Cash Audit Procedures Analysis: Alpine Cupcakes Inc. Report

VerifiedAdded on 2022/08/20

|8

|1202

|12

Report

AI Summary

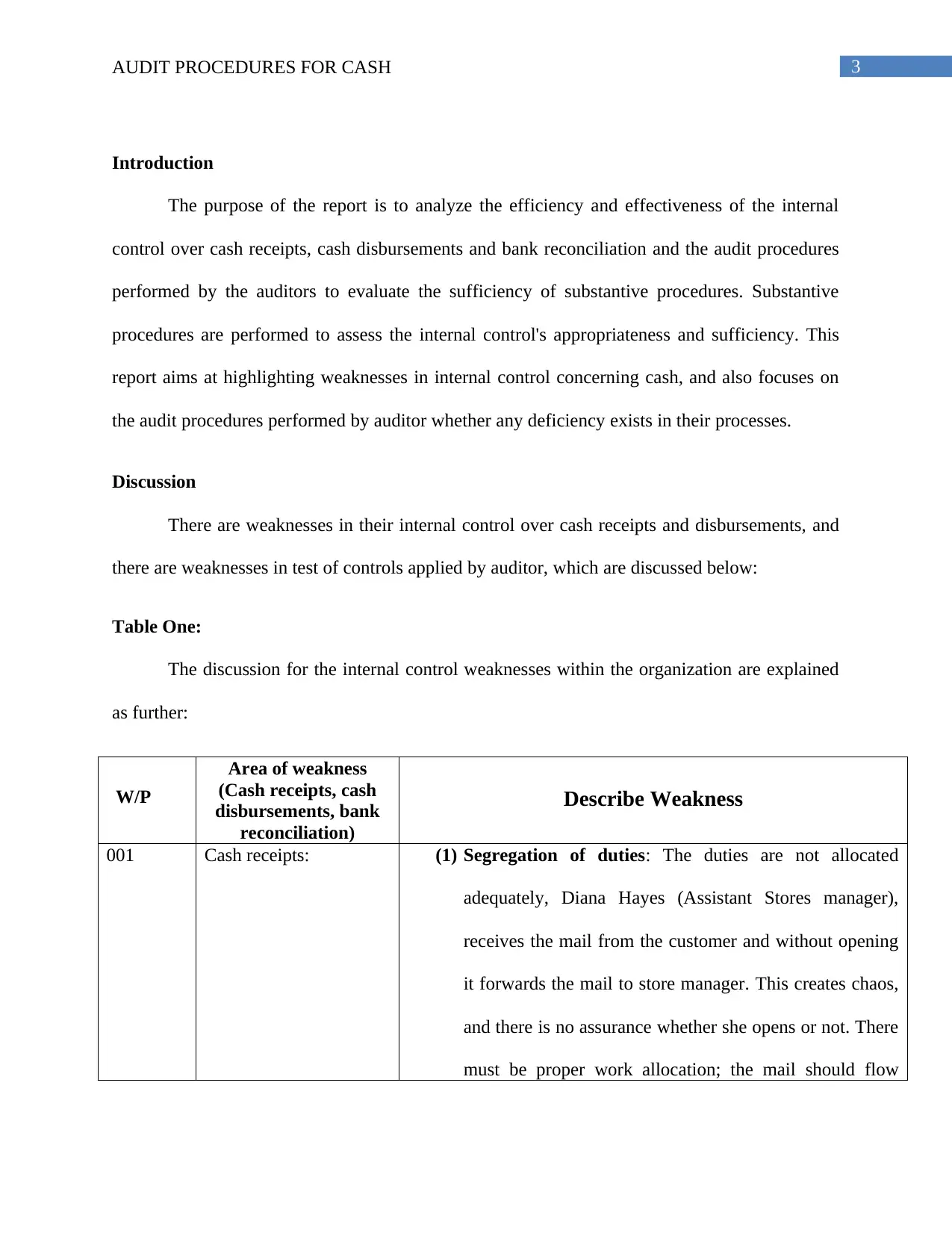

