloitte is

observed to use sample testing so that the cash flow models could be checked for accuracy

8AUDIT, ASSURANCE AND COMPLIANCE

(Kend 2015). Therefore, the auditor has considered all the accounting related impairment

disclosures from the annual report of CSR Limited in 2018.

Audit committee:

As apparent from the latest annual report of CSR Limited, a risk and audit committee

is established that would govern the various internal control guidelines in order to shield

company liabilities and assets. Moreover, the committee would be responsible to assure

that the financial reporting guidelines are maintained with integrity. The committee consists

of four non-executive directors and they are listed as follows:

Mike Ihlein

John Gillam

Penny Winn

Matthew Quinn

These personnel along with the other members of the committee look after the

evaluation of the different processes to ensure that integrity is maintained within financial

reporting. Moreover, they also assess the factors needed to recognise commercial incomes

and framework evaluation of audit risk management (Kend, Houghton and Jubb 2014). The

organisation does not have any audit committee charter, as no evidences could be gathered

about the same in its financial reports.

Audit opinion:

CSR Limited has the independent auditor’s report, in which it has been clearly

mentioned that it has followed the Corporations Act 2001 to develop its remuneration

report by adhering to the guidelines mentioned in “Section 300A of the Act”. In addition, the

(Kend 2015). Therefore, the auditor has considered all the accounting related impairment

disclosures from the annual report of CSR Limited in 2018.

Audit committee:

As apparent from the latest annual report of CSR Limited, a risk and audit committee

is established that would govern the various internal control guidelines in order to shield

company liabilities and assets. Moreover, the committee would be responsible to assure

that the financial reporting guidelines are maintained with integrity. The committee consists

of four non-executive directors and they are listed as follows:

Mike Ihlein

John Gillam

Penny Winn

Matthew Quinn

These personnel along with the other members of the committee look after the

evaluation of the different processes to ensure that integrity is maintained within financial

reporting. Moreover, they also assess the factors needed to recognise commercial incomes

and framework evaluation of audit risk management (Kend, Houghton and Jubb 2014). The

organisation does not have any audit committee charter, as no evidences could be gathered

about the same in its financial reports.

Audit opinion:

CSR Limited has the independent auditor’s report, in which it has been clearly

mentioned that it has followed the Corporations Act 2001 to develop its remuneration

report by adhering to the guidelines mentioned in “Section 300A of the Act”. In addition, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

other accounting standards laid down in AASB, IFRS and IASB are followed as well. The

auditor has stated that no material misstatements are apparent in the financial reports of

CSR Limited and hence, no distortions are made in representing the financial condition of

the organisation that would affect the users of the financial statements in undertaking

decisions. This implies unqualified audit opinion was expressed by Deloitte after it has

audited its financial statements accompanied by supporting notes so that their

appropriateness could be tested.

Variations between accountabilities of the management, directors and auditors:

As observed from the latest annual report of the organisation, the roles of the

management and directors vary greatly from those of the auditors at the time of financial

report presentation and preparation. Both management and directors are needed to bear

into mind the accounting rules and guidelines of the nation at the time of preparing financial

statements and they need to assess whether the organisation is capable enough of

continuing as going concern by applying the appropriate accounting bases.

Conversely, the auditors do not carry out the same roles as those of the

management and directors (Kend, Houghton and Jubb 2014). The primary responsibility of

the auditors is to check whether any material misstatements prevail in the financial reports

because of illicit practices, errors or others based on which they would issue their opinion.

Deloitte has carried out the following accountabilities while the auditing the financial

reports of CSR Limited:

Discovering and dissecting material misstatement risks

Knowledge about the procedures of internal control

Checking the effectiveness of accounting processes

other accounting standards laid down in AASB, IFRS and IASB are followed as well. The

auditor has stated that no material misstatements are apparent in the financial reports of

CSR Limited and hence, no distortions are made in representing the financial condition of

the organisation that would affect the users of the financial statements in undertaking

decisions. This implies unqualified audit opinion was expressed by Deloitte after it has

audited its financial statements accompanied by supporting notes so that their

appropriateness could be tested.

Variations between accountabilities of the management, directors and auditors:

As observed from the latest annual report of the organisation, the roles of the

management and directors vary greatly from those of the auditors at the time of financial

report presentation and preparation. Both management and directors are needed to bear

into mind the accounting rules and guidelines of the nation at the time of preparing financial

statements and they need to assess whether the organisation is capable enough of

continuing as going concern by applying the appropriate accounting bases.

Conversely, the auditors do not carry out the same roles as those of the

management and directors (Kend, Houghton and Jubb 2014). The primary responsibility of

the auditors is to check whether any material misstatements prevail in the financial reports

because of illicit practices, errors or others based on which they would issue their opinion.

