Audit and Assurance Report: Four Chimps Audit, Ethics, and Procedures

VerifiedAdded on 2022/12/29

|12

|3270

|69

Report

AI Summary

This report provides a comprehensive overview of audit and assurance principles, focusing on the responsibilities of external auditors like RBK, audit ethics, and substantive testing procedures. The report examines the duties of RBK as an external auditor, considering factors such as compliance with food hygiene regulations and the materiality concept. It explores the benefits of establishing an internal audit department and outlines audit tests to verify account payables. The report also analyzes audit committees, internal controls over cash in the not-for-profit sector, and substantive testing for trade debtors and redundancy provisions. Ethical threats and mitigation strategies are also discussed. Furthermore, the report delves into auditor considerations regarding the going concern assumption, providing a detailed analysis of various aspects of auditing and financial reporting.

AUDIT AND ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

SECTION A.....................................................................................................................................1

1. Duties of RBK as an external auditor of four chimps.......................................................1

9...................................................................................................................................................2

10.................................................................................................................................................2

SECTION B.....................................................................................................................................3

11. Audit Committees, Internal Controls over Cash and Audit in the Not-for-Profit Sector......3

b)..................................................................................................................................................3

c)..................................................................................................................................................4

12 Substantive Testing for Trade Debtors and Redundancy Provisions.....................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

c)..................................................................................................................................................6

13 Audit Ethics............................................................................................................................6

14 Auditor considerations regarding the Going Concern assumption.........................................8

a)..................................................................................................................................................8

b)..................................................................................................................................................9

c)..................................................................................................................................................9

REFERENCES..............................................................................................................................10

TABLE OF CONTENTS................................................................................................................2

SECTION A.....................................................................................................................................1

1. Duties of RBK as an external auditor of four chimps.......................................................1

9...................................................................................................................................................2

10.................................................................................................................................................2

SECTION B.....................................................................................................................................3

11. Audit Committees, Internal Controls over Cash and Audit in the Not-for-Profit Sector......3

b)..................................................................................................................................................3

c)..................................................................................................................................................4

12 Substantive Testing for Trade Debtors and Redundancy Provisions.....................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

c)..................................................................................................................................................6

13 Audit Ethics............................................................................................................................6

14 Auditor considerations regarding the Going Concern assumption.........................................8

a)..................................................................................................................................................8

b)..................................................................................................................................................9

c)..................................................................................................................................................9

REFERENCES..............................................................................................................................10

SECTION A

1. Duties of RBK as an external auditor of four chimps

RBK as an External auditor has several responsibility that are essential to perform .

foremost duty of auditor is to understand company operations and evaluate control and manage

audit report. Consult with management of four chips to assess risk and supervise control of cost

and make rectifications of error statements. It also has duty to visit branches and can check

records of cost reports.

2. to lauana januzzi for prohibiting RBK from providing both audit and non audit services

An auditor has to follow several norms of committee of auditing for being eligible to perform

auditing of financial statement of company. An external auditor can not perform as internal

auditor of organization to co cope with regulation. As it is differentiate between two types of

auditors and their roles and responsibilities are also divided so that evasion of tax can not be

done. this is the main reason for prohibiting RBK from providing both services.

3. Reasons for which four chimps compliance with food hygiene regulations

Quality control partner of RBK do not want company or any member of management to get in

touch with audit reports because they can make changes that are suitable or advantageous for

their firm. As director of comp1.any was not sure about its internal reports so wanted to

compliance with food hygiene so it can make changes and improve status of company’s financial

statement and avoid unwanted penality that it may have to pay in case of any mistakes (Masdor

and Shamsuddin, 2018)

.

4. Materiality concept and its compliance with food hygiene regulations

It is a concept that can be ignored by organization if it has very less impact on financial

statements of company. Compliance with food hygiene regulation can give adverse impact on

financial statements of company. As audit committee will review the transactions between firm

and its related party to cross check the statements (Bananuka, and et.al., 2019). It can be

consider appropriate only if it is interest of company and parties.

5 Benefits for setting up an internal audit department for Four chimps

There are different advantages according to type of firm. Biggest advantage is that it can improve

efficiency of operations of firms. Financial reliability and integrity is also increases with the

help of internal audit team. Company can serve evidence its reports as internal auditor can

assure reports are prepared with laws regulators norms and conditions Akisik and Gal, (2019). It

1

1. Duties of RBK as an external auditor of four chimps

RBK as an External auditor has several responsibility that are essential to perform .

foremost duty of auditor is to understand company operations and evaluate control and manage

audit report. Consult with management of four chips to assess risk and supervise control of cost

and make rectifications of error statements. It also has duty to visit branches and can check

records of cost reports.

2. to lauana januzzi for prohibiting RBK from providing both audit and non audit services

An auditor has to follow several norms of committee of auditing for being eligible to perform

auditing of financial statement of company. An external auditor can not perform as internal

auditor of organization to co cope with regulation. As it is differentiate between two types of

auditors and their roles and responsibilities are also divided so that evasion of tax can not be

done. this is the main reason for prohibiting RBK from providing both services.

3. Reasons for which four chimps compliance with food hygiene regulations

Quality control partner of RBK do not want company or any member of management to get in

touch with audit reports because they can make changes that are suitable or advantageous for

their firm. As director of comp1.any was not sure about its internal reports so wanted to

compliance with food hygiene so it can make changes and improve status of company’s financial

statement and avoid unwanted penality that it may have to pay in case of any mistakes (Masdor

and Shamsuddin, 2018)

.

4. Materiality concept and its compliance with food hygiene regulations

It is a concept that can be ignored by organization if it has very less impact on financial

statements of company. Compliance with food hygiene regulation can give adverse impact on

financial statements of company. As audit committee will review the transactions between firm

and its related party to cross check the statements (Bananuka, and et.al., 2019). It can be

consider appropriate only if it is interest of company and parties.