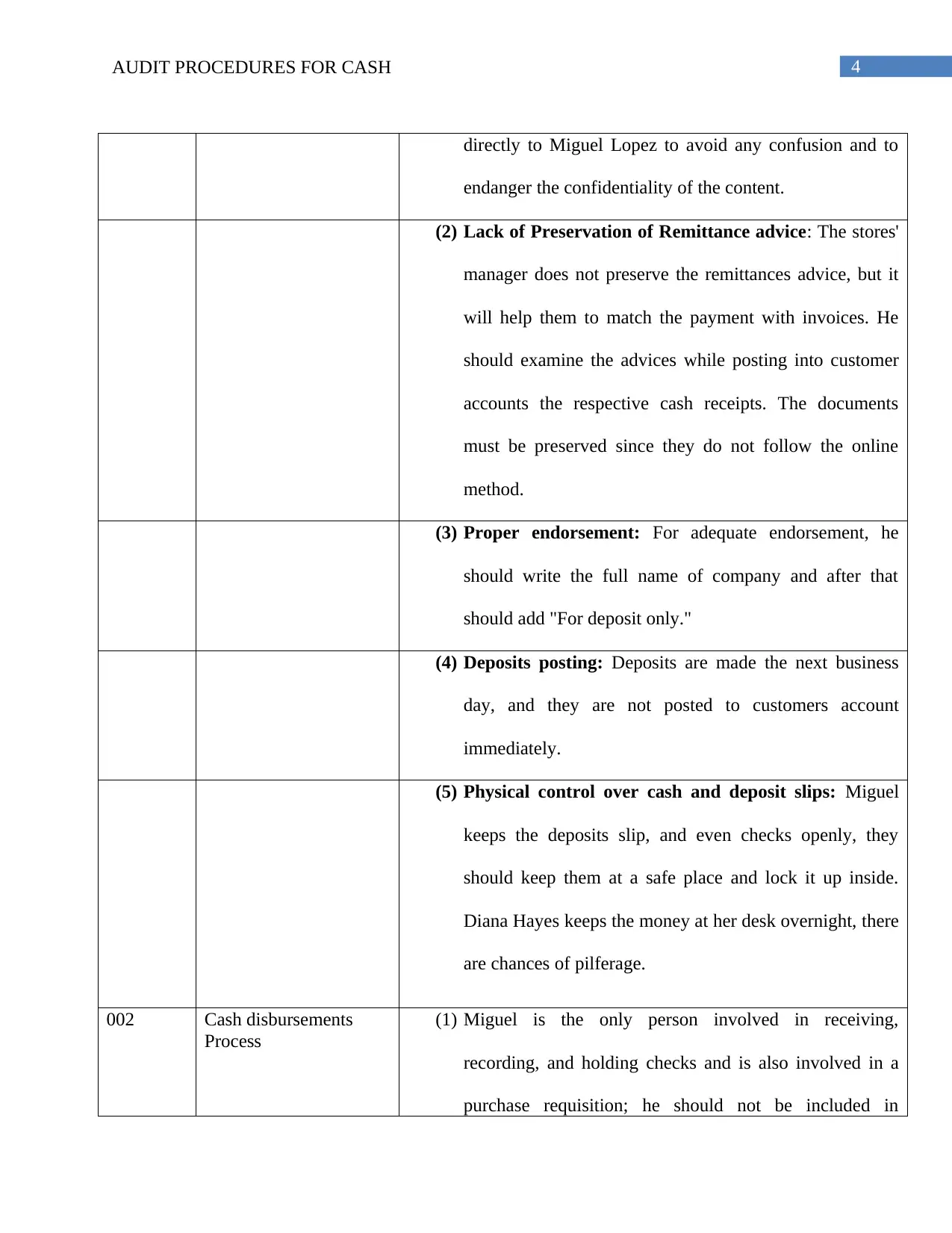

