Audit, Assurance, Compliance Report: DIPL Financial Analysis and Risks

VerifiedAdded on 2020/03/01

|13

|2968

|47

Report

AI Summary

This report provides a comprehensive analysis of an audit, assurance, and compliance case study focusing on the financial performance and risk assessment of DIPL. It begins by exploring the application of analytical methods, such as common sizing, benchmarking, and ratio analysis, to evaluate DIPL's financial statements and develop an effective audit plan. The report then delves into the identification of inherent risks, including those related to employee experience, environmental factors, and CEO succession, and their potential impact on the accuracy of financial reporting. Furthermore, it examines fraud risks associated with employee dissatisfaction and pressures to meet financial targets, highlighting potential misstatements and fraudulent activities. The analysis includes a detailed examination of financial ratios, such as solvency and current ratios, to assess DIPL's financial position. The report concludes with an assessment of the valuation of inventory and the implementation of a new IT system, providing insights into the complexities of financial auditing and risk management.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Answer to Question 3:.....................................................................................................................7

Answer to Part A:........................................................................................................................7

Answer to Part B:.......................................................................................................................10

References:....................................................................................................................................11

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Answer to Question 3:.....................................................................................................................7

Answer to Part A:........................................................................................................................7

Answer to Part B:.......................................................................................................................10

References:....................................................................................................................................11

2AUDIT, ASSURANCE AND COMPLIANCE

Answer to Question 1:

The analytical method pertaining to the financial information of DIPL could enable in

preparing the audit plan. Such plan could be adjudged as a specific guideline, which is required

to be followed during the undertaking of audit. Specifically, this enables the assessor to maintain

the overall cost of audit at an effective level, which helps in minimising understanding with the

clients (Zureigat 2015). The analytical approach to the financial announcements of DIPL

indicates the procedure of information dissemination from the same. Such evaluation method

could be conducted by using a group of mechanisms. However, with the help of analytical

method of evaluating financial announcements, various financial analysts as well as accountants

could decipher information for enabling in arriving at crucial business decisions (Barr-Pulliam et

al. 2017).

The common sizing analytical method enables in assessing the financial announcements

to a common point of reference. As a result, the financial statements could be contrasted in

relation to various timeframe or in relation to various entities. The assessors could consider the

various item lines depicted in the financial report along with their method of reporting. For

instance, the method of registering items like assets, liabilities and owner’s equity in the financial

reporting of the organisation along with investigating digression from usual scenario (Bayer and

Cowell 2016). Benchmarking is considered as an analytical process and it could be used further

for the assessment of audit plan. The variance of the real financial declaration from the yardstick

enables in recognising the deviation and it assists in evaluating the reason of the identified

variance. Along with this, ratio analysis could be adjudged as an effective analytical method,

Answer to Question 1:

The analytical method pertaining to the financial information of DIPL could enable in

preparing the audit plan. Such plan could be adjudged as a specific guideline, which is required

to be followed during the undertaking of audit. Specifically, this enables the assessor to maintain

the overall cost of audit at an effective level, which helps in minimising understanding with the

clients (Zureigat 2015). The analytical approach to the financial announcements of DIPL

indicates the procedure of information dissemination from the same. Such evaluation method

could be conducted by using a group of mechanisms. However, with the help of analytical

method of evaluating financial announcements, various financial analysts as well as accountants

could decipher information for enabling in arriving at crucial business decisions (Barr-Pulliam et

al. 2017).

The common sizing analytical method enables in assessing the financial announcements

to a common point of reference. As a result, the financial statements could be contrasted in

relation to various timeframe or in relation to various entities. The assessors could consider the

various item lines depicted in the financial report along with their method of reporting. For

instance, the method of registering items like assets, liabilities and owner’s equity in the financial

reporting of the organisation along with investigating digression from usual scenario (Bayer and

Cowell 2016). Benchmarking is considered as an analytical process and it could be used further

for the assessment of audit plan. The variance of the real financial declaration from the yardstick

enables in recognising the deviation and it assists in evaluating the reason of the identified

variance. Along with this, ratio analysis could be adjudged as an effective analytical method,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

which could be used for contrasting financial declarations coupled with the assessment of audit

plan (Bepari and Mollik 2015).

