Audit Assurance and Compliance Report: DIPL's Financial Performance

VerifiedAdded on 2020/03/02

|12

|2824

|59

Report

AI Summary

This report provides a comprehensive analysis of an audit assurance and compliance report, focusing on the financial performance of DIPL. It begins with an application of analytical procedures to DIPL's financial statements, evaluating the impact of results on audit planning decisions. The report then identifies inherent risk factors arising from the nature of DIPL's business operations, detailing how these risks could lead to material misstatements in the financial report. Furthermore, the report identifies and explains two key fraud risk factors related to misstatements arising from fraudulent financial reporting, including asset loss and financial reporting fraud. The analysis includes a review of financial ratios, assessment of management integrity, and the impact of IT infrastructure implementation on financial reporting processes. The report highlights the importance of understanding and mitigating risks to ensure accurate and reliable financial reporting.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................7

References........................................................................................................................................9

List of Appendix............................................................................................................................11

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................7

References........................................................................................................................................9

List of Appendix............................................................................................................................11

2AUDIT ASSURANCE AND COMPLIANCE

Answer to Question 1:

Application of analytical procedures to the financial sreport information of DIPL

The various types of the aspects of the financial processing of DIPL have been developed

based on the audit plan. The blueprint of the audit has been considered based on the time taken to

frame the audit plan. In this aspect, the assessor has been able to consider the auditing costs at a

reasonable aspect for assisting and averting the misunderstanding with the clientele. The

declarations associated to the analytical framework for DIPL is considered as the dissemination

process of the information in terms of the financial proclamations. The evaluation mechanism

needs to be set as per the proper utilization of the variety of the mechanisms. The analytical

procedure needs to be based on the financial considerations. The different types of the evaluation

process needs to be considered as per the utilization of the various mechanism procedures.

Despite of this, the analytical process needs to be analysed as per the financial declarations of the

firm. The various types of the evaluation process is based on the dissemination of information as

per the financial information for DIPL. The evaluation process has been carried as per utilizing

the various types of the mechanisms. The financial declarations has been further analysed as per

the vital decisions made for the business (Regoliosi & d’Eri, 2014).

The common sizing for the analytical process has been considered as per the common

reference point. The comparison of the financial statement has been done based on the

consideration of the various corporations. The assessors need to consider the financial report and

evaluate the method for reporting. The registering of the items as per the net liabilities and the

assets needs to consider as per the owner’s equity in the financial report. This needs to be further

examined as per digressing from normal procedure. The analytical benchmarking is based on the

Answer to Question 1:

Application of analytical procedures to the financial sreport information of DIPL

The various types of the aspects of the financial processing of DIPL have been developed

based on the audit plan. The blueprint of the audit has been considered based on the time taken to

frame the audit plan. In this aspect, the assessor has been able to consider the auditing costs at a

reasonable aspect for assisting and averting the misunderstanding with the clientele. The

declarations associated to the analytical framework for DIPL is considered as the dissemination

process of the information in terms of the financial proclamations. The evaluation mechanism

needs to be set as per the proper utilization of the variety of the mechanisms. The analytical

procedure needs to be based on the financial considerations. The different types of the evaluation

process needs to be considered as per the utilization of the various mechanism procedures.

Despite of this, the analytical process needs to be analysed as per the financial declarations of the

firm. The various types of the evaluation process is based on the dissemination of information as

per the financial information for DIPL. The evaluation process has been carried as per utilizing

the various types of the mechanisms. The financial declarations has been further analysed as per

the vital decisions made for the business (Regoliosi & d’Eri, 2014).

The common sizing for the analytical process has been considered as per the common

reference point. The comparison of the financial statement has been done based on the

consideration of the various corporations. The assessors need to consider the financial report and

evaluate the method for reporting. The registering of the items as per the net liabilities and the

assets needs to consider as per the owner’s equity in the financial report. This needs to be further

examined as per digressing from normal procedure. The analytical benchmarking is based on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT ASSURANCE AND COMPLIANCE

utilization of the audit plan. The actual variance from the benchmark from the financial

declarations is seen to detect the root cause (Regoliosi & d’Eri, 2014).