5 Benefits for setting up an internal audit department for Four chimps

There are different advantages according to type of firm. Biggest advantage is that it can improve

efficiency of operations of firms. Financial reliability and integrity is also increases with the

help of internal audit team. Company can serve evidence its reports as internal auditor can

assure reports are prepared with laws regulators norms and conditions Akisik and Gal, (2019). It

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also establishes supervisory procedures.

6. Audit test to verify completeness of account payable

Three ways to check accuracy of account payable, first way can be reconciling account payable

ledger with abbreviation of account with control. Another way is contacting to company’s major

vendors to check the transactions of company statement that they match with it or not. and third

method is an detail analysis of statements so omission and rectification of transaction can be

checked. With te help of these tests verification can be done. Best way out of all three can be

detailed analysis of statements.

7. Reasons for difference in three accounts of suppliers

From the above statement it can be analyzed that wrong transaction of £88929as credit note is

the reason that difference in all three suppliers is occurring. As the ledger balance has been

miscalculated due to wrong amount of credit note entry. Such errors are big that can lead to big

changes in statement. As correct entry of invoice are very essential for proper accounting.

8. Evidence for difference in Arcelor mittal difference

Evidence can be given in many ways like receipt can be use as evidence which ahs been given to

Arcelor mittal , statement of bank can also be used as evidence. Difference in the transaction of

ledger is proof for the difference.

9

Review of the previous year ending balance with opening balance of purchases.

Discuss with management about the reasons behind such difference

Review the aged balance of suppliers from last year and current year and why they are

not cleared or marked as paid

It would have to review the purchase invoices and agree it with the balance in ledger

accounts of account payables

It has to review if any disputes are existing over the payment.

10

The overstatements of the purchase and operating expense overstated will require the audit

tests for payables to be performed to agree the expenses are authorised by the proper authority.

The balance of previous year should be agreed with opening balance. It would require to perform

2

6. Audit test to verify completeness of account payable

Three ways to check accuracy of account payable, first way can be reconciling account payable

ledger with abbreviation of account with control. Another way is contacting to company’s major

vendors to check the transactions of company statement that they match with it or not. and third

method is an detail analysis of statements so omission and rectification of transaction can be

checked. With te help of these tests verification can be done. Best way out of all three can be

detailed analysis of statements.

7. Reasons for difference in three accounts of suppliers

From the above statement it can be analyzed that wrong transaction of £88929as credit note is

the reason that difference in all three suppliers is occurring. As the ledger balance has been

miscalculated due to wrong amount of credit note entry. Such errors are big that can lead to big

changes in statement. As correct entry of invoice are very essential for proper accounting.

8. Evidence for difference in Arcelor mittal difference

Evidence can be given in many ways like receipt can be use as evidence which ahs been given to

Arcelor mittal , statement of bank can also be used as evidence. Difference in the transaction of

ledger is proof for the difference.

9

Review of the previous year ending balance with opening balance of purchases.

Discuss with management about the reasons behind such difference

Review the aged balance of suppliers from last year and current year and why they are

not cleared or marked as paid

It would have to review the purchase invoices and agree it with the balance in ledger

accounts of account payables

It has to review if any disputes are existing over the payment.

10

The overstatements of the purchase and operating expense overstated will require the audit

tests for payables to be performed to agree the expenses are authorised by the proper authority.

The balance of previous year should be agreed with opening balance. It would require to perform

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

additional substantive procedures to identify the actual purchases and expenses including

external party confirmations.

SECTION B

11. Audit Committees, Internal Controls over Cash and Audit in the Not-for-Profit Sector

a) Objectives of audit committee and benefits

There are various objectives that an audit committee set for fair practices of an organsiation .

main objective of an auditor is to assist the board in fulfilling its responsibilities and roles so that

company can perform in fair manner. Another objective is to check the quality and accuracy of

accounting , auditing and company’s reporting practice and how its follow the regulatory and

legal requirement.

The main purpose of conducting auditing is to oversee financial reports and accounting of

company and auditing of firm. The other objectives are to seek information regarding unfair

practices from employees of company and managing reconciliation of those practices to make

reports right. Other objective is to enhancement of internal and external creditability of financial

reports. And risk protection and financial management, compliance with regulation of law and

best practices to maintain corporation with guidelines of audit Nurunnabi, (2017)

Monitoring is main objective of auditing committee and keeping internal and external

audior efficient so proper auditing can take place. Review of independence of statutory audit

firm in provision of any extra or supplement service to audited entity. Operating risk

management is another objective to identify, prioritize and reaction to risk are mainly monitored

by audit committee.

b)

The funds could be restricted by charity where donor wants money to go for specific program or

donor has defined the specific use of money for event or time. It provides assurance to donor that

the funds are used for defined purpose. The auditor has to review composition of all the

restricted funds. The use of such funds should be analysed and ensured that they are released

3

external party confirmations.

SECTION B

11. Audit Committees, Internal Controls over Cash and Audit in the Not-for-Profit Sector

a) Objectives of audit committee and benefits

There are various objectives that an audit committee set for fair practices of an organsiation .

main objective of an auditor is to assist the board in fulfilling its responsibilities and roles so that

company can perform in fair manner. Another objective is to check the quality and accuracy of

accounting , auditing and company’s reporting practice and how its follow the regulatory and

legal requirement.