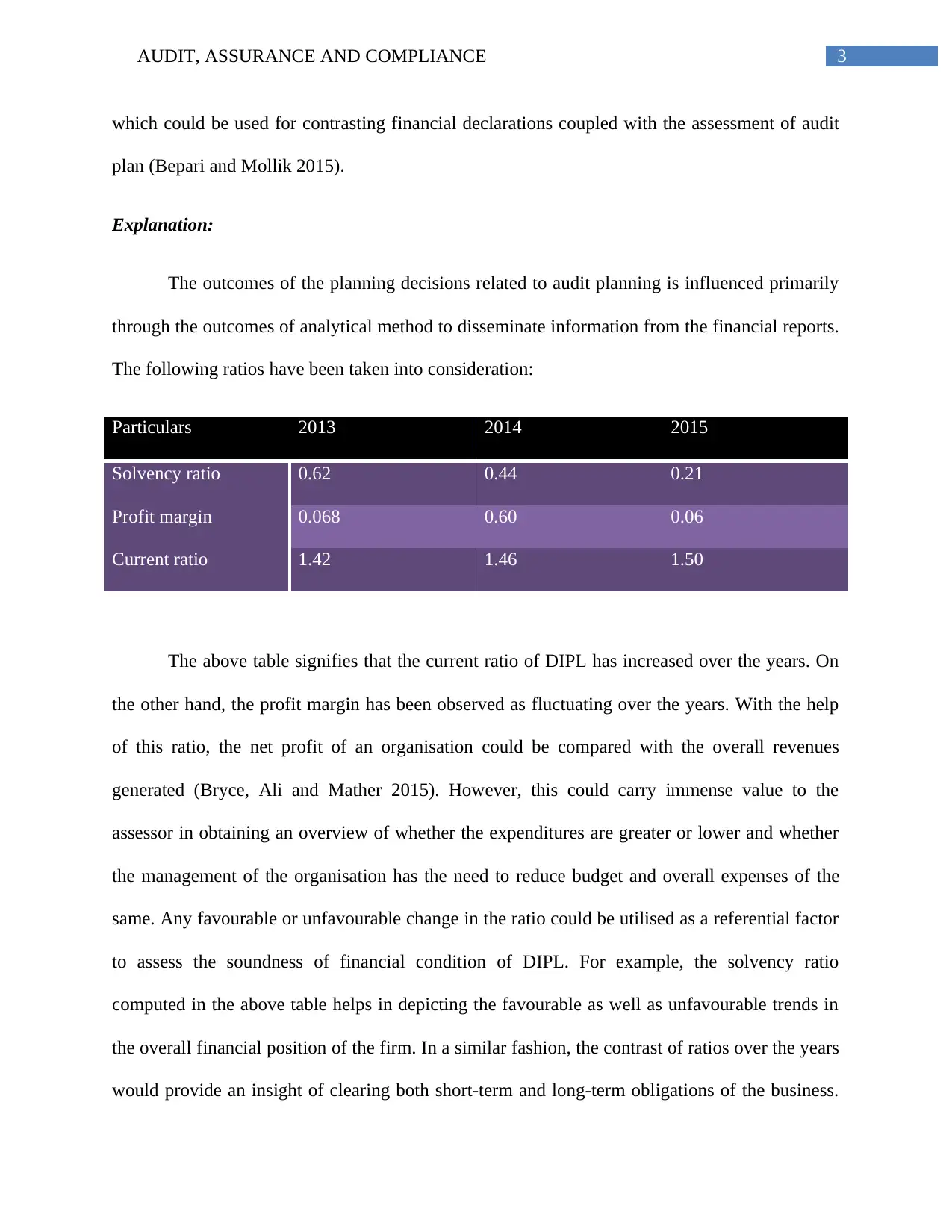

Explanation:

The outcomes of the planning decisions related to audit planning is influenced primarily

through the outcomes of analytical method to disseminate information from the financial reports.

The following ratios have been taken into consideration:

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

The above table signifies that the current ratio of DIPL has increased over the years. On

the other hand, the profit margin has been observed as fluctuating over the years. With the help

of this ratio, the net profit of an organisation could be compared with the overall revenues

generated (Bryce, Ali and Mather 2015). However, this could carry immense value to the

assessor in obtaining an overview of whether the expenditures are greater or lower and whether

the management of the organisation has the need to reduce budget and overall expenses of the

same. Any favourable or unfavourable change in the ratio could be utilised as a referential factor

to assess the soundness of financial condition of DIPL. For example, the solvency ratio

computed in the above table helps in depicting the favourable as well as unfavourable trends in

the overall financial position of the firm. In a similar fashion, the contrast of ratios over the years

would provide an insight of clearing both short-term and long-term obligations of the business.

which could be used for contrasting financial declarations coupled with the assessment of audit

plan (Bepari and Mollik 2015).

