Comprehensive Financial Audit Report for BML Ltd. Analysis

VerifiedAdded on 2021/06/14

|12

|3019

|33

Report

AI Summary

This report presents a comprehensive financial analysis of BML Ltd., focusing on identifying weaknesses in its internal controls and suggesting corrective measures. The analysis includes an examination of financial ratios, assessment of audit risks related to plant and equipment, machinery finance liabilities, and accounts receivables. The report also delves into the company's business risks, such as the obsolescence of machinery and market fluctuations, and their implications on financial performance. Furthermore, it evaluates the effectiveness of existing internal controls and proposes enhancements, particularly in inventory management, receivables software, and accounting software. The report also highlights specific weaknesses in the payroll contract's internal control system and suggests improvements such as maintaining soft copies of employee details and automating time tracking. The findings aim to provide insights into the company's financial health and offer recommendations for improved risk management and operational efficiency.

Running head: AUDIT

Audit

Name of the Student:

Name of the University:

Authors Note:

Audit

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT

Executive summary:

The various aspects that might affect the BML Ltd. performance over the years have been

discussed in the following report. Finding out the weakness in the internal control of the

company and to suggest the ways of remediating them is the prime focus of the report. For

achievement of the purpose various financial and non-financial information available with the

auditor will be utilised.

Executive summary:

The various aspects that might affect the BML Ltd. performance over the years have been

discussed in the following report. Finding out the weakness in the internal control of the

company and to suggest the ways of remediating them is the prime focus of the report. For

achievement of the purpose various financial and non-financial information available with the

auditor will be utilised.

2AUDIT

Table of Contents

Introduction:...............................................................................................................................3

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:........................................................................................................................3

Analysis of the ratios and the additional information to determine the risks faced by the

company:....................................................................................................................................6

Internal controls that are effective, risks that they alleviate and the test of control to check

them............................................................................................................................................9

Identification of the weaknesses in the internal control for contract payroll:..........................10

Conclusion:..............................................................................................................................11

Reference..................................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................3

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:........................................................................................................................3

Analysis of the ratios and the additional information to determine the risks faced by the

company:....................................................................................................................................6

Internal controls that are effective, risks that they alleviate and the test of control to check

them............................................................................................................................................9

Identification of the weaknesses in the internal control for contract payroll:..........................10

Conclusion:..............................................................................................................................11

Reference..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT

Introduction:

The following report presents the analysis of all the financial and the non –financial

aspect so the company. The purpose of the analysis is to determine the weaknesses that are

present in the internal control of the company. After the weaknesses of the internal control of

the company are being identified, an effort will be made to determine their implication on the

audit risk of the company. In addition to that an effort will be made to alleviate, the various

risk faced by the company (William et al., 2016).

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:

Account Analysis Audit risk Audit steps to reduce

risk

Plantand

equipment

It has been seen over the period of 18

months that the assets of the company

had to encounter a significant decrease

in their utility due to the obsolescence

of the mechanical equipment’s prior to

the use oftechnology-aided machinery.

The company is facing the risk of

losing its present customers and the

viability of its operations in the event it

fails to replace the aging machinery

with the new computer aided ones

(Rezaee et al.,2018). The requirement

of the company in respect of the plant

and machinery has changed drastically

over the period. The company needs to

Of the significant audit risk

present in the present case is

that of the right treatment of

the deprecation or rather

determination of a policy that

will most efficiently reflect

the changes that has happened

in the recent times in respect

of the value of the assets and

factor in that information to

determine the depreciation

amount of the assets (Wang et

al., 2015). In addition to that,

the present share of the

market held by the company

Several steps can be

taken by the auditor to

reduce the risks. On of

them include the

physical verification of

the assets. The reason

being that the auditor

will get an idea

regarding the revenue

generating capacity of

the asset. In addition to

this, the auditor must

make sure that the

company makes use of

such accounting policy

Introduction:

The following report presents the analysis of all the financial and the non –financial

aspect so the company. The purpose of the analysis is to determine the weaknesses that are

present in the internal control of the company. After the weaknesses of the internal control of

the company are being identified, an effort will be made to determine their implication on the

audit risk of the company. In addition to that an effort will be made to alleviate, the various

risk faced by the company (William et al., 2016).

