Audit and Assurance: Procedures, Deficiencies, and Financial Ratios

VerifiedAdded on 2023/06/18

|7

|1756

|497

Homework Assignment

AI Summary

This assignment solution covers key aspects of audit and assurance, including substantive procedures for machinery additions and disposals, inventory valuation, and going concern assessments. It also addresses control deficiencies within a company's order processing system, recommending improvements to enhance accuracy and efficiency. Furthermore, the solution analyzes financial ratios such as gross profit margin, interest cover, receivable days, and payable days to assess a company's financial performance and identifies potential audit risks related to new machinery purchases, training costs, changes in payable days, share issuances, and revenue recognition. Finally, it outlines procedures for addressing redundancy costs, including reviewing board minutes, obtaining redundancy calculations, and ensuring compliance with accounting standards. Desklib provides access to a wide range of solved assignments and study resources for students.

Audit and Assurance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Q1...............................................................................................................................................3

a..............................................................................................................................................3

b..............................................................................................................................................3

c..............................................................................................................................................4

Q2...............................................................................................................................................4

a..............................................................................................................................................4

b..............................................................................................................................................5

Q3...............................................................................................................................................5

a..............................................................................................................................................5

b..............................................................................................................................................6

c..............................................................................................................................................7

Q1...............................................................................................................................................3

a..............................................................................................................................................3

b..............................................................................................................................................3

c..............................................................................................................................................4

Q2...............................................................................................................................................4

a..............................................................................................................................................4

b..............................................................................................................................................5

Q3...............................................................................................................................................5

a..............................................................................................................................................5

b..............................................................................................................................................6

c..............................................................................................................................................7

Q1

a.

Five substantive procedures which auditors of Jack Co should perform in relation to the

machinery additions and disposals in order to obtain sufficient and appropriate audit evidence

are given below:

Obtaining the breakdown of additions, derive the list and along with it agree to the

non-current asset register in order to confirm the completeness of the machinery.

Select the sample of the additions made and match it with the agreed cost to supplier

invoice with the objective to confirm valuation.

Review the board minutes to ensure that significant capital expenditure purchases

have been authorised by the board.

Obtain a breakdown of disposals, cast the list and agree all assets removed from the

non-current asset register to confirm existence.

Recalculate the profit/loss on disposal and agree to the income statement.

b.

Five substantive procedures which auditors of Charlie Co. should conducted for obtaining the

sufficient and appropriate audit evidence pertaining to the inventory of Charlie Co. are

described below.

Obtaining the schedule for the raw materials, finished goods and the WIP inventory

and then cast to make a confirmation about the completeness and accuracy of the

balance and agree to trial balance and financial statements.

Review aged inventory reports and identify any slow moving goods and also having a

discussion with the management why these items have not been written down or if an

allowance is required.

In respect to quality issue in the products manufactured, discuss the same with the

management about their plans of disposing this off and reason they believe that the

goods are having the cost of $900,000. It should be supported with proper

documentation with breakdown of raw material cost, labour cost and any overheads

attributed to the cost.

Confirm that the final adjustment for the goods is $200,000 and discuss with

management if this adjustment has been made; if so, follow through the write down to

confirm.

a.

Five substantive procedures which auditors of Jack Co should perform in relation to the

machinery additions and disposals in order to obtain sufficient and appropriate audit evidence

are given below:

Obtaining the breakdown of additions, derive the list and along with it agree to the

non-current asset register in order to confirm the completeness of the machinery.

Select the sample of the additions made and match it with the agreed cost to supplier

invoice with the objective to confirm valuation.

Review the board minutes to ensure that significant capital expenditure purchases

have been authorised by the board.

Obtain a breakdown of disposals, cast the list and agree all assets removed from the

non-current asset register to confirm existence.

Recalculate the profit/loss on disposal and agree to the income statement.

b.

Five substantive procedures which auditors of Charlie Co. should conducted for obtaining the

sufficient and appropriate audit evidence pertaining to the inventory of Charlie Co. are

described below.

