Audit and Assurance in Australia: DIPL Case Study Report

VerifiedAdded on 2020/02/24

|12

|3074

|42

Report

AI Summary

This report provides an in-depth analysis of an audit and assurance case study, focusing on Double Pink Printers Ltd (DIPL). It begins by examining the importance of analytical procedures in audit planning, highlighting the use of ratio analysis (current, profit margin, and solvency ratios) and benchmarking to assess financial performance. The report identifies key financial and IT-related risks faced by DIPL, including financial risks like solvency issues and misstatements, and IT risks stemming from inadequate IT controls and software integration. Furthermore, it explores fraudulent risks, particularly those related to employee discontent and the implementation of new accounting systems. The report also discusses risks associated with financial reporting. Overall, the report offers a comprehensive overview of the audit process, risk assessment, and financial reporting challenges within the context of the DIPL case study.

Running head: AUDIT AND ASSURANCE IN AUSTRALIA

Audit and Assurance in Australia

Name of the Student:

Name of the University:

Author’s Note:

Audit and Assurance in Australia

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT AND ASSURANCE IN AUSTRALIA

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to Question No 2................................................................................................................5

Answer to Question No 3................................................................................................................7

Answer to Question No 3 (a).......................................................................................................7

Answer to Question 3 (b).............................................................................................................9

Reference List................................................................................................................................10

AUDIT AND ASSURANCE IN AUSTRALIA

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to Question No 2................................................................................................................5

Answer to Question No 3................................................................................................................7

Answer to Question No 3 (a).......................................................................................................7

Answer to Question 3 (b).............................................................................................................9

Reference List................................................................................................................................10

2

AUDIT AND ASSURANCE IN AUSTRALIA

Answer to Question No 1

The analytical process has supreme importance for the assessment and review of the

financial data that has been gathered from the financial statements of the company under

consideration. During the time of constructing the plan of audit for Double Pink Printers Ltd

(DIPL), the analytical mechanism of financial data is regarded as the most appropriate and

cherished component. It requires to be cited that the audit plan of the organizations gives

essential path and direction to the auditors while undertaking the process of audit during a

specified time period. With the help of a distinct note, the audit plan aids the auditors to keep

track of the audit costs in order to restrict any miscommunication and misunderstanding with the

clients who require audit (Hardy 2014).

The analytical process of the financial data of DIPL answers to the method of scattering

the financial data from various types of financial disclosures of the firm. It is even seen that there

are various categories of techniques that aids in carrying out the analytical mechanism of the

financial data. By taking help of the analytical process for the examination of the financial data,

the accountants and the managers of finance of the firm exploits this data so that effective and

several types of decisions with respect to accounting and finance can be undertaken.

Furthermore, by taking help of the general sized analytical approach of the financial data, the

finance managers of the organizations gain the authority to dichotomize the financial disclosures

of the firm from various financial insights (Kend et al., 2014). It has been observed that one of

the significant advantages of this is that it aids to give out assistance for the construction of the

financial statements and undertake a comparison of the financial statements of the firms for the

last three accounting years.

AUDIT AND ASSURANCE IN AUSTRALIA

Answer to Question No 1

The analytical process has supreme importance for the assessment and review of the

financial data that has been gathered from the financial statements of the company under

consideration. During the time of constructing the plan of audit for Double Pink Printers Ltd

(DIPL), the analytical mechanism of financial data is regarded as the most appropriate and

cherished component. It requires to be cited that the audit plan of the organizations gives

essential path and direction to the auditors while undertaking the process of audit during a

specified time period. With the help of a distinct note, the audit plan aids the auditors to keep

track of the audit costs in order to restrict any miscommunication and misunderstanding with the

clients who require audit (Hardy 2014).

The analytical process of the financial data of DIPL answers to the method of scattering

the financial data from various types of financial disclosures of the firm. It is even seen that there

are various categories of techniques that aids in carrying out the analytical mechanism of the

financial data. By taking help of the analytical process for the examination of the financial data,

the accountants and the managers of finance of the firm exploits this data so that effective and

several types of decisions with respect to accounting and finance can be undertaken.