The main purpose of conducting auditing is to oversee financial reports and accounting of

company and auditing of firm. The other objectives are to seek information regarding unfair

practices from employees of company and managing reconciliation of those practices to make

reports right. Other objective is to enhancement of internal and external creditability of financial

reports. And risk protection and financial management, compliance with regulation of law and

best practices to maintain corporation with guidelines of audit Nurunnabi, (2017)

Monitoring is main objective of auditing committee and keeping internal and external

audior efficient so proper auditing can take place. Review of independence of statutory audit

firm in provision of any extra or supplement service to audited entity. Operating risk

management is another objective to identify, prioritize and reaction to risk are mainly monitored

by audit committee.

b)

The funds could be restricted by charity where donor wants money to go for specific program or

donor has defined the specific use of money for event or time. It provides assurance to donor that

the funds are used for defined purpose. The auditor has to review composition of all the

restricted funds. The use of such funds should be analysed and ensured that they are released

3

from the specific purpose stated by Imtiaz. The restricted fund should be released as per the

requirements and also verify that released funds are also used for that specific purpose (Bucior

and Kujawski, 2017). Also the auditor has to inspect the type of restriction imposed over funds

from the receipts.

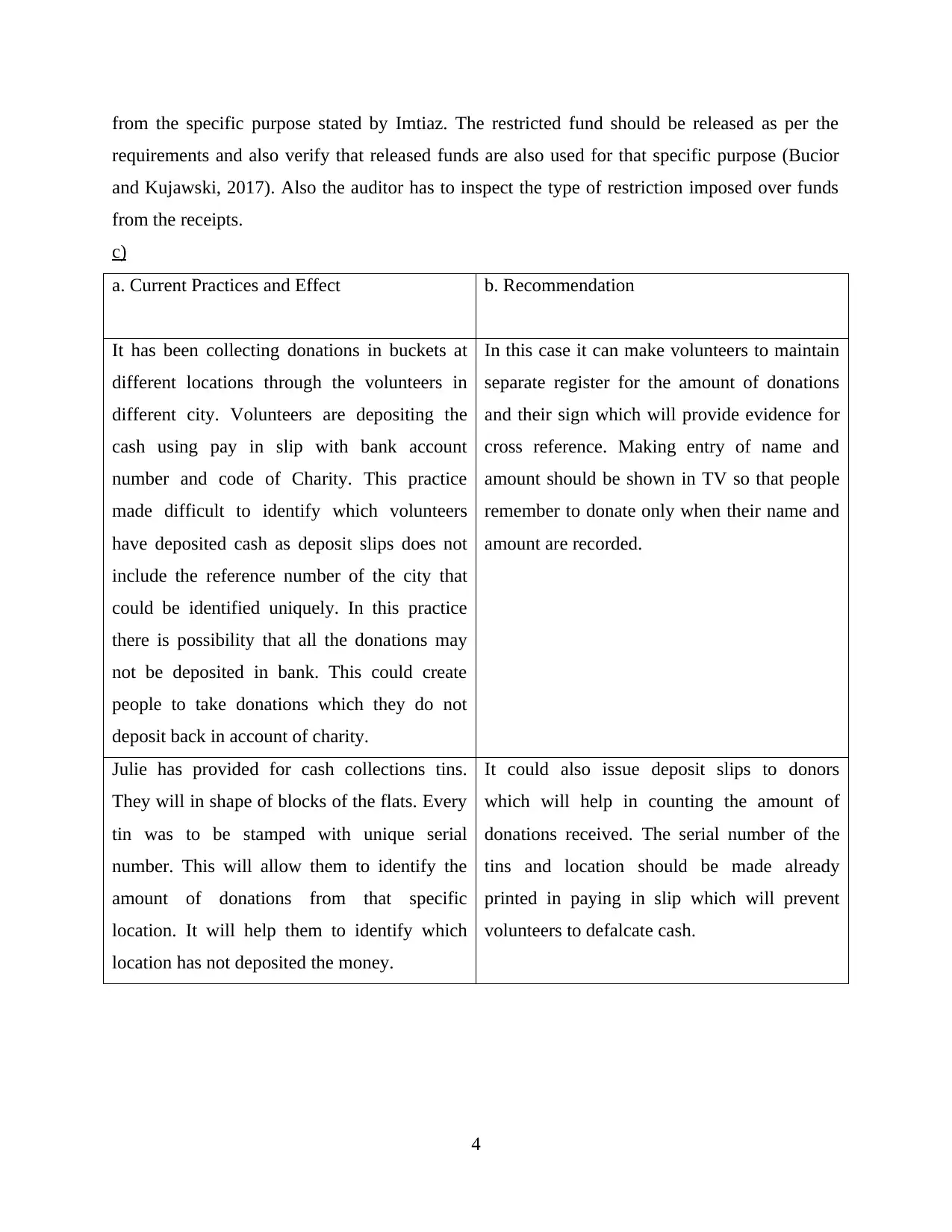

c)

a. Current Practices and Effect b. Recommendation

It has been collecting donations in buckets at

different locations through the volunteers in

different city. Volunteers are depositing the

cash using pay in slip with bank account

number and code of Charity. This practice

made difficult to identify which volunteers

have deposited cash as deposit slips does not

include the reference number of the city that

could be identified uniquely. In this practice

there is possibility that all the donations may

not be deposited in bank. This could create

people to take donations which they do not

deposit back in account of charity.

In this case it can make volunteers to maintain

separate register for the amount of donations

and their sign which will provide evidence for

cross reference. Making entry of name and

amount should be shown in TV so that people

remember to donate only when their name and

amount are recorded.

Julie has provided for cash collections tins.

They will in shape of blocks of the flats. Every

tin was to be stamped with unique serial

number. This will allow them to identify the

amount of donations from that specific

location. It will help them to identify which

location has not deposited the money.

It could also issue deposit slips to donors

which will help in counting the amount of

donations received. The serial number of the

tins and location should be made already

printed in paying in slip which will prevent

volunteers to defalcate cash.

