Audit, Assurance and Services Report: Materiality and Going Concern

VerifiedAdded on 2023/01/06

|9

|2384

|20

Report

AI Summary

This report presents an analysis of an audit, assurance, and services assignment. It begins with an introduction to audit and assurance services, including reasonable assurance and professional skepticism. The report then delves into an ethical problem involving unpaid audit fees, proposing solutions. It explains the concept of materiality, both qualitative and quantitative, and discusses how information impacts preliminary materiality assessments. The report further examines the auditor's responsibilities regarding going concern assumptions, identifying events that may cast doubt on a company's ability to continue as a going concern. Finally, it provides an overview of audit procedures related to client accounting treatments. The report provides valuable insights into the complexities of auditing, ethical considerations, and the importance of assessing financial statements accurately. The report includes references to academic journals and books.

Audit, Assurance and

Services

Services

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

QUESTION 1..............................................................................................................................................3

(a) Concept of reasonable assurance, and how reasonable assurance is determined. Explain why an

auditor cannot offer absolute assurance...................................................................................................3

(b) Concept of 'professional scepticism' and how it is not the same as assuming that managers are

always trying to deceive auditors.............................................................................................................4

QUESTION 2..............................................................................................................................................4

Explain the ethical problem in this case. Why is it a problem?................................................................4

What can be done about it?......................................................................................................................5

QUESTION 3..............................................................................................................................................5

Explain why determination of materiality is a matter of auditor judgment. Refer to both qualitative and

quantitative materiality assessments........................................................................................................5

Explain whether (and, if so, how) the information provided impacts on the auditor's assessment of

preliminary materiality............................................................................................................................5

QUESTION 4..............................................................................................................................................6

(a) What are the auditor's responsibilities for 'going concern assumptions?............................................6

Identify any significant events or conditions that individually or collectively may cast significant doubt

on SS's ability to continue as a going concern.........................................................................................7

QUESTION 5..............................................................................................................................................7

REFERENCES............................................................................................................................................9

INTRODUCTION.......................................................................................................................................3

QUESTION 1..............................................................................................................................................3

(a) Concept of reasonable assurance, and how reasonable assurance is determined. Explain why an

auditor cannot offer absolute assurance...................................................................................................3

(b) Concept of 'professional scepticism' and how it is not the same as assuming that managers are

always trying to deceive auditors.............................................................................................................4

QUESTION 2..............................................................................................................................................4

Explain the ethical problem in this case. Why is it a problem?................................................................4

What can be done about it?......................................................................................................................5

QUESTION 3..............................................................................................................................................5

Explain why determination of materiality is a matter of auditor judgment. Refer to both qualitative and

quantitative materiality assessments........................................................................................................5

Explain whether (and, if so, how) the information provided impacts on the auditor's assessment of

preliminary materiality............................................................................................................................5

QUESTION 4..............................................................................................................................................6

(a) What are the auditor's responsibilities for 'going concern assumptions?............................................6

Identify any significant events or conditions that individually or collectively may cast significant doubt

on SS's ability to continue as a going concern.........................................................................................7

QUESTION 5..............................................................................................................................................7

REFERENCES............................................................................................................................................9

INTRODUCTION

An audit is an assurance service of a kind. Assurance programmers can be compliance-based or

legislative. They focus on ensuring that protocols, rules and regulations are followed by a

corporation or agency, and have both internally and externally confidence in government reports.

Assurance services are audit operations which provide income reports or enforcement initiatives

with an impartial, objective review (Axén, 2018). The aims of these audits are to ensure that

financial reports are correct and activities are conducted in compliance with relevant laws and

regulations by management, the Board, and regulatory.