Furthermore, by taking help of the general sized analytical approach of the financial data, the

finance managers of the organizations gain the authority to dichotomize the financial disclosures

of the firm from various financial insights (Kend et al., 2014). It has been observed that one of

the significant advantages of this is that it aids to give out assistance for the construction of the

financial statements and undertake a comparison of the financial statements of the firms for the

last three accounting years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT AND ASSURANCE IN AUSTRALIA

By taking help of the analytical process, the finance managers of the organizations can exploit

the financial information from the financial statements and they can authenticate the method of

financial broadcasting of the highlighted data. For instance, the process of financial reporting of

the net liabilities and the owner of the equity can be deliberated in this respect along with the

excursion of the data (Moroney et al., 2014). It requires to be cited that benchmarking has been

taken as the chief analytical process of financial data and it can be exploited for the construction

of the audit plan of the company.

By taking help of the process of benchmarking, the finance managers can recognise the

modifications in the financial statements of the organizations. Furthermore, the actual factor of

these alterations along with their core factors can be recognised. Along with the method

benchmarking, ratio analysis is regarded as a crucial analytical process of the financial data

(Min, & Lv 2017). The method of ratio analysis aids in the construction of the audit plan by

undertaking a comparison of the financial reports of more than one organization.

Explanation:

With respect to the case study, the implemented analytical process has a significant

impact on the construction of the audit plan. Additionally, it even has the significance in

distributing the financial data within several accounting and financial departments of the firm.

The following ratios can be constructed as these are a part of the analytical technique.

AUDIT AND ASSURANCE IN AUSTRALIA

By taking help of the analytical process, the finance managers of the organizations can exploit

the financial information from the financial statements and they can authenticate the method of

financial broadcasting of the highlighted data. For instance, the process of financial reporting of

the net liabilities and the owner of the equity can be deliberated in this respect along with the

excursion of the data (Moroney et al., 2014). It requires to be cited that benchmarking has been

taken as the chief analytical process of financial data and it can be exploited for the construction

of the audit plan of the company.

By taking help of the process of benchmarking, the finance managers can recognise the

modifications in the financial statements of the organizations. Furthermore, the actual factor of

these alterations along with their core factors can be recognised. Along with the method

benchmarking, ratio analysis is regarded as a crucial analytical process of the financial data

(Min, & Lv 2017). The method of ratio analysis aids in the construction of the audit plan by

undertaking a comparison of the financial reports of more than one organization.

Explanation:

With respect to the case study, the implemented analytical process has a significant

impact on the construction of the audit plan. Additionally, it even has the significance in

distributing the financial data within several accounting and financial departments of the firm.

The following ratios can be constructed as these are a part of the analytical technique.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT AND ASSURANCE IN AUSTRALIA