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:

Account Analysis Audit risk Audit steps to reduce

risk

Plantand

equipment

It has been seen over the period of 18

months that the assets of the company

had to encounter a significant decrease

in their utility due to the obsolescence

of the mechanical equipment’s prior to

the use oftechnology-aided machinery.

The company is facing the risk of

losing its present customers and the

viability of its operations in the event it

fails to replace the aging machinery

with the new computer aided ones

(Rezaee et al.,2018). The requirement

of the company in respect of the plant

and machinery has changed drastically

over the period. The company needs to

Of the significant audit risk

present in the present case is

that of the right treatment of

the deprecation or rather

determination of a policy that

will most efficiently reflect

the changes that has happened

in the recent times in respect

of the value of the assets and

factor in that information to

determine the depreciation

amount of the assets (Wang et

al., 2015). In addition to that,

the present share of the

market held by the company

Several steps can be

taken by the auditor to

reduce the risks. On of

them include the

physical verification of

the assets. The reason

being that the auditor

will get an idea

regarding the revenue

generating capacity of

the asset. In addition to

this, the auditor must

make sure that the

company makes use of

such accounting policy

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT

address the issue of incapacity of the

present fleet of machinery to generate

the revenue and income for the

company and the issue of adopting a

policy of depreciation that can better

reflect the recent changes in the

environment of the company.

has reduced significantly over

the years. The company needs

to address the issue very

objectively to determine the

real reduction in the value of

the assets (Alles et al., 2018).

The reason being that the

circumstance in which the

machineries were bought and

the present circumstances of

the company

haschangedcompletely.

in respect of the

depreciation that

objectively recognises

the amount to be

recorded in the

finalcoalstatementsof

the company in respect

of the depreciation.

Machinery

finance

liabilities

The company, in order to meet up with

the requirement of the computer-aided

machinery took a huge loan for the

financing of the assets of the company.

In addition to that, the company had

also originally taken loans for

purchasing the old machineries, which

the company was presently operating.

Hence, the accumulation of all such

liabilities has increased the financial

liabilities of the company (Chan &

Vasarhelyi, 2018). It is necessary that

the revenue generation capacity of the

new assets acquired by the company

compensate the finance cost of the

The audit risk faced by the

auditor is to determine

reliably the revenue

generating capacity of the

entity. The auditor will also

determine the amount to be

recognised in respect of the

reduction in the market share

of the company and thereby

the reduction in the revenue

generation capacity of the

company. This may hamper

the liquidity position of the

company.

Some of the

steps to be

taken up by

the auditor to

reduce the

risks are as

follows:

a) To analyse

the debt

taken by

the

company

very

carefully.

address the issue of incapacity of the

present fleet of machinery to generate

the revenue and income for the

company and the issue of adopting a

policy of depreciation that can better

reflect the recent changes in the

environment of the company.

has reduced significantly over

the years. The company needs

to address the issue very

objectively to determine the

real reduction in the value of

the assets (Alles et al., 2018).

The reason being that the

circumstance in which the

machineries were bought and

the present circumstances of

the company

haschangedcompletely.

in respect of the

depreciation that

objectively recognises

the amount to be

recorded in the

finalcoalstatementsof

the company in respect

of the depreciation.

Machinery

finance

liabilities

The company, in order to meet up with

the requirement of the computer-aided

machinery took a huge loan for the

financing of the assets of the company.

In addition to that, the company had

also originally taken loans for

purchasing the old machineries, which

the company was presently operating.

Hence, the accumulation of all such

liabilities has increased the financial

liabilities of the company (Chan &

Vasarhelyi, 2018). It is necessary that

the revenue generation capacity of the

new assets acquired by the company

compensate the finance cost of the

The audit risk faced by the

auditor is to determine

reliably the revenue

generating capacity of the

entity. The auditor will also

determine the amount to be

recognised in respect of the

reduction in the market share

of the company and thereby

the reduction in the revenue

generation capacity of the

company. This may hamper

the liquidity position of the

company.

Some of the

steps to be

taken up by

the auditor to

reduce the

risks are as

follows:

a) To analyse

the debt

taken by

the

company

very

carefully.