QUESTION 1

(a) Concept of reasonable assurance, and how reasonable assurance is determined. Explain why

an auditor cannot offer absolute assurance

Reasonable assurance requires recognizing that there is a remote possibility of not

avoiding or identifying material errors on a periodic manner. While not complete certainty, fair

certainty is a good threshold of certainty, nonetheless. A difference exists between the standards

of Nga and the performance levels of the auditor. Fair verification is given by an audit, not total

assurance. The audit improves the validity and integrity of the details used in the financial

statement, but does not ensure that the financial statement will not collapse or be free from errors

or corruption. In addition, this is attributable to the meaning of financial reporting. Judgments on

financial accounting and the selection and implementation of various forms of reporting are

needed. In the context of organisation benefit, there is generally not one 'correct' response

(Bradbury, 2017). The auditor does not confirm that the corporation's purchasing stage is

'correct,' but only offer evidence of the suitability of the formulation and application of the

income statement and the significant accounting. The essence of the assessment process is yet

another explanation the guarantee is not complete. Auditors are unable to evaluate every

expenditure and payment history, so they use filtering (which may imply that relevant objects for

evaluation are not chosen). It is difficult to obtain accurate information regarding certain

financial statements, customers can obstruct justice, and auditors have a short time period upon

which to execute the audit.

An audit is an assurance service of a kind. Assurance programmers can be compliance-based or

legislative. They focus on ensuring that protocols, rules and regulations are followed by a

corporation or agency, and have both internally and externally confidence in government reports.

Assurance services are audit operations which provide income reports or enforcement initiatives

with an impartial, objective review (Axén, 2018). The aims of these audits are to ensure that

financial reports are correct and activities are conducted in compliance with relevant laws and

regulations by management, the Board, and regulatory.

QUESTION 1

(a) Concept of reasonable assurance, and how reasonable assurance is determined. Explain why

an auditor cannot offer absolute assurance

Reasonable assurance requires recognizing that there is a remote possibility of not

avoiding or identifying material errors on a periodic manner. While not complete certainty, fair

certainty is a good threshold of certainty, nonetheless. A difference exists between the standards

of Nga and the performance levels of the auditor. Fair verification is given by an audit, not total

assurance. The audit improves the validity and integrity of the details used in the financial

statement, but does not ensure that the financial statement will not collapse or be free from errors

or corruption. In addition, this is attributable to the meaning of financial reporting. Judgments on

financial accounting and the selection and implementation of various forms of reporting are

needed. In the context of organisation benefit, there is generally not one 'correct' response

(Bradbury, 2017). The auditor does not confirm that the corporation's purchasing stage is

'correct,' but only offer evidence of the suitability of the formulation and application of the

income statement and the significant accounting. The essence of the assessment process is yet

another explanation the guarantee is not complete. Auditors are unable to evaluate every

expenditure and payment history, so they use filtering (which may imply that relevant objects for

evaluation are not chosen). It is difficult to obtain accurate information regarding certain

financial statements, customers can obstruct justice, and auditors have a short time period upon

which to execute the audit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) Concept of 'professional scepticism' and how it is not the same as assuming that managers are

always trying to deceive auditors

Professional scepticism is a behavior involving an expanded hazard, being alert to

circumstances which might suggest potential misrepresentation due to mistake or cheating, and a

detailed evaluation of audit proof. These examples of professional scepticism illustrate the issues

of the supervisor and help internal auditors react to these problems. An auditor needs

professional scepticism. It is an attitude which needs the accountant to stay separate of the

customer and his employees. The auditor has an expanded hazard and reviews all facts provided

by his company extensively. This will not indicate that they consider the customer a fraud, but

also that they ought to do something other than accept the opinion of the customer on something.

Usually, documentation supporting the assertions of the client ( e.g. copies of agreements, policy

documents, etc.) can be checked. Data obtained from neutral third sources is normally considered

to be more accurate than that obtained from the consumer. Supervisors would not necessarily

seek to cheat auditors, but auditors should assume accountability for obtaining evidence to

demonstrate the claims of managers. The auditor ought to be sensitive to the possibility that

certain executives often try to mislead inspectors (Cohen and Rozario, 2019).

QUESTION 2

Explain the ethical problem in this case. Why is it a problem?

A given action, situation or behavior causes a dispute with the moral values of a

community, ethical concerns arise. These disputes will affect both people and institutions, as all

of their actions may be challenged from an ethical perspective. As per the case it is analyzed that

ethical issue client does not pay fees on time and delay for the auditing. It is considering as

ethical problem because with amount an auditor cannot publish auditor report that impact on

client business in direct manner. Most law says it before counseling starts, payments have to be

negotiated so that consumers know what is required of them. And, this would include the fact

that if the payment is not charged, you have the option to end (Denisov, Khachaturyan and

Umnova, 2018) .

always trying to deceive auditors

Professional scepticism is a behavior involving an expanded hazard, being alert to

circumstances which might suggest potential misrepresentation due to mistake or cheating, and a

detailed evaluation of audit proof. These examples of professional scepticism illustrate the issues

of the supervisor and help internal auditors react to these problems. An auditor needs

professional scepticism. It is an attitude which needs the accountant to stay separate of the

customer and his employees. The auditor has an expanded hazard and reviews all facts provided

by his company extensively. This will not indicate that they consider the customer a fraud, but

also that they ought to do something other than accept the opinion of the customer on something.