The ratio analysis has not been considered appropriately and this needs to be further

considered for the plan of audit.

Explanation of the way the results influence planning decisions for the audit

The decisions associated to the audit plan have been based on the influence of the

analytical approach and segregation of the data as per the annual report. The current ratio has

been seen to be 1.42 in 2013, 1.46 in 2014 and 1.5 in 2015. In the profitability ratio, the profit

margin of the company has been seen to be 0.068 in 2013, 0.60 in 2014 and 0.06 in 2015. Based

on the various types of the information associated to the profitability, the various aspects of the

net income are compared based on the net sales of the DIPL firm. The assessor will be able to

understand the expenses are appropriate and whether the same can be considered to curtail the

budget and time consideration of the firm. The various natures of the changes in the ratio has

been considered as per the soundness of the financial position and financial condition. For

instance, the solvency ratio is discerned as 0.62 in 2013, 0.44 in 2014 and 0.21 in 2015. This has

been further seen to be considered as per the trends of the financial statements. The comparison

of the ratio for the three periods has been seen to be based on the overall cash transactions based

on the long term liability evaluation of the corporation (Yang & Jia, 2013).

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

utilization of the audit plan. The actual variance from the benchmark from the financial

declarations is seen to detect the root cause (Regoliosi & d’Eri, 2014).

The ratio analysis has not been considered appropriately and this needs to be further

considered for the plan of audit.

Explanation of the way the results influence planning decisions for the audit

The decisions associated to the audit plan have been based on the influence of the

analytical approach and segregation of the data as per the annual report. The current ratio has

been seen to be 1.42 in 2013, 1.46 in 2014 and 1.5 in 2015. In the profitability ratio, the profit

margin of the company has been seen to be 0.068 in 2013, 0.60 in 2014 and 0.06 in 2015. Based

on the various types of the information associated to the profitability, the various aspects of the

net income are compared based on the net sales of the DIPL firm. The assessor will be able to

understand the expenses are appropriate and whether the same can be considered to curtail the

budget and time consideration of the firm. The various natures of the changes in the ratio has

been considered as per the soundness of the financial position and financial condition. For

instance, the solvency ratio is discerned as 0.62 in 2013, 0.44 in 2014 and 0.21 in 2015. This has

been further seen to be considered as per the trends of the financial statements. The comparison

of the ratio for the three periods has been seen to be based on the overall cash transactions based

on the long term liability evaluation of the corporation (Yang & Jia, 2013).

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT ASSURANCE AND COMPLIANCE

The several types of the important considerations have been considered as per the

material misstatements in the financial consideration of the specific concern. This has been

further seen to be considered as per risks reference as per the misstatement in the financial

decisions taken by the corporations. The identified risks have been able to reflect the various

facets of the misstatement as per the financial data. The different nature of the risks has been

further associated to the financial and non-financial factors which can be considered to be true

with a fair view of the financial declarations. The evaluator may further see it demanding for the

associated risk. The evaluator may further detect the risk for non consideration of the various

natures of the distinct risk factors. The identified risk may also be seen to be related to the

diverse errors in the specific bookkeeper. With this essence the main form of the inherent risk

may arise in terms of the DIPL business operations (Ryoo et al., 2014).

The given study has shown the numerous transactions which are particularly omitted by

the accountants or the management of the corporation of DIPL. This can however be sequentially

avoided by DIPL. The corporation has direct lead towards the various types of the

inconsistencies which will be ineffective based on the planning of the sales activities. In addition

to this, the financial declarations of the firm has revealed about the preferred level of profit from

the revenue which has been considered from the sales. The management of the firm may decide

to specify the requirement and the consequent adjustments which need to be made based on the

functionality of the corporation. It can be hereby stated that the DIPL has led to failure for

analysing of the micro and the macro economic factors and associating the existence of the same

in the social and political factors. The subsequent consideration has been further seen to be

reflected as per the poor sales figure and the inherent risks.