4

requirements and also verify that released funds are also used for that specific purpose (Bucior

and Kujawski, 2017). Also the auditor has to inspect the type of restriction imposed over funds

from the receipts.

c)

a. Current Practices and Effect b. Recommendation

It has been collecting donations in buckets at

different locations through the volunteers in

different city. Volunteers are depositing the

cash using pay in slip with bank account

number and code of Charity. This practice

made difficult to identify which volunteers

have deposited cash as deposit slips does not

include the reference number of the city that

could be identified uniquely. In this practice

there is possibility that all the donations may

not be deposited in bank. This could create

people to take donations which they do not

deposit back in account of charity.

In this case it can make volunteers to maintain

separate register for the amount of donations

and their sign which will provide evidence for

cross reference. Making entry of name and

amount should be shown in TV so that people

remember to donate only when their name and

amount are recorded.

Julie has provided for cash collections tins.

They will in shape of blocks of the flats. Every

tin was to be stamped with unique serial

number. This will allow them to identify the

amount of donations from that specific

location. It will help them to identify which

location has not deposited the money.

It could also issue deposit slips to donors

which will help in counting the amount of

donations received. The serial number of the

tins and location should be made already

printed in paying in slip which will prevent

volunteers to defalcate cash.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12 Substantive Testing for Trade Debtors and Redundancy Provisions

a)

Obtain consent from finance director of the Ritzy ltd for undertaking circularisation in

advance

Obtain list of the trade receivables at year end, cast list and then agree it with sales ledger

control account

Select sample from receivable list to ensure that number of old, nil, credit and big balance

are chosen

Circularisation letter needs to be prepared on letter head of Ritzy ltd requesting

confirmation of year end balance of receivables and replies to sent directly to auditors

using pre-paid envelopes (Larrinaga and et.al., 2020).

Where no reply is received, needs to follow with other letter or call and also alternative

procedures to be performed where essential

Where replies are given, it should be agreed with receivable records and discrepancies

should be investigated.

b)

Receivables substantive procedures

Valuation, Accuracy and allocation

Review after the date receipts of cash and follow through previous year ending balance of

receivables

Inspect aged receivables to identify which have been due from long whether they needs

allowance or should be written down

For slow moving balances review the customers correspondence to identify if any

invoices are under dispute.

Completeness

Select sample of the goods despatched notes of before year end, to agree with sales

invoice and its inclusion in sales ledger and year ending receivable ledger.

Agree total of the individual sales ledger to aged receivables lists and with trial balance.

Obtaining previous year receivable list and compare significant balances with the current

year receivables list for amount due and inclusions

5

a)

Obtain consent from finance director of the Ritzy ltd for undertaking circularisation in

advance

Obtain list of the trade receivables at year end, cast list and then agree it with sales ledger

control account

Select sample from receivable list to ensure that number of old, nil, credit and big balance

are chosen

Circularisation letter needs to be prepared on letter head of Ritzy ltd requesting

confirmation of year end balance of receivables and replies to sent directly to auditors

using pre-paid envelopes (Larrinaga and et.al., 2020).

Where no reply is received, needs to follow with other letter or call and also alternative

procedures to be performed where essential

Where replies are given, it should be agreed with receivable records and discrepancies

should be investigated.

b)

Receivables substantive procedures

Valuation, Accuracy and allocation

Review after the date receipts of cash and follow through previous year ending balance of

receivables

Inspect aged receivables to identify which have been due from long whether they needs

allowance or should be written down

For slow moving balances review the customers correspondence to identify if any

invoices are under dispute.

Completeness

Select sample of the goods despatched notes of before year end, to agree with sales

invoice and its inclusion in sales ledger and year ending receivable ledger.

Agree total of the individual sales ledger to aged receivables lists and with trial balance.

Obtaining previous year receivable list and compare significant balances with the current

year receivables list for amount due and inclusions

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Review sales ledger for credit balance and identify if they need to be classified as

payables

Rights and Obligations

Review loan agreements and bank confirmations for evidence that the receivables are

assigned security for the amounts owed by Ritzy

Review the board minutes for evidences that legal title of receivables is sold to third party

like factor (Lobwo, Davis and Anthony, 2020).

For sample of receivables, agree balance recorded over sales ledger to original name of

customers on sales order or contract.

c)

Substantive procedures

Discussion with directors about whether they have announced intention for closing

production and making employees redundant for confirming present obligation at year

end

If this is announced before year end, the review of support documents for verifying that

decisions are announced formally

Review minutes of board to identify probability of payments for redundancy

Obtain break down of redundancy calculations from employee and cast them to ensure its

completeness and agree them with trial balance.

Recalculating redundancy provisions for confirming completeness and agreeing

components of calculations for supporting documentation like employee contracts.

Obtain written representation from the management for confirming completeness of

provisions

Review disclosures of redundancy provisions for ensuring compliance with the IAS 37

13 Audit Ethics

Ethical threats Mitigations

Finance Director requires the audit report of

financial statements of CBL before the normal

EP should discuss timing with Financial

director, and ask to commence audit earlier for

6

payables

Rights and Obligations

Review loan agreements and bank confirmations for evidence that the receivables are

assigned security for the amounts owed by Ritzy

Review the board minutes for evidences that legal title of receivables is sold to third party

like factor (Lobwo, Davis and Anthony, 2020).

For sample of receivables, agree balance recorded over sales ledger to original name of

customers on sales order or contract.

c)

Substantive procedures

Discussion with directors about whether they have announced intention for closing

production and making employees redundant for confirming present obligation at year

end

If this is announced before year end, the review of support documents for verifying that

decisions are announced formally

Review minutes of board to identify probability of payments for redundancy

Obtain break down of redundancy calculations from employee and cast them to ensure its

completeness and agree them with trial balance.