Usually, documentation supporting the assertions of the client ( e.g. copies of agreements, policy

documents, etc.) can be checked. Data obtained from neutral third sources is normally considered

to be more accurate than that obtained from the consumer. Supervisors would not necessarily

seek to cheat auditors, but auditors should assume accountability for obtaining evidence to

demonstrate the claims of managers. The auditor ought to be sensitive to the possibility that

certain executives often try to mislead inspectors (Cohen and Rozario, 2019).

QUESTION 2

Explain the ethical problem in this case. Why is it a problem?

A given action, situation or behavior causes a dispute with the moral values of a

community, ethical concerns arise. These disputes will affect both people and institutions, as all

of their actions may be challenged from an ethical perspective. As per the case it is analyzed that

ethical issue client does not pay fees on time and delay for the auditing. It is considering as

ethical problem because with amount an auditor cannot publish auditor report that impact on

client business in direct manner. Most law says it before counseling starts, payments have to be

negotiated so that consumers know what is required of them. And, this would include the fact

that if the payment is not charged, you have the option to end (Denisov, Khachaturyan and

Umnova, 2018) .

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

What can be done about it?

To sort out this problem require to give warning t client that if he does not pay on time so

do not publish auditor report that impact on his business in inverse manner. As a result clients

pressurizes for the payment and communicate with that person who have power and control to

handle this situation appropriately.

QUESTION 3

Explain why determination of materiality is a matter of auditor judgment. Refer to both

qualitative and quantitative materiality assessments

Auditors rely on rules of thumb and highly qualified judgment to maintain an amount of

materiality. The number and sort of mistake is also considered by them. The level of materiality

is usually specified as a particular amount of a budget item of a particular financial report. Data

is material if this might impact decisions taken by users in terms of monetary knowledge about a

single financial statement by ignoring or misrepresenting it. In other terms, in the context of a

particular organization's financial report, materiality is an object-specific feature of importance

based on the existence or significance, or both, of the objects to whom the policy applies.

Subsequently, the Board can not define a standard quantitative standard for materiality or, in a

specific case, predetermine what could be content. The MMM chartered accountants paid their

suppliers late, well in excess of the supplier’s normal credit terms. As a resulted it impact on the

suppliers and requesting from the cash on delivery from the business. When analyzing the

business, it is assessing that company have cash flow problem from last two years. Thus, it

impact on the qualitative and quantitative assessment of the materiality.

Explain whether (and, if so, how) the information provided impacts on the auditor's assessment

of preliminary materiality

Materiality depends on the degree and quality of the omission or defect measured in the

events surrounding it. The deciding factor may be the size or value of the object, or a mixture of

the both. Evaluating a degree of materiality for the financial statements presented overall

promote interaction the decisions of the accountant in the detection and potential consequences

of material errors and in the preparation of the type, pacing, and degree of more audit process.

Qualitative variables that impact the materiality decision of an investigator include: quantities

To sort out this problem require to give warning t client that if he does not pay on time so

do not publish auditor report that impact on his business in inverse manner. As a result clients

pressurizes for the payment and communicate with that person who have power and control to

handle this situation appropriately.

QUESTION 3

Explain why determination of materiality is a matter of auditor judgment. Refer to both

qualitative and quantitative materiality assessments

Auditors rely on rules of thumb and highly qualified judgment to maintain an amount of

materiality. The number and sort of mistake is also considered by them. The level of materiality

is usually specified as a particular amount of a budget item of a particular financial report. Data

is material if this might impact decisions taken by users in terms of monetary knowledge about a

single financial statement by ignoring or misrepresenting it. In other terms, in the context of a

particular organization's financial report, materiality is an object-specific feature of importance

based on the existence or significance, or both, of the objects to whom the policy applies.