Explanation:

The outcomes of the planning decisions related to audit planning is influenced primarily

through the outcomes of analytical method to disseminate information from the financial reports.

The following ratios have been taken into consideration:

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

The above table signifies that the current ratio of DIPL has increased over the years. On

the other hand, the profit margin has been observed as fluctuating over the years. With the help

of this ratio, the net profit of an organisation could be compared with the overall revenues

generated (Bryce, Ali and Mather 2015). However, this could carry immense value to the

assessor in obtaining an overview of whether the expenditures are greater or lower and whether

the management of the organisation has the need to reduce budget and overall expenses of the

same. Any favourable or unfavourable change in the ratio could be utilised as a referential factor

to assess the soundness of financial condition of DIPL. For example, the solvency ratio

computed in the above table helps in depicting the favourable as well as unfavourable trends in

the overall financial position of the firm. In a similar fashion, the contrast of ratios over the years

would provide an insight of clearing both short-term and long-term obligations of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

Hence, the auditors could gain an insight of the relative position of DIPL over the years along

with evaluating the factors leading to undesirable position of the organisation (Cason, Friesen

and Gangadharan 2016).

Answer to Question 2:

Various significant factors are inherent in auditing constituting of incidence of material

misstatements in the financial declarations of a particular entity. However, it is inherent that

there are various kinds of both systematic and unsystematic risks depicting the way towards

financial misstatements in the financial announcements of the organisations. In addition, the

identified risks might be because of financial and non-financial factors, which could

subsequently avert a particular entity in reflecting a fair view of the financial announcements.

According to Devos and Zackrisson (2015), the detected risks might be associated with various

risks of omission coupled with risks of various unthinkable errors for a particular bookkeeper.

Thus, it could be adjudged as the inherent risk arising from the business operations of DIPL.

Besides, the employees of DIPL are inexperienced and lack in proficiency, which have

escalated the overall inherent risk of the organisation. In addition, such lack of experience might

result in committing mistakes; thus, increasing the inherent risk. This is because the employees

form a significant part of the organisation and it is not possible for the firm to ensure its business

success and growth in future without effective employee contributions. The other important

factors contributing towards inherent risk could be classified into various sections like

environmental and external facets, material misstatements in past periods and false exercises

(Gani, Wijeweera and Eddie 2017). The environmental facets directing the way towards inherent

risk constitutes of rapid alterations where issues would arise associated with inventory valuation,

Hence, the auditors could gain an insight of the relative position of DIPL over the years along

with evaluating the factors leading to undesirable position of the organisation (Cason, Friesen

and Gangadharan 2016).

Answer to Question 2:

Various significant factors are inherent in auditing constituting of incidence of material

misstatements in the financial declarations of a particular entity. However, it is inherent that

there are various kinds of both systematic and unsystematic risks depicting the way towards

financial misstatements in the financial announcements of the organisations. In addition, the

identified risks might be because of financial and non-financial factors, which could

subsequently avert a particular entity in reflecting a fair view of the financial announcements.

According to Devos and Zackrisson (2015), the detected risks might be associated with various

risks of omission coupled with risks of various unthinkable errors for a particular bookkeeper.

Thus, it could be adjudged as the inherent risk arising from the business operations of DIPL.

Besides, the employees of DIPL are inexperienced and lack in proficiency, which have

escalated the overall inherent risk of the organisation. In addition, such lack of experience might

result in committing mistakes; thus, increasing the inherent risk. This is because the employees

form a significant part of the organisation and it is not possible for the firm to ensure its business

success and growth in future without effective employee contributions. The other important

factors contributing towards inherent risk could be classified into various sections like

environmental and external facets, material misstatements in past periods and false exercises

(Gani, Wijeweera and Eddie 2017). The environmental facets directing the way towards inherent

risk constitutes of rapid alterations where issues would arise associated with inventory valuation,

5AUDIT, ASSURANCE AND COMPLIANCE

intense competition in the market and lack of capital. Moreover, there is possibility of material

misstatements, which would direct DIPL towards inherent risk in the upcoming years.

