Comprehensive Audit, Assurance and Compliance Report for CSR Limited

VerifiedAdded on 2023/06/07

|16

|3784

|442

Report

AI Summary

This report provides a comprehensive analysis of the audit, assurance, and compliance aspects of CSR Limited, an Australian Securities Exchange (ASX) listed company. It examines the auditors' independence, compliance with regulations, and the provision of non-audit services, including sustainability and advisory services, alongside auditor remuneration details. The report delves into key audit matters, such as product liability and asset valuation, outlining the substantive audit procedures employed by Deloitte. Furthermore, it assesses the role of the Audit Committee and provides an overview of the auditor's opinion on CSR Limited's financial statements, highlighting the responsibilities of the directors in financial reporting. The report also discusses material subsequent events and the assessment of material information by the auditors.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Executive Summary

Analysis and evaluation of the diversified roles and responsibilities of the auditors is the central

objective of this study. This report takes into account the independence of the auditors. After

that, this report also considers the analysis of the material events in the financial statements of

the company. After that, this report takes into account the key audit matters of the company

along with the disclosure of the substantive audit procedures.

Executive Summary

Analysis and evaluation of the diversified roles and responsibilities of the auditors is the central

objective of this study. This report takes into account the independence of the auditors. After

that, this report also considers the analysis of the material events in the financial statements of

the company. After that, this report takes into account the key audit matters of the company

along with the disclosure of the substantive audit procedures.

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Introduction.....................................................................................................................................3

Compliance with Auditors’ Independence Requirement................................................................3

Non-Audit Services..........................................................................................................................4

Auditor’s Remuneration..................................................................................................................5

Key Audit Matters............................................................................................................................6

Audit Committee..............................................................................................................................8

Audit Opinion...................................................................................................................................9

Difference between Responsibilities...............................................................................................9

Material Subsequent Events..........................................................................................................10

Assessment of Material Information by the Auditors...................................................................10

Material Information Missing........................................................................................................11

Follow-up Questions......................................................................................................................11

Conclusion......................................................................................................................................12

References.....................................................................................................................................13

Table of Contents

Introduction.....................................................................................................................................3

Compliance with Auditors’ Independence Requirement................................................................3

Non-Audit Services..........................................................................................................................4

Auditor’s Remuneration..................................................................................................................5

Key Audit Matters............................................................................................................................6

Audit Committee..............................................................................................................................8

Audit Opinion...................................................................................................................................9

Difference between Responsibilities...............................................................................................9

Material Subsequent Events..........................................................................................................10

Assessment of Material Information by the Auditors...................................................................10

Material Information Missing........................................................................................................11

Follow-up Questions......................................................................................................................11

Conclusion......................................................................................................................................12

References.....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

Introduction

Financial success of the business entities largely depends on the report of the auditors

as the investors and other users see this report as a tool to judge the fairness and truthfulness

of the presented financial statements of the business entities (Chambers 2014). At the same

time, it is also the responsibility of the auditors to find out the main reasons for the occurrence

if material missstements in the financial statements of the companies. Thus, at the time to

conduct the audit procedure, the requirement of the auditors is to take into consideration all

the relevant financial aspects of the client organization (Christensen, Glover and Wolfe 2014).

The consideration of all these aspects helps in enhancing the quality of audit operations in the

companies. After the identification of material misstatements and their reasons for occurrence,

it is needed for the auditor to make the effective communication of those crucial aspects in the

annual reports so that all the stakeholders of the company can become aware of these facts. As

auditing is considered as one of the major aspects for the financial success of the companies,

the authorities have taken different kinds of initiatives with the aim to enhance the quality of

audit operations (Ojala 2014). The objective of this report is to inspect and analyze different

aspect of auditing in CSR Limited, an Australian Securities Exchange (ASX) listed company.

Compliance with Auditors’ Independence Requirement

In order to avoid the violation of any aspects of auditor’s independence, it is the

requirement for the auditors to make compliance with the required standards and regulations

of auditor’s independence (Tepalagul and Lin 2015). This aspect is also applicable in the case of

CSR Limited. It needs to be mentioned that the audit partner of CSR Limited for the year 2018 is

Introduction

Financial success of the business entities largely depends on the report of the auditors

as the investors and other users see this report as a tool to judge the fairness and truthfulness

of the presented financial statements of the business entities (Chambers 2014). At the same

time, it is also the responsibility of the auditors to find out the main reasons for the occurrence

if material missstements in the financial statements of the companies. Thus, at the time to

conduct the audit procedure, the requirement of the auditors is to take into consideration all

the relevant financial aspects of the client organization (Christensen, Glover and Wolfe 2014).