Subsequently, the Board can not define a standard quantitative standard for materiality or, in a

specific case, predetermine what could be content. The MMM chartered accountants paid their

suppliers late, well in excess of the supplier’s normal credit terms. As a resulted it impact on the

suppliers and requesting from the cash on delivery from the business. When analyzing the

business, it is assessing that company have cash flow problem from last two years. Thus, it

impact on the qualitative and quantitative assessment of the materiality.

Explain whether (and, if so, how) the information provided impacts on the auditor's assessment

of preliminary materiality

Materiality depends on the degree and quality of the omission or defect measured in the

events surrounding it. The deciding factor may be the size or value of the object, or a mixture of

the both. Evaluating a degree of materiality for the financial statements presented overall

promote interaction the decisions of the accountant in the detection and potential consequences

of material errors and in the preparation of the type, pacing, and degree of more audit process.

Qualitative variables that impact the materiality decision of an investigator include: quantities

associated with fraud. Scam quantities are generally deemed more severe that accidental

mistakes of equivalent amounts of dollars because fraud represents the integrity and competence

of the managers or other workers involved. As per the information Auditor analysis the financial

statement after that takes right decision in regard of suppliers. These information direct impact

on the auditor assessment (Engage, 2019).

QUESTION 4

(a) What are the auditor's responsibilities for 'going concern assumptions?

It is the duty of the auditor to obtain ample adequate audit procedures in the audited

financial statements on the suitability of the manager's use of the going concern basis and to

determine whether there is a substantial doubt regarding the capacity of the organisation to

survive as a continuing concern. In the preparation of financial statements, the principle of

current concern is an implicit presumption, since it is presumed that the company neither has the

purpose nor there is a need to significantly buy up or curtail the size of its activities. "The duty of

the auditor to think of going from over given comments is:" The auditor is not capable of

predicting potential events or situations. The probability that the organisation may eventually

disappear as an ongoing concern despite the receipt by the accountant of a report which does not

give rise to significant doubt, within those one year after the end of the financial period, does not,

in itself, imply the audit ineffective results. Appropriately, the lack of relation in an auditor's

report to serious doubt should not be seen as offering certainty as to the capacity of an

organisation to proceed as an ongoing concern.

According to ISA 570, the auditor 's duty is to achieve acceptable audit proof as to the

acceptability of the manager's the use of reporting basis of current issue in the audited financial

statements and to determine if there is significant doubt as to the capacity of the company to

function as a growing concern. Applicants will be asked to identify the audit process that the

auditor may carry out in the AA exam to determine whether or not a business is a current

concern (Lenz, Sarens and Hoos, 2017).

mistakes of equivalent amounts of dollars because fraud represents the integrity and competence

of the managers or other workers involved. As per the information Auditor analysis the financial

statement after that takes right decision in regard of suppliers. These information direct impact

on the auditor assessment (Engage, 2019).

QUESTION 4

(a) What are the auditor's responsibilities for 'going concern assumptions?

It is the duty of the auditor to obtain ample adequate audit procedures in the audited

financial statements on the suitability of the manager's use of the going concern basis and to

determine whether there is a substantial doubt regarding the capacity of the organisation to

survive as a continuing concern. In the preparation of financial statements, the principle of

current concern is an implicit presumption, since it is presumed that the company neither has the

purpose nor there is a need to significantly buy up or curtail the size of its activities. "The duty of

the auditor to think of going from over given comments is:" The auditor is not capable of

predicting potential events or situations. The probability that the organisation may eventually

disappear as an ongoing concern despite the receipt by the accountant of a report which does not

give rise to significant doubt, within those one year after the end of the financial period, does not,

in itself, imply the audit ineffective results. Appropriately, the lack of relation in an auditor's

report to serious doubt should not be seen as offering certainty as to the capacity of an

organisation to proceed as an ongoing concern.

According to ISA 570, the auditor 's duty is to achieve acceptable audit proof as to the

acceptability of the manager's the use of reporting basis of current issue in the audited financial

statements and to determine if there is significant doubt as to the capacity of the company to

function as a growing concern. Applicants will be asked to identify the audit process that the

auditor may carry out in the AA exam to determine whether or not a business is a current

concern (Lenz, Sarens and Hoos, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identify any significant events or conditions that individually or collectively may cast significant

doubt on SS's ability to continue as a going concern

Many constraints, along with some other issues as set out in note x, imply that there is an

earn abnormal that may cast considerable doubt on the ability of the group to survive as a

continuing concern. With respect to this issue, our view is not altered.