The several types of the important considerations have been considered as per the

material misstatements in the financial consideration of the specific concern. This has been

further seen to be considered as per risks reference as per the misstatement in the financial

decisions taken by the corporations. The identified risks have been able to reflect the various

facets of the misstatement as per the financial data. The different nature of the risks has been

further associated to the financial and non-financial factors which can be considered to be true

with a fair view of the financial declarations. The evaluator may further see it demanding for the

associated risk. The evaluator may further detect the risk for non consideration of the various

natures of the distinct risk factors. The identified risk may also be seen to be related to the

diverse errors in the specific bookkeeper. With this essence the main form of the inherent risk

may arise in terms of the DIPL business operations (Ryoo et al., 2014).

The given study has shown the numerous transactions which are particularly omitted by

the accountants or the management of the corporation of DIPL. This can however be sequentially

avoided by DIPL. The corporation has direct lead towards the various types of the

inconsistencies which will be ineffective based on the planning of the sales activities. In addition

to this, the financial declarations of the firm has revealed about the preferred level of profit from

the revenue which has been considered from the sales. The management of the firm may decide

to specify the requirement and the consequent adjustments which need to be made based on the

functionality of the corporation. It can be hereby stated that the DIPL has led to failure for

analysing of the micro and the macro economic factors and associating the existence of the same

in the social and political factors. The subsequent consideration has been further seen to be

reflected as per the poor sales figure and the inherent risks.

5AUDIT ASSURANCE AND COMPLIANCE

The firm has stated about the various nature of the inherent risk. The main consideration

for this has been based on the lack of expertise and the proficiency of the employees of the

corporation along with the escalated issues. The specific business concern has been dependent on

the members of the staff to prove their competency. In addition to this, the various types of the

non-proficient workforce will be able to enhance the inherent risk of making mistakes, errors

associated to the exclusion and other announcements made by the firm (Carey et al., 2013).

The significant aspects of the risks have been further seen to be categorised as per the

material misstatements, environmental risks and the consideration of the falsified exercises. The

environmental consideration has been made as per the internal risk and the associated valuation

for the major issues of stiff competition, inventory and generic market along with the shortage in

the capital. The corporation will be further able to consider the material misstatements which

have been directed for the inherent risk.

The present DIP case has reflected on the various types of the complexities and the

difficulties on the succession process of CEO based on the inherent risk. The succession of the

CEO has been further able to consider the individual candidates. There has been several risks

which has been further associated to the quality of the selection procedure. The process which

are not complying with the initiating the process and the strategy has been considered for

inadequate involvement of the CEO and the candidate’s departure from the firm (Al-khaddash et

al., 2013).

The case study has shown the implementation process of IT infrastructure has generated

significant problems. DIPL does not have adequate staff for execution and the installation of the

reconciliation process which is necessary for making prior arrangement at the end of the year.

The firm has stated about the various nature of the inherent risk. The main consideration

for this has been based on the lack of expertise and the proficiency of the employees of the

corporation along with the escalated issues. The specific business concern has been dependent on

the members of the staff to prove their competency. In addition to this, the various types of the

non-proficient workforce will be able to enhance the inherent risk of making mistakes, errors

associated to the exclusion and other announcements made by the firm (Carey et al., 2013).

The significant aspects of the risks have been further seen to be categorised as per the

material misstatements, environmental risks and the consideration of the falsified exercises. The

environmental consideration has been made as per the internal risk and the associated valuation

for the major issues of stiff competition, inventory and generic market along with the shortage in

the capital. The corporation will be further able to consider the material misstatements which

have been directed for the inherent risk.

The present DIP case has reflected on the various types of the complexities and the

difficulties on the succession process of CEO based on the inherent risk. The succession of the

CEO has been further able to consider the individual candidates. There has been several risks

which has been further associated to the quality of the selection procedure. The process which

are not complying with the initiating the process and the strategy has been considered for

inadequate involvement of the CEO and the candidate’s departure from the firm (Al-khaddash et

al., 2013).

The case study has shown the implementation process of IT infrastructure has generated

significant problems. DIPL does not have adequate staff for execution and the installation of the

reconciliation process which is necessary for making prior arrangement at the end of the year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT ASSURANCE AND COMPLIANCE

The initial testing has shown that the transaction has not seen to be considered properly in the

given time span. This has been further seen to be based on the various considerations of material

misstatements and the inherent factors which are necessary for the considerations of the

omissions and the financial declarations.