The consideration of all these aspects helps in enhancing the quality of audit operations in the

companies. After the identification of material misstatements and their reasons for occurrence,

it is needed for the auditor to make the effective communication of those crucial aspects in the

annual reports so that all the stakeholders of the company can become aware of these facts. As

auditing is considered as one of the major aspects for the financial success of the companies,

the authorities have taken different kinds of initiatives with the aim to enhance the quality of

audit operations (Ojala 2014). The objective of this report is to inspect and analyze different

aspect of auditing in CSR Limited, an Australian Securities Exchange (ASX) listed company.

Compliance with Auditors’ Independence Requirement

In order to avoid the violation of any aspects of auditor’s independence, it is the

requirement for the auditors to make compliance with the required standards and regulations

of auditor’s independence (Tepalagul and Lin 2015). This aspect is also applicable in the case of

CSR Limited. It needs to be mentioned that the audit partner of CSR Limited for the year 2018 is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

Deloitte. It can be found in the annual report of CSR limited, especially in the section of report

of the director that there is a major standard that has been adhered to for the elimination for

the risk related to the violation of auditor’s independence and the standard is from 307C of the

Corporations Act 2001 (Csr.com.au 2018). In addition, the compliance with this major

principles has prevented the risk of the violation of requirements of auditor’s independence

(Csr.com.au 2018). Apart from this, the directors of the company have also mentioned that the

auditors have complied with all the requirements of Code of Professional Conduct while

providing the professional services in auditing.

Non-Audit Services

It needs to be mentioned that the auditors use to provide their audit clients with some

major non-audit services. The annual report of the company provides the evidence of providing

non-audit services by the auditors to the company; and they are Assurance Services related to

Sustainability and Carbon; and Other Assurance and Advisory Services. CSR Limited paid

$77,108 and $58,000 in 2018 and 2018 respectively for the sustainability and carbon related

non-audit services. At the same time, CSR Limited paid $9000 and $40,600 in 2018 and 2017 for

the services of assurance and advisory to the auditors (Csr.com.au 2018).

This fact is also evident from the latest annual report of CSR Limited that the auditors of

Deloitte have followed the guiding principles and standards of Corporations Act 2001 for

providing the non-audit services. For this reason, Deloitte has made the aspect clear that they

have not compromised the standards of Corporations Act 2001 for materiality determination in

Deloitte. It can be found in the annual report of CSR limited, especially in the section of report

of the director that there is a major standard that has been adhered to for the elimination for

the risk related to the violation of auditor’s independence and the standard is from 307C of the

Corporations Act 2001 (Csr.com.au 2018). In addition, the compliance with this major

principles has prevented the risk of the violation of requirements of auditor’s independence

(Csr.com.au 2018). Apart from this, the directors of the company have also mentioned that the

auditors have complied with all the requirements of Code of Professional Conduct while

providing the professional services in auditing.

Non-Audit Services

It needs to be mentioned that the auditors use to provide their audit clients with some

major non-audit services. The annual report of the company provides the evidence of providing

non-audit services by the auditors to the company; and they are Assurance Services related to

Sustainability and Carbon; and Other Assurance and Advisory Services. CSR Limited paid

$77,108 and $58,000 in 2018 and 2018 respectively for the sustainability and carbon related

non-audit services. At the same time, CSR Limited paid $9000 and $40,600 in 2018 and 2017 for

the services of assurance and advisory to the auditors (Csr.com.au 2018).

This fact is also evident from the latest annual report of CSR Limited that the auditors of

Deloitte have followed the guiding principles and standards of Corporations Act 2001 for

providing the non-audit services. For this reason, Deloitte has made the aspect clear that they

have not compromised the standards of Corporations Act 2001 for materiality determination in

5AUDIT, ASSURANCE AND COMPLIANCE

the process of providing the non-audit services. They have considered the monitoring of

auditor’s independence while providing the non-audit services (Makarenko 2016).

