Audit and Assurance Report: Key Audit Risks and Analysis

VerifiedAdded on 2021/05/30

|7

|786

|22

Report

AI Summary

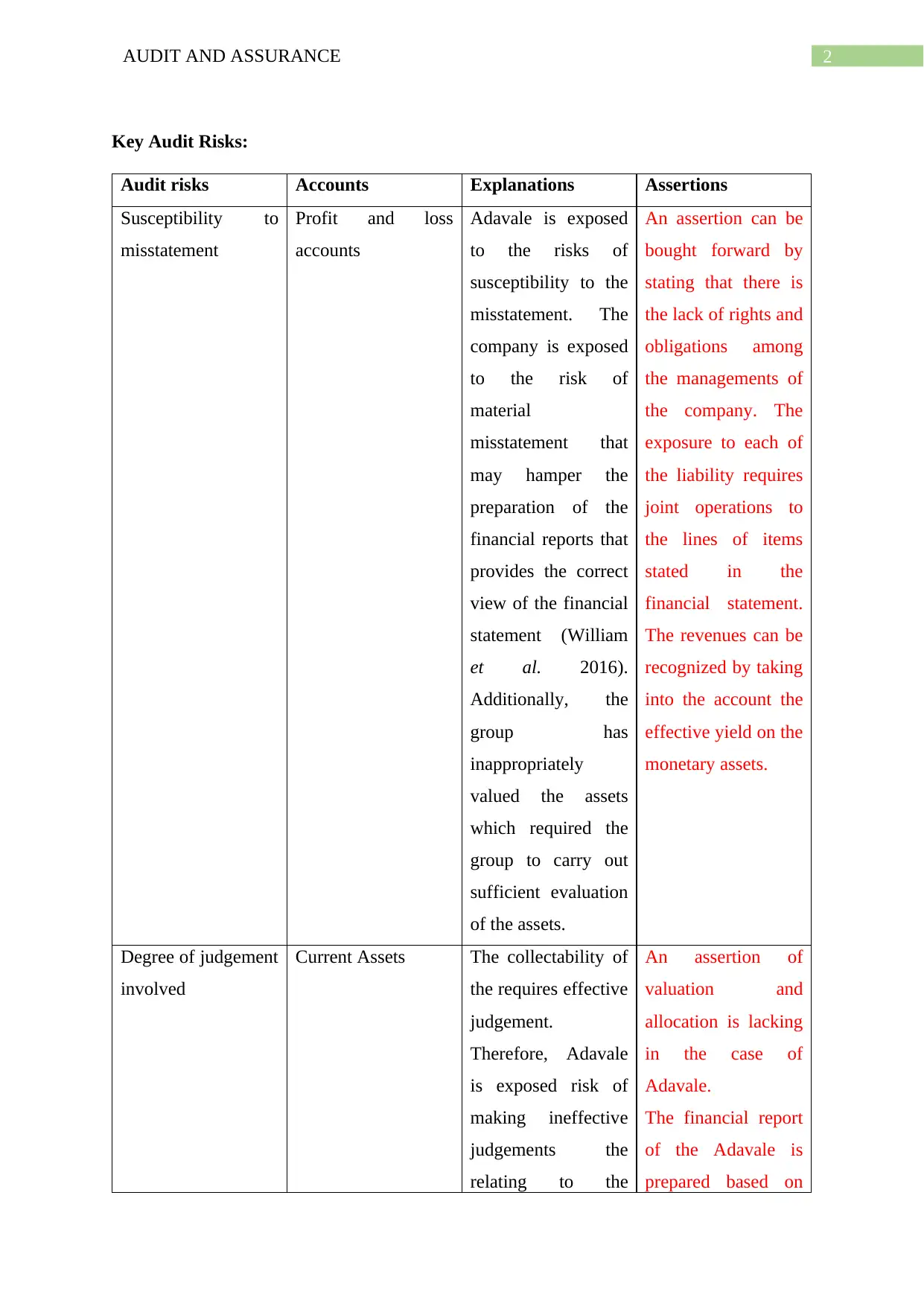

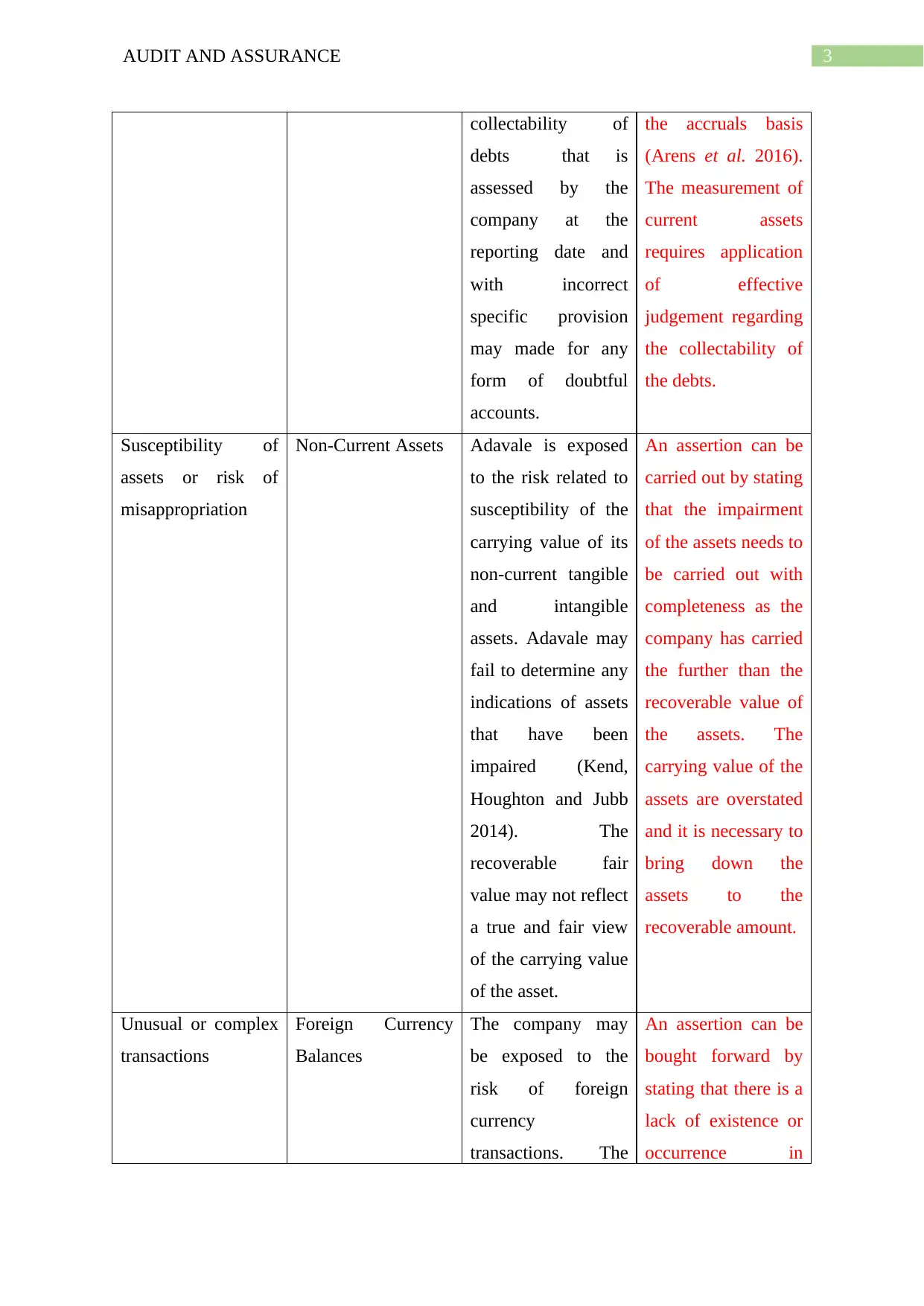

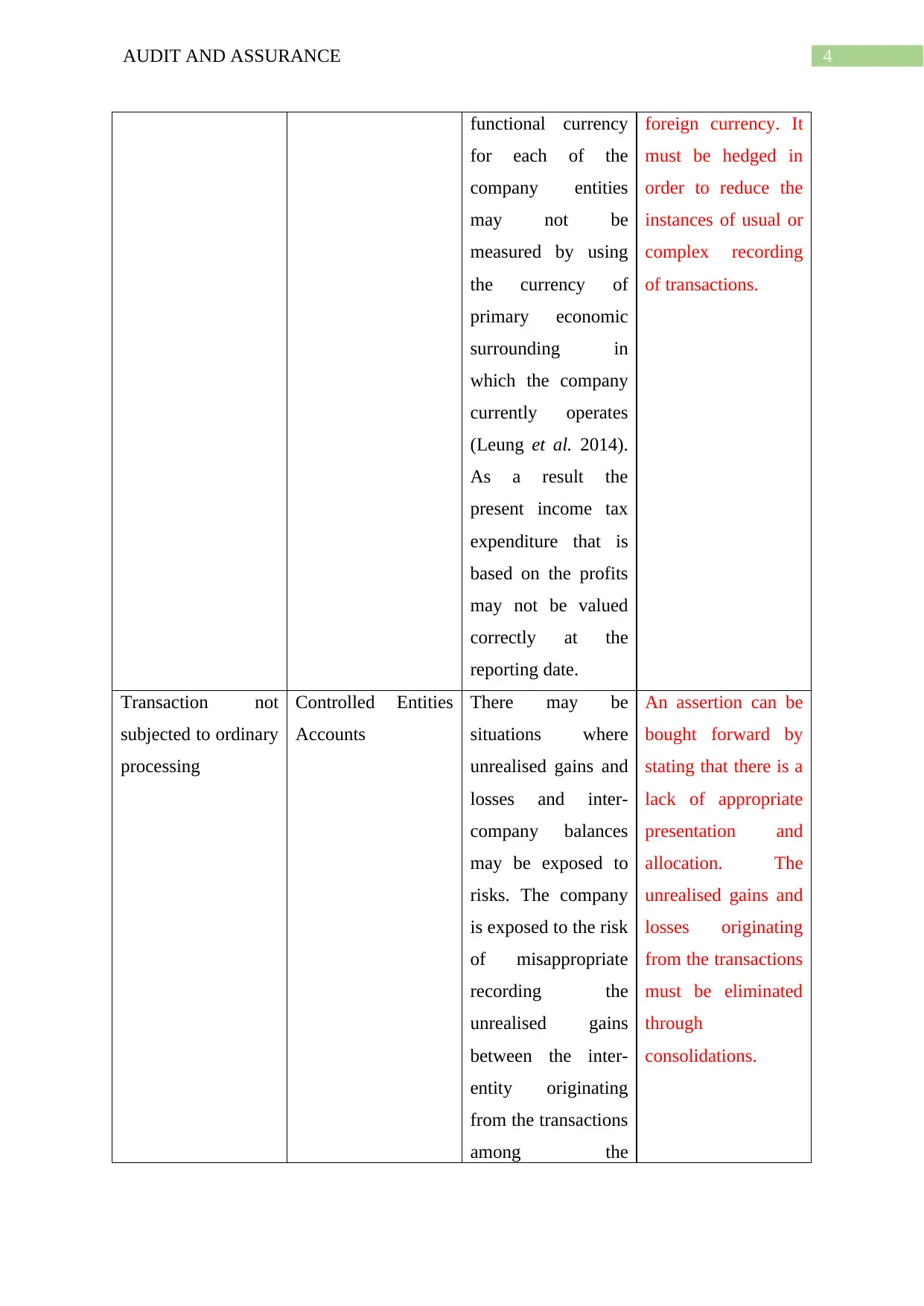

This report provides an analysis of key audit risks within the context of audit and assurance. It identifies and explains various risks associated with profit and loss accounts, current assets, non-current assets, foreign currency balances, and controlled entities. The report details potential misstatements, assertions, and the degree of judgment involved in financial reporting. For each area, the report outlines the specific audit risks, explains the potential for misstatement, and suggests relevant assertions. The report also considers the impact of unusual or complex transactions, such as those involving foreign currency and inter-company balances. It emphasizes the importance of proper valuation, allocation, and the elimination of unrealized gains and losses. The report concludes with a reference list of supporting literature.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.