5AUDIT

company. Ina

addition to

this

finding out

the period

of time for

which the

debt has

been taken

by the

company.

b) The

auditor

should

also

objectivel

y calculate

the

amount of

revenue to

be

generated

by the

company

in the near

company. Ina

addition to

this

finding out

the period

of time for

which the

debt has

been taken

by the

company.

b) The

auditor

should

also

objectivel

y calculate

the

amount of

revenue to

be

generated

by the

company

in the near

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

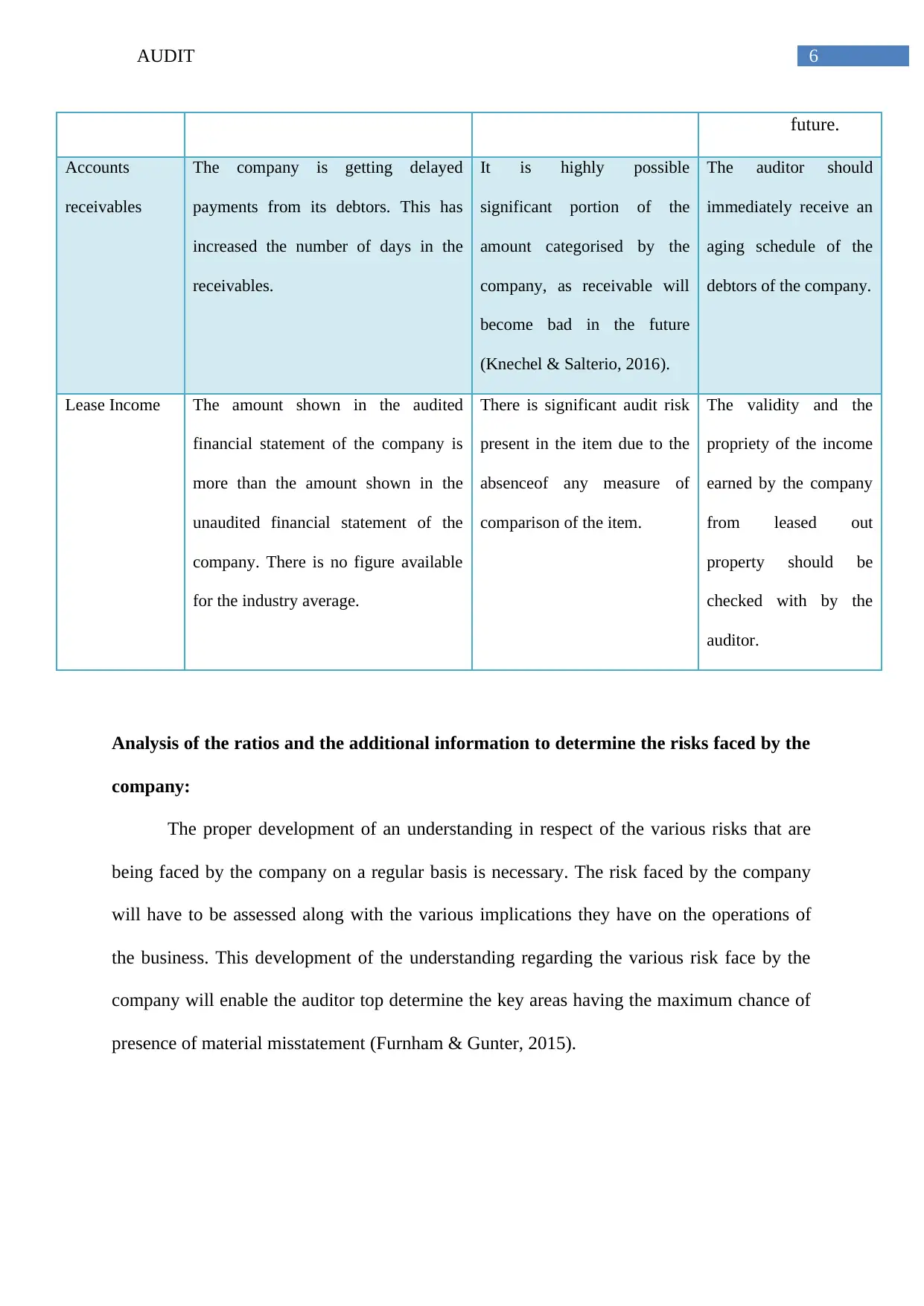

6AUDIT

future.

