Audit Case Study Analysis

VerifiedAdded on 2020/02/24

|10

|2392

|109

Case Study

AI Summary

This case study analyzes the audit process of DIPL, a printing press, highlighting the importance of risk identification and mitigation in auditing. It discusses inherent, control, and detection risks, emphasizing the need for proper internal controls and the potential for fraud. The study also includes a ratio analysis to assess the company's financial health and the implications of recent changes in accounting policies and IT systems.

By student name

Professor

University

Date: 27 August 2017.

Professor

University

Date: 27 August 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….8

Refrences.....……………………………………………………………….......10

1 | P a g e

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….8

Refrences.....……………………………………………………………….......10

1 | P a g e

2

Question no 1

Audit of the entity may be defined as an independent examination of the books of accounts of

an entity, whether profit making or not, small or big, government or private, prepared by the

management. It is using accounting policies and procedures and making use of the estimates and

judgements with the view to express and opinion on the financials, whether it is showing the correct

view and has been prepared on an unbiased basis. This activity post the closing of the books gives a

reasonable assurance to both the internal and external users of the financial statements, a certainty and

confidence on the figures quoted. Auditors may use diverse procedures during the audit of an entity

depending on the nature of the entity like for a manufacturing concern, emphasis would be on the

production areas, sales, purchases of raw material, for a software entity, the emphasis would be on the

manpower costs and subcontracting costs, etc. For this, they may use both the substantive and

compliance audit procedures, besides checking compliance with the regulatory and reporting norms

prescribed by Accounting board and IFRS committee. Substantive audit procedures include the checking

the recording of the incomes and expenses in the books with the respective evidences, invoices, bills,

delivery challans, whether they are properly dated and signed and stamped, whether appropriate tax

has been calculate and paid on it. Furthermore, it also includes within it ambit the verification of the

assets and liabilities recorded in the statement of affairs. This includes checking the basis on which

respective assets have been recorded, the basis on which the provision is accounted for, etc. This is

mainly performed with the objective of determining and confirming that whatever has been recorded in

the books materially exists and a false representation or the window dressing has not been done. In case

any discrepancies are noted upfront, these are brought to the notice of the management and proper

justification is asked for. All the substantive audit procedures are done with the methods including

inspection of books of accounts and calculations, observation of the records, external confirmation to be

taken from the debtors, creditors, banks, etc., inquiry from the external parties, recalculation and

reperformance of significant adjustments, etc. All these substantive procedures are mainly aimed at

getting the comfortability on the five basic assertions i.e., completeness, rights, existence, valuation and

existence of the assets and liabilities (DeZoort & Harrison 2016).

If the materiality of the errors is found to be more, the auditor has to increase the extent of the

audit procedures and apply further checking through the use of analytical audit procedures which

generally include analysis of key financial ratios, comparison of the actual from the expected and the

budgeted figures, variance analysis, etc . Besides this, the auditor also takes note of the internal control

2 | P a g e

Question no 1

Audit of the entity may be defined as an independent examination of the books of accounts of

an entity, whether profit making or not, small or big, government or private, prepared by the

management. It is using accounting policies and procedures and making use of the estimates and

judgements with the view to express and opinion on the financials, whether it is showing the correct

view and has been prepared on an unbiased basis. This activity post the closing of the books gives a

reasonable assurance to both the internal and external users of the financial statements, a certainty and

confidence on the figures quoted. Auditors may use diverse procedures during the audit of an entity

depending on the nature of the entity like for a manufacturing concern, emphasis would be on the

production areas, sales, purchases of raw material, for a software entity, the emphasis would be on the

manpower costs and subcontracting costs, etc. For this, they may use both the substantive and

compliance audit procedures, besides checking compliance with the regulatory and reporting norms

prescribed by Accounting board and IFRS committee. Substantive audit procedures include the checking

the recording of the incomes and expenses in the books with the respective evidences, invoices, bills,

delivery challans, whether they are properly dated and signed and stamped, whether appropriate tax

has been calculate and paid on it. Furthermore, it also includes within it ambit the verification of the

assets and liabilities recorded in the statement of affairs. This includes checking the basis on which

respective assets have been recorded, the basis on which the provision is accounted for, etc. This is