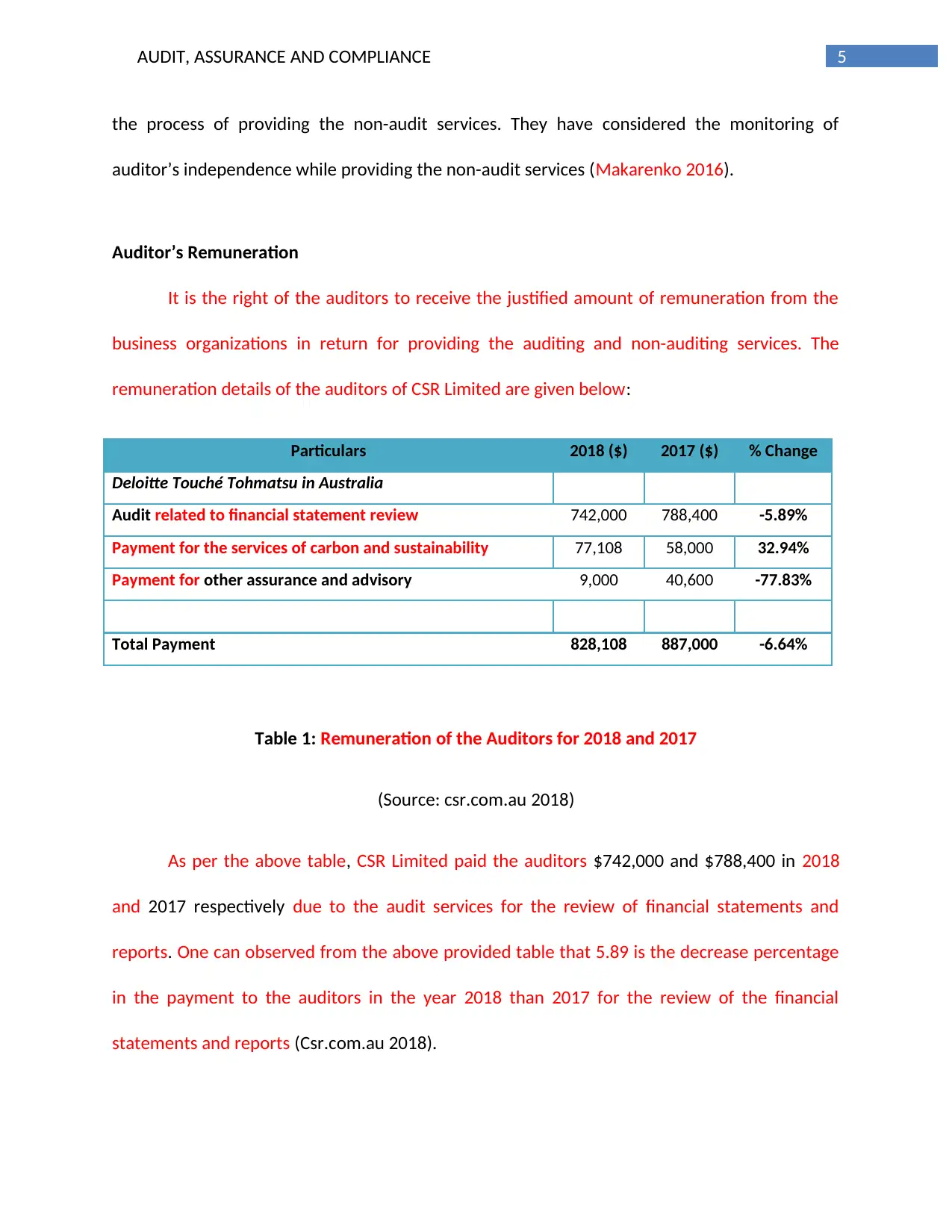

Auditor’s Remuneration

It is the right of the auditors to receive the justified amount of remuneration from the

business organizations in return for providing the auditing and non-auditing services. The

remuneration details of the auditors of CSR Limited are given below:

Particulars 2018 ($) 2017 ($) % Change

Deloitte Touché Tohmatsu in Australia

Audit related to financial statement review 742,000 788,400 -5.89%

Payment for the services of carbon and sustainability 77,108 58,000 32.94%

Payment for other assurance and advisory 9,000 40,600 -77.83%

Total Payment 828,108 887,000 -6.64%

Table 1: Remuneration of the Auditors for 2018 and 2017

(Source: csr.com.au 2018)

As per the above table, CSR Limited paid the auditors $742,000 and $788,400 in 2018

and 2017 respectively due to the audit services for the review of financial statements and

reports. One can observed from the above provided table that 5.89 is the decrease percentage

in the payment to the auditors in the year 2018 than 2017 for the review of the financial

statements and reports (Csr.com.au 2018).

the process of providing the non-audit services. They have considered the monitoring of

auditor’s independence while providing the non-audit services (Makarenko 2016).