The cash receipts have been recorded by the finance professionals and they might

consider the various types of the internal risks. The members of the staff need to follow the

sequence as per the accounts receivable registered and the recording of the same in terms of the

bank reconciliation statements. The revenue registration has been generated from the e-book and

taking into consideration for reprinting the textbooks and upcoming period off the internal risks

and the complexity of the process (Mihret, 2014).

Risk and way it might affect the risk of material misstatement in the financial report

The inherent risk is considered as per the particular assertions made in terms of the

material misstatement.

Excessive pressure on employees and management- The excessive workload of the staff has

led to poor bookkeeping. The propensity of the certain aspects has been further considered as per

the poor liquidity, cash flow issues and outcomes of the poor operating outcomes.

Risks of errors or else incorrect misrepresentation- The intricacy and the reliability have been

related to the risks of errors of misrepresentation.

Integrity of the entire management – The management of DIPL, has been able to consider the

essential drawback of the required integrity and prepared with the reputation loss and entire

community of the business (Lee & Talen, 2014).

The initial testing has shown that the transaction has not seen to be considered properly in the

given time span. This has been further seen to be based on the various considerations of material

misstatements and the inherent factors which are necessary for the considerations of the

omissions and the financial declarations.

The cash receipts have been recorded by the finance professionals and they might

consider the various types of the internal risks. The members of the staff need to follow the

sequence as per the accounts receivable registered and the recording of the same in terms of the

bank reconciliation statements. The revenue registration has been generated from the e-book and

taking into consideration for reprinting the textbooks and upcoming period off the internal risks

and the complexity of the process (Mihret, 2014).

Risk and way it might affect the risk of material misstatement in the financial report

The inherent risk is considered as per the particular assertions made in terms of the

material misstatement.

Excessive pressure on employees and management- The excessive workload of the staff has

led to poor bookkeeping. The propensity of the certain aspects has been further considered as per

the poor liquidity, cash flow issues and outcomes of the poor operating outcomes.

Risks of errors or else incorrect misrepresentation- The intricacy and the reliability have been

related to the risks of errors of misrepresentation.

Integrity of the entire management – The management of DIPL, has been able to consider the

essential drawback of the required integrity and prepared with the reputation loss and entire

community of the business (Lee & Talen, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT ASSURANCE AND COMPLIANCE

Unusual pressure on management – The existing incentive in terms of the management and the

misstatements in the declarations.

Nature of entity business – DIPL has considered as per the competitive aspects. The main

consideration of the overall internal risk is essential for audit analysis and the structure of the

audit plan in an effective way(Wang et al., 2013).

Answer to Question 3:

A) Identification and explanation of two key fraud risk factors relating to

misstatements arising from fraudulent financial reporting

Identification of the fraud risk leads to considerable amount of losses pertaining to the material

misstatement.

Asset Loss In various cases the losses of the assets has led to several instances of fraud. The

workforce dissatisfaction has further considered from the excessive workload

among the employees which can be considered for the fraud. The expectation of

the investors need to report the specific considerations of the management to

attain the appropriate performance leading to fraud risk. The strong pressures to

declare the specific financial are outcomes to generate the guarantees.

Financial reporting

fraud

The major involvement of the risks pertaining to fraud has been further seen to

be considered as per the operations of DIPL, which includes the workforce

engagement of the fraudulent activities. As per the given case the DIPL

operations management remains a challenge pertaining to the novel accounting

system. The enormous pressure on the employees has been further seen to be

based on the installation of the new IT system, which might lead to accounting.

This has been further able to imply that the fraudulent activity related to handle

Unusual pressure on management – The existing incentive in terms of the management and the

misstatements in the declarations.

Nature of entity business – DIPL has considered as per the competitive aspects. The main

consideration of the overall internal risk is essential for audit analysis and the structure of the

audit plan in an effective way(Wang et al., 2013).