Obtaining the schedule for the raw materials, finished goods and the WIP inventory

and then cast to make a confirmation about the completeness and accuracy of the

balance and agree to trial balance and financial statements.

Review aged inventory reports and identify any slow moving goods and also having a

discussion with the management why these items have not been written down or if an

allowance is required.

In respect to quality issue in the products manufactured, discuss the same with the

management about their plans of disposing this off and reason they believe that the

goods are having the cost of $900,000. It should be supported with proper

documentation with breakdown of raw material cost, labour cost and any overheads

attributed to the cost.

Confirm that the final adjustment for the goods is $200,000 and discuss with

management if this adjustment has been made; if so, follow through the write down to

confirm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Review the financial statements disclosures in regard to the inventory and WIP to

ensure they comply with relevant accounting standards.

c.

Audit procedures for assessing going concern

Acquire the firm’s cash flow forecast and review the cash flows. Assess the

assumptions for reasonableness and discuss the findings with management to

understand if the company will have sufficient cash flows.

Review any contract or agreement with the bank to determine whether any other

covenants have been breached, mainly in association with the bank overdraft

facilities.

Review the company’s post year-end sales and order book to assess the levels of trade

and if the revenue figures in the cash flow forecast are reasonable.

Carrying out the sensitivity analysis of the cash flows which will help in knowing the

margin of safety of the company pertaining to the cash inflows and outflows.

Having a discussion with the finance director or CFO in order to know whether sales

director is being replaced or the new customer base is being generated.

Q2.

a.