Auditor’s Remuneration

It is the right of the auditors to receive the justified amount of remuneration from the

business organizations in return for providing the auditing and non-auditing services. The

remuneration details of the auditors of CSR Limited are given below:

Particulars 2018 ($) 2017 ($) % Change

Deloitte Touché Tohmatsu in Australia

Audit related to financial statement review 742,000 788,400 -5.89%

Payment for the services of carbon and sustainability 77,108 58,000 32.94%

Payment for other assurance and advisory 9,000 40,600 -77.83%

Total Payment 828,108 887,000 -6.64%

Table 1: Remuneration of the Auditors for 2018 and 2017

(Source: csr.com.au 2018)

As per the above table, CSR Limited paid the auditors $742,000 and $788,400 in 2018

and 2017 respectively due to the audit services for the review of financial statements and

reports. One can observed from the above provided table that 5.89 is the decrease percentage

in the payment to the auditors in the year 2018 than 2017 for the review of the financial

statements and reports (Csr.com.au 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

The above table also includes the payment to Deloitte for non-audit services. It is

evident from the above table that CSR Limited has paid the auditors with $77,108 and $58,000

in 2018 and 2017 respectively for the non-audit services in the areas of carbon and

sustainability. Hence, as compared to the year 2017, Deloitte has received 32.94% more

remuneration in 2018 for providing this specific kind of non-audit services (Csr.com.au 2018).

It can also be observed from the above table that Deloitte has received $9000 in 2018

and $40,600 in 2017 from CSR Limited for providing the company with the non-audit services

related to advisory and other assurance services. Thus, as compared to the year 2017, there is a

77.83% decrease in this payment in the year 2018. On can also observed the fact from the

above table that CSR Limited has paid the auditors with $828,108 and $887,000 in 2018 and

2017 respectively due to get the auditing and non-auditing services (Kusnadi et al. 2016). Thus,

from the above, it can be observed that Deloitte has received 6.64% less audit fees on total

basis in the year 2018 as compared to the year 2017 for providing both audit and non-audit

services.

Key Audit Matters

The recent reformation in the auditing regulations puts the obligation on the companies

and the auditor to disclose the Key Audit Matters along with the applied substantive audit

procedures to minimize them. The following part of the report sheds light on the key audit

matters of identified by the auditors from the review of the financial statements of CSR Limited.

Key Audit Matter 1

The above table also includes the payment to Deloitte for non-audit services. It is

evident from the above table that CSR Limited has paid the auditors with $77,108 and $58,000

in 2018 and 2017 respectively for the non-audit services in the areas of carbon and

sustainability. Hence, as compared to the year 2017, Deloitte has received 32.94% more

remuneration in 2018 for providing this specific kind of non-audit services (Csr.com.au 2018).

It can also be observed from the above table that Deloitte has received $9000 in 2018

and $40,600 in 2017 from CSR Limited for providing the company with the non-audit services

related to advisory and other assurance services. Thus, as compared to the year 2017, there is a

77.83% decrease in this payment in the year 2018. On can also observed the fact from the

above table that CSR Limited has paid the auditors with $828,108 and $887,000 in 2018 and

2017 respectively due to get the auditing and non-auditing services (Kusnadi et al. 2016). Thus,

from the above, it can be observed that Deloitte has received 6.64% less audit fees on total

basis in the year 2018 as compared to the year 2017 for providing both audit and non-audit

services.

Key Audit Matters

The recent reformation in the auditing regulations puts the obligation on the companies

and the auditor to disclose the Key Audit Matters along with the applied substantive audit

procedures to minimize them. The following part of the report sheds light on the key audit

matters of identified by the auditors from the review of the financial statements of CSR Limited.

