Audit Assurance 12 Report on Audit Assurance and Compliance

VerifiedAdded on 2020/03/04

|15

|2935

|70

Report

AI Summary

This report provides a comprehensive analysis of audit assurance and compliance, focusing on Double Ink Printers Ltd (DIPL). It begins by applying analytical procedures to DIPL's financial reports over three years, explaining how the results influence audit planning decisions. The report then identifies inherent risk factors arising from DIPL's business operations, such as copyright challenges and author grants, and explains their potential impact on material misstatements. Finally, it examines fraud risk factors, including incentives and opportunities, and discusses how these factors affect the conduct of the audit. The report covers various financial ratios, copyright issues, privacy concerns, and the effects of market competition on audit procedures, offering insights into the complexities of financial auditing within the publishing industry.

Audit Assurance 1

Report on Audit Assurance and Compliance Risk

Report on Audit Assurance and Compliance Risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Assurance 2

Table of Contents

Introduction:...............................................................................................................................4

Question 1:.................................................................................................................................5

Apply analytical procedures to the financial report information of DIPL for the last three

years. Explain how your results influence your planning decisions for the audit for the year

ending 30 June 2015...................................................................................................................5

Question 2..................................................................................................................................7

Identify two inherent risk factors that arise from the nature of DIPL’s business operations.

Explain why it is a risk and how it may affect the risk of material misstatement in the

financial report...........................................................................................................................7

Question 3: As part of your audit of DIPL for the year ended 30 June 2015, you are

considering the risk that fraud may have occurred..................................................................10

(a) Based on the background information for DIPL contained in the case, identify and

explain two key fraud risk factors relating to misstatements arising from fraudulent

financial reporting to which DIPL may be susceptible........................................................10

(b) Explain how the risk factors identified in (a) above would affect the conduct of the (a)

audit......................................................................................................................................11

Conclusion:..............................................................................................................................13

References................................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................4

Question 1:.................................................................................................................................5

Apply analytical procedures to the financial report information of DIPL for the last three

years. Explain how your results influence your planning decisions for the audit for the year

ending 30 June 2015...................................................................................................................5

Question 2..................................................................................................................................7

Identify two inherent risk factors that arise from the nature of DIPL’s business operations.

Explain why it is a risk and how it may affect the risk of material misstatement in the

financial report...........................................................................................................................7

Question 3: As part of your audit of DIPL for the year ended 30 June 2015, you are

considering the risk that fraud may have occurred..................................................................10

(a) Based on the background information for DIPL contained in the case, identify and

explain two key fraud risk factors relating to misstatements arising from fraudulent

financial reporting to which DIPL may be susceptible........................................................10

(b) Explain how the risk factors identified in (a) above would affect the conduct of the (a)

audit......................................................................................................................................11

Conclusion:..............................................................................................................................13

References................................................................................................................................14

Audit Assurance 3

Introduction:

The basic propose lying behind the preparation of this report is to develop the understanding

on the audit assurance and compliance. This case problem is based on the organization of

Double Ink Printers Ltd (DIPL). This report will focus on analysis of DIPL financial reports

for the three years. At the same time, report also has a focus on the study of decision related

to planning of the audit in organization. On the other hand, this report also focuses on the

inherent risk factors in auditing. In this report, there is also a discussion on how inherent risk

factors affect the risk of misstatement in the financial reports. Finally, this case study focuses

on analysis of different fraud risk factors, which are related to the misstatements arising

through the fraudulent financial reports.

Introduction:

The basic propose lying behind the preparation of this report is to develop the understanding

on the audit assurance and compliance. This case problem is based on the organization of

Double Ink Printers Ltd (DIPL). This report will focus on analysis of DIPL financial reports

for the three years. At the same time, report also has a focus on the study of decision related

to planning of the audit in organization. On the other hand, this report also focuses on the

inherent risk factors in auditing. In this report, there is also a discussion on how inherent risk

factors affect the risk of misstatement in the financial reports. Finally, this case study focuses

on analysis of different fraud risk factors, which are related to the misstatements arising

through the fraudulent financial reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit Assurance 4

Question 1: Apply analytical procedures to the financial report information of DIPL for

the last three years. Explain how your results influence your planning decisions for the

audit for the year ending 30 June 2015

Basically, the Double Ink Printers Limited is engaged in the business of printing of books and

magazines, advertising materials for different articles, trading in different books on the basis

of demand. The company use to print the exact number of books that it has received in its

orders from different customers. Company provides a fee of 5% of its revenue to the

publishers for publish its books. Short term turnover policy has followed by the organisation.