Answer to Question 3:

A) Identification and explanation of two key fraud risk factors relating to

misstatements arising from fraudulent financial reporting

Identification of the fraud risk leads to considerable amount of losses pertaining to the material

misstatement.

Asset Loss In various cases the losses of the assets has led to several instances of fraud. The

workforce dissatisfaction has further considered from the excessive workload

among the employees which can be considered for the fraud. The expectation of

the investors need to report the specific considerations of the management to

attain the appropriate performance leading to fraud risk. The strong pressures to

declare the specific financial are outcomes to generate the guarantees.

Financial reporting

fraud

The major involvement of the risks pertaining to fraud has been further seen to

be considered as per the operations of DIPL, which includes the workforce

engagement of the fraudulent activities. As per the given case the DIPL

operations management remains a challenge pertaining to the novel accounting

system. The enormous pressure on the employees has been further seen to be

based on the installation of the new IT system, which might lead to accounting.

This has been further able to imply that the fraudulent activity related to handle

8AUDIT ASSURANCE AND COMPLIANCE

the procedure for reconciliation done in an inappropriate manner with the

subsequent misstatement in the material. The case study has been also able to

consider the various processes for the execution related to the implementation

of the certain transactions which has been considered in the end of each year.

This may further lead to losses for the fraud risk and the material misstatements

(Jans et al., 2013).

Unsuitable average

cost

Another important financial reporting has been further considered as per the

financial fraud reporting. During the time of excessive expectation from the

outside financiers, the financial announcements needs to meet with the specific

performance related to meet with the qualification of the goal criteria and the

high amount of the risk related to the improper announcement of the finance.

The various information of the financial position has been further seen to be

based on the revenue of DIPL which has increased from 2013-2015.

Furthermore, the current and the total assets for DIPL have also increased

considerably. As per the given situation the valuation of the raw materials from

the inventory cost was not seen to be suitable for the present cost on paper,

which was considerably higher than the average costs. The risk of the

identification of the fraudulent acts are involves as per the implementation of

the new information technology systems, which can be carried out based on the

monitoring of the various activities in various phases. The financial risk of the

reporting has been based on the evaluation carried as per the monitoring,

assessing and control of the mechanisms.

the procedure for reconciliation done in an inappropriate manner with the

subsequent misstatement in the material. The case study has been also able to

consider the various processes for the execution related to the implementation

of the certain transactions which has been considered in the end of each year.

This may further lead to losses for the fraud risk and the material misstatements

(Jans et al., 2013).

Unsuitable average

cost

Another important financial reporting has been further considered as per the

financial fraud reporting. During the time of excessive expectation from the

outside financiers, the financial announcements needs to meet with the specific

performance related to meet with the qualification of the goal criteria and the

high amount of the risk related to the improper announcement of the finance.

The various information of the financial position has been further seen to be

based on the revenue of DIPL which has increased from 2013-2015.

Furthermore, the current and the total assets for DIPL have also increased

considerably. As per the given situation the valuation of the raw materials from

the inventory cost was not seen to be suitable for the present cost on paper,

which was considerably higher than the average costs. The risk of the

identification of the fraudulent acts are involves as per the implementation of

the new information technology systems, which can be carried out based on the

monitoring of the various activities in various phases. The financial risk of the

reporting has been based on the evaluation carried as per the monitoring,

assessing and control of the mechanisms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT ASSURANCE AND COMPLIANCE

References

Al-khaddash, H., Nawas, R. Al, & Ramadan, A. (2013). Factors affecting the quality of

Auditing : The Case of Jordanian Commercial Banks. International Journal of Business and

Social Science, 4(11), 206–222.