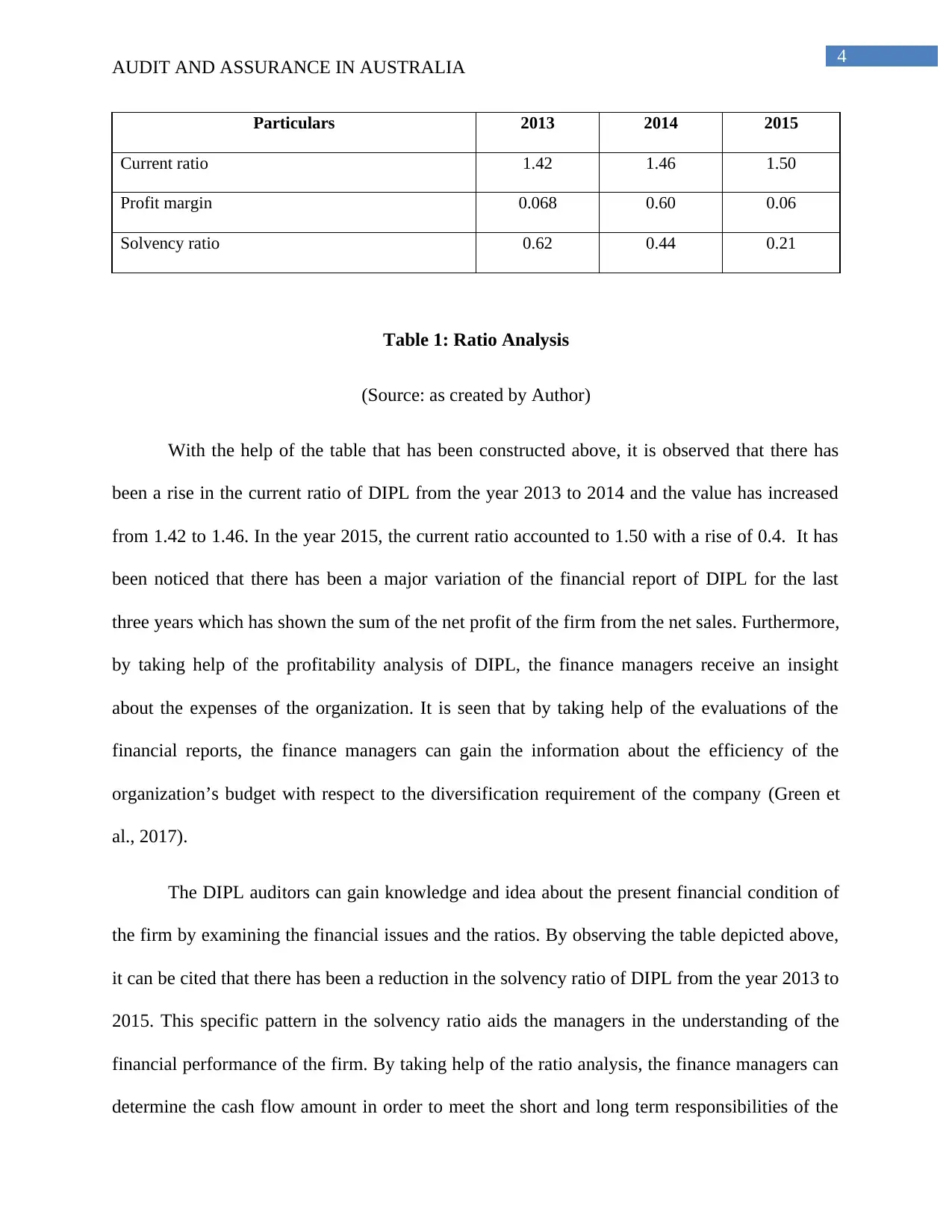

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

With the help of the table that has been constructed above, it is observed that there has

been a rise in the current ratio of DIPL from the year 2013 to 2014 and the value has increased

from 1.42 to 1.46. In the year 2015, the current ratio accounted to 1.50 with a rise of 0.4. It has

been noticed that there has been a major variation of the financial report of DIPL for the last

three years which has shown the sum of the net profit of the firm from the net sales. Furthermore,

by taking help of the profitability analysis of DIPL, the finance managers receive an insight

about the expenses of the organization. It is seen that by taking help of the evaluations of the

financial reports, the finance managers can gain the information about the efficiency of the

organization’s budget with respect to the diversification requirement of the company (Green et

al., 2017).