Apart from this, the company is also going to start its online portal in order to publish its

books and magazines (Collis and Hussey, 2013).

Analytical procedure can be defined as a set of methods and procedures that is used for the

purpose of analysing the approximate relationships between the financial and non-financial

aspect of data on order to evaluate the financial facts and findings of the company. They are

also done to find out deviations that are occurring due to other related information. Expecting

the existence of approximate relationship between various data provides the basic premise for

the application of analytical procedure (Lobo and Zhao, 2013).

There are four stages comprising the analytical procedures:

Developing an independent expectation’: This is the initial stage of analytical procedure.

Developing an expectation for recorded amount or data comprises this step. Every auditor is

required to develop an independent expectation about the data. Identification of relationships

between the financial and non-financial aspect of data can help the auditor in developing this.

Defining a significant variation’: Before proceeding the analytical procedure, the auditors

are required to develop a reasonable difference between expected data and the data provided

Question 1: Apply analytical procedures to the financial report information of DIPL for

the last three years. Explain how your results influence your planning decisions for the

audit for the year ending 30 June 2015

Basically, the Double Ink Printers Limited is engaged in the business of printing of books and

magazines, advertising materials for different articles, trading in different books on the basis

of demand. The company use to print the exact number of books that it has received in its

orders from different customers. Company provides a fee of 5% of its revenue to the

publishers for publish its books. Short term turnover policy has followed by the organisation.

Apart from this, the company is also going to start its online portal in order to publish its

books and magazines (Collis and Hussey, 2013).

Analytical procedure can be defined as a set of methods and procedures that is used for the

purpose of analysing the approximate relationships between the financial and non-financial

aspect of data on order to evaluate the financial facts and findings of the company. They are

also done to find out deviations that are occurring due to other related information. Expecting

the existence of approximate relationship between various data provides the basic premise for

the application of analytical procedure (Lobo and Zhao, 2013).

There are four stages comprising the analytical procedures:

Developing an independent expectation’: This is the initial stage of analytical procedure.

Developing an expectation for recorded amount or data comprises this step. Every auditor is

required to develop an independent expectation about the data. Identification of relationships

between the financial and non-financial aspect of data can help the auditor in developing this.

Defining a significant variation’: Before proceeding the analytical procedure, the auditors

are required to develop a reasonable difference between expected data and the data provided

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Assurance 5

by the company. This is necessary in appropriate application of the procedure and to remove

biasness from data.

Calculation of variances: This step is dedicated towards the calculating the differences

between the expected data and actual data. This should only do after applying the significant

amount of expected data. This should not be calculated without this application.

Analysing variations and interfering conclusions: This is the last step of the procedure.

This step is dedicated towards the analysing the variances that are computed in the previous

step and then drawing conclusions on the basis of them.