Key Audit Matter 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

Description: The auditors have considered the position of CSR Limited in product liability for

$289 million as at 31 March 2018 and this situation is connected to the future claims of the

predictable and known asbestos (Sirois, Bédard and Bera 2018). CSR Limited has hired the

outside experts from United States and Australia for the determination of the required

provision for these types of claims. In the presence of the dimension and complication of the

assumptions in order to determine the provision, the auditors have treated this situation as a

key audit matter (Csr.com.au 2018).

Audit Procedures: The auditors of Deloitte have undertaken the assessment of the

independence and competency of the hired outside experts. They have also assessed

methodologies that the experts used for the determination of provision. Most important, the

appointment mechanism of the external experts has been assessed for this purpose. Apart from

these, the auditors have also undertaken the assessment of the determination basis for

prudential margin and the appropriateness of the financial statements of CSR Limited. With the

aim to conduct the testing of the basis to include and exclude the asbestos claims, the process

of the testing of the relevant sample has been considered from the auditor’s side. In the

presence of all these reasons, these performed substantial audit procedures can be classified as

analytical procedures and tests of controls (Kuenkaikaew and Vasarhelyi 2013).

Key Audit Matter 2

Description: This key audit matters is related to the valuation of asset of CSR Limited; and

intangible assets like goodwill along with property, plant and equipments are the related assets

for this key audit matter. It needs to be mentioned that there has been use of major financial

Description: The auditors have considered the position of CSR Limited in product liability for

$289 million as at 31 March 2018 and this situation is connected to the future claims of the

predictable and known asbestos (Sirois, Bédard and Bera 2018). CSR Limited has hired the

outside experts from United States and Australia for the determination of the required

provision for these types of claims. In the presence of the dimension and complication of the

assumptions in order to determine the provision, the auditors have treated this situation as a

key audit matter (Csr.com.au 2018).

Audit Procedures: The auditors of Deloitte have undertaken the assessment of the

independence and competency of the hired outside experts. They have also assessed

methodologies that the experts used for the determination of provision. Most important, the

appointment mechanism of the external experts has been assessed for this purpose. Apart from

these, the auditors have also undertaken the assessment of the determination basis for

prudential margin and the appropriateness of the financial statements of CSR Limited. With the

aim to conduct the testing of the basis to include and exclude the asbestos claims, the process

of the testing of the relevant sample has been considered from the auditor’s side. In the

presence of all these reasons, these performed substantial audit procedures can be classified as

analytical procedures and tests of controls (Kuenkaikaew and Vasarhelyi 2013).

Key Audit Matter 2

Description: This key audit matters is related to the valuation of asset of CSR Limited; and

intangible assets like goodwill along with property, plant and equipments are the related assets

for this key audit matter. It needs to be mentioned that there has been use of major financial

8AUDIT, ASSURANCE AND COMPLIANCE

judgments and assumptions relate to growth rate, discount rate, inflation rate, change in

forecast and others as these all are related to valuation of assets (Velte 2018). For the

identification of the cost generating units, the management of CSR Limited has used

impairment trigger analysis. The involvement of some crucial verdict for the ascertainment of

future cash flows can be seen in this situation that has forced the auditors to consider this

situation as a key audit matter (Csr.com.au 2018).

Audit Procedures: With the aim to address this matter, Deloitte has undertaken the evaluation

process for the determination of the cash generating units. In order to achieve this, Deloitte has

also undertaken the assessment and analysis of certain aspects like terminal rate of growth,

discount rate, rate of inflation, forecaster cash flow and others. Sample testing has been taken

into consideration for the assessment of the mathematical accuracy of the cash flows. At the

same time, Deloitte has also assessed the accuracy of the disclosure of the financial statements

of the company. All these procedures can be considered as analytical procedures and subtitle

test of details (Goh, Krishnan and Li 2013).

Audit Committee

The Board of Directors of CSR Limited has a Risk and Audit Committee can with the

objective for monitoring all the dimensions and issues of the internal control policies and

procedures so that effective safeguard for the financial reporting integrity can be developed

and implemented (Guo et al. 2017). This Risk and Audit Committee includes Four non-executive

directors; they are Mike Ihlein, Mathew Quinn, Penny Winn and John Gillam. The analysis of the

judgments and assumptions relate to growth rate, discount rate, inflation rate, change in

forecast and others as these all are related to valuation of assets (Velte 2018). For the

identification of the cost generating units, the management of CSR Limited has used

impairment trigger analysis. The involvement of some crucial verdict for the ascertainment of

future cash flows can be seen in this situation that has forced the auditors to consider this

situation as a key audit matter (Csr.com.au 2018).