The DIPL auditors can gain knowledge and idea about the present financial condition of

the firm by examining the financial issues and the ratios. By observing the table depicted above,

it can be cited that there has been a reduction in the solvency ratio of DIPL from the year 2013 to

2015. This specific pattern in the solvency ratio aids the managers in the understanding of the

financial performance of the firm. By taking help of the ratio analysis, the finance managers can

determine the cash flow amount in order to meet the short and long term responsibilities of the

AUDIT AND ASSURANCE IN AUSTRALIA

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

With the help of the table that has been constructed above, it is observed that there has

been a rise in the current ratio of DIPL from the year 2013 to 2014 and the value has increased

from 1.42 to 1.46. In the year 2015, the current ratio accounted to 1.50 with a rise of 0.4. It has

been noticed that there has been a major variation of the financial report of DIPL for the last

three years which has shown the sum of the net profit of the firm from the net sales. Furthermore,

by taking help of the profitability analysis of DIPL, the finance managers receive an insight

about the expenses of the organization. It is seen that by taking help of the evaluations of the

financial reports, the finance managers can gain the information about the efficiency of the

organization’s budget with respect to the diversification requirement of the company (Green et

al., 2017).

The DIPL auditors can gain knowledge and idea about the present financial condition of

the firm by examining the financial issues and the ratios. By observing the table depicted above,

it can be cited that there has been a reduction in the solvency ratio of DIPL from the year 2013 to

2015. This specific pattern in the solvency ratio aids the managers in the understanding of the

financial performance of the firm. By taking help of the ratio analysis, the finance managers can

determine the cash flow amount in order to meet the short and long term responsibilities of the

5

AUDIT AND ASSURANCE IN AUSTRALIA

firm. Furthermore, it can be cited that the assessment and the comparison of the performance and

the ratios of the company can aid the financial managers to determine the financial condition and

performance of DIPL over the past three year time period. Additionally, the finance managers

can determine whether the present financial situation of the firm is unfavourable or not (Shah et

al., 2017). In circumstances of a unfavourable the DIPL managers requires remedial actions in

order to bring back the efficient financial condition of DIPL. Therefore, by examining the tables

that have been constructed above, it can be cited that the analytical techniques of the financial

data has significant figures for the organization.

Answer to Question No 2

The risks that are in association to a business can be described as the potentiality of the

organizational inability in order to reach the objectives of the organization. There have been

various factors of risk that are related to DIPL and this makes the firm ineffective to attain their

objectives. It has been observed that DIPL has been unable to record various financial

transactions of their activities (Rahim & Idowu 2015). By looking at the case study, the faults of

the management have a direct relation with the unreliable and futile planning of the several sales,

financial and marketing operations of DIPL. With respect to the case study there have been

specifically two factors of risk that have a significant effect on restricting DIPL to attain their

goals. They are explained as follows:

Financial Risk

The risk associated with finance can be explained as the ineffectiveness of an

organization in order to payout their liabilities that are in nature long term. With the rise in the

extrinsic liabilities, the extent of risk even gets raised. The debt percentage of DIPL in

AUDIT AND ASSURANCE IN AUSTRALIA

firm. Furthermore, it can be cited that the assessment and the comparison of the performance and

the ratios of the company can aid the financial managers to determine the financial condition and

performance of DIPL over the past three year time period. Additionally, the finance managers

can determine whether the present financial situation of the firm is unfavourable or not (Shah et

al., 2017). In circumstances of a unfavourable the DIPL managers requires remedial actions in

order to bring back the efficient financial condition of DIPL. Therefore, by examining the tables

that have been constructed above, it can be cited that the analytical techniques of the financial

data has significant figures for the organization.

Answer to Question No 2

The risks that are in association to a business can be described as the potentiality of the

organizational inability in order to reach the objectives of the organization. There have been

various factors of risk that are related to DIPL and this makes the firm ineffective to attain their

objectives. It has been observed that DIPL has been unable to record various financial

transactions of their activities (Rahim & Idowu 2015). By looking at the case study, the faults of

the management have a direct relation with the unreliable and futile planning of the several sales,

financial and marketing operations of DIPL. With respect to the case study there have been

specifically two factors of risk that have a significant effect on restricting DIPL to attain their

goals. They are explained as follows:

Financial Risk

The risk associated with finance can be explained as the ineffectiveness of an

organization in order to payout their liabilities that are in nature long term. With the rise in the

extrinsic liabilities, the extent of risk even gets raised. The debt percentage of DIPL in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT AND ASSURANCE IN AUSTRALIA

accordance to their equity by comparing with the figures obtained for the last three years have

increased significantly in the year 2015. It is even observed that there has been a rise in the

payment pressure that are in relation to liabilities of loan payout and the fixed rate interests of the

company within a stipulated time period (Carson et al., 2014). The observations have indicated

that there exists a challenge to the solvency condition of DIPL in the long run if DIPL is unable

to make payments for the principle and the interest amount.