The analysis of the present case of DIPL depicts the fact that the issues and complexities

related to CEO succession comprise of inherent risk as well. In essence, the CEO succession

could be adjudged as different, as the candidates are individuals (Graham 2015). Hence, the

commencement of the process without compliance with the strategy, late initiation of the

process, ineffective association of CEO and attrition of the staffs might result in inherent risk.

The assessment of the provided case implies that the implementation process of the IT

system has lead to certain issues. DIPL has employee shortage for managing the execution

process and installation along with conducting the reconciliation and testing primarily before

new arrangement at the end of the period. In addition, the initial assessment disclosed that

several transactions carried out were not recorded in an appropriate manner. Hence, this results

in material misstatement due to inherent factors, which is an error of omission in a particular

financial announcement (Gray et al. 2016).

The staff members of DIPL are needed to follow an appropriate sequence for registering

accounts receivable and ledgers associated with accounts receivable. Along with this, the bank

reconciliation is needed to be recorded appropriately as well (Milonas et al. 2016). Furthermore,

the registration of revenue obtained from e-book and considering the reprint of textbooks in

future could result in various inherent risks because of complexity associated with the process.

Thus, the valuation of inventory pertaining to raw materials at average cost is not appropriate, as

the average cost is well below the existing cost of paper.

intense competition in the market and lack of capital. Moreover, there is possibility of material

misstatements, which would direct DIPL towards inherent risk in the upcoming years.

The analysis of the present case of DIPL depicts the fact that the issues and complexities

related to CEO succession comprise of inherent risk as well. In essence, the CEO succession

could be adjudged as different, as the candidates are individuals (Graham 2015). Hence, the

commencement of the process without compliance with the strategy, late initiation of the

process, ineffective association of CEO and attrition of the staffs might result in inherent risk.

The assessment of the provided case implies that the implementation process of the IT

system has lead to certain issues. DIPL has employee shortage for managing the execution

process and installation along with conducting the reconciliation and testing primarily before

new arrangement at the end of the period. In addition, the initial assessment disclosed that

several transactions carried out were not recorded in an appropriate manner. Hence, this results

in material misstatement due to inherent factors, which is an error of omission in a particular

financial announcement (Gray et al. 2016).

The staff members of DIPL are needed to follow an appropriate sequence for registering

accounts receivable and ledgers associated with accounts receivable. Along with this, the bank

reconciliation is needed to be recorded appropriately as well (Milonas et al. 2016). Furthermore,

the registration of revenue obtained from e-book and considering the reprint of textbooks in

future could result in various inherent risks because of complexity associated with the process.

Thus, the valuation of inventory pertaining to raw materials at average cost is not appropriate, as

the average cost is well below the existing cost of paper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

The detected inherent risks could be adjudged as the susceptibility of a specific assertion

in relation to the material misstatements and they are depicted briefly as follows:

Increasing burden on employees and management:

Due to the rising burden of work on the staffs of DIPL, it has resulted in inaccurate

bookkeeping. As a result, various attributes have happened that include the propensity in

encountering cash flows, poor liquidity and operating results (Mumford et al. 2014).

Error risk or wrong representation:

Reliability and intricacy are inherent due to risk associated with errors and

misrepresentation in a simultaneous fashion.

Integrity of the overall management:

As per the case study, the management of DIPL has lack of integrity and it is expected to

be ready for any loss of reputation in the business community.

Unusual pressure on management:

Often, it occurs that there is existence of incentives for the management. As a result, it

leads to misstatement in the financial announcements (Nalewaik and Mills 2016).

Nature of the business entity:

DIPL contributes to growth to major economic and competitive circumstances. In

addition, these facets might have influence on the inherent risk of the business entity for the

assessment of audit planning structure in an appropriate fashion.

The detected inherent risks could be adjudged as the susceptibility of a specific assertion

in relation to the material misstatements and they are depicted briefly as follows:

Increasing burden on employees and management:

Due to the rising burden of work on the staffs of DIPL, it has resulted in inaccurate

bookkeeping. As a result, various attributes have happened that include the propensity in

encountering cash flows, poor liquidity and operating results (Mumford et al. 2014).

Error risk or wrong representation:

Reliability and intricacy are inherent due to risk associated with errors and

misrepresentation in a simultaneous fashion.

Integrity of the overall management:

As per the case study, the management of DIPL has lack of integrity and it is expected to

be ready for any loss of reputation in the business community.

Unusual pressure on management:

Often, it occurs that there is existence of incentives for the management. As a result, it

leads to misstatement in the financial announcements (Nalewaik and Mills 2016).