Recalculating redundancy provisions for confirming completeness and agreeing

components of calculations for supporting documentation like employee contracts.

Obtain written representation from the management for confirming completeness of

provisions

Review disclosures of redundancy provisions for ensuring compliance with the IAS 37

13 Audit Ethics

Ethical threats Mitigations

Finance Director requires the audit report of

financial statements of CBL before the normal

EP should discuss timing with Financial

director, and ask to commence audit earlier for

6

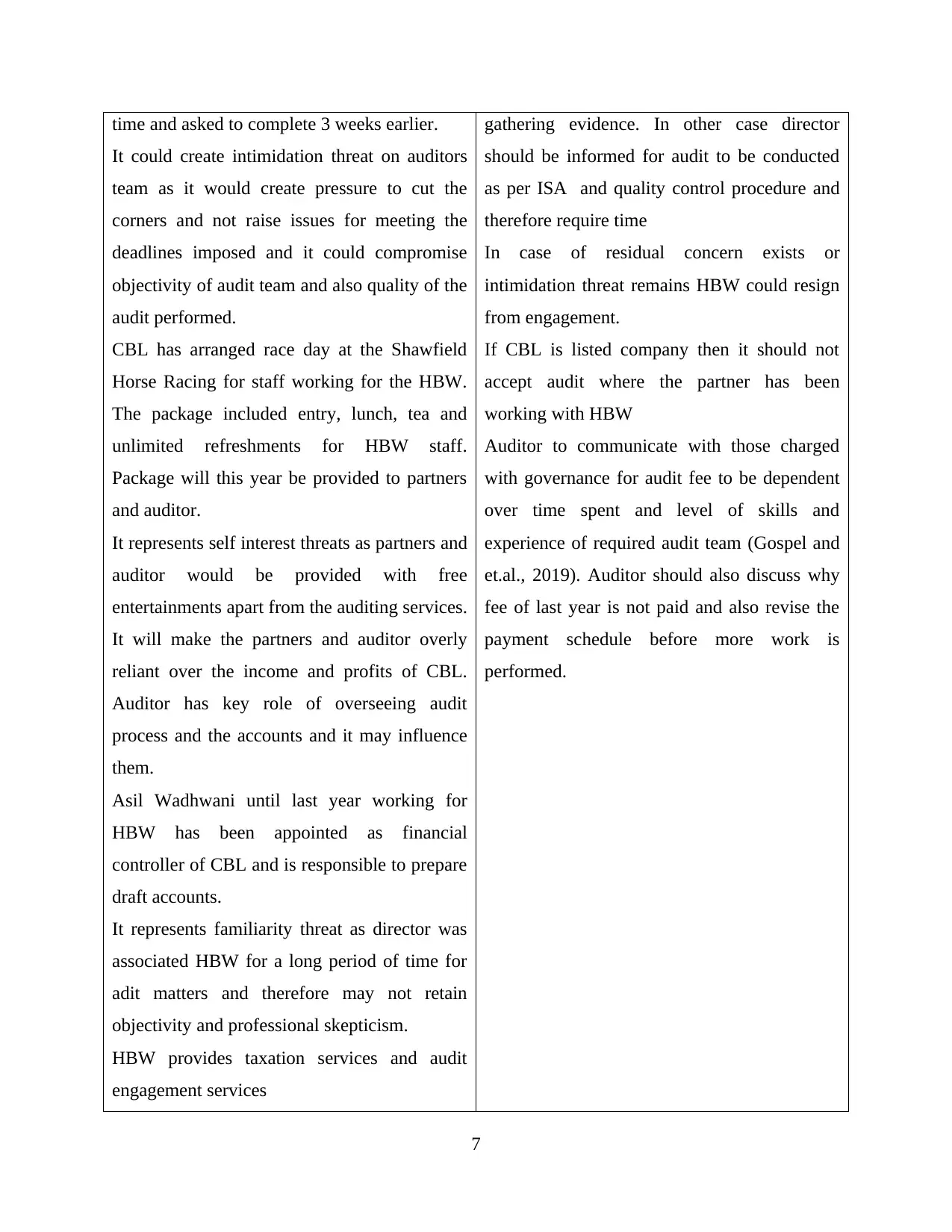

time and asked to complete 3 weeks earlier.

It could create intimidation threat on auditors

team as it would create pressure to cut the

corners and not raise issues for meeting the

deadlines imposed and it could compromise

objectivity of audit team and also quality of the

audit performed.

CBL has arranged race day at the Shawfield

Horse Racing for staff working for the HBW.

The package included entry, lunch, tea and

unlimited refreshments for HBW staff.

Package will this year be provided to partners

and auditor.

It represents self interest threats as partners and

auditor would be provided with free

entertainments apart from the auditing services.

It will make the partners and auditor overly

reliant over the income and profits of CBL.

Auditor has key role of overseeing audit

process and the accounts and it may influence

them.

Asil Wadhwani until last year working for

HBW has been appointed as financial

controller of CBL and is responsible to prepare

draft accounts.

It represents familiarity threat as director was

associated HBW for a long period of time for

adit matters and therefore may not retain

objectivity and professional skepticism.

HBW provides taxation services and audit

engagement services

gathering evidence. In other case director

should be informed for audit to be conducted

as per ISA and quality control procedure and

therefore require time

In case of residual concern exists or

intimidation threat remains HBW could resign

from engagement.

If CBL is listed company then it should not

accept audit where the partner has been

working with HBW

Auditor to communicate with those charged

with governance for audit fee to be dependent

over time spent and level of skills and

experience of required audit team (Gospel and

et.al., 2019). Auditor should also discuss why

fee of last year is not paid and also revise the

payment schedule before more work is

performed.