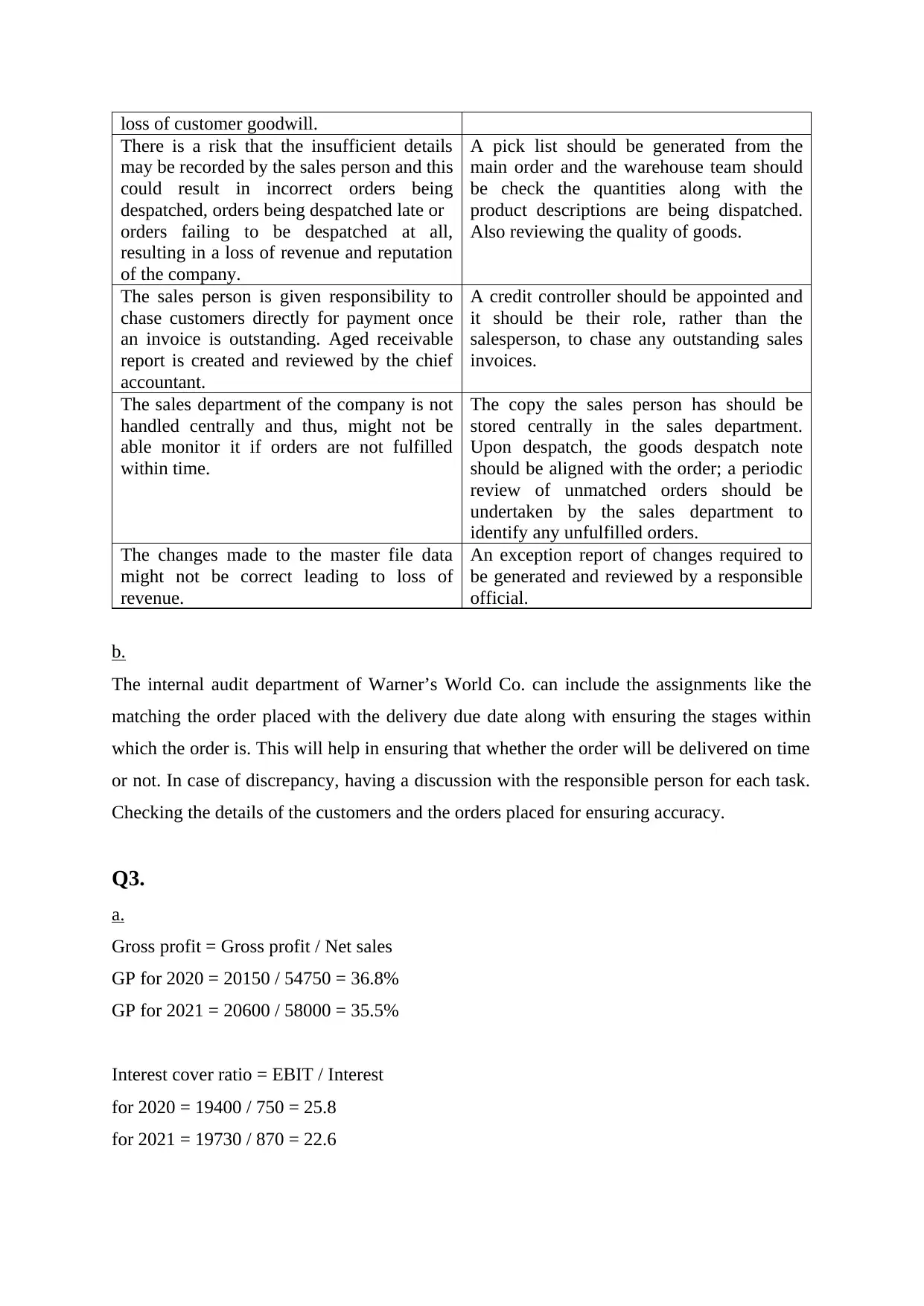

Control deficiency Control Recommendations

The customer orders are basically recorded

in the 2 parts, so one copy is left with the

customer and other with the sales person.

The order form should be recorded into at

least 4 parts. The third part of the order

should be sent to the warehouse while the

4th should be sent to the finance department.

Sales staff can make changes to the

customer master data file, in order to record

discounts allowed and these changes are not

reviewed.

The sales staff should not be having an

access to the master data file to making

changes. Such changes should be restricted

to the sales director.

There is a risk that goods might not be

available and the customers not aware of

this prior to placing an order might lead to

unfulfilled orders and customer

dissatisfaction, which would impact the

company’s reputation.

Before the salesperson finalize the order, the

inventory system should be checked in order

to make sure the availability of goods to be

notified to the customers.

Customer orders are given a number

automatically by the system which is not

reviewed. In case of system error, it is

difficult for company to identify missing

orders and to monitor if all orders are being

despatched in a timely manner, leading to a

Thus, timely monitoring of the order

number should be implemented which will

help in finding out any missing orders.

ensure they comply with relevant accounting standards.

c.

Audit procedures for assessing going concern

Acquire the firm’s cash flow forecast and review the cash flows. Assess the

assumptions for reasonableness and discuss the findings with management to

understand if the company will have sufficient cash flows.

Review any contract or agreement with the bank to determine whether any other

covenants have been breached, mainly in association with the bank overdraft

facilities.

Review the company’s post year-end sales and order book to assess the levels of trade

and if the revenue figures in the cash flow forecast are reasonable.

Carrying out the sensitivity analysis of the cash flows which will help in knowing the

margin of safety of the company pertaining to the cash inflows and outflows.

Having a discussion with the finance director or CFO in order to know whether sales

director is being replaced or the new customer base is being generated.

Q2.

a.

Control deficiency Control Recommendations

The customer orders are basically recorded

in the 2 parts, so one copy is left with the

customer and other with the sales person.

The order form should be recorded into at

least 4 parts. The third part of the order

should be sent to the warehouse while the

4th should be sent to the finance department.

Sales staff can make changes to the

customer master data file, in order to record

discounts allowed and these changes are not

reviewed.

The sales staff should not be having an

access to the master data file to making

changes. Such changes should be restricted

to the sales director.

There is a risk that goods might not be

available and the customers not aware of

this prior to placing an order might lead to

unfulfilled orders and customer

dissatisfaction, which would impact the

company’s reputation.

Before the salesperson finalize the order, the

inventory system should be checked in order

to make sure the availability of goods to be

notified to the customers.

Customer orders are given a number

automatically by the system which is not

reviewed. In case of system error, it is

difficult for company to identify missing

orders and to monitor if all orders are being

despatched in a timely manner, leading to a

Thus, timely monitoring of the order

number should be implemented which will

help in finding out any missing orders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

loss of customer goodwill.