Nature of the business entity:

DIPL contributes to growth to major economic and competitive circumstances. In

addition, these facets might have influence on the inherent risk of the business entity for the

assessment of audit planning structure in an appropriate fashion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

Answer to Question 3:

Answer to Part A:

In the words of Saad (2014), the fraud risk could result in severe losses of assets due to

fraudulent activities. The lack of motivation of the workforce due to additional work pressure of

the staffs could induce them to engage in various kinds of fraudulent activities. Along with this,

the expectations from the various groups of investors in reporting particular financial results or

specifically on the part of the management in achieving particular targets of performance could

result in increased fraud risk. Furthermore, strong pressure is exerted on the management of

DIPL to announce particular financial results in a bid for averting generating the guarantees.

The major types of risks that are identified in the context of the business operations of

DIPL are briefly classified as follows:

Types of risk Identification

Engagement of workforce in fraudulent

activities

The primary fraud risk that might take place

due to the business operations of DIPL is the

engagement of the workforce in fraudulent

activities because of greater level of employee

dissatisfaction. The provided case study

pertaining to the operations of DOPL states

that the board has exerted heavy pressure on

the organisation in acquiring a novel system of

accounting. Such additional pressure on the

staffs in conducting the installation process of

Answer to Question 3:

Answer to Part A:

In the words of Saad (2014), the fraud risk could result in severe losses of assets due to

fraudulent activities. The lack of motivation of the workforce due to additional work pressure of

the staffs could induce them to engage in various kinds of fraudulent activities. Along with this,

the expectations from the various groups of investors in reporting particular financial results or

specifically on the part of the management in achieving particular targets of performance could

result in increased fraud risk. Furthermore, strong pressure is exerted on the management of

DIPL to announce particular financial results in a bid for averting generating the guarantees.

The major types of risks that are identified in the context of the business operations of

DIPL are briefly classified as follows:

Types of risk Identification

Engagement of workforce in fraudulent

activities

The primary fraud risk that might take place

due to the business operations of DIPL is the

engagement of the workforce in fraudulent

activities because of greater level of employee

dissatisfaction. The provided case study

pertaining to the operations of DOPL states

that the board has exerted heavy pressure on

the organisation in acquiring a novel system of

accounting. Such additional pressure on the

staffs in conducting the installation process of

8AUDIT, ASSURANCE AND COMPLIANCE

the new information technology system for

accounting might result in fraud.

This signifies that the staffs might involve in

fraudulent behaviours and activities for

managing the process of reconciliation in an

ineffective fashion and accordingly, material

misstatements. The provided case depicts that

the ineffective management of the execution

process related to implementation of

information technology for the system of

accounting results in incorrect apportionment

of various transactions at the end of the period.

As a result, this might lead to severe loss

because of material misstatement and

fraudulent risk (DeFond and Zhang 2014).

Method pertaining to financial reporting Another fraud risk that might confront the

business operations of DIPL takes into account

the risk related to financial reporting fraud.

During certain situations, it has been observed

that there is additional expectation from the

external financiers or from the management.

Such expectation is to achieve the particular

targets of performance or other goals in order

the new information technology system for

accounting might result in fraud.

This signifies that the staffs might involve in

fraudulent behaviours and activities for

managing the process of reconciliation in an

ineffective fashion and accordingly, material

misstatements. The provided case depicts that

the ineffective management of the execution

process related to implementation of

information technology for the system of

accounting results in incorrect apportionment

of various transactions at the end of the period.

As a result, this might lead to severe loss

because of material misstatement and

fraudulent risk (DeFond and Zhang 2014).

Method pertaining to financial reporting Another fraud risk that might confront the

business operations of DIPL takes into account

the risk related to financial reporting fraud.

During certain situations, it has been observed

that there is additional expectation from the

external financiers or from the management.

Such expectation is to achieve the particular

targets of performance or other goals in order

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

to qualify to obtain debt. As a result, there is

enhanced risk of incorrect financial

declarations. According to the balance sheet

statement of DIPL provided in the case study,

the net revenue of the organisation has

increased from the year 2103 to the year 2015.

Along with this, both the gross income and net

income of the organisation have increased in

tandem as well.