A major decline in revenue from sales. ...

Significant Debt or Interest Payable Overdue sum. ...

Most of the checking account. ...

Absence of research & design Fund. ...

Lost in Key Management. ...

Problems with Cash Flow. ...

Lost from the Great Project (Nedyalkova, 2017).

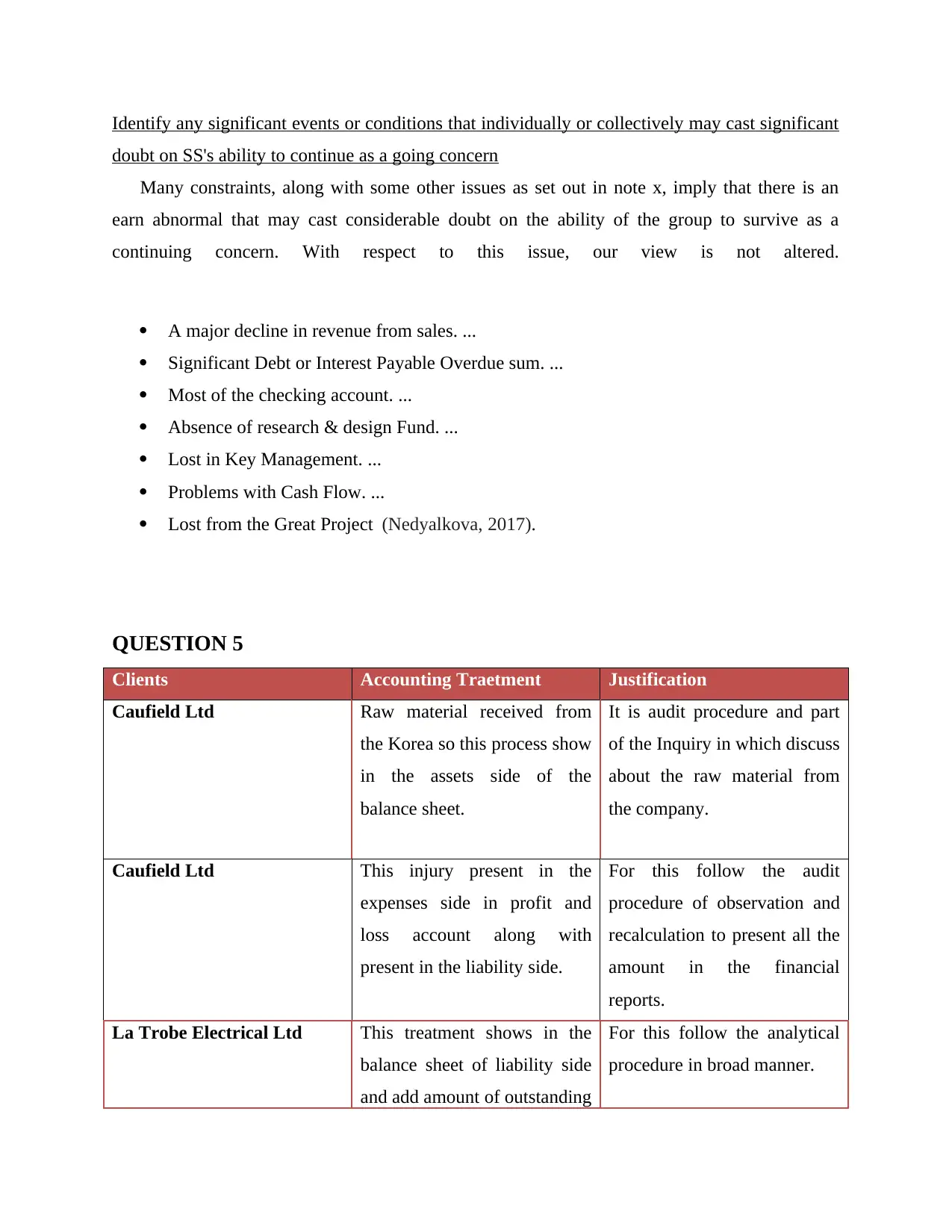

QUESTION 5

Clients Accounting Traetment Justification

Caufield Ltd Raw material received from

the Korea so this process show

in the assets side of the

balance sheet.