mainly performed with the objective of determining and confirming that whatever has been recorded in

the books materially exists and a false representation or the window dressing has not been done. In case

any discrepancies are noted upfront, these are brought to the notice of the management and proper

justification is asked for. All the substantive audit procedures are done with the methods including

inspection of books of accounts and calculations, observation of the records, external confirmation to be

taken from the debtors, creditors, banks, etc., inquiry from the external parties, recalculation and

reperformance of significant adjustments, etc. All these substantive procedures are mainly aimed at

getting the comfortability on the five basic assertions i.e., completeness, rights, existence, valuation and

existence of the assets and liabilities (DeZoort & Harrison 2016).

If the materiality of the errors is found to be more, the auditor has to increase the extent of the

audit procedures and apply further checking through the use of analytical audit procedures which

generally include analysis of key financial ratios, comparison of the actual from the expected and the

budgeted figures, variance analysis, etc . Besides this, the auditor also takes note of the internal control

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

existing in the organisation, if it is strongly built, then the risk would be low and hence the level of

checking required would be less. Similarly, if the internal control processes and test of designs are

adequately built in the organisation, then automatically the risks would be low and hence the level of

checking would be low. All this helps the auditor to plan the audit and to determine the nature, extent

and timing of the audit (Sonu, Ahn & Choi 2017).

In the case study, DIPL is a printing press, which is being subject to audit by Stewart and Kathy,

the newly appointed auditors of the company. The company has undergone many changes with respect

to the change in the accounting policies and internal IT system, which again was implemented without

much testing and validation by the management, therefore the need to do the extended verification and

checking arises so that they can give the reasonable assurance about the financials to its users. We have

done the ratio analysis based on the information given for the last three financial years to check the

status of liquidity, asset management, debt management and solvency, etc (Raiborn, Butler & Martin

2016).

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

Ratio Analysis

1. Short term solvency or liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

3 | P a g e

existing in the organisation, if it is strongly built, then the risk would be low and hence the level of

checking required would be less. Similarly, if the internal control processes and test of designs are

adequately built in the organisation, then automatically the risks would be low and hence the level of

checking would be low. All this helps the auditor to plan the audit and to determine the nature, extent

and timing of the audit (Sonu, Ahn & Choi 2017).

In the case study, DIPL is a printing press, which is being subject to audit by Stewart and Kathy,

the newly appointed auditors of the company. The company has undergone many changes with respect

to the change in the accounting policies and internal IT system, which again was implemented without

much testing and validation by the management, therefore the need to do the extended verification and

checking arises so that they can give the reasonable assurance about the financials to its users. We have

done the ratio analysis based on the information given for the last three financial years to check the

status of liquidity, asset management, debt management and solvency, etc (Raiborn, Butler & Martin

2016).