Misstatement of the financial statements:

There exists a chance that DIPL may look to make transformations in their financial

statements in order to maintain their debt to equity and their current ratio in line with the contract

agreement with the borrowing firm. DIPL in order to preserve their current ratio may look to

increase their current assets with the help of the rising receivables or inventory values as well.

DIPL tries to preserve their debt-to-equity ratio looks to increase their equity values with the

help of the rising retained earnings value.

Risks related to information technology

The use of information technology within DIPL creates a serious amount of challenge for

them. The scarcity in the control of information technology may have extreme effect on DIPL.

There was a significant amount of burden that was stressed over to the IT personnel by the

management of DIPL in order to conclude the technique in the year 2015. The accounting

information process has threat related to security and this has mainly been due to the natural and

man-made calamities (Sutherland 2017).

AUDIT AND ASSURANCE IN AUSTRALIA

accordance to their equity by comparing with the figures obtained for the last three years have

increased significantly in the year 2015. It is even observed that there has been a rise in the

payment pressure that are in relation to liabilities of loan payout and the fixed rate interests of the

company within a stipulated time period (Carson et al., 2014). The observations have indicated

that there exists a challenge to the solvency condition of DIPL in the long run if DIPL is unable

to make payments for the principle and the interest amount.

Misstatement of the financial statements:

There exists a chance that DIPL may look to make transformations in their financial

statements in order to maintain their debt to equity and their current ratio in line with the contract

agreement with the borrowing firm. DIPL in order to preserve their current ratio may look to

increase their current assets with the help of the rising receivables or inventory values as well.

DIPL tries to preserve their debt-to-equity ratio looks to increase their equity values with the

help of the rising retained earnings value.

Risks related to information technology

The use of information technology within DIPL creates a serious amount of challenge for

them. The scarcity in the control of information technology may have extreme effect on DIPL.

There was a significant amount of burden that was stressed over to the IT personnel by the

management of DIPL in order to conclude the technique in the year 2015. The accounting

information process has threat related to security and this has mainly been due to the natural and

man-made calamities (Sutherland 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT AND ASSURANCE IN AUSTRALIA

Misstatement in the financial statements

DIPL has been unable to maintain the equivalency among the current software process

and the innovative accounting system. There has been an issue of the ineffective transaction

allocation. The periodicity concept of accounting has not been followed by DIPL. Therefore, it

can be seen that it could lead to an ineffective disclosure of the profit condition as well as the

financial condition of DIPL (Varughese et al., 2014)

Answer to Question No 3

Answer to Question No 3 (a)

The backdrop data of DIPL that has been gathered with the help of the case study has

disclosed the potentiality of the introduction of the in effective financial statement construction

processes of DIPL. The important factors of risk that are associated with the use of these

practices can be described as follows:

Types of

Risk

Details and Identification

Fraudulent

Risk

By examining the information gathered from the DIPL case study, it can be

noticed that the key risk of counterfeit is related with the staffs and the

employees of the organization, as they have the possibility to be associated with

the operations. The key factor that is associated with the risk is the discontent

within the employees of the corporation (Joshi et al., 2014). According to the

case study that is associated with DIPL, there has been an observation that there

has been extensive stress from the side of the management so that the new

accounting process can be implemented. As the implementation of the concerned

AUDIT AND ASSURANCE IN AUSTRALIA

Misstatement in the financial statements

DIPL has been unable to maintain the equivalency among the current software process

and the innovative accounting system. There has been an issue of the ineffective transaction

allocation. The periodicity concept of accounting has not been followed by DIPL. Therefore, it

can be seen that it could lead to an ineffective disclosure of the profit condition as well as the

financial condition of DIPL (Varughese et al., 2014)