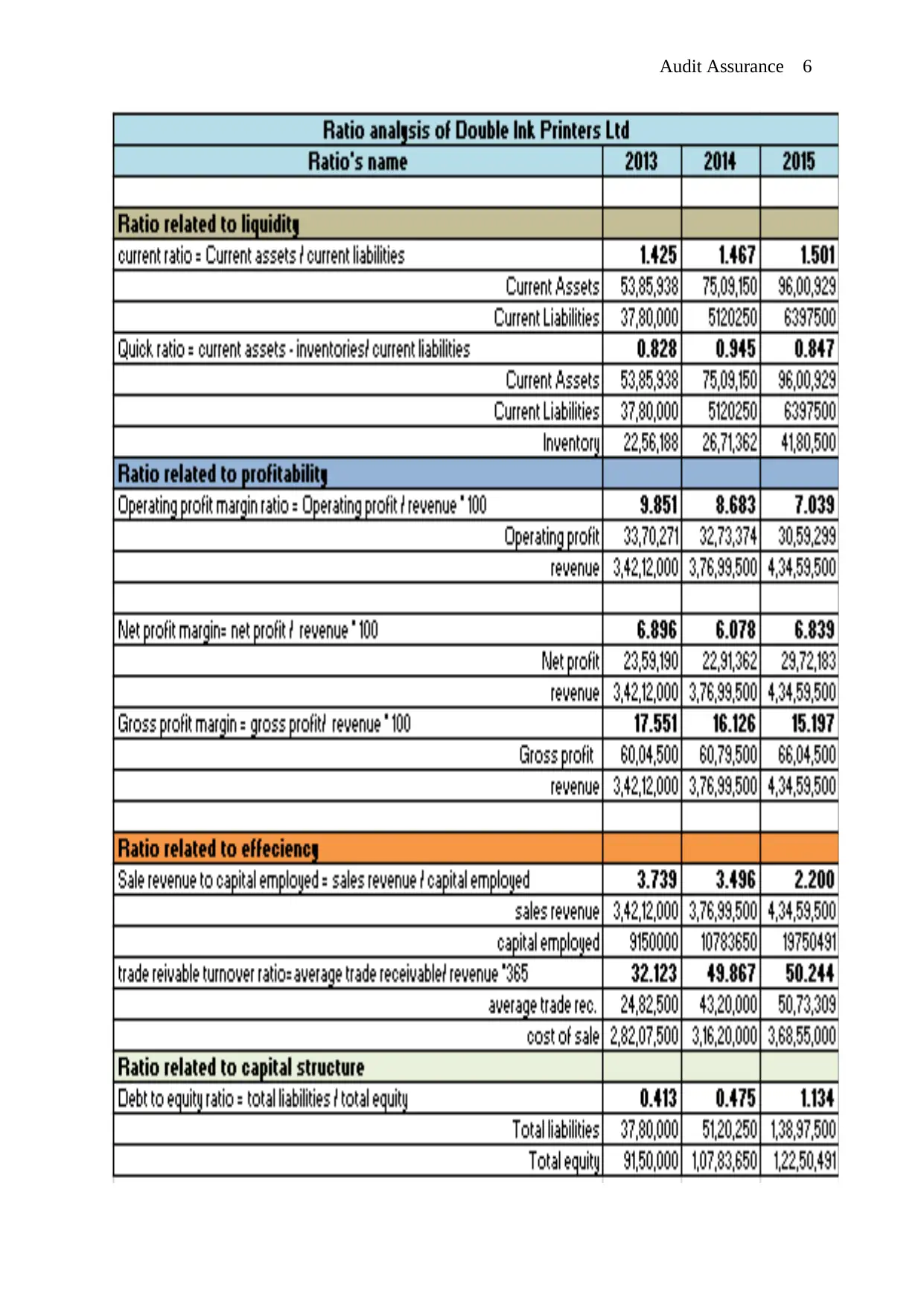

On the basis of the financial information given in this report, it can be said that the liquid

assets of the company has fallen this year as compared to previous two years. The value of its

long term assets increases two times that shows a good sign for the company. Along with

this, the liabilities of company also increases that shows a pressure on the assets of the

company. Current ratio of the company increases from 1.425 to 1.501. Quick ratio of the

company also increases from 0.828 to 0.847 which shows the better functioning of the

company. Operating profit of the company declines from 9.851 to 7.039 over the time which

shows the deficiency in the functioning of organisation. Net profit margin ration does not

vary and remains almost same at 0.84. Gross profit ratio of the company also goes on

declining which shows decline in operational efficiency. Capital employed ratio has

decreased from 3.739 to 2.200 which show leverage to capital. Trade receivables ratio has

also increased from 32.123 to 50.244 which show the increased debtor period. Debt equity

ratio has also increased from 0.413 to 1.134 (Saaty and Kearns, 2014).

by the company. This is necessary in appropriate application of the procedure and to remove

biasness from data.

Calculation of variances: This step is dedicated towards the calculating the differences

between the expected data and actual data. This should only do after applying the significant

amount of expected data. This should not be calculated without this application.

Analysing variations and interfering conclusions: This is the last step of the procedure.

This step is dedicated towards the analysing the variances that are computed in the previous

step and then drawing conclusions on the basis of them.