It is audit procedure and part

of the Inquiry in which discuss

about the raw material from

the company.

Caufield Ltd This injury present in the

expenses side in profit and

loss account along with

present in the liability side.

For this follow the audit

procedure of observation and

recalculation to present all the

amount in the financial

reports.

La Trobe Electrical Ltd This treatment shows in the

balance sheet of liability side

and add amount of outstanding

For this follow the analytical

procedure in broad manner.

doubt on SS's ability to continue as a going concern

Many constraints, along with some other issues as set out in note x, imply that there is an

earn abnormal that may cast considerable doubt on the ability of the group to survive as a

continuing concern. With respect to this issue, our view is not altered.

A major decline in revenue from sales. ...

Significant Debt or Interest Payable Overdue sum. ...

Most of the checking account. ...

Absence of research & design Fund. ...

Lost in Key Management. ...

Problems with Cash Flow. ...

Lost from the Great Project (Nedyalkova, 2017).

QUESTION 5

Clients Accounting Traetment Justification

Caufield Ltd Raw material received from

the Korea so this process show

in the assets side of the

balance sheet.

It is audit procedure and part

of the Inquiry in which discuss

about the raw material from

the company.

Caufield Ltd This injury present in the

expenses side in profit and

loss account along with

present in the liability side.

For this follow the audit

procedure of observation and

recalculation to present all the

amount in the financial

reports.

La Trobe Electrical Ltd This treatment shows in the

balance sheet of liability side

and add amount of outstanding

For this follow the analytical

procedure in broad manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shares which is considering as

liability.