7

It could create intimidation threat on auditors

team as it would create pressure to cut the

corners and not raise issues for meeting the

deadlines imposed and it could compromise

objectivity of audit team and also quality of the

audit performed.

CBL has arranged race day at the Shawfield

Horse Racing for staff working for the HBW.

The package included entry, lunch, tea and

unlimited refreshments for HBW staff.

Package will this year be provided to partners

and auditor.

It represents self interest threats as partners and

auditor would be provided with free

entertainments apart from the auditing services.

It will make the partners and auditor overly

reliant over the income and profits of CBL.

Auditor has key role of overseeing audit

process and the accounts and it may influence

them.

Asil Wadhwani until last year working for

HBW has been appointed as financial

controller of CBL and is responsible to prepare

draft accounts.

It represents familiarity threat as director was

associated HBW for a long period of time for

adit matters and therefore may not retain

objectivity and professional skepticism.

HBW provides taxation services and audit

engagement services

gathering evidence. In other case director

should be informed for audit to be conducted

as per ISA and quality control procedure and

therefore require time

In case of residual concern exists or

intimidation threat remains HBW could resign

from engagement.

If CBL is listed company then it should not

accept audit where the partner has been

working with HBW

Auditor to communicate with those charged

with governance for audit fee to be dependent

over time spent and level of skills and

experience of required audit team (Gospel and

et.al., 2019). Auditor should also discuss why

fee of last year is not paid and also revise the

payment schedule before more work is

performed.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

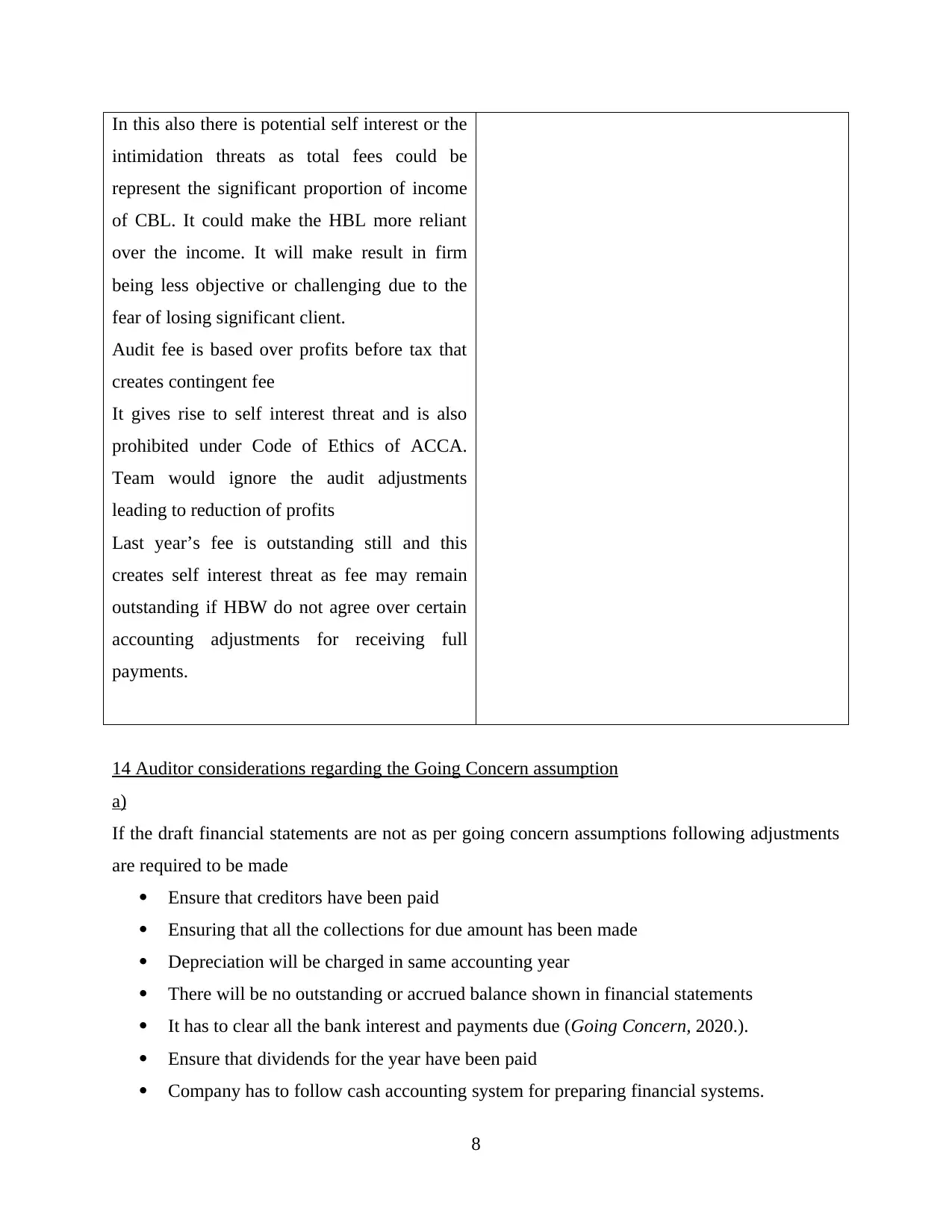

In this also there is potential self interest or the

intimidation threats as total fees could be

represent the significant proportion of income

of CBL. It could make the HBL more reliant

over the income. It will make result in firm

being less objective or challenging due to the

fear of losing significant client.

Audit fee is based over profits before tax that

creates contingent fee

It gives rise to self interest threat and is also

prohibited under Code of Ethics of ACCA.

Team would ignore the audit adjustments

leading to reduction of profits

Last year’s fee is outstanding still and this

creates self interest threat as fee may remain

outstanding if HBW do not agree over certain

accounting adjustments for receiving full

payments.