Accounts

receivables

The company is getting delayed

payments from its debtors. This has

increased the number of days in the

receivables.

It is highly possible

significant portion of the

amount categorised by the

company, as receivable will

become bad in the future

(Knechel & Salterio, 2016).

The auditor should

immediately receive an

aging schedule of the

debtors of the company.

Lease Income The amount shown in the audited

financial statement of the company is

more than the amount shown in the

unaudited financial statement of the

company. There is no figure available

for the industry average.

There is significant audit risk

present in the item due to the

absenceof any measure of

comparison of the item.

The validity and the

propriety of the income

earned by the company

from leased out

property should be

checked with by the

auditor.

Analysis of the ratios and the additional information to determine the risks faced by the

company:

The proper development of an understanding in respect of the various risks that are

being faced by the company on a regular basis is necessary. The risk faced by the company

will have to be assessed along with the various implications they have on the operations of

the business. This development of the understanding regarding the various risk face by the

company will enable the auditor top determine the key areas having the maximum chance of

presence of material misstatement (Furnham & Gunter, 2015).

future.

Accounts

receivables

The company is getting delayed

payments from its debtors. This has

increased the number of days in the

receivables.

It is highly possible

significant portion of the

amount categorised by the

company, as receivable will

become bad in the future

(Knechel & Salterio, 2016).

The auditor should

immediately receive an

aging schedule of the

debtors of the company.

Lease Income The amount shown in the audited

financial statement of the company is

more than the amount shown in the

unaudited financial statement of the

company. There is no figure available

for the industry average.

There is significant audit risk

present in the item due to the

absenceof any measure of

comparison of the item.

The validity and the

propriety of the income

earned by the company

from leased out

property should be

checked with by the

auditor.

Analysis of the ratios and the additional information to determine the risks faced by the

company:

The proper development of an understanding in respect of the various risks that are

being faced by the company on a regular basis is necessary. The risk faced by the company

will have to be assessed along with the various implications they have on the operations of

the business. This development of the understanding regarding the various risk face by the

company will enable the auditor top determine the key areas having the maximum chance of

presence of material misstatement (Furnham & Gunter, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT

The additional information has also presented some of the other business risks in the

operations of the company. They are as follows:

a) The present inventory of machinery operated by the company is unable to generate

revenue for it because of the advent of the computer-aidedmachinery in the market.

Hence, the company will need to replace its entire inventory consisting of only such

machinery, whichdoes not make use of computer aid (Griffiths, 2016).

b) The amount of finance required by the company has increased over the years due the

fact that the company will be requiring more funds to finance the new machineries to

be purchased by it, which will utilise the aid of computer for functioning (He et

al.,2015).

c) The metal industry have gone through several fluctuations over the period and the

same has affected the operations of the business in the following manner:

i) There has been a downfall in the gold market of around 24.85% since the year

2012.

ii) There has been a downfall in the iron ore market amounting to 43.78% since

the year 2012.

d) The additional funds that have been acquired by the company for financing its new

machineries come with a huge financial burden that will have to be borne by the

company in the future.

e) The new machineries, which are being operated by the company using the latest

computer technologies, will require employees who have superior training and will

definitely demand higher salaries (Cannon & Bedard, 2016). Hence, the company will

have to bear higher employee costs for the year.

The presence of the business risk in the operation of the company is substantiated by the

results of the ratio analysis as follows:

The additional information has also presented some of the other business risks in the

operations of the company. They are as follows:

a) The present inventory of machinery operated by the company is unable to generate

revenue for it because of the advent of the computer-aidedmachinery in the market.