On the basis of the financial information given in this report, it can be said that the liquid

assets of the company has fallen this year as compared to previous two years. The value of its

long term assets increases two times that shows a good sign for the company. Along with

this, the liabilities of company also increases that shows a pressure on the assets of the

company. Current ratio of the company increases from 1.425 to 1.501. Quick ratio of the

company also increases from 0.828 to 0.847 which shows the better functioning of the

company. Operating profit of the company declines from 9.851 to 7.039 over the time which

shows the deficiency in the functioning of organisation. Net profit margin ration does not

vary and remains almost same at 0.84. Gross profit ratio of the company also goes on

declining which shows decline in operational efficiency. Capital employed ratio has

decreased from 3.739 to 2.200 which show leverage to capital. Trade receivables ratio has

also increased from 32.123 to 50.244 which show the increased debtor period. Debt equity

ratio has also increased from 0.413 to 1.134 (Saaty and Kearns, 2014).

Audit Assurance 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit Assurance 7

Question 2: Identify two inherent risk factors that arise from the nature of DIPL’s

business operations. Explain why it is a risk and how it may affect the risk of material

misstatement in the financial report.

Inherent Risk: Inherent risk is the term, which is pretended through mistake and exclusion

within a financial statement (Merna and Al-Thani, 2011). This is because of a factor, which is

not a failure of control. The situations, in which inherent risk is frequent to occur in financial

audit, are as below:

- when relations are complex

- In those situations that need high degree of decision making, keeping the financial

estimations in mind.

Inherent risk is a form of risk that represents the worst-case situation, when all controls are

botched. Auditors and predictors should look for inherent risk before studying the financial

statements. This should be done along with detection risk or control risk (Loughran 2017).

There are several types of risks associated with publishing companies like:

Copyright challenges: The copyright context is the most valuable assets of the book

publishers in the books. It is a copyright tool in the hands of companies. Besides this, it is

provided in the framework, which enables the publishers to control content. This term

permits them to earn money with selling books or licensing subsidiary right like book club,

serial, adaptation, merchandising or foreign translation (Song, 2011). Therefore, a type of

legal challenge with the context of patent context is challenge in order to learn that how to

understand, avoid or exploit infringement of copyrights. There are different types of

copyrights such as author grants, copyright licenses, copyright procedures, protecting against

infringement, internet and electronic uses. The expiry of patents of companies can also affect

the audit operations.

Question 2: Identify two inherent risk factors that arise from the nature of DIPL’s

business operations. Explain why it is a risk and how it may affect the risk of material

misstatement in the financial report.

Inherent Risk: Inherent risk is the term, which is pretended through mistake and exclusion

within a financial statement (Merna and Al-Thani, 2011). This is because of a factor, which is

not a failure of control. The situations, in which inherent risk is frequent to occur in financial

audit, are as below:

- when relations are complex

- In those situations that need high degree of decision making, keeping the financial

estimations in mind.

Inherent risk is a form of risk that represents the worst-case situation, when all controls are

botched. Auditors and predictors should look for inherent risk before studying the financial

statements. This should be done along with detection risk or control risk (Loughran 2017).

There are several types of risks associated with publishing companies like:

Copyright challenges: The copyright context is the most valuable assets of the book

publishers in the books. It is a copyright tool in the hands of companies. Besides this, it is

provided in the framework, which enables the publishers to control content. This term

permits them to earn money with selling books or licensing subsidiary right like book club,

serial, adaptation, merchandising or foreign translation (Song, 2011). Therefore, a type of

legal challenge with the context of patent context is challenge in order to learn that how to

understand, avoid or exploit infringement of copyrights. There are different types of

copyrights such as author grants, copyright licenses, copyright procedures, protecting against

infringement, internet and electronic uses. The expiry of patents of companies can also affect

the audit operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Assurance 8

Author Grants: The first step that lies with the publishing process is to order accurately to

acquire rights through the author. This could be done in the two ways. The mainly operator

publishers become exclusive licensees of every copyrights generated with their writers. On

the other hand, most scholastic or expert publishers, rather to be assignees of these

copyrights, thus obtaining a complete ownership concern. Although, from these variations,

almost every publisher is knowing the writers right in order to improve their copyrights when

their books withdraw of print or the publisher stop in order to utilize these rights (McElrath,

2013). Along with this, lot of publishers are required to allow the writers for the purpose of

retention of certain subsidiary rights like theatrical, television or movie and electronic rights.

Protection against Infringement: This is the one of the copyright forms, which assesses the

applying measures or guides individuals to encourage the proper use or non- infringement of

the rights of others. During the frequent writings, writers start having warrant, which their

works do not infringe third-party rights as well as at being required to indemnify publishers

for breach, publisher want like “tough love” provisions in order to force writers to take these

problems seriously. Normally, former writers take legal actions, which they hold someone

responsible for infringements as well as privacy violations, defamation or similar issues (Wei,

2012). Writers have to cooperate with publishers in identifying potential problems or helping

to resolve them in proceeds.