There is a risk that the insufficient details

may be recorded by the sales person and this

could result in incorrect orders being

despatched, orders being despatched late or

orders failing to be despatched at all,

resulting in a loss of revenue and reputation

of the company.

A pick list should be generated from the

main order and the warehouse team should

be check the quantities along with the

product descriptions are being dispatched.

Also reviewing the quality of goods.

The sales person is given responsibility to

chase customers directly for payment once

an invoice is outstanding. Aged receivable

report is created and reviewed by the chief

accountant.

A credit controller should be appointed and

it should be their role, rather than the

salesperson, to chase any outstanding sales

invoices.

The sales department of the company is not

handled centrally and thus, might not be

able monitor it if orders are not fulfilled

within time.

The copy the sales person has should be

stored centrally in the sales department.

Upon despatch, the goods despatch note

should be aligned with the order; a periodic

review of unmatched orders should be

undertaken by the sales department to

identify any unfulfilled orders.

The changes made to the master file data

might not be correct leading to loss of

revenue.

An exception report of changes required to

be generated and reviewed by a responsible

official.

b.

The internal audit department of Warner’s World Co. can include the assignments like the

matching the order placed with the delivery due date along with ensuring the stages within

which the order is. This will help in ensuring that whether the order will be delivered on time

or not. In case of discrepancy, having a discussion with the responsible person for each task.

Checking the details of the customers and the orders placed for ensuring accuracy.

Q3.

a.

Gross profit = Gross profit / Net sales

GP for 2020 = 20150 / 54750 = 36.8%

GP for 2021 = 20600 / 58000 = 35.5%

Interest cover ratio = EBIT / Interest

for 2020 = 19400 / 750 = 25.8

for 2021 = 19730 / 870 = 22.6

There is a risk that the insufficient details

may be recorded by the sales person and this

could result in incorrect orders being

despatched, orders being despatched late or

orders failing to be despatched at all,

resulting in a loss of revenue and reputation

of the company.

A pick list should be generated from the

main order and the warehouse team should

be check the quantities along with the

product descriptions are being dispatched.

Also reviewing the quality of goods.

The sales person is given responsibility to

chase customers directly for payment once

an invoice is outstanding. Aged receivable

report is created and reviewed by the chief

accountant.

A credit controller should be appointed and

it should be their role, rather than the

salesperson, to chase any outstanding sales

invoices.

The sales department of the company is not

handled centrally and thus, might not be

able monitor it if orders are not fulfilled

within time.

The copy the sales person has should be

stored centrally in the sales department.

Upon despatch, the goods despatch note

should be aligned with the order; a periodic

review of unmatched orders should be

undertaken by the sales department to

identify any unfulfilled orders.

The changes made to the master file data

might not be correct leading to loss of

revenue.

An exception report of changes required to

be generated and reviewed by a responsible

official.

b.

The internal audit department of Warner’s World Co. can include the assignments like the

matching the order placed with the delivery due date along with ensuring the stages within

which the order is. This will help in ensuring that whether the order will be delivered on time

or not. In case of discrepancy, having a discussion with the responsible person for each task.

Checking the details of the customers and the orders placed for ensuring accuracy.

Q3.

a.