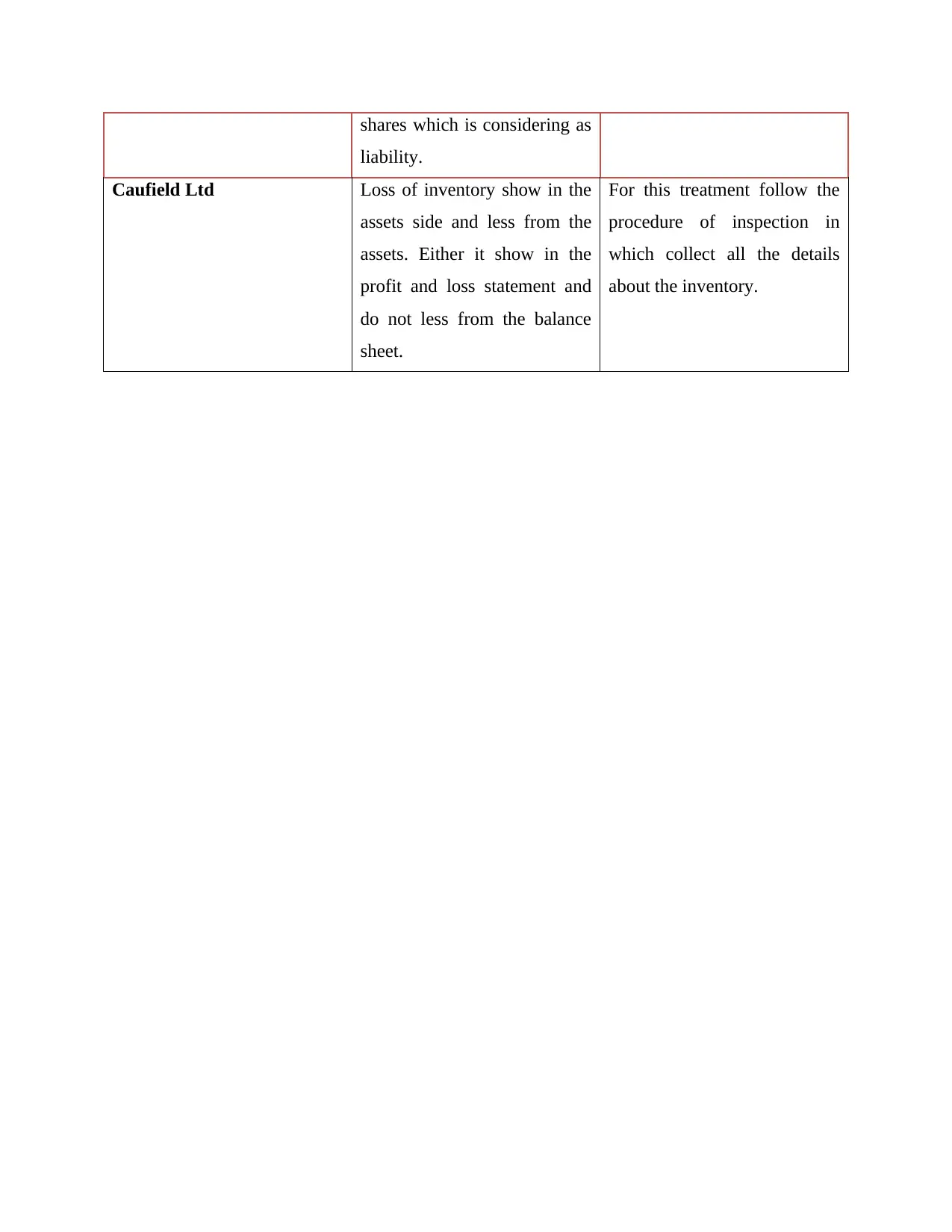

Caufield Ltd Loss of inventory show in the

assets side and less from the

assets. Either it show in the

profit and loss statement and

do not less from the balance

sheet.

For this treatment follow the

procedure of inspection in

which collect all the details

about the inventory.

liability.

Caufield Ltd Loss of inventory show in the

assets side and less from the

assets. Either it show in the

profit and loss statement and

do not less from the balance

sheet.

For this treatment follow the

procedure of inspection in

which collect all the details

about the inventory.

REFERENCES

Books and Journals

Axén, L., 2018. Exploring the association between the content of internal audit disclosures and

external audit fees: Evidence from Sweden. International Journal of Auditing. 22(2).

pp.285-297.

Bradbury, M. E., 2017. Large audit firm premium and audit specialisation in the public

sector. Accounting & Finance. 57(3). pp.657-679.

Cohen, M. and Rozario, A., 2019. Exploring the Use of Robotic Process Automation (RPA) in

Substantive Audit Procedures. The CPA Journal, 89(7), pp.49-53.

Denisov, I. V., Khachaturyan, M. V. and Umnova, M. G., 2018. Corporate social responsibility

in Russian companies: Introduction of social audit as assurance of

quality. Calitatea. 19(164). pp.63-73.

Engage, E., 2019. Textual-Analysis for Research in Professional Judgment and Decision

Making, Audit and Assurance, Risk, Control, Governance, and Regulation.

Lenz, R., Sarens, G. and Hoos, F., 2017. Internal audit effectiveness: multiple case study

research involving chief audit executives and senior management. EDPACS. 55(1). pp.1-

17.

Nedyalkova, P., 2017. Study on the factors affecting the assessment of internal audit in the

public sector. International Journal of Business and Social Science. 8(7).

Books and Journals

Axén, L., 2018. Exploring the association between the content of internal audit disclosures and

external audit fees: Evidence from Sweden. International Journal of Auditing. 22(2).

pp.285-297.

Bradbury, M. E., 2017. Large audit firm premium and audit specialisation in the public

sector. Accounting & Finance. 57(3). pp.657-679.

Cohen, M. and Rozario, A., 2019. Exploring the Use of Robotic Process Automation (RPA) in

Substantive Audit Procedures. The CPA Journal, 89(7), pp.49-53.

Denisov, I. V., Khachaturyan, M. V. and Umnova, M. G., 2018. Corporate social responsibility

in Russian companies: Introduction of social audit as assurance of

quality. Calitatea. 19(164). pp.63-73.

Engage, E., 2019. Textual-Analysis for Research in Professional Judgment and Decision

Making, Audit and Assurance, Risk, Control, Governance, and Regulation.

Lenz, R., Sarens, G. and Hoos, F., 2017. Internal audit effectiveness: multiple case study

research involving chief audit executives and senior management. EDPACS. 55(1). pp.1-

17.

Nedyalkova, P., 2017. Study on the factors affecting the assessment of internal audit in the

public sector. International Journal of Business and Social Science. 8(7).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.