Carey, P., Knechel, W. R., & Tanewski, G. (2013). Costs and Benefits of Mandatory Auditing of

For-profit Private and Not-for-profit Companies in Australia. Australian Accounting

Review, 23(1), 43–53. https://doi.org/10.1111/auar.12003

Jans, M., Alles, M., & Vasarhelyi, M. (2013). The case for process mining in auditing: Sources

of value added and areas of application. International Journal of Accounting Information

Systems, 14(1), 1–20. https://doi.org/10.1016/j.accinf.2012.06.015

Lee, S., & Talen, E. (2014). Measuring Walkability: A Note on Auditing Methods. Journal of

Urban Design, 19(3), 368–388. https://doi.org/10.1080/13574809.2014.890040

Mihret, D. G. (2014). How can we explain internal auditing? The inadequacy of agency theory

and a labor process alternative. Critical Perspectives on Accounting, 25(8), 771–782.

https://doi.org/10.1016/j.cpa.2014.01.003

Regoliosi, C., & d’Eri, A. (2014). “Good” corporate governance and the quality of internal

auditing departments in Italian listed firms. An exploratory investigation in Italian listed

firms. Journal of Management and Governance, 18(3), 891–920.

https://doi.org/10.1007/s10997-012-9254-1

Ryoo, J., Rizvi, S., Aiken, W., & Kissell, J. (2014). Cloud Security Auditing: Challenges and

Emerging Approaches. IEEE Security & Privacy, 12(6), 68–74.

References

Al-khaddash, H., Nawas, R. Al, & Ramadan, A. (2013). Factors affecting the quality of

Auditing : The Case of Jordanian Commercial Banks. International Journal of Business and

Social Science, 4(11), 206–222.

Carey, P., Knechel, W. R., & Tanewski, G. (2013). Costs and Benefits of Mandatory Auditing of

For-profit Private and Not-for-profit Companies in Australia. Australian Accounting

Review, 23(1), 43–53. https://doi.org/10.1111/auar.12003

Jans, M., Alles, M., & Vasarhelyi, M. (2013). The case for process mining in auditing: Sources

of value added and areas of application. International Journal of Accounting Information

Systems, 14(1), 1–20. https://doi.org/10.1016/j.accinf.2012.06.015

Lee, S., & Talen, E. (2014). Measuring Walkability: A Note on Auditing Methods. Journal of

Urban Design, 19(3), 368–388. https://doi.org/10.1080/13574809.2014.890040

Mihret, D. G. (2014). How can we explain internal auditing? The inadequacy of agency theory

and a labor process alternative. Critical Perspectives on Accounting, 25(8), 771–782.

https://doi.org/10.1016/j.cpa.2014.01.003

Regoliosi, C., & d’Eri, A. (2014). “Good” corporate governance and the quality of internal

auditing departments in Italian listed firms. An exploratory investigation in Italian listed

firms. Journal of Management and Governance, 18(3), 891–920.

https://doi.org/10.1007/s10997-012-9254-1

Ryoo, J., Rizvi, S., Aiken, W., & Kissell, J. (2014). Cloud Security Auditing: Challenges and

Emerging Approaches. IEEE Security & Privacy, 12(6), 68–74.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT ASSURANCE AND COMPLIANCE

https://doi.org/10.1109/MSP.2013.132

Wang, C., Chow, S. S. M., Wang, Q., Ren, K., & Lou, W. (2013). Privacy-preserving public

auditing for secure cloud storage. IEEE Transactions on Computers, 62(2), 362–375.

https://doi.org/10.1109/TC.2011.245

Yang, K., & Jia, X. (2013). An efficient and secure dynamic auditing protocol for data storage in

cloud computing. IEEE Transactions on Parallel and Distributed Systems, 24(9), 1717–

1726. https://doi.org/10.1109/TPDS.2012.278

https://doi.org/10.1109/MSP.2013.132

Wang, C., Chow, S. S. M., Wang, Q., Ren, K., & Lou, W. (2013). Privacy-preserving public

auditing for secure cloud storage. IEEE Transactions on Computers, 62(2), 362–375.

https://doi.org/10.1109/TC.2011.245

Yang, K., & Jia, X. (2013). An efficient and secure dynamic auditing protocol for data storage in

cloud computing. IEEE Transactions on Parallel and Distributed Systems, 24(9), 1717–