Gross profit = Gross profit / Net sales

GP for 2020 = 20150 / 54750 = 36.8%

GP for 2021 = 20600 / 58000 = 35.5%

Interest cover ratio = EBIT / Interest

for 2020 = 19400 / 750 = 25.8

for 2021 = 19730 / 870 = 22.6

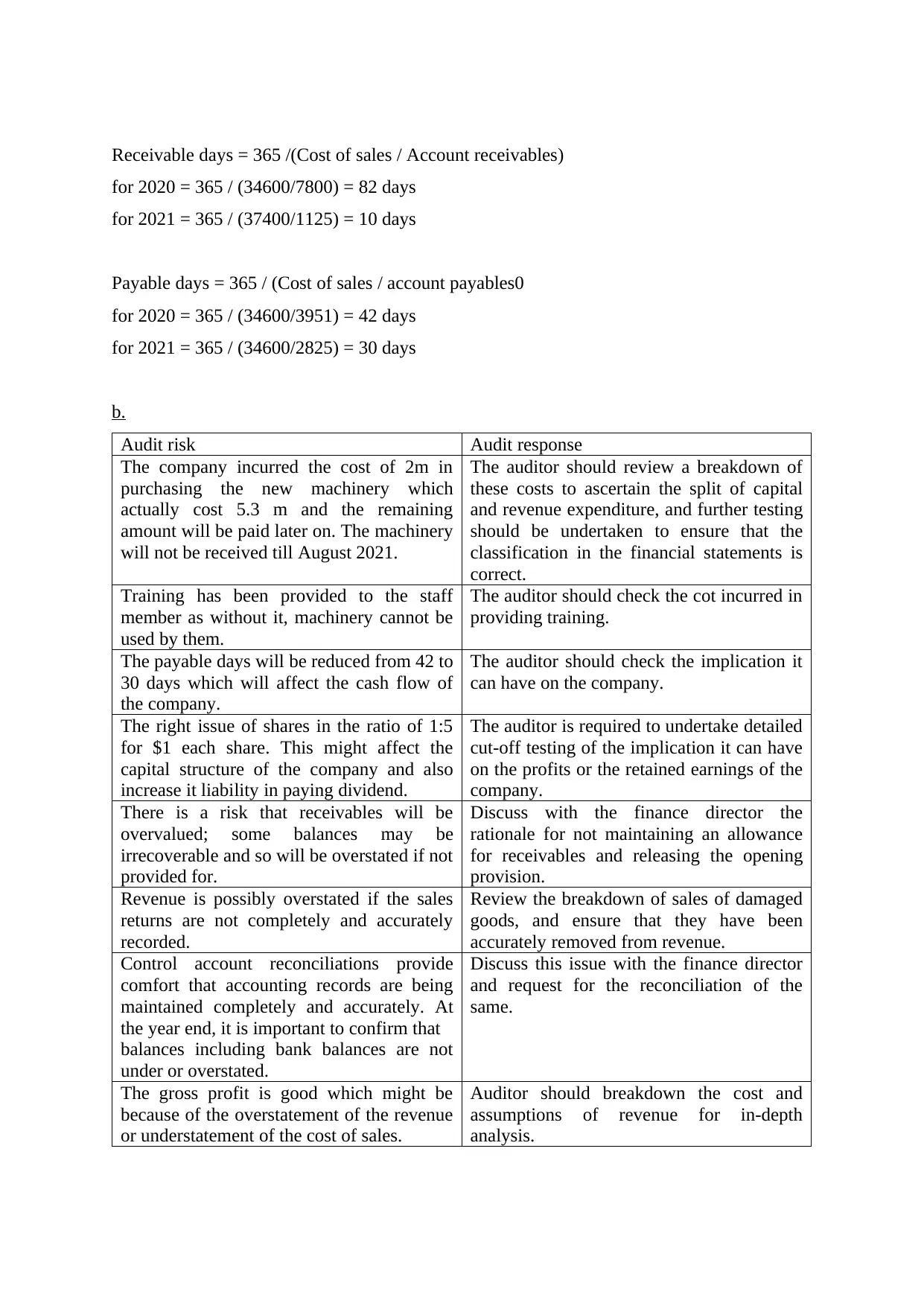

Receivable days = 365 /(Cost of sales / Account receivables)

for 2020 = 365 / (34600/7800) = 82 days

for 2021 = 365 / (37400/1125) = 10 days

Payable days = 365 / (Cost of sales / account payables0

for 2020 = 365 / (34600/3951) = 42 days

for 2021 = 365 / (34600/2825) = 30 days

b.

Audit risk Audit response

The company incurred the cost of 2m in

purchasing the new machinery which

actually cost 5.3 m and the remaining

amount will be paid later on. The machinery

will not be received till August 2021.