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

Ratio Analysis

1. Short term solvency or liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

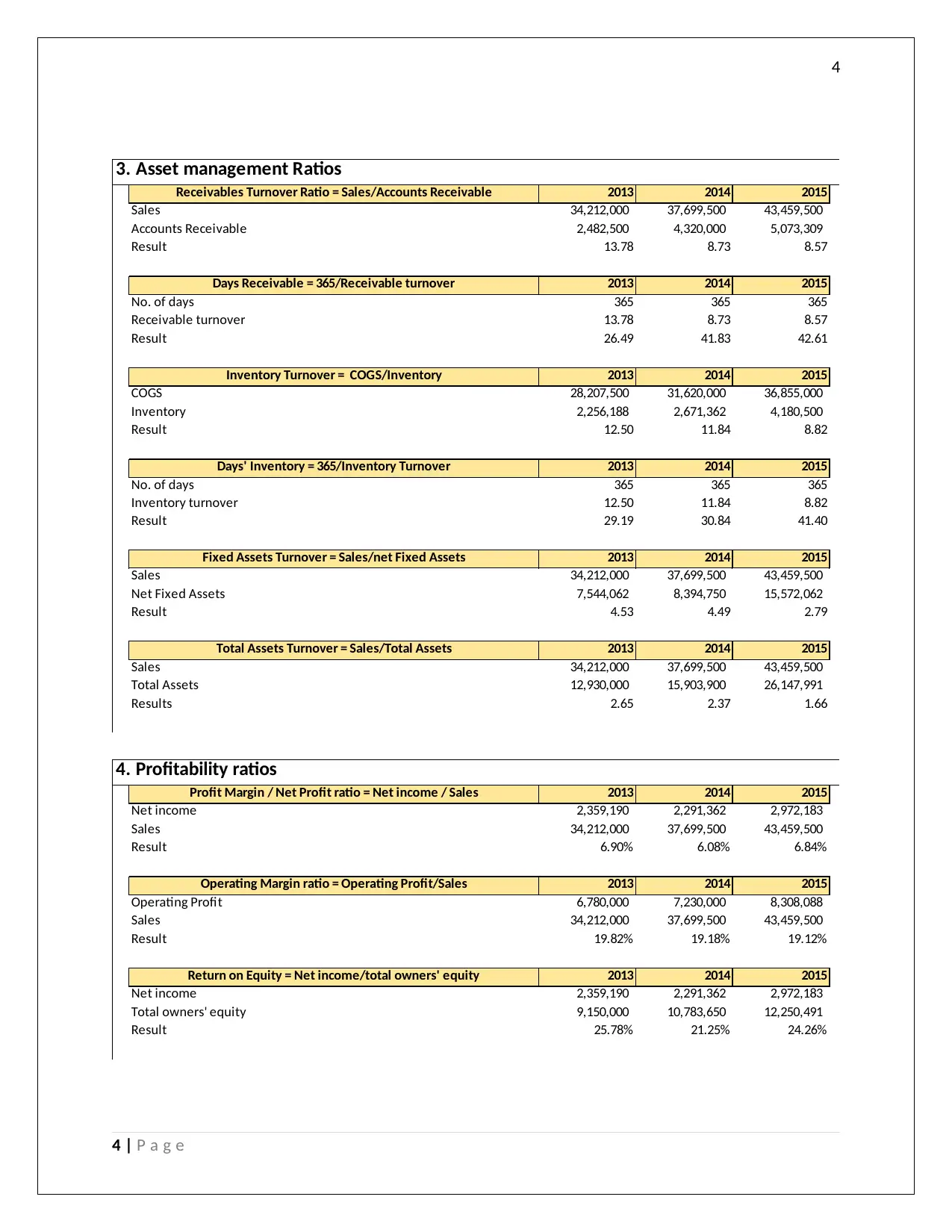

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

3. Asset management Ratios

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

4. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

4 | P a g e

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

3. Asset management Ratios

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

4. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

4 | P a g e

5

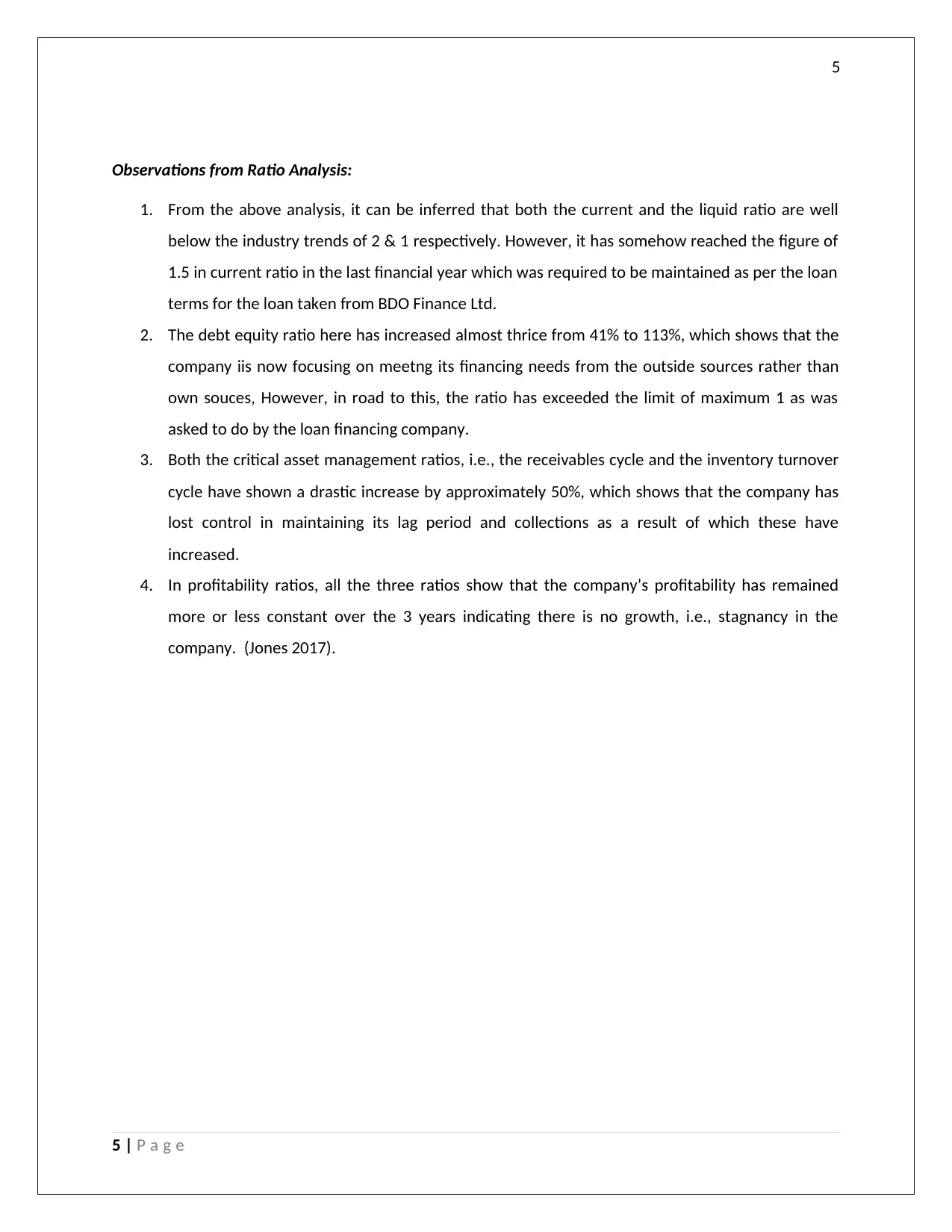

Observations from Ratio Analysis:

1. From the above analysis, it can be inferred that both the current and the liquid ratio are well

below the industry trends of 2 & 1 respectively. However, it has somehow reached the figure of

1.5 in current ratio in the last financial year which was required to be maintained as per the loan

terms for the loan taken from BDO Finance Ltd.

2. The debt equity ratio here has increased almost thrice from 41% to 113%, which shows that the

company iis now focusing on meetng its financing needs from the outside sources rather than

own souces, However, in road to this, the ratio has exceeded the limit of maximum 1 as was

asked to do by the loan financing company.

3. Both the critical asset management ratios, i.e., the receivables cycle and the inventory turnover

cycle have shown a drastic increase by approximately 50%, which shows that the company has

lost control in maintaining its lag period and collections as a result of which these have

increased.

4. In profitability ratios, all the three ratios show that the company’s profitability has remained

more or less constant over the 3 years indicating there is no growth, i.e., stagnancy in the

company. (Jones 2017).

5 | P a g e

Observations from Ratio Analysis:

1. From the above analysis, it can be inferred that both the current and the liquid ratio are well

below the industry trends of 2 & 1 respectively. However, it has somehow reached the figure of

1.5 in current ratio in the last financial year which was required to be maintained as per the loan

terms for the loan taken from BDO Finance Ltd.

2. The debt equity ratio here has increased almost thrice from 41% to 113%, which shows that the

company iis now focusing on meetng its financing needs from the outside sources rather than

own souces, However, in road to this, the ratio has exceeded the limit of maximum 1 as was

asked to do by the loan financing company.

3. Both the critical asset management ratios, i.e., the receivables cycle and the inventory turnover

cycle have shown a drastic increase by approximately 50%, which shows that the company has

lost control in maintaining its lag period and collections as a result of which these have

increased.

4. In profitability ratios, all the three ratios show that the company’s profitability has remained

more or less constant over the 3 years indicating there is no growth, i.e., stagnancy in the

company. (Jones 2017).

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Solution 2.