14 Auditor considerations regarding the Going Concern assumption

a)

If the draft financial statements are not as per going concern assumptions following adjustments

are required to be made

Ensure that creditors have been paid

Ensuring that all the collections for due amount has been made

Depreciation will be charged in same accounting year

There will be no outstanding or accrued balance shown in financial statements

It has to clear all the bank interest and payments due (Going Concern, 2020.).

Ensure that dividends for the year have been paid

Company has to follow cash accounting system for preparing financial systems.

8

intimidation threats as total fees could be

represent the significant proportion of income

of CBL. It could make the HBL more reliant

over the income. It will make result in firm

being less objective or challenging due to the

fear of losing significant client.

Audit fee is based over profits before tax that

creates contingent fee

It gives rise to self interest threat and is also

prohibited under Code of Ethics of ACCA.

Team would ignore the audit adjustments

leading to reduction of profits

Last year’s fee is outstanding still and this

creates self interest threat as fee may remain

outstanding if HBW do not agree over certain

accounting adjustments for receiving full

payments.

14 Auditor considerations regarding the Going Concern assumption

a)

If the draft financial statements are not as per going concern assumptions following adjustments

are required to be made

Ensure that creditors have been paid

Ensuring that all the collections for due amount has been made

Depreciation will be charged in same accounting year

There will be no outstanding or accrued balance shown in financial statements

It has to clear all the bank interest and payments due (Going Concern, 2020.).

Ensure that dividends for the year have been paid

Company has to follow cash accounting system for preparing financial systems.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b)

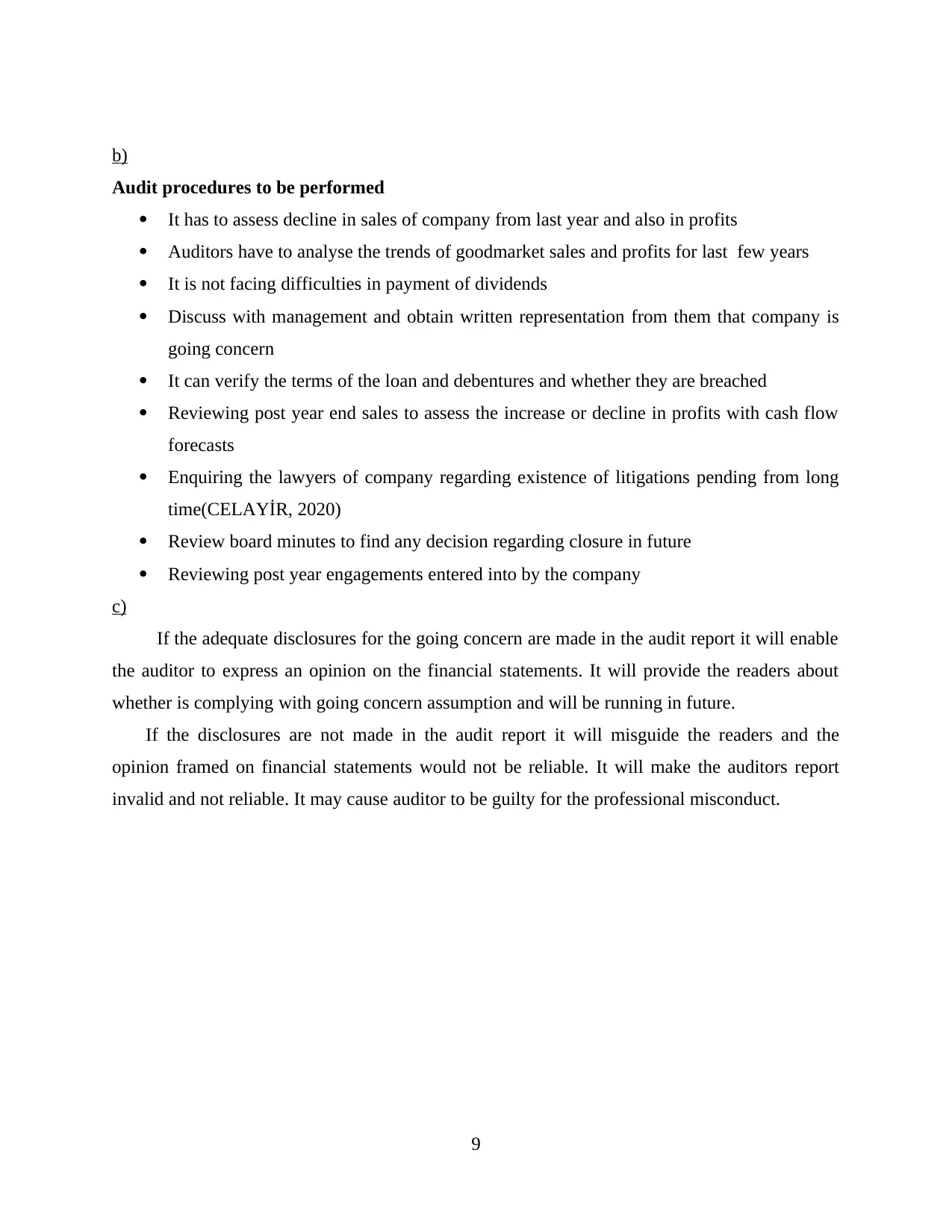

Audit procedures to be performed

It has to assess decline in sales of company from last year and also in profits

Auditors have to analyse the trends of goodmarket sales and profits for last few years

It is not facing difficulties in payment of dividends

Discuss with management and obtain written representation from them that company is

going concern

It can verify the terms of the loan and debentures and whether they are breached

Reviewing post year end sales to assess the increase or decline in profits with cash flow

forecasts

Enquiring the lawyers of company regarding existence of litigations pending from long

time(CELAYİR, 2020)

Review board minutes to find any decision regarding closure in future

Reviewing post year engagements entered into by the company

c)

If the adequate disclosures for the going concern are made in the audit report it will enable

the auditor to express an opinion on the financial statements. It will provide the readers about

whether is complying with going concern assumption and will be running in future.