Audit Procedures: With the aim to address this matter, Deloitte has undertaken the evaluation

process for the determination of the cash generating units. In order to achieve this, Deloitte has

also undertaken the assessment and analysis of certain aspects like terminal rate of growth,

discount rate, rate of inflation, forecaster cash flow and others. Sample testing has been taken

into consideration for the assessment of the mathematical accuracy of the cash flows. At the

same time, Deloitte has also assessed the accuracy of the disclosure of the financial statements

of the company. All these procedures can be considered as analytical procedures and subtitle

test of details (Goh, Krishnan and Li 2013).

Audit Committee

The Board of Directors of CSR Limited has a Risk and Audit Committee can with the

objective for monitoring all the dimensions and issues of the internal control policies and

procedures so that effective safeguard for the financial reporting integrity can be developed

and implemented (Guo et al. 2017). This Risk and Audit Committee includes Four non-executive

directors; they are Mike Ihlein, Mathew Quinn, Penny Winn and John Gillam. The analysis of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

2018 Annual Report of CSR Limited indicates towards the absence of any Audit Committee

Charted within the organization (Csr.com.au 2018).

Audit Opinion

One can absorbed certain crucial aspect from the provided opinion by the auditors and

these aspects of the opinion help the investors in various ways. The audit opinion states that

there has been major adherence to the different standards of Corporations Act 2001 so that

efficiency can be maintained in the preparation of the financial statements (Salleh and Jasmani

2014). The opinion of the auditors also indicates towards the fact that the users can get the

true and fair view of the financial performance of CSR Limited from their financial statements.

The auditors have also stated the fact in the auditor’s report that CSR Limited has compliance

with the standards of Corporations Act 2001 and Australian Accounting Standards for financial

reporting (Csr.com.au 2018).

Difference between Responsibilities

To prepare and present the financial statements after making the necessary compliance

with the guiding principles of Australian Accounting Standards and Corporations Act 2001 is the

prime responsibility of the directors of CSR Limited in financial reporting (Frias‐Aceituno,

Rodriguez‐Ariza and Garcia‐Sanchez 2013). After that, assessment of the capability of the

company to continue as a going concern is another responsibility of the directors (Martínez‐

Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros 2015).

2018 Annual Report of CSR Limited indicates towards the absence of any Audit Committee

Charted within the organization (Csr.com.au 2018).

Audit Opinion

One can absorbed certain crucial aspect from the provided opinion by the auditors and

these aspects of the opinion help the investors in various ways. The audit opinion states that

there has been major adherence to the different standards of Corporations Act 2001 so that

efficiency can be maintained in the preparation of the financial statements (Salleh and Jasmani

2014). The opinion of the auditors also indicates towards the fact that the users can get the

true and fair view of the financial performance of CSR Limited from their financial statements.

The auditors have also stated the fact in the auditor’s report that CSR Limited has compliance

with the standards of Corporations Act 2001 and Australian Accounting Standards for financial

reporting (Csr.com.au 2018).

Difference between Responsibilities

To prepare and present the financial statements after making the necessary compliance

with the guiding principles of Australian Accounting Standards and Corporations Act 2001 is the

prime responsibility of the directors of CSR Limited in financial reporting (Frias‐Aceituno,

Rodriguez‐Ariza and Garcia‐Sanchez 2013). After that, assessment of the capability of the

company to continue as a going concern is another responsibility of the directors (Martínez‐

Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

To obtain the require assurance on the fact that there is not any material misstatements

in the financial statements of the company is the prime responsibility of the auditors (Litt et al.

2014). The next major responsibility of the auditors can be seen in providing the correct audit

opinion based on the assessment of material misstatements. Some other responsibilities of the

auditors are the assessment of the internal control mechanism, valuation of the accounting

policies, analysis of the gong concern status and others (Peecher, Solomon and Trotman 2013).