Hence, the company will need to replace its entire inventory consisting of only such

machinery, whichdoes not make use of computer aid (Griffiths, 2016).

b) The amount of finance required by the company has increased over the years due the

fact that the company will be requiring more funds to finance the new machineries to

be purchased by it, which will utilise the aid of computer for functioning (He et

al.,2015).

c) The metal industry have gone through several fluctuations over the period and the

same has affected the operations of the business in the following manner:

i) There has been a downfall in the gold market of around 24.85% since the year

2012.

ii) There has been a downfall in the iron ore market amounting to 43.78% since

the year 2012.

d) The additional funds that have been acquired by the company for financing its new

machineries come with a huge financial burden that will have to be borne by the

company in the future.

e) The new machineries, which are being operated by the company using the latest

computer technologies, will require employees who have superior training and will

definitely demand higher salaries (Cannon & Bedard, 2016). Hence, the company will

have to bear higher employee costs for the year.

The presence of the business risk in the operation of the company is substantiated by the

results of the ratio analysis as follows:

8AUDIT

a) The industry average in respect of the Rerun on Assets is significantly higher than the

company’s figure.

b) The industry average of Return on Equity is higher than the figures of the company.

c) The profit margin prevalent in the industry is significantly higher than that earned by

the company.

Some of the business risks that can be identified from the ratio analysis are as follows:

a) The difference between the audited and the unaudited financial statements of the

company is substantial. The reason for this might be because of the fault and mistakes

committed by the accountant of the company or due to the lack of efficiency of the

software implemented by the company for the purpose of preparation and presentation

of the financial statements of the company (Demb et al.,2017).

b) The time taken by the debtors to make the payment to the company in respectof the

amount due from them by the company is very long. The lag in the payment made by

the debtors is significantly confirmed by the figures of the financial statement so the

company.

Internal controls that are effective, risks that they alleviate and the test of control to

check them.

Control Risk Alleviated Test of Control

Inventory control system:

The company neds to update the

inverntory control

system so as to remain

updated to measure the

obsolescence of its

It will alleviate the risk of over

obsolescence of the inventory of

the company

The company must put in all the

details of the present inventory

and check for the correctness of

the present obsolescence shown

by the system.

a) The industry average in respect of the Rerun on Assets is significantly higher than the

company’s figure.

b) The industry average of Return on Equity is higher than the figures of the company.

c) The profit margin prevalent in the industry is significantly higher than that earned by

the company.

Some of the business risks that can be identified from the ratio analysis are as follows:

a) The difference between the audited and the unaudited financial statements of the

company is substantial. The reason for this might be because of the fault and mistakes

committed by the accountant of the company or due to the lack of efficiency of the

software implemented by the company for the purpose of preparation and presentation

of the financial statements of the company (Demb et al.,2017).

b) The time taken by the debtors to make the payment to the company in respectof the

amount due from them by the company is very long. The lag in the payment made by

the debtors is significantly confirmed by the figures of the financial statement so the

company.

Internal controls that are effective, risks that they alleviate and the test of control to

check them.

Control Risk Alleviated Test of Control

Inventory control system:

The company neds to update the

inverntory control

system so as to remain

updated to measure the

obsolescence of its

It will alleviate the risk of over

obsolescence of the inventory of

the company

The company must put in all the

details of the present inventory

and check for the correctness of

the present obsolescence shown

by the system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT

present inventory.

Software for receivables

management:

Adoption of such softwares will

enable the detailed record

keeping by the company of all

the debtors of the company. It

will intimidate the company

regarding the payment due from

each individual and at the same

time enable the debtor to

recognise that the payment has

to be made.

The use of the systemwill

enable the company to reduce

or eliminate the risk of bad debt

completely (Griffin & Wright,

2015).

The debtors at present are

making very late payments and

hence the present system will

keep the detailed records of all

the debtors of the company to

ensure timely payment.

Use of effective and efficient

accounting softwares:

The company as of now has

failed to reduce the difference

between the amount presented

in the audited and the amount in

the unaudited financial

statements. Confirming that it is

incapable of preparing accurate

financial statements (Yu et al.,

2015).

The software will eliminate the

risk of faulty and inappropriate

recording by the company in its

financial statements. Significant

matter will be given more focus

by the auditor rather than all the

petty sues.

The accounting software must

be provided an input in respect

of all the recent amendments

that have been prescribed by the

statute for compliance.

present inventory.

Software for receivables

management:

Adoption of such softwares will

enable the detailed record

keeping by the company of all

the debtors of the company. It

will intimidate the company

regarding the payment due from

each individual and at the same

time enable the debtor to

recognise that the payment has

to be made.

