Comprehensive Analysis of Audit and Assurance: Procedures & Risk

VerifiedAdded on 2023/06/07

|8

|1260

|191

Report

AI Summary

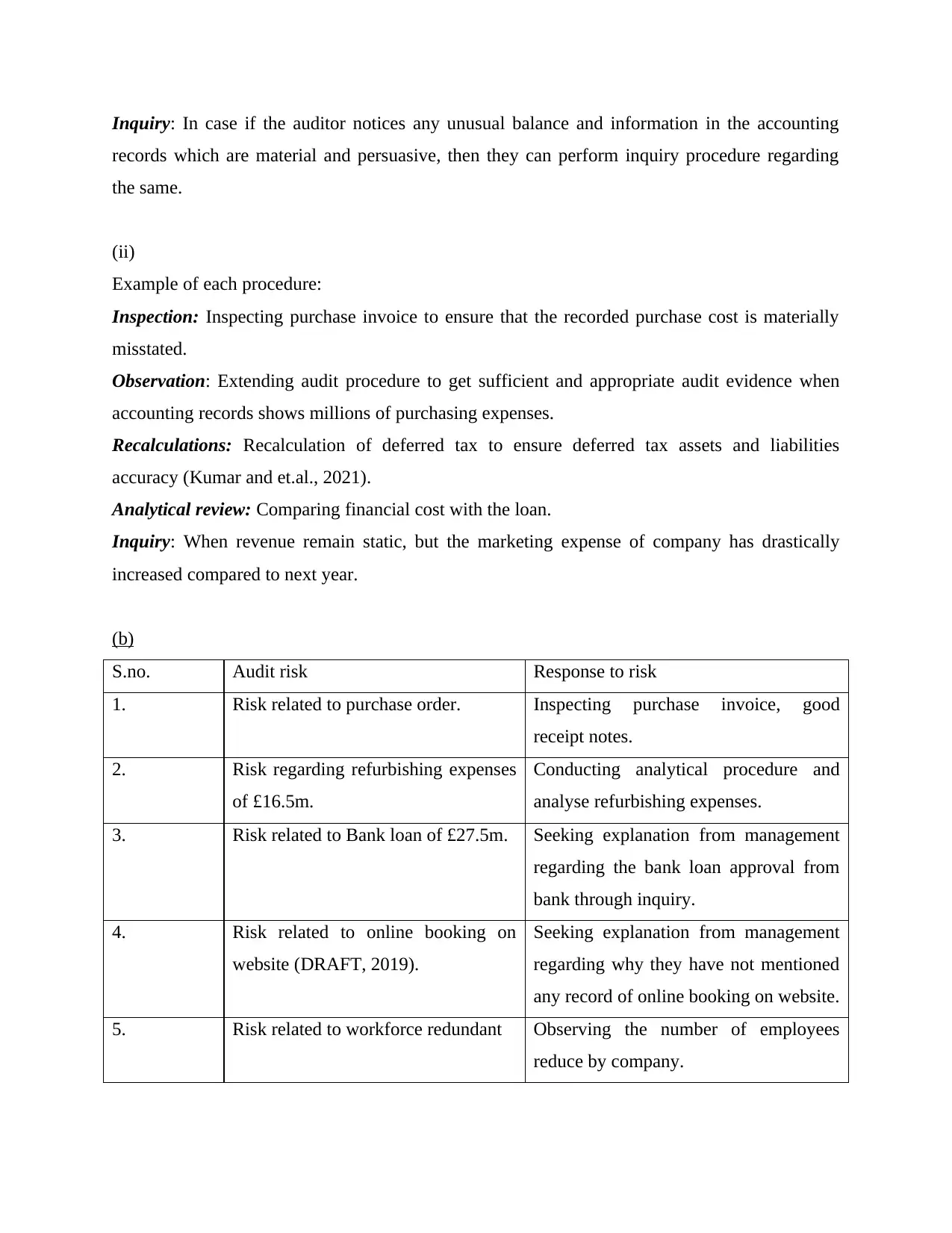

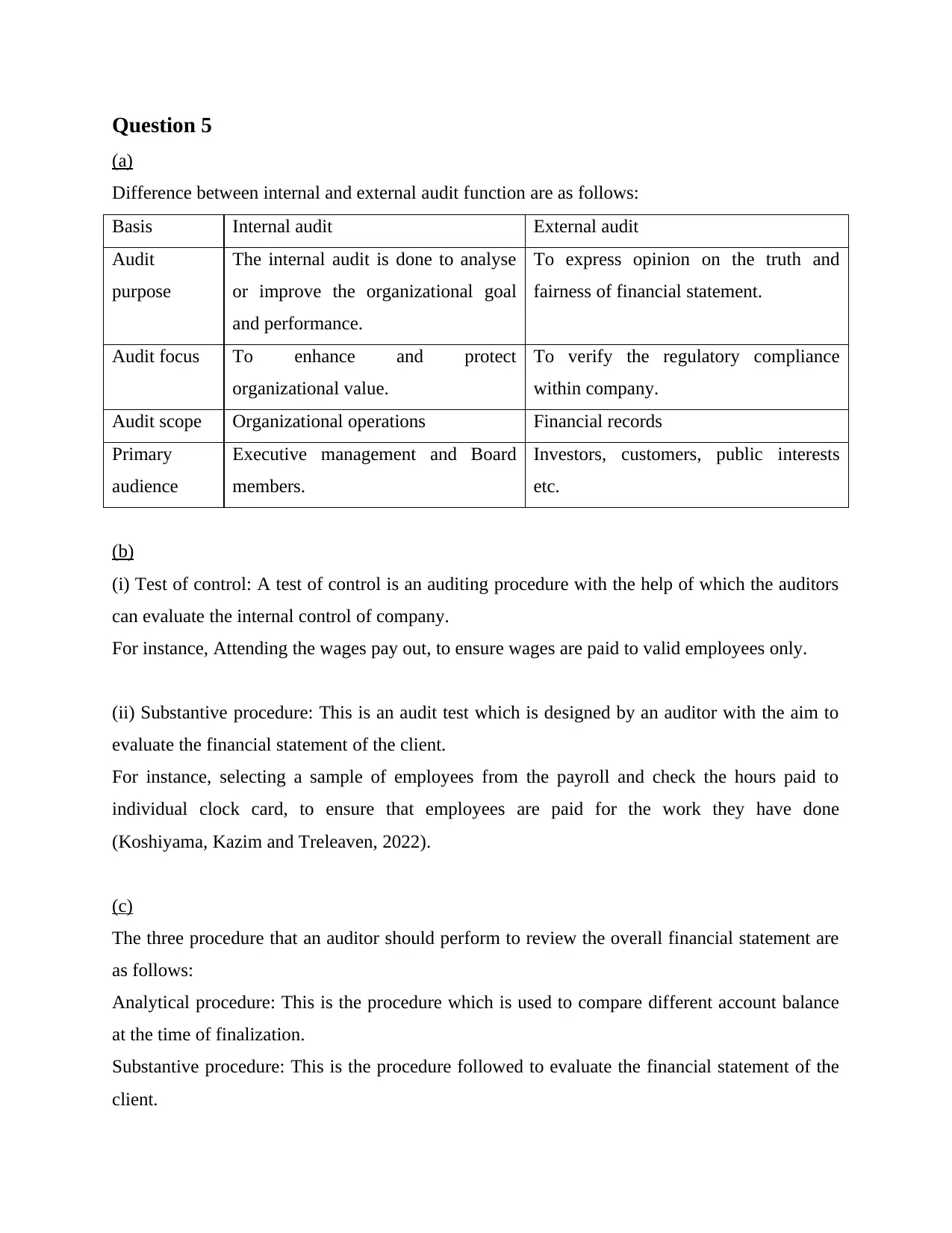

This report provides a detailed overview of audit and assurance procedures, differentiating between internal and external audit functions, and outlining various methods for obtaining audit evidence. It discusses analytical procedures, inquiry, inspection, observation, and recalculation, highlighting their suitability and limitations in the context of financial statement analysis. Furthermore, the report addresses risk assessment, detailing responses to specific risks such as those related to purchase orders, refurbishing expenses, bank loans, and online bookings. It also contrasts test of controls with substantive procedures, and identifies three key procedures for reviewing overall financial statements, including analytical procedures, substantive procedures, and inquiry. The document serves as a comprehensive resource for understanding the core principles and practices of auditing and assurance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.