1726. https://doi.org/10.1109/TPDS.2012.278

11AUDIT ASSURANCE AND COMPLIANCE

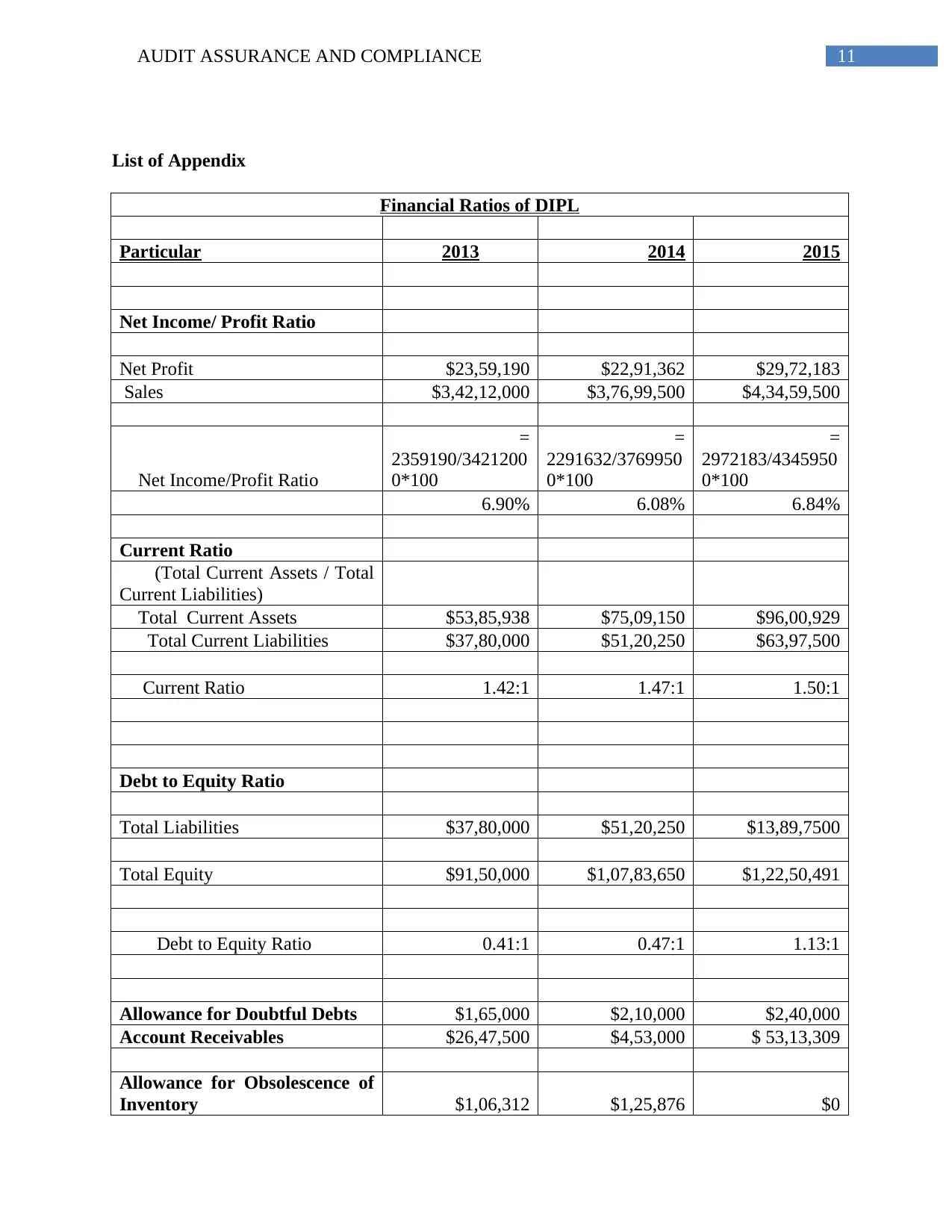

List of Appendix

Financial Ratios of DIPL

Particular 2013 2014 2015

Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

Current Ratio

(Total Current Assets / Total

Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilities $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

Allowance for Doubtful Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence of

Inventory $1,06,312 $1,25,876 $0

List of Appendix

Financial Ratios of DIPL

Particular 2013 2014 2015

Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

Current Ratio

(Total Current Assets / Total

Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilities $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

Allowance for Doubtful Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence of

Inventory $1,06,312 $1,25,876 $0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.