The use of the systemwill

enable the company to reduce

or eliminate the risk of bad debt

completely (Griffin & Wright,

2015).

The debtors at present are

making very late payments and

hence the present system will

keep the detailed records of all

the debtors of the company to

ensure timely payment.

Use of effective and efficient

accounting softwares:

The company as of now has

failed to reduce the difference

between the amount presented

in the audited and the amount in

the unaudited financial

statements. Confirming that it is

incapable of preparing accurate

financial statements (Yu et al.,

2015).

The software will eliminate the

risk of faulty and inappropriate

recording by the company in its

financial statements. Significant

matter will be given more focus

by the auditor rather than all the

petty sues.

The accounting software must

be provided an input in respect

of all the recent amendments

that have been prescribed by the

statute for compliance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT

Identification of the weaknesses in the internal control for contract payroll:

In respect to the internal control of the payroll contract of the company, certain weaknesses in

the internal control system of the company are as follows:

a) The company should maintain he soft copy of the employee details along with the

hard copy of the details. The reason being that it is easy to lose the hard copy and it

encourages wrong input of data by the project manager (Power & Gendron, 2015).

Hence, the soft copy of the details of the employees must be kept in the computer of

the company.

b) It is physically impossible for the project manager to maintain record of the entry

times of the various employees working in the company. Hence, the practice of the

manual entry of the time of entry should be prohibited by the company and instead the

time should be automated by making use of hardware such as biometric attendance

keepers etc.

c) The entire process of recording and preparation of the financial statements of the

company is fully automated. It can lead to severe misstatement in the financial

statements of the company inn case of any error on the part of the accountant (Dennis

et al., 2018).

d) The accountant must not be provided with such log in details of the bank that can give

him access to the authentication of making payments. The reason being that it can be

misused by him to embezzle cash from the company.

e) Separate calculations should be conducted by the management of the company in

respect of the regular payments to be made to the employees of the entity and special

payments like that of the annulations fund (Griffin & Wright, 2015). This will help in

deterring the cascading effect of the error committed by the system.

Identification of the weaknesses in the internal control for contract payroll:

In respect to the internal control of the payroll contract of the company, certain weaknesses in

the internal control system of the company are as follows:

a) The company should maintain he soft copy of the employee details along with the

hard copy of the details. The reason being that it is easy to lose the hard copy and it

encourages wrong input of data by the project manager (Power & Gendron, 2015).

Hence, the soft copy of the details of the employees must be kept in the computer of

the company.

b) It is physically impossible for the project manager to maintain record of the entry

times of the various employees working in the company. Hence, the practice of the

manual entry of the time of entry should be prohibited by the company and instead the

time should be automated by making use of hardware such as biometric attendance

keepers etc.

c) The entire process of recording and preparation of the financial statements of the

company is fully automated. It can lead to severe misstatement in the financial

statements of the company inn case of any error on the part of the accountant (Dennis

et al., 2018).

d) The accountant must not be provided with such log in details of the bank that can give

him access to the authentication of making payments. The reason being that it can be

misused by him to embezzle cash from the company.

e) Separate calculations should be conducted by the management of the company in

respect of the regular payments to be made to the employees of the entity and special

payments like that of the annulations fund (Griffin & Wright, 2015). This will help in

deterring the cascading effect of the error committed by the system.

11AUDIT

Conclusion:

After conducting the detailed analysis of the financial and the non-financial factors

f0o the company, it can be concluded that the company at present is encountering huge

amount of threats from its external environment. The threats include the obsolescence of the

assets used byte company and the shrinking of the share in the market enjoyed by the

company. It has also been established from the internal control of the company is not strong

enough. In order to increase the efficiency and the effectiveness of the internal control system

of the company it should make use of the software-aided technologies.

Conclusion:

After conducting the detailed analysis of the financial and the non-financial factors

f0o the company, it can be concluded that the company at present is encountering huge

amount of threats from its external environment. The threats include the obsolescence of the

assets used byte company and the shrinking of the share in the market enjoyed by the

company. It has also been established from the internal control of the company is not strong

enough. In order to increase the efficiency and the effectiveness of the internal control system

of the company it should make use of the software-aided technologies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.