Risk identification and mitigation is an important part of nay audit. It is very important that auditor must

verify all the records properly so that any kind of risk can be mitigated. It is important on part of the

management to support the auditor in all these cases. Three types of risk are a part of the overall

auditing process. The first type of risk is inherent risk. Inherent risk in cases where even if the

management establishes control, it is not in its hand. This risk does not occur in the general day-to-day

activities. These risks cannot be eliminated from the system, they can only be reduced. The second type

of risk is the control risk, which occurs when the management has not installed that proper internal

control measures, it occurs because of lack of proper management. The management can be held

responsible for any kind of damage that might occur because of the same. The last major type of risk is

the detection risk which happens when the management, accountant or the auditors fails to identify the

errors and flaws in the accounting books and system. The auditor can be held responsible for the same,

and it occurs due to lack of professional scepticism on his part (Grenier 2017).

The case study of DIPL has many risk factors, the major amongst which are two. First, the company is

changing the routine transactions and methods that are used in the course of accounting. The company

is adopting new methods without any proper research. It is highly possible that it will lead to

misstatement in the books of account of the company. Here, the company has calculated the

depreciation using 20 years useful life of the assets as compared to the industry where the useful life

has been assumed to be 30 years. It is also changing the method of valuation of the inventories (Knechel

& Salterio 2016). All these might lead to over or undervaluation of the accounts and affect the overall

functioning of the company. Thus, it is the duty of the company that proper disclosures are given in the

books of account, the auditor must check the validity of the same and then make an opinion. It will help

in reduction of the overall risk factor that might be involved. The major inherent risk that the company is

suffering with is the installation of the new IT system without proper planning, testing and control. The

company is undertaking the same, without conducting nay reconciliation or research. It might affect the

overall productivity of the company. The books might be over or dune valued because of the same. It is

thus important that before applying such changes, the management of the company must take expert

opinion from outsiders, must judge the overall profitability of the system and then take a decision on

6 | P a g e

Solution 2.

Risk identification and mitigation is an important part of nay audit. It is very important that auditor must

verify all the records properly so that any kind of risk can be mitigated. It is important on part of the

management to support the auditor in all these cases. Three types of risk are a part of the overall

auditing process. The first type of risk is inherent risk. Inherent risk in cases where even if the

management establishes control, it is not in its hand. This risk does not occur in the general day-to-day

activities. These risks cannot be eliminated from the system, they can only be reduced. The second type

of risk is the control risk, which occurs when the management has not installed that proper internal

control measures, it occurs because of lack of proper management. The management can be held

responsible for any kind of damage that might occur because of the same. The last major type of risk is

the detection risk which happens when the management, accountant or the auditors fails to identify the

errors and flaws in the accounting books and system. The auditor can be held responsible for the same,

and it occurs due to lack of professional scepticism on his part (Grenier 2017).

The case study of DIPL has many risk factors, the major amongst which are two. First, the company is

changing the routine transactions and methods that are used in the course of accounting. The company

is adopting new methods without any proper research. It is highly possible that it will lead to

misstatement in the books of account of the company. Here, the company has calculated the

depreciation using 20 years useful life of the assets as compared to the industry where the useful life

has been assumed to be 30 years. It is also changing the method of valuation of the inventories (Knechel

& Salterio 2016). All these might lead to over or undervaluation of the accounts and affect the overall

functioning of the company. Thus, it is the duty of the company that proper disclosures are given in the

books of account, the auditor must check the validity of the same and then make an opinion. It will help

in reduction of the overall risk factor that might be involved. The major inherent risk that the company is

suffering with is the installation of the new IT system without proper planning, testing and control. The

company is undertaking the same, without conducting nay reconciliation or research. It might affect the

overall productivity of the company. The books might be over or dune valued because of the same. It is

thus important that before applying such changes, the management of the company must take expert

opinion from outsiders, must judge the overall profitability of the system and then take a decision on

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

the same. The auditor must verify the records properly so that any chances of material misstatement

are reduced and the company is able to show the true view of its financials (DeZoort & Harrison 2016).