Deloitte has carried out the following accountabilities while the auditing the financial

reports of CSR Limited:

Discovering and dissecting material misstatement risks

Knowledge about the procedures of internal control

Checking the effectiveness of accounting processes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

Judging whether CSR Limited has applied appropriate recognition bases for operating

as a going concern

Reviewing whether the financial statements are prepared and depicted accurately

Accumulation of considerable evidence for audit functions (Knechel and Salterio

2016)

Material subsequent events:

Two material subsequent events are deemed to be identified from the annual report

of CSR Limited. One of them is sale of a surplus asset and another is associated with

declaration of dividend. The organisation has announced that it would dispose-off its Hosley

Park excess land, which is situated in New South Wales on April 3, 2018. From sales

agreement, it is estimated that recognition of $30 million profit would be realised in profit

and loss statement before tax deduction in the next year’s annual report. This is because the

sale would be conducted in April, 2019. In 2018, it has declared a dividend of $0.135 per

share, which is fully-franked and the total dividend payment is expected at $68.1 million,

which should be settled on July 3, 2018. However, the dividend amount is not distributed

yet among the shareholders of the organisation.

Appropriateness of material information:

When this situation is analysed by positioning as a third party stakeholder, the

members of Deloitte involved in audit work of CSR Limited have made thorough analysis of

material information of the organisation in the most responsible manner. They have

conformed to the necessary standards mentioned in APES 110, Australian standards for

auditing, IFRS, IASB, Corporations Act 2001 and others. Along with this, the auditors have

identified two events, which are treated as key audit matters and hence, the risks expected

Judging whether CSR Limited has applied appropriate recognition bases for operating

as a going concern

Reviewing whether the financial statements are prepared and depicted accurately

Accumulation of considerable evidence for audit functions (Knechel and Salterio

2016)

Material subsequent events:

Two material subsequent events are deemed to be identified from the annual report

of CSR Limited. One of them is sale of a surplus asset and another is associated with

declaration of dividend. The organisation has announced that it would dispose-off its Hosley

Park excess land, which is situated in New South Wales on April 3, 2018. From sales

agreement, it is estimated that recognition of $30 million profit would be realised in profit

and loss statement before tax deduction in the next year’s annual report. This is because the

sale would be conducted in April, 2019. In 2018, it has declared a dividend of $0.135 per

share, which is fully-franked and the total dividend payment is expected at $68.1 million,

which should be settled on July 3, 2018. However, the dividend amount is not distributed

yet among the shareholders of the organisation.

Appropriateness of material information:

When this situation is analysed by positioning as a third party stakeholder, the

members of Deloitte involved in audit work of CSR Limited have made thorough analysis of

material information of the organisation in the most responsible manner. They have

conformed to the necessary standards mentioned in APES 110, Australian standards for

auditing, IFRS, IASB, Corporations Act 2001 and others. Along with this, the auditors have

identified two events, which are treated as key audit matters and hence, the risks expected

11AUDIT, ASSURANCE AND COMPLIANCE

to arise from these events are to be mitigated supported by relevant recommendations.

Hence, all these aspects together clearly state that Deloitte has performed all the necessary

audit-related work to identify and analyse material information laid out in the financial

reports of the organisation (Knechel 2016).

Missing or undisclosed material information:

As per the latest annual report of CSR Limited, Deloitte has performed all the

necessary functions needed to analyse the material aspects as well other information that

have the possibility of developing material misstatement risk in terms of financial reporting.

Moreover, it has provided explanation of the reasons behind why certain events are

considered to have material factors. Hence, it could be said that no material information is

excluded or missing materiality aspects (Louwers et al. 2015).

Follow-up questions:

Certain questions could be raised for the auditor at the annual general meeting. In

this case, it would be Deloitte, since it has audited the financial statements of CSR Limited in

2018. Some of the important follow-up questions that could be put forth in front of Deloitte

include the following:

Are you engaged in discussion of any accounting issues with management before

discussion?

How have you planned the scope of your audit work?

Is your audit scope effective enough to detect material errors and unethical

practices?

to arise from these events are to be mitigated supported by relevant recommendations.

Hence, all these aspects together clearly state that Deloitte has performed all the necessary

audit-related work to identify and analyse material information laid out in the financial

reports of the organisation (Knechel 2016).

Missing or undisclosed material information:

As per the latest annual report of CSR Limited, Deloitte has performed all the

necessary functions needed to analyse the material aspects as well other information that

have the possibility of developing material misstatement risk in terms of financial reporting.

Moreover, it has provided explanation of the reasons behind why certain events are

considered to have material factors. Hence, it could be said that no material information is

excluded or missing materiality aspects (Louwers et al. 2015).

Follow-up questions:

Certain questions could be raised for the auditor at the annual general meeting. In

this case, it would be Deloitte, since it has audited the financial statements of CSR Limited in

2018. Some of the important follow-up questions that could be put forth in front of Deloitte

include the following:

Are you engaged in discussion of any accounting issues with management before

discussion?

How have you planned the scope of your audit work?

Is your audit scope effective enough to detect material errors and unethical

practices?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.