Material Subsequent Events

There is mention about two specific subsequent event of the financial reporting of CSR

Limited for the year 2018. The process to pay the dividend after 31st March 2018 is one of them.

Sale of surplus land at Horsley Park is the second subsequent event. Due to the presence of this

event, CSR Limited is expecting a profit before tax worth $30 million in the statement of

financial performance on 31St March 2019. After the analysis of these two events, the auditors

of Deloitte has provide their opinion that these events do not have any material impact on the

financial statements of CSR Limited (Peecher, Solomon and Trotman 2013).

Assessment of Material Information by the Auditors

An individual third party stakeholder can observe certain facts from the annual report of

CSR Limited and one of them is the fact that the auditors of the company have been efficient at

the time to review the financial reports; and for this reason, they have been able in the

identification of the key audit matters in the business that are the major material issues in the

financial statements. In this process, APES 110, Corporations Act 2001 and Australian Auditing

To obtain the require assurance on the fact that there is not any material misstatements

in the financial statements of the company is the prime responsibility of the auditors (Litt et al.

2014). The next major responsibility of the auditors can be seen in providing the correct audit

opinion based on the assessment of material misstatements. Some other responsibilities of the

auditors are the assessment of the internal control mechanism, valuation of the accounting

policies, analysis of the gong concern status and others (Peecher, Solomon and Trotman 2013).

Material Subsequent Events

There is mention about two specific subsequent event of the financial reporting of CSR

Limited for the year 2018. The process to pay the dividend after 31st March 2018 is one of them.

Sale of surplus land at Horsley Park is the second subsequent event. Due to the presence of this

event, CSR Limited is expecting a profit before tax worth $30 million in the statement of

financial performance on 31St March 2019. After the analysis of these two events, the auditors

of Deloitte has provide their opinion that these events do not have any material impact on the

financial statements of CSR Limited (Peecher, Solomon and Trotman 2013).

Assessment of Material Information by the Auditors

An individual third party stakeholder can observe certain facts from the annual report of

CSR Limited and one of them is the fact that the auditors of the company have been efficient at

the time to review the financial reports; and for this reason, they have been able in the

identification of the key audit matters in the business that are the major material issues in the

financial statements. In this process, APES 110, Corporations Act 2001 and Australian Auditing

11AUDIT, ASSURANCE AND COMPLIANCE

Standards are the major standards that have been adhered to. It can also be seen that the

auditors have communicated the key audit matters in the annual report of 2018 along with the

applied substantive audit procedures. All these aspects indicate towards the effective

treatment of the material events by the auditors of Deloitte (Edgley 2014).

Material Information Missing

The auditors of Deloitte have been able to identify the major material issue in the

financial statements that are the key audit matters while effectively maintaining the compliance

with all the required standards; and they have also properly addressed these issues with the

help of substantive audit procedures. It can also be seen that the auditors of Deloitte has

effectively communicated these key audit matters through their audit report with the required

stakeholders of CSR Limited. All these aspects indicate towards the fact that the auditors have

not missed the assessment of material information of the company (Johnstone, Gramling and

Rittenberg 2013).

Follow-up Questions

1. What are the major procedures in order to detect the material issues?

2. What they have found after the discussion with the internal auditors of CSR Limited?

3. Is there any back-up plan for the audit procedures of CSR Limited in case the existing

one fails? (Adams 2015)

Standards are the major standards that have been adhered to. It can also be seen that the

auditors have communicated the key audit matters in the annual report of 2018 along with the

applied substantive audit procedures. All these aspects indicate towards the effective

treatment of the material events by the auditors of Deloitte (Edgley 2014).

Material Information Missing

The auditors of Deloitte have been able to identify the major material issue in the

financial statements that are the key audit matters while effectively maintaining the compliance

with all the required standards; and they have also properly addressed these issues with the

help of substantive audit procedures. It can also be seen that the auditors of Deloitte has

effectively communicated these key audit matters through their audit report with the required

stakeholders of CSR Limited. All these aspects indicate towards the fact that the auditors have

not missed the assessment of material information of the company (Johnstone, Gramling and

Rittenberg 2013).

Follow-up Questions

1. What are the major procedures in order to detect the material issues?

2. What they have found after the discussion with the internal auditors of CSR Limited?

3. Is there any back-up plan for the audit procedures of CSR Limited in case the existing

one fails? (Adams 2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.