The auditor should review a breakdown of

these costs to ascertain the split of capital

and revenue expenditure, and further testing

should be undertaken to ensure that the

classification in the financial statements is

correct.

Training has been provided to the staff

member as without it, machinery cannot be

used by them.

The auditor should check the cot incurred in

providing training.

The payable days will be reduced from 42 to

30 days which will affect the cash flow of

the company.

The auditor should check the implication it

can have on the company.

The right issue of shares in the ratio of 1:5

for $1 each share. This might affect the

capital structure of the company and also

increase it liability in paying dividend.

The auditor is required to undertake detailed

cut-off testing of the implication it can have

on the profits or the retained earnings of the

company.

There is a risk that receivables will be

overvalued; some balances may be

irrecoverable and so will be overstated if not

provided for.

Discuss with the finance director the

rationale for not maintaining an allowance

for receivables and releasing the opening

provision.

Revenue is possibly overstated if the sales

returns are not completely and accurately

recorded.

Review the breakdown of sales of damaged

goods, and ensure that they have been

accurately removed from revenue.

Control account reconciliations provide

comfort that accounting records are being

maintained completely and accurately. At

the year end, it is important to confirm that

balances including bank balances are not

under or overstated.

Discuss this issue with the finance director

and request for the reconciliation of the

same.

The gross profit is good which might be

because of the overstatement of the revenue

or understatement of the cost of sales.

Auditor should breakdown the cost and

assumptions of revenue for in-depth

analysis.

for 2020 = 365 / (34600/7800) = 82 days

for 2021 = 365 / (37400/1125) = 10 days

Payable days = 365 / (Cost of sales / account payables0

for 2020 = 365 / (34600/3951) = 42 days

for 2021 = 365 / (34600/2825) = 30 days

b.

Audit risk Audit response

The company incurred the cost of 2m in

purchasing the new machinery which

actually cost 5.3 m and the remaining

amount will be paid later on. The machinery

will not be received till August 2021.

The auditor should review a breakdown of

these costs to ascertain the split of capital

and revenue expenditure, and further testing

should be undertaken to ensure that the

classification in the financial statements is

correct.

Training has been provided to the staff

member as without it, machinery cannot be

used by them.

The auditor should check the cot incurred in

providing training.

The payable days will be reduced from 42 to

30 days which will affect the cash flow of

the company.

The auditor should check the implication it

can have on the company.

The right issue of shares in the ratio of 1:5

for $1 each share. This might affect the

capital structure of the company and also

increase it liability in paying dividend.

The auditor is required to undertake detailed

cut-off testing of the implication it can have

on the profits or the retained earnings of the

company.

There is a risk that receivables will be

overvalued; some balances may be

irrecoverable and so will be overstated if not

provided for.

Discuss with the finance director the

rationale for not maintaining an allowance

for receivables and releasing the opening

provision.

Revenue is possibly overstated if the sales

returns are not completely and accurately

recorded.

Review the breakdown of sales of damaged

goods, and ensure that they have been

accurately removed from revenue.

Control account reconciliations provide

comfort that accounting records are being

maintained completely and accurately. At

the year end, it is important to confirm that

balances including bank balances are not

under or overstated.

Discuss this issue with the finance director

and request for the reconciliation of the

same.

The gross profit is good which might be

because of the overstatement of the revenue

or understatement of the cost of sales.