If the disclosures are not made in the audit report it will misguide the readers and the

opinion framed on financial statements would not be reliable. It will make the auditors report

invalid and not reliable. It may cause auditor to be guilty for the professional misconduct.

9

Audit procedures to be performed

It has to assess decline in sales of company from last year and also in profits

Auditors have to analyse the trends of goodmarket sales and profits for last few years

It is not facing difficulties in payment of dividends

Discuss with management and obtain written representation from them that company is

going concern

It can verify the terms of the loan and debentures and whether they are breached

Reviewing post year end sales to assess the increase or decline in profits with cash flow

forecasts

Enquiring the lawyers of company regarding existence of litigations pending from long

time(CELAYİR, 2020)

Review board minutes to find any decision regarding closure in future

Reviewing post year engagements entered into by the company

c)

If the adequate disclosures for the going concern are made in the audit report it will enable

the auditor to express an opinion on the financial statements. It will provide the readers about

whether is complying with going concern assumption and will be running in future.

If the disclosures are not made in the audit report it will misguide the readers and the

opinion framed on financial statements would not be reliable. It will make the auditors report

invalid and not reliable. It may cause auditor to be guilty for the professional misconduct.

9

REFERENCES

Books and Journals

Bucior, G. and Kujawski, J., 2017. Podyplomowe studia „Rachunkowość ACCA-poziom

profesjonalny” na Wydziale Zarządzania Uniwersytetu Gdańskiego. Folia Pomeranae

Universitatis Technologiae Stetinensis. Oeconomica. 87.

Larrinaga, C., and et.al., 2020. Institutionalization of the contents of sustainability assurance

services: A comparison between Italy and United States. Journal of Business

Ethics. 163(1). pp.67-83.

Lobwo, S.K., Davis, J. and Anthony, V.D., 2020. AUDIT AND ASSURANCE: SOME

EMERGING ISSUES. Studies in Indian Place Names. 40(29). pp.317-326.

Gospel, J., and et.al., 2019. Sufficiency and Appropriateness of Audit Evidence for Giving an

Opinion on the True and Fair View of Financial Statements.

CELAYİR, D., KEY AUDIT ISSUES AS AN ELEMENT OF THE INDEPENDENT AUDIT

REPORTS AND A STUDY WITHIN THE SCOPE OF THE INTERNATIONAL

STANDARD ON AUDITING (ISA) 701. In ACADEMIC STUDIES (p. 2).

Bananuka, J., and et.al., 2019. Audit committee effectiveness, isomorphic forces, managerial

attitude and adoption of international financial reporting standards. Journal of accounting

in Emerging Economies.

Masdor, N. and Shamsuddin, A., 2018. The Implementation of ISA 701-Key Audit Matters: A

Review. Global Business & Management Research. 10(3).

Akisik, O. and Gal, G., 2019. Integrated reports, external assurance and financial

performance. Sustainability Accounting, Management and Policy Journal.

Nurunnabi, M., 2017. Auditors’ perceptions of the implementation of International Financial

Reporting Standards (IFRS) in a developing country. Journal of Accounting in Emerging

Economies.

Online

Going Concern. 2020. [Online]. Available through : <

https://www.accaglobal.com/ca/en/student/exam-support-resources/fundamentals-exams-

study-resources/f8/technical-articles/going-concern.html>.

10

Books and Journals

Bucior, G. and Kujawski, J., 2017. Podyplomowe studia „Rachunkowość ACCA-poziom

profesjonalny” na Wydziale Zarządzania Uniwersytetu Gdańskiego. Folia Pomeranae

Universitatis Technologiae Stetinensis. Oeconomica. 87.

Larrinaga, C., and et.al., 2020. Institutionalization of the contents of sustainability assurance

services: A comparison between Italy and United States. Journal of Business

Ethics. 163(1). pp.67-83.

Lobwo, S.K., Davis, J. and Anthony, V.D., 2020. AUDIT AND ASSURANCE: SOME

EMERGING ISSUES. Studies in Indian Place Names. 40(29). pp.317-326.

Gospel, J., and et.al., 2019. Sufficiency and Appropriateness of Audit Evidence for Giving an

Opinion on the True and Fair View of Financial Statements.

CELAYİR, D., KEY AUDIT ISSUES AS AN ELEMENT OF THE INDEPENDENT AUDIT

REPORTS AND A STUDY WITHIN THE SCOPE OF THE INTERNATIONAL

STANDARD ON AUDITING (ISA) 701. In ACADEMIC STUDIES (p. 2).

Bananuka, J., and et.al., 2019. Audit committee effectiveness, isomorphic forces, managerial

attitude and adoption of international financial reporting standards. Journal of accounting

in Emerging Economies.

Masdor, N. and Shamsuddin, A., 2018. The Implementation of ISA 701-Key Audit Matters: A

Review. Global Business & Management Research. 10(3).

Akisik, O. and Gal, G., 2019. Integrated reports, external assurance and financial

performance. Sustainability Accounting, Management and Policy Journal.

Nurunnabi, M., 2017. Auditors’ perceptions of the implementation of International Financial

Reporting Standards (IFRS) in a developing country. Journal of Accounting in Emerging

Economies.

Online

Going Concern. 2020. [Online]. Available through : <

https://www.accaglobal.com/ca/en/student/exam-support-resources/fundamentals-exams-

study-resources/f8/technical-articles/going-concern.html>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.