Privacy and Public issues: Writers put off the challenges in front of publishers to approach

through the sifting limits of the laws of publicity, privacy or libel.

Privacy Rights: The privacy right can be defined as the right of an individual to protect

his/her personal identity from unauthentic persons. Privacy is in the company that publishes

the magazines or newspapers can be related to identity of personal details of writers (Bridges,

Author Grants: The first step that lies with the publishing process is to order accurately to

acquire rights through the author. This could be done in the two ways. The mainly operator

publishers become exclusive licensees of every copyrights generated with their writers. On

the other hand, most scholastic or expert publishers, rather to be assignees of these

copyrights, thus obtaining a complete ownership concern. Although, from these variations,

almost every publisher is knowing the writers right in order to improve their copyrights when

their books withdraw of print or the publisher stop in order to utilize these rights (McElrath,

2013). Along with this, lot of publishers are required to allow the writers for the purpose of

retention of certain subsidiary rights like theatrical, television or movie and electronic rights.

Protection against Infringement: This is the one of the copyright forms, which assesses the

applying measures or guides individuals to encourage the proper use or non- infringement of

the rights of others. During the frequent writings, writers start having warrant, which their

works do not infringe third-party rights as well as at being required to indemnify publishers

for breach, publisher want like “tough love” provisions in order to force writers to take these

problems seriously. Normally, former writers take legal actions, which they hold someone

responsible for infringements as well as privacy violations, defamation or similar issues (Wei,

2012). Writers have to cooperate with publishers in identifying potential problems or helping

to resolve them in proceeds.

Privacy and Public issues: Writers put off the challenges in front of publishers to approach

through the sifting limits of the laws of publicity, privacy or libel.

Privacy Rights: The privacy right can be defined as the right of an individual to protect

his/her personal identity from unauthentic persons. Privacy is in the company that publishes

the magazines or newspapers can be related to identity of personal details of writers (Bridges,

Audit Assurance 9

2017). In this, up-to- the- minute reporting may propel the disclosure of facts which should

be made public, including medical, financial and other highly personal information.

Publicity rights: It is directly associated with the right of publicity. Usually, the rights of

publicity prevent the commercial exploitation of the value of a personal name or likeness.

The publicity rights not only protect the celebrities or others, whose names or appearances

are real commercial, or value (Dreyfuss and Ginsburg, 2014). It also avoids the usage of

another name and likeness within advertising and trade without their permission.

2017). In this, up-to- the- minute reporting may propel the disclosure of facts which should

be made public, including medical, financial and other highly personal information.

Publicity rights: It is directly associated with the right of publicity. Usually, the rights of

publicity prevent the commercial exploitation of the value of a personal name or likeness.

The publicity rights not only protect the celebrities or others, whose names or appearances

are real commercial, or value (Dreyfuss and Ginsburg, 2014). It also avoids the usage of

another name and likeness within advertising and trade without their permission.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit Assurance 10

Question 3: As part of your audit of DIPL for the year ended 30 June 2015, you are

considering the risk that fraud may have occurred

(a) Based on the background information for DIPL contained in the case, identify and

explain two key fraud risk factors relating to misstatements arising from fraudulent

financial reporting to which DIPL may be susceptible.

There are two major types of fraud risk factors relating to misstatements arising from

fraudulent financial reporting.

Incentives related factor

Prevailing of high degree of competition in the market results in falling down of the

profit margins

Rapid changes in technology negatively hamper the functioning of an organisation

Severe situations like insolvency, foreclosure may be created due to losses occurs in

operation of business

Continuous occurrence of negative balances reveals the disability of business in

generating the revenues (Knechel and et al., 2016)

Continuous falling in the level of demand may results in shut down of business units

in the economy

Continuous amendments in statutory requirements often creates hurdles in the path of

effective business operations

Companies may often requires the additional debt and equity

Opportunities Factor

Ordinary course of business sometimes do not includes transactions specified to a

business

Question 3: As part of your audit of DIPL for the year ended 30 June 2015, you are

considering the risk that fraud may have occurred

(a) Based on the background information for DIPL contained in the case, identify and

explain two key fraud risk factors relating to misstatements arising from fraudulent

financial reporting to which DIPL may be susceptible.