Furthermore, the current assets and overall

assets of the organisation DIPL have escalated

as well. However, the provided case signifies

that during the year 2015, DIPL has made a

loan acquisition of $7.5 million, the major part

of which has been obtained from BDO

Finance. Apart from this, the provided case

depicts that the loan obtained has a particular

agreement of loan requiring DIPL in

maintaining a current ratio of nearly 1.5 along

with debt-equity of below 1. This depicts that

such need might compel the organisation in

maintaining the financial ratio for acquiring the

credit terms. Hence, this might result in

to qualify to obtain debt. As a result, there is

enhanced risk of incorrect financial

declarations. According to the balance sheet

statement of DIPL provided in the case study,

the net revenue of the organisation has

increased from the year 2103 to the year 2015.

Along with this, both the gross income and net

income of the organisation have increased in

tandem as well.

Furthermore, the current assets and overall

assets of the organisation DIPL have escalated

as well. However, the provided case signifies

that during the year 2015, DIPL has made a

loan acquisition of $7.5 million, the major part

of which has been obtained from BDO

Finance. Apart from this, the provided case

depicts that the loan obtained has a particular

agreement of loan requiring DIPL in

maintaining a current ratio of nearly 1.5 along

with debt-equity of below 1. This depicts that

such need might compel the organisation in

maintaining the financial ratio for acquiring the

credit terms. Hence, this might result in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

fraudulent activities, which could to lead

inaccurate depiction of the financial position.

As a result, the failure of the organisation in

maintaining the standard yardsticks could

make the organisation ineligible in acquiring

funds from BDO Finance.

Answer to Part B:

Based on the provided case study, it could be remarked that the method of valuation

associated with valuation of inventory of various raw materials at specifically average cost has

not been appropriate. This is because of the fact that the average cost has been considerably

lower in contrast to the existing paper cost. The risk of detecting fraudulent actions associated

with implementing the new system pertaining to information technology could be conducted by

monitoring various activities at various phases. The risk associated with financial reporting could

be identified by conducting dissection of the financial statements on the part of the assessors

along with reviewing the mechanisms of control over time (Stephenson et al. 2015).

Benchmarking is considered as an analytical process and it could be used further for the

assessment of audit plan. The variance of the real financial declaration from the yardstick

enables in recognising the deviation and it assists in evaluating the reason of the identified

variance.

fraudulent activities, which could to lead

inaccurate depiction of the financial position.

As a result, the failure of the organisation in

maintaining the standard yardsticks could

make the organisation ineligible in acquiring

funds from BDO Finance.

Answer to Part B:

Based on the provided case study, it could be remarked that the method of valuation

associated with valuation of inventory of various raw materials at specifically average cost has

not been appropriate. This is because of the fact that the average cost has been considerably

lower in contrast to the existing paper cost. The risk of detecting fraudulent actions associated

with implementing the new system pertaining to information technology could be conducted by

monitoring various activities at various phases. The risk associated with financial reporting could

be identified by conducting dissection of the financial statements on the part of the assessors

along with reviewing the mechanisms of control over time (Stephenson et al. 2015).

Benchmarking is considered as an analytical process and it could be used further for the

assessment of audit plan. The variance of the real financial declaration from the yardstick

enables in recognising the deviation and it assists in evaluating the reason of the identified

variance.

11AUDIT, ASSURANCE AND COMPLIANCE

References:

Barr-Pulliam, D., Nkansa, P., Walker, K., appreciate helpful comments from Helen, W., Brown-

Liburd, A.G. and Stefaniak, C., 2017. From Compliance to Strategy: Using the Three Lines of

Defense Model to Evaluate and Motivate Internal Audit Contributions to Accounting Research.

Bayer, R. and Cowell, F., 2016. Tax compliance by firms and audit policy. Research in

Economics, 70(1), pp.38-52.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Cason, T.N., Friesen, L. and Gangadharan, L., 2016. Regulatory performance of audit

tournaments and compliance observability. European Economic Review, 85, pp.288-306.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), p.108.

References:

Barr-Pulliam, D., Nkansa, P., Walker, K., appreciate helpful comments from Helen, W., Brown-

Liburd, A.G. and Stefaniak, C., 2017. From Compliance to Strategy: Using the Three Lines of

Defense Model to Evaluate and Motivate Internal Audit Contributions to Accounting Research.

Bayer, R. and Cowell, F., 2016. Tax compliance by firms and audit policy. Research in

Economics, 70(1), pp.38-52.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Cason, T.N., Friesen, L. and Gangadharan, L., 2016. Regulatory performance of audit

tournaments and compliance observability. European Economic Review, 85, pp.288-306.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), p.108.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.