Answer to Question No 3

Answer to Question No 3 (a)

The backdrop data of DIPL that has been gathered with the help of the case study has

disclosed the potentiality of the introduction of the in effective financial statement construction

processes of DIPL. The important factors of risk that are associated with the use of these

practices can be described as follows:

Types of

Risk

Details and Identification

Fraudulent

Risk

By examining the information gathered from the DIPL case study, it can be

noticed that the key risk of counterfeit is related with the staffs and the

employees of the organization, as they have the possibility to be associated with

the operations. The key factor that is associated with the risk is the discontent

within the employees of the corporation (Joshi et al., 2014). According to the

case study that is associated with DIPL, there has been an observation that there

has been extensive stress from the side of the management so that the new

accounting process can be implemented. As the implementation of the concerned

8

AUDIT AND ASSURANCE IN AUSTRALIA

accounting system establishes a enormous strain on the employees, there exists

an increased amount of risk as the employees may be associated with

malpractices (Gu et al., 2017). Therefore, in order to act as a remedy for the

reconciliation process, the employees of DIPL may make use of malpractices

and this process may result to financial report misstatement. According to the

concerned case study, because of inefficient introduction of the innovative

accounting software, the company accountants have been unable to record in a

proper manner, the financial transactions and the initial accounting for the

present accounting year (Diez et al., 2015). Furthermore, the fraudulent risk can

be discovered in the mechanism in order to choose the CEO succession of the

organization. Due to this effect, there can be an increased opportunity of intrinsic

risks within DIPL.

Risk related

to Financial

Reporting

During the business activities of DIPL, the other key risk can be noticed in the

mechanism of financial reporting of DIPL (Beiles et al., 2015). During the

situation, if the stakeholders of DIPL have key financial anticipations from the

financial presentation of DIPL, there is an increased probability of malpractices

in the financial statements from the side of the organization. It has been observed

that the management of DIPL makes alterations in the financial reports thereby

showing a false presentation to the stakeholders that the organization has been

undergoing financial growth and effective operations. Therefore, it can be cited

that the risk of fraud in the reporting of the financial statements is one of the key

risks in DIPL.

AUDIT AND ASSURANCE IN AUSTRALIA

accounting system establishes a enormous strain on the employees, there exists

an increased amount of risk as the employees may be associated with

malpractices (Gu et al., 2017). Therefore, in order to act as a remedy for the

reconciliation process, the employees of DIPL may make use of malpractices

and this process may result to financial report misstatement. According to the

concerned case study, because of inefficient introduction of the innovative

accounting software, the company accountants have been unable to record in a

proper manner, the financial transactions and the initial accounting for the

present accounting year (Diez et al., 2015). Furthermore, the fraudulent risk can

be discovered in the mechanism in order to choose the CEO succession of the

organization. Due to this effect, there can be an increased opportunity of intrinsic

risks within DIPL.

Risk related

to Financial

Reporting

During the business activities of DIPL, the other key risk can be noticed in the

mechanism of financial reporting of DIPL (Beiles et al., 2015). During the

situation, if the stakeholders of DIPL have key financial anticipations from the

financial presentation of DIPL, there is an increased probability of malpractices

in the financial statements from the side of the organization. It has been observed

that the management of DIPL makes alterations in the financial reports thereby

showing a false presentation to the stakeholders that the organization has been

undergoing financial growth and effective operations. Therefore, it can be cited

that the risk of fraud in the reporting of the financial statements is one of the key

risks in DIPL.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT AND ASSURANCE IN AUSTRALIA

Answer to Question 3 (b)

With respect to the given case study, there has been a major deficiency in the valuation of

the raw materials of DIPL that is on the basis of the mechanism of the aggregate cost. The key

factor has been the rise in the cost of paper that has been way higher than the aggregate cost.