Auditor should breakdown the cost and

assumptions of revenue for in-depth

analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

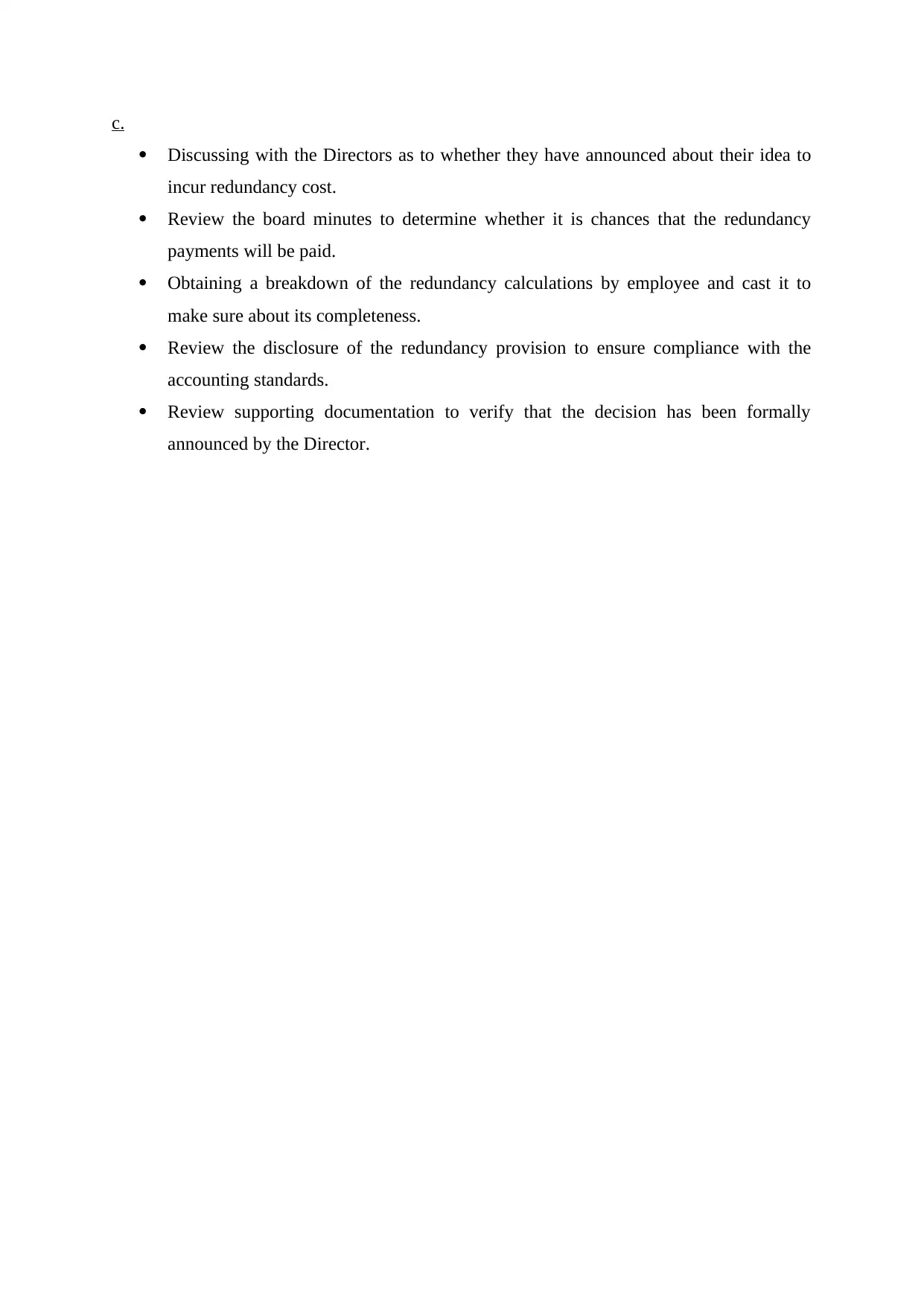

c.

Discussing with the Directors as to whether they have announced about their idea to

incur redundancy cost.

Review the board minutes to determine whether it is chances that the redundancy

payments will be paid.

Obtaining a breakdown of the redundancy calculations by employee and cast it to

make sure about its completeness.

Review the disclosure of the redundancy provision to ensure compliance with the

accounting standards.

Review supporting documentation to verify that the decision has been formally

announced by the Director.

Discussing with the Directors as to whether they have announced about their idea to

incur redundancy cost.

Review the board minutes to determine whether it is chances that the redundancy

payments will be paid.

Obtaining a breakdown of the redundancy calculations by employee and cast it to

make sure about its completeness.

Review the disclosure of the redundancy provision to ensure compliance with the

accounting standards.

Review supporting documentation to verify that the decision has been formally

announced by the Director.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.