There are two major types of fraud risk factors relating to misstatements arising from

fraudulent financial reporting.

Incentives related factor

Prevailing of high degree of competition in the market results in falling down of the

profit margins

Rapid changes in technology negatively hamper the functioning of an organisation

Severe situations like insolvency, foreclosure may be created due to losses occurs in

operation of business

Continuous occurrence of negative balances reveals the disability of business in

generating the revenues (Knechel and et al., 2016)

Continuous falling in the level of demand may results in shut down of business units

in the economy

Continuous amendments in statutory requirements often creates hurdles in the path of

effective business operations

Companies may often requires the additional debt and equity

Opportunities Factor

Ordinary course of business sometimes do not includes transactions specified to a

business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Assurance 11

A firm holding strong position in terms of financial status or having the potential to

influence the other company’s decisions may involve in doing extra length

transactions.

Judgements or uncertainties based on the forecast of revenues, expenses, assets and

liabilities are difficult to confirmations

Differences in business culture and environment often creates problems in effective

operations when business is carried beyond the geographical boundaries of a country

Having branches of a business on different countries generally faces the problems of

compiling with the tax norms of the country in which business is running

Ineffective group of board of directors and committee of auditing may results in

development of misunderstanding about financial reports (Sadgrove, 2016).

(b) Explain how the risk factors identified in (a) above would affect the conduct of the

(a) audit.

When high degree of competition prevails in the market, then the whole segments of market

entirely depends on the side of customer. Customer is treated as king of the market in that

scenario. The companies are required to keep prices for their products below the level of

price designed by their competitive in order to increase their sales and capture a good portion

of market. If a company is continuously suffering from operational losses, then it may

become impossible for the company to survive in long run. This loss may occur due to fall in

demand, increase in cost of production. If company does not control its operational losses,

then, it might happen that the company can survive with the severe situations like shut down

of business (Bentley, et al., 2013). It also reveals the poor functioning and mismanagement

among the organisation.

Along with it, if taxation policies continuously amended by the government often creates

problem for companies in compiling with them. It is compulsory for a company by law to

A firm holding strong position in terms of financial status or having the potential to

influence the other company’s decisions may involve in doing extra length

transactions.

Judgements or uncertainties based on the forecast of revenues, expenses, assets and

liabilities are difficult to confirmations

Differences in business culture and environment often creates problems in effective

operations when business is carried beyond the geographical boundaries of a country

Having branches of a business on different countries generally faces the problems of

compiling with the tax norms of the country in which business is running

Ineffective group of board of directors and committee of auditing may results in

development of misunderstanding about financial reports (Sadgrove, 2016).

(b) Explain how the risk factors identified in (a) above would affect the conduct of the

(a) audit.

When high degree of competition prevails in the market, then the whole segments of market

entirely depends on the side of customer. Customer is treated as king of the market in that

scenario. The companies are required to keep prices for their products below the level of

price designed by their competitive in order to increase their sales and capture a good portion

of market. If a company is continuously suffering from operational losses, then it may

become impossible for the company to survive in long run. This loss may occur due to fall in

demand, increase in cost of production. If company does not control its operational losses,

then, it might happen that the company can survive with the severe situations like shut down

of business (Bentley, et al., 2013). It also reveals the poor functioning and mismanagement

among the organisation.

Along with it, if taxation policies continuously amended by the government often creates

problem for companies in compiling with them. It is compulsory for a company by law to

Audit Assurance 12

comply with the legal obligations of tax and audit. But continuous amendments may divert

the focus of the company from its main objective to the meeting with different revised rules

and regulations (Abdullatif, 2013). Taking finance from market and other sources may

increase the pressure of interest and repayments. Firms having potential to influence the

decisions of others may create problems for minor scale firms. Decisions taken on the basis

of past facts and findings without developing the premises for future sometimes may fails in

business case.

comply with the legal obligations of tax and audit. But continuous amendments may divert

the focus of the company from its main objective to the meeting with different revised rules

and regulations (Abdullatif, 2013). Taking finance from market and other sources may

increase the pressure of interest and repayments. Firms having potential to influence the

decisions of others may create problems for minor scale firms. Decisions taken on the basis

of past facts and findings without developing the premises for future sometimes may fails in

business case.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.