Therefore, it can be concluded that this is not an efficient method. The principal risk associated

with the process of the introduction of the innovative accounting software can be recognised by

taking assistance of examining several steps of the jobs within the organization (Singh et al.,

2014). Furthermore, the evaluation and assessment of the financial statements of DIPL aids the

administration to discover the fraudulent risk that is associated with the reporting of the

financials. According to the discussions made earlier, the assessment can be undertaken with the

assistance of several analytical techniques that is known as ratio analysis, benchmarking and

other financial mechanisms (Stewart et al., 2015). It is essential for the administration of DIPL in

order to complete the analysis and assessment mechanism in a timely manner.

AUDIT AND ASSURANCE IN AUSTRALIA

Answer to Question 3 (b)

With respect to the given case study, there has been a major deficiency in the valuation of

the raw materials of DIPL that is on the basis of the mechanism of the aggregate cost. The key

factor has been the rise in the cost of paper that has been way higher than the aggregate cost.

Therefore, it can be concluded that this is not an efficient method. The principal risk associated

with the process of the introduction of the innovative accounting software can be recognised by

taking assistance of examining several steps of the jobs within the organization (Singh et al.,

2014). Furthermore, the evaluation and assessment of the financial statements of DIPL aids the

administration to discover the fraudulent risk that is associated with the reporting of the

financials. According to the discussions made earlier, the assessment can be undertaken with the

assistance of several analytical techniques that is known as ratio analysis, benchmarking and

other financial mechanisms (Stewart et al., 2015). It is essential for the administration of DIPL in

order to complete the analysis and assessment mechanism in a timely manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT AND ASSURANCE IN AUSTRALIA

Reference List

Beiles, C. B., Retegan, C., & Maddern, G. J. (2015). Victorian Audit of Surgical Mortality is

associated with improved clinical outcomes. ANZ journal of surgery, 85(11), 803-807.

Carson, E., Redmayne, N. B., & Liao, L. (2014). Audit market structure and competition in

Australia. Australian Accounting Review, 24(4), 298-312.

Diez, P., Aird, E. G. A., Gouldstone, C. A., Sander, T., Eaton, D. J., & Sharpe, P. H. G. (2015).

OC-0271: A multicentre audit of HDR and PDR brachytherapy absolute dosimetry in

association with the INTERLACE trial. Radiotherapy and Oncology, 115, S139.

Green, W., Green, W., Taylor, S., Taylor, S., Wu, J., & Wu, J. (2017). Determinants of

greenhouse gas assurance provider choice. Meditari Accountancy Research, 25(1), 114-

135.

Gu, T., Simunic, D. A., & Stein, M. T. (2017). Fixed Costs, Audit Production, and Audit

Markets: Theory and Evidence.

Hardy, C. A. (2014). The messy matters of continuous assurance: Findings from exploratory

research in Australia. Journal of Information Systems, 28(2), 357-377.

Joshi, R., Hocking, C., O’Neill, S., Singhal, N., Kee, M., & Keefe, D. M. (2014). A Prospective

Audit of Inpatient Medical Oncology Consultation Patterns in a Tertiary Teaching

Hospital in South Australia. Global Journal of Epidemiology and Public Health, 1, 42-

47.

AUDIT AND ASSURANCE IN AUSTRALIA

Reference List

Beiles, C. B., Retegan, C., & Maddern, G. J. (2015). Victorian Audit of Surgical Mortality is

associated with improved clinical outcomes. ANZ journal of surgery, 85(11), 803-807.

Carson, E., Redmayne, N. B., & Liao, L. (2014). Audit market structure and competition in

Australia. Australian Accounting Review, 24(4), 298-312.

Diez, P., Aird, E. G. A., Gouldstone, C. A., Sander, T., Eaton, D. J., & Sharpe, P. H. G. (2015).

OC-0271: A multicentre audit of HDR and PDR brachytherapy absolute dosimetry in

association with the INTERLACE trial. Radiotherapy and Oncology, 115, S139.