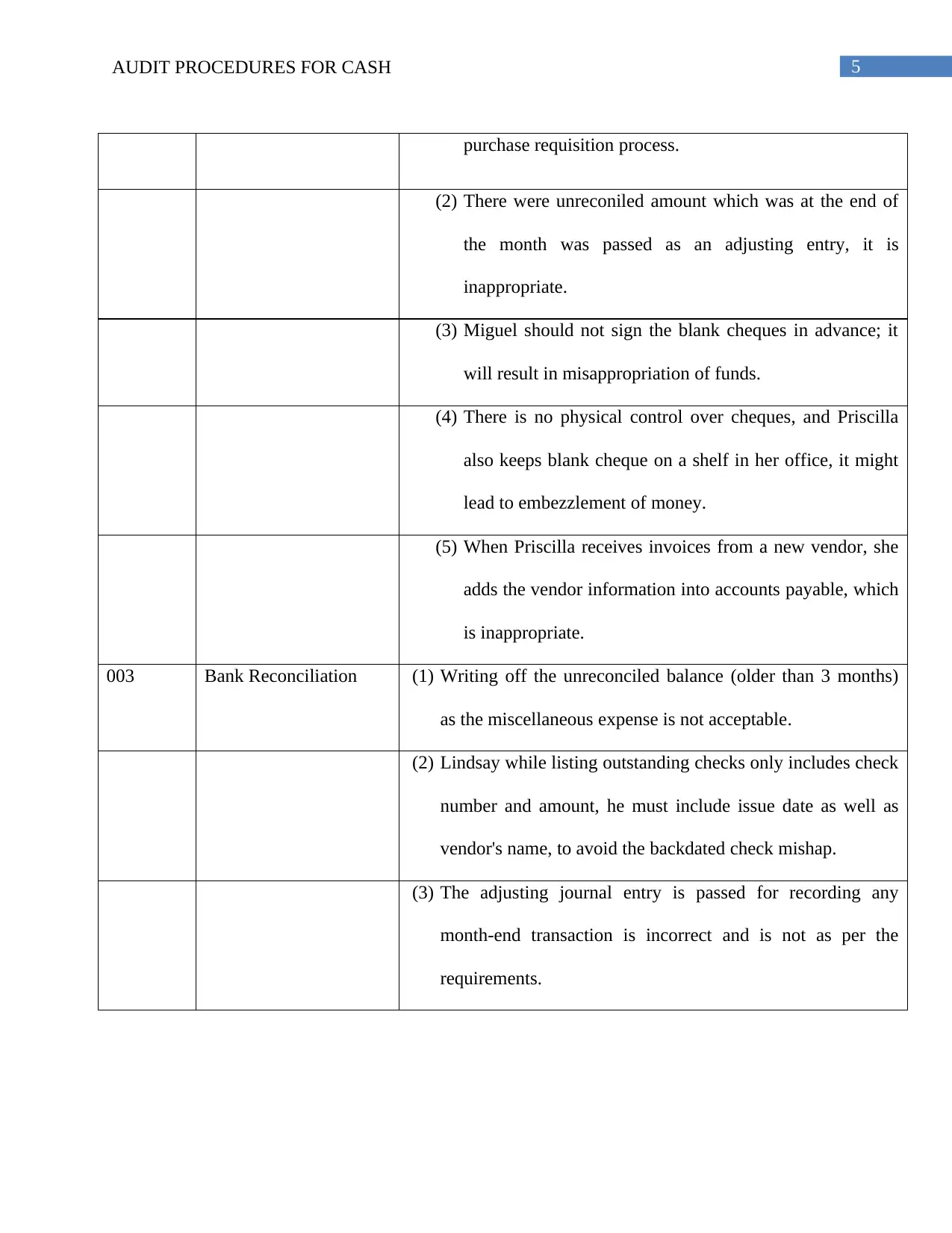

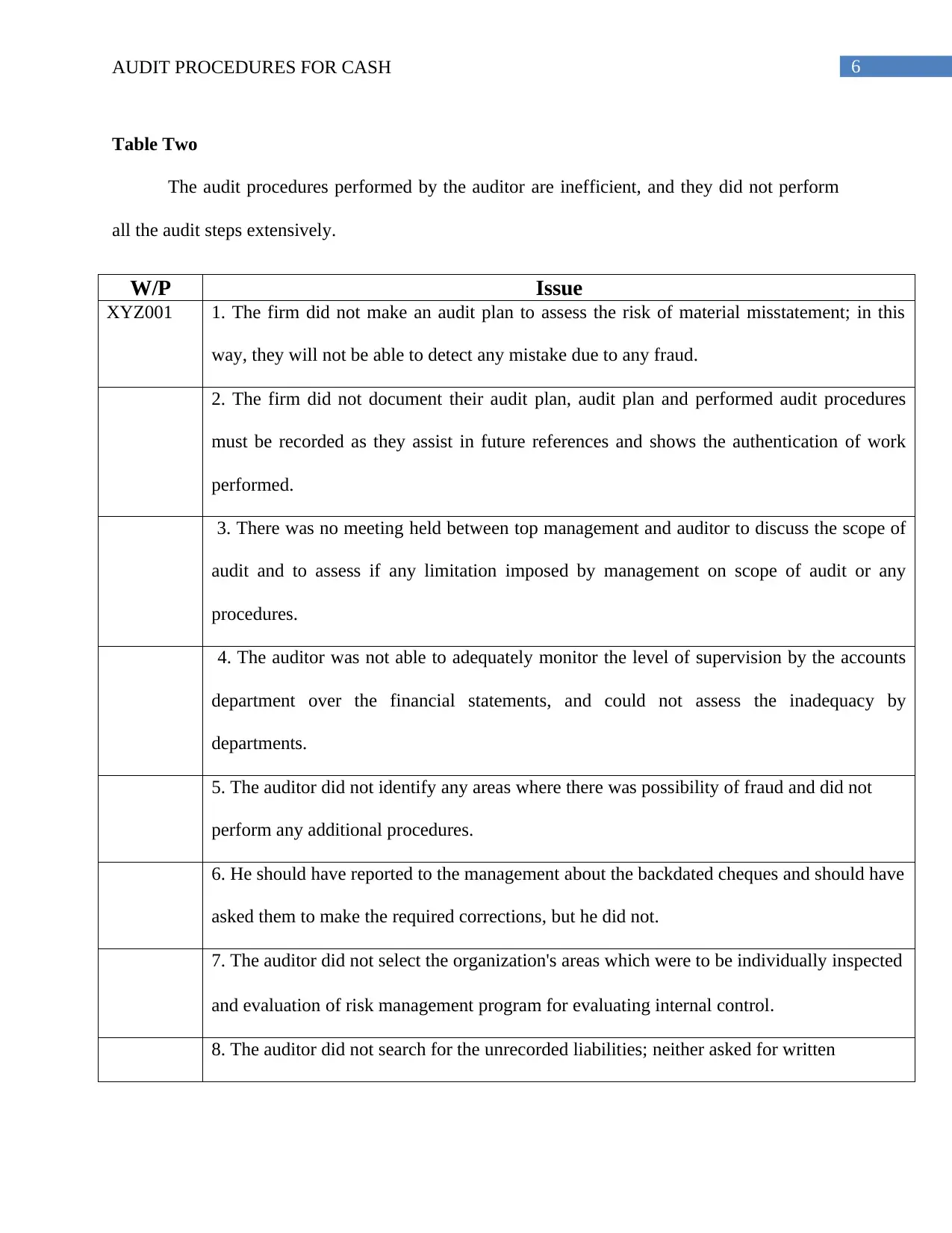

