Comprehensive Audit Report: Big Machine Limited, Miller Yates Howarth

VerifiedAdded on 2021/05/31

|10

|1550

|33

Report

AI Summary

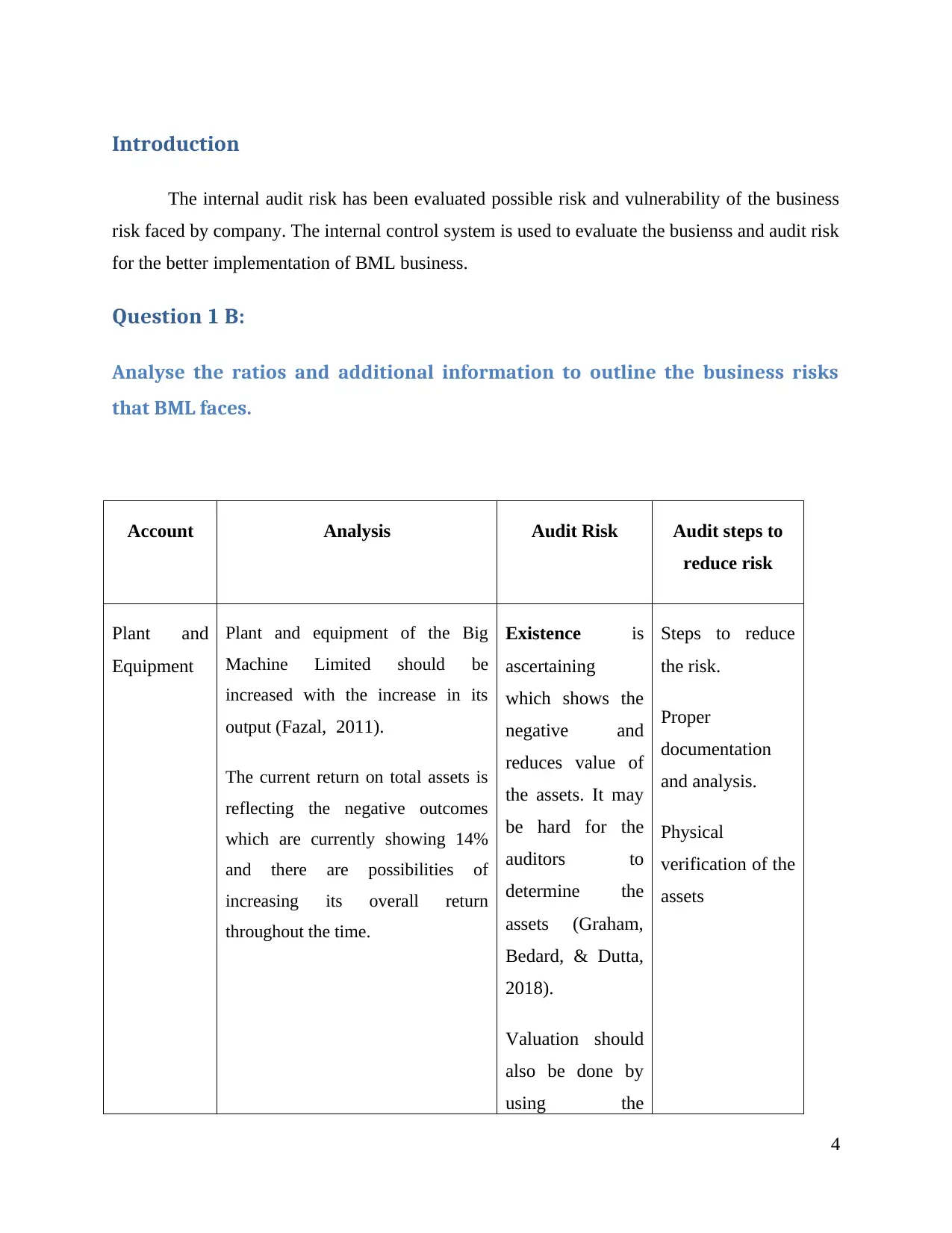

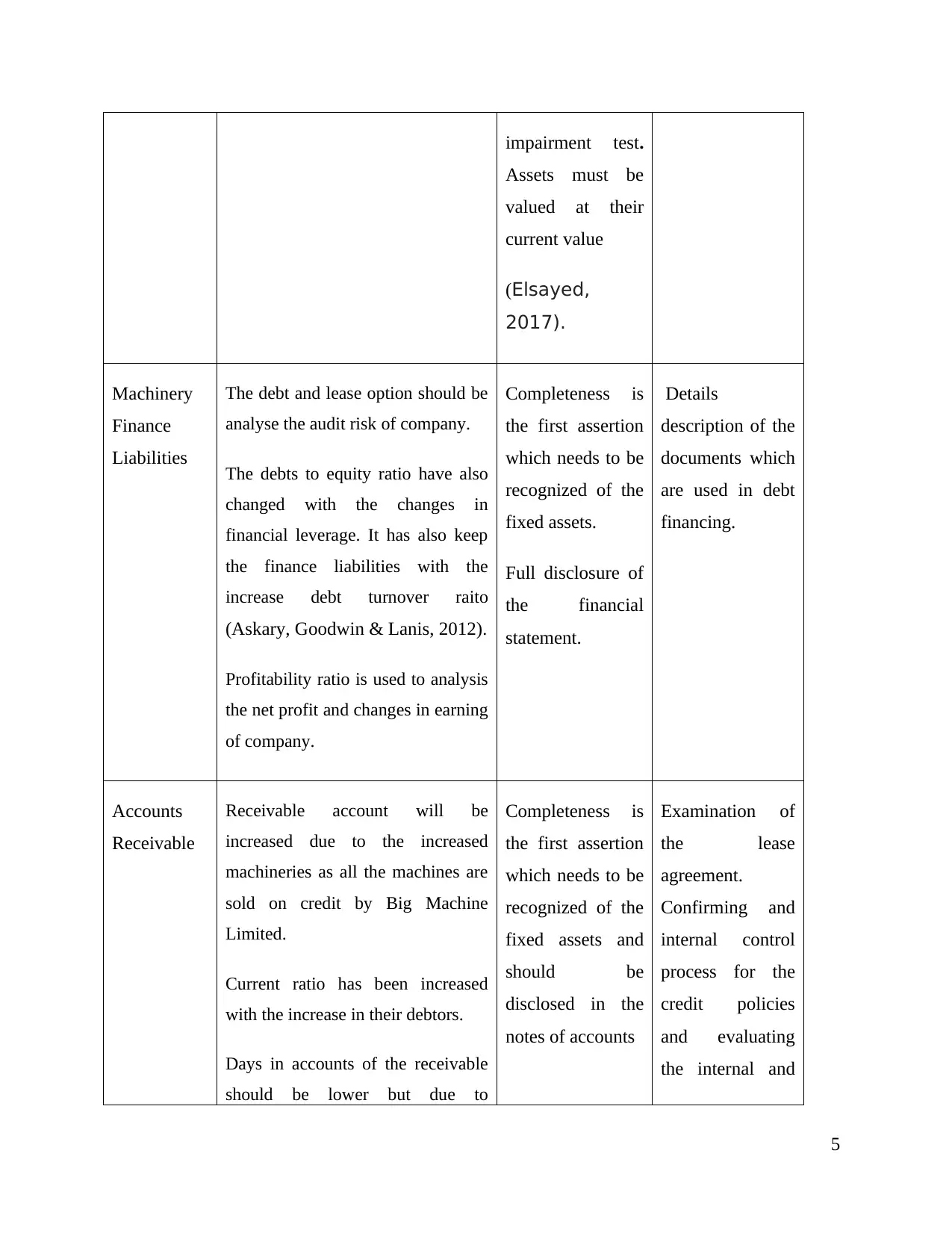

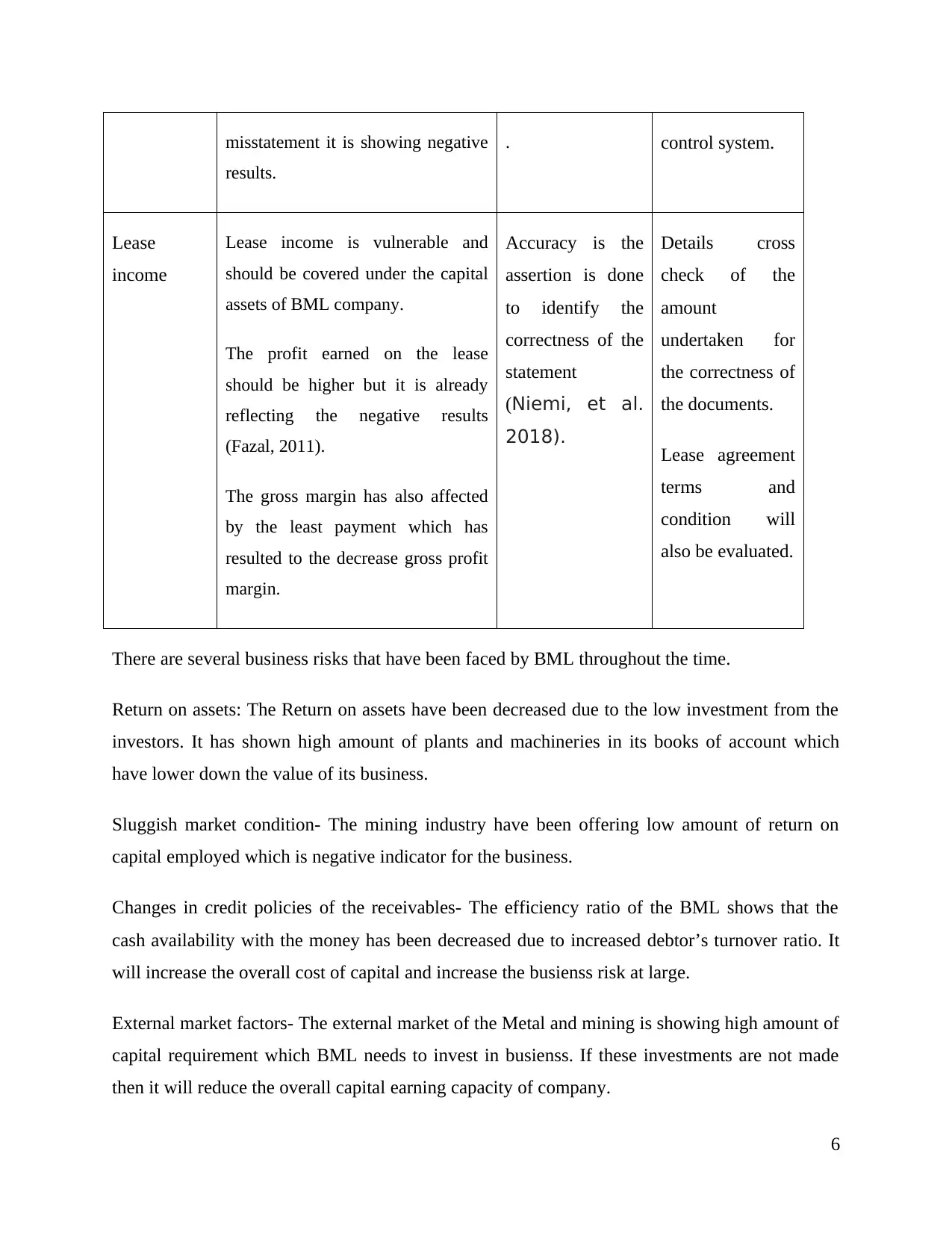

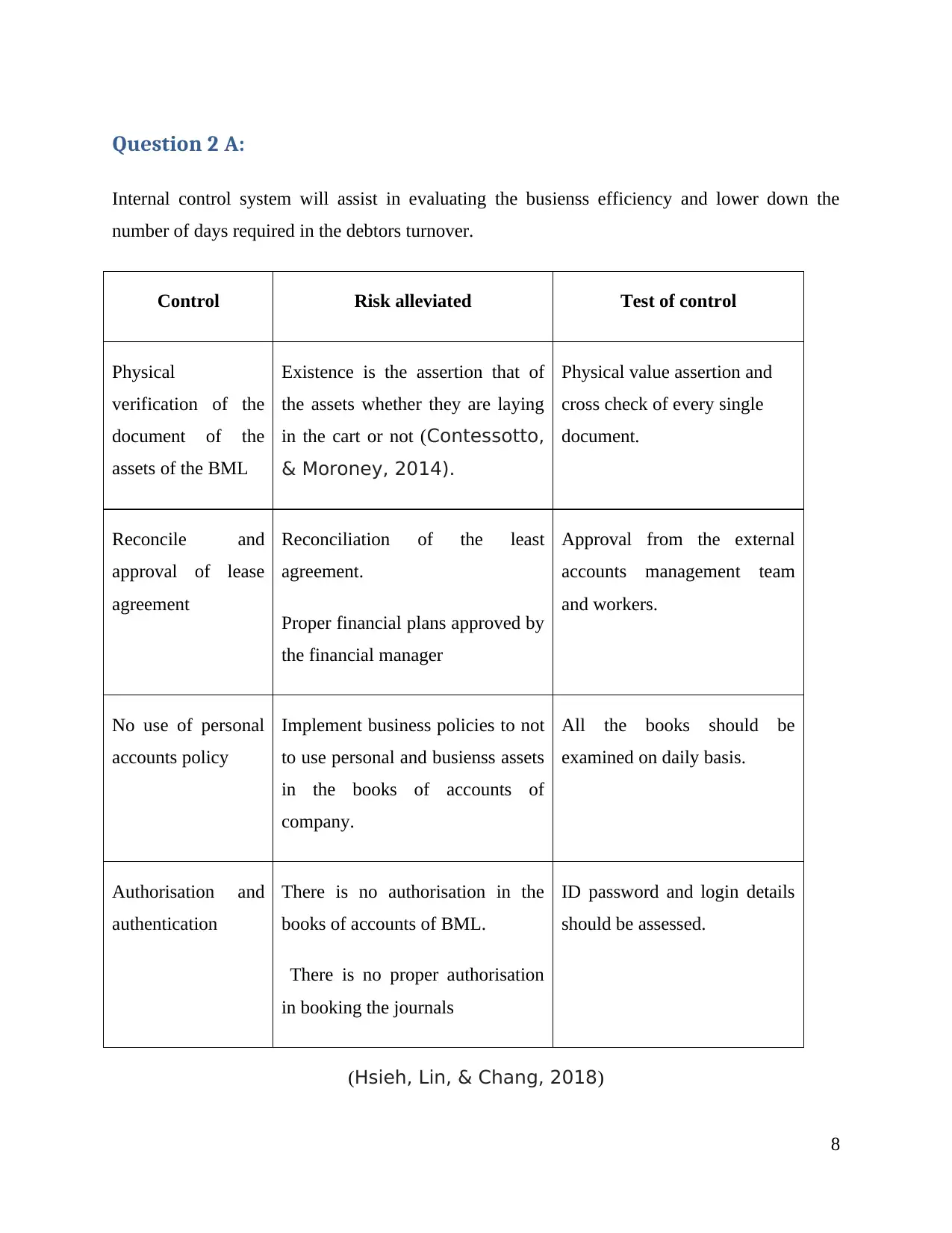

This report provides an in-depth analysis of the audit of Big Machine Limited (BML), focusing on audit planning and internal control. The report evaluates the business risks faced by BML, using ratio analysis and other financial information to identify potential vulnerabilities. It examines the current internal control system and pinpoints weaknesses, particularly in contract payroll. The report assesses audit risks related to plant and equipment, machinery finance, accounts receivable, and lease income, proposing audit steps to mitigate these risks. Furthermore, the report highlights specific issues such as the decrease in return on assets, sluggish market conditions in the mining industry, changes in credit policies, and external market factors. The report also examines the internal control system, control risk and proposes tests of control. It concludes by emphasizing the importance of effective audit control procedures to reduce business and audit risks, offering valuable insights for improving BML's financial management and operational efficiency. This report is designed to help students understand the audit process and the importance of internal controls.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.