Green, W., Green, W., Taylor, S., Taylor, S., Wu, J., & Wu, J. (2017). Determinants of

greenhouse gas assurance provider choice. Meditari Accountancy Research, 25(1), 114-

135.

Gu, T., Simunic, D. A., & Stein, M. T. (2017). Fixed Costs, Audit Production, and Audit

Markets: Theory and Evidence.

Hardy, C. A. (2014). The messy matters of continuous assurance: Findings from exploratory

research in Australia. Journal of Information Systems, 28(2), 357-377.

Joshi, R., Hocking, C., O’Neill, S., Singhal, N., Kee, M., & Keefe, D. M. (2014). A Prospective

Audit of Inpatient Medical Oncology Consultation Patterns in a Tertiary Teaching

Hospital in South Australia. Global Journal of Epidemiology and Public Health, 1, 42-

47.

11

AUDIT AND ASSURANCE IN AUSTRALIA

Kend, M., Houghton, K. A., & Jubb, C. (2014). Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4),

313-320.

Min, S. H. E. N., & LV, L. Q. (2017). English-Chinese Translation for Tax Vocabularies in

Business English. DEStech Transactions on Social Science, Education and Human

Science, (meit).

Moroney, R., Campbell, F., Hamilton, J., & Warren, V. (2014). Auditing: A Practical Approach.

Wiley Global Education.

Rahim, M. M., & Idowu, S. O. (Eds.). (2015). Social Audit Regulation: Development,

Challenges and Opportunities. Springer.

Shah, N., Reintjes, F., Courtney, M., Klarenbach, S. W., Ye, F., Schick-Makaroff, K., ... &

Pauly, R. P. (2017). Quality assurance audit of technique failure and 90-day mortality

after program discharge in a Canadian home hemodialysis program. Clinical Journal of

the American Society of Nephrology, CJN-00140117.

Singh, H., Woodliff, D., Sultana, N., & Newby, R. (2014). Additional evidence on the

relationship between an internal audit function and external audit fees in

Australia. International Journal of Auditing, 18(1), 27-39.

Stewart, J., Kent, P., & Routledge, J. (2015). The association between audit partner rotation and

audit fees: Empirical evidence from the Australian market. Auditing: A Journal of

Practice & Theory, 35(1), 181-197.

Sutherland, D. W. (2017). Independent audit report. Newsmonth, 37(3), 19.

AUDIT AND ASSURANCE IN AUSTRALIA

Kend, M., Houghton, K. A., & Jubb, C. (2014). Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4),

313-320.

Min, S. H. E. N., & LV, L. Q. (2017). English-Chinese Translation for Tax Vocabularies in

Business English. DEStech Transactions on Social Science, Education and Human

Science, (meit).

Moroney, R., Campbell, F., Hamilton, J., & Warren, V. (2014). Auditing: A Practical Approach.

Wiley Global Education.

Rahim, M. M., & Idowu, S. O. (Eds.). (2015). Social Audit Regulation: Development,

Challenges and Opportunities. Springer.

Shah, N., Reintjes, F., Courtney, M., Klarenbach, S. W., Ye, F., Schick-Makaroff, K., ... &

Pauly, R. P. (2017). Quality assurance audit of technique failure and 90-day mortality

after program discharge in a Canadian home hemodialysis program. Clinical Journal of

the American Society of Nephrology, CJN-00140117.

Singh, H., Woodliff, D., Sultana, N., & Newby, R. (2014). Additional evidence on the

relationship between an internal audit function and external audit fees in

Australia. International Journal of Auditing, 18(1), 27-39.

Stewart, J., Kent, P., & Routledge, J. (2015). The association between audit partner rotation and

audit fees: Empirical evidence from the Australian market. Auditing: A Journal of

Practice & Theory, 35(1), 181-197.

Sutherland, D. W. (2017). Independent audit report. Newsmonth, 37(3), 19.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.