Solution 3

Fraud is generally entered into for the profitability puposes by any of the employee or management of

the company in order to make the profist by window dressing the books of acounts. Often there are

certain personal motives involved behind taking such actions. It is important that while conducting

audit, the auditor must apply all kind of procedures so that fraud risk factor can be easily identified and

mitigated by the company. This is the most important work of an auditor and it is very necessary that

the management of the company provide full support to the auditor. In the given case study of DIPL,

there are many fraud risk factor which indicates that there may be material misstatement. Some of

them are identifiable and can be mitigated. The major one of them is non segregation of duties amongst

the management. Single person handles all the major departments, if that person defalcates the

accounts. It will be very difficult for the management to ascertain the same. In this case, we can see that

a single personnel has been given all the responsibilities of invoicing, collection, verify the payment,

manging all the ledger accounts and reconciliation of the accounts at the end of the period. Moreover

the entire cash department which is one of the critical resouces is being handled by a single person in

the organisation is there is no control over it. Thus, what is important that the company properly

segregate the work, so that proper authority and responsibility can be established? The auditor must

see to it that the boos of the company and checked weekly and surprise checks must be undertaken to

judge the sincerity of the employees. If any of the employees is found guilty, he must be restricted form

the work. Proper it security locks and control system moist be there so that any somewhat mis-

happening can be easily avoided (Fay & Negangard 2017).

The second fraud risk factor might be present in the installation of the new It system; the management

of the company installed the same without taking any precautions. The management may themselves be

directly responsible for all this as there might be personal hidden motives behind all this such that no

one is able to track the frauds, if any, amidst all this. It is thus important as an auditor to gets all the

necessary information regarding the new system and reconcile the overall cost and profit. In such a case,

it becomes immensely significant that nothing is undervalued or overvalued. The management must

take expert opinion, pre installation cost and the management must properly segregate post installation

7 | P a g e

the same. The auditor must verify the records properly so that any chances of material misstatement

are reduced and the company is able to show the true view of its financials (DeZoort & Harrison 2016).

Solution 3

Fraud is generally entered into for the profitability puposes by any of the employee or management of

the company in order to make the profist by window dressing the books of acounts. Often there are

certain personal motives involved behind taking such actions. It is important that while conducting

audit, the auditor must apply all kind of procedures so that fraud risk factor can be easily identified and

mitigated by the company. This is the most important work of an auditor and it is very necessary that

the management of the company provide full support to the auditor. In the given case study of DIPL,

there are many fraud risk factor which indicates that there may be material misstatement. Some of

them are identifiable and can be mitigated. The major one of them is non segregation of duties amongst

the management. Single person handles all the major departments, if that person defalcates the

accounts. It will be very difficult for the management to ascertain the same. In this case, we can see that

a single personnel has been given all the responsibilities of invoicing, collection, verify the payment,

manging all the ledger accounts and reconciliation of the accounts at the end of the period. Moreover

the entire cash department which is one of the critical resouces is being handled by a single person in

the organisation is there is no control over it. Thus, what is important that the company properly

segregate the work, so that proper authority and responsibility can be established? The auditor must

see to it that the boos of the company and checked weekly and surprise checks must be undertaken to

judge the sincerity of the employees. If any of the employees is found guilty, he must be restricted form

the work. Proper it security locks and control system moist be there so that any somewhat mis-

happening can be easily avoided (Fay & Negangard 2017).

The second fraud risk factor might be present in the installation of the new It system; the management

of the company installed the same without taking any precautions. The management may themselves be

directly responsible for all this as there might be personal hidden motives behind all this such that no

one is able to track the frauds, if any, amidst all this. It is thus important as an auditor to gets all the

necessary information regarding the new system and reconcile the overall cost and profit. In such a case,

it becomes immensely significant that nothing is undervalued or overvalued. The management must

take expert opinion, pre installation cost and the management must properly segregate post installation

7 | P a g e

8

result. It is not only the responsibility but the control mechanism which must be set and practiced by

both the company as well as the auditors to have a surprise audit and continuous tracking of the major

financials to avoid any fraud by the employees of the company. All this will lead to paving the way for

quality audit and follow up procedures and clean books of accounts. (Bae 2017)

References

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

8 | P a g e

result. It is not only the responsibility but the control mechanism which must be set and practiced by

both the company as well as the auditors to have a surprise audit and continuous tracking of the major

financials to avoid any fraud by the employees of the company. All this will lead to paving the way for

quality audit and follow up procedures and clean books of accounts. (Bae 2017)

References

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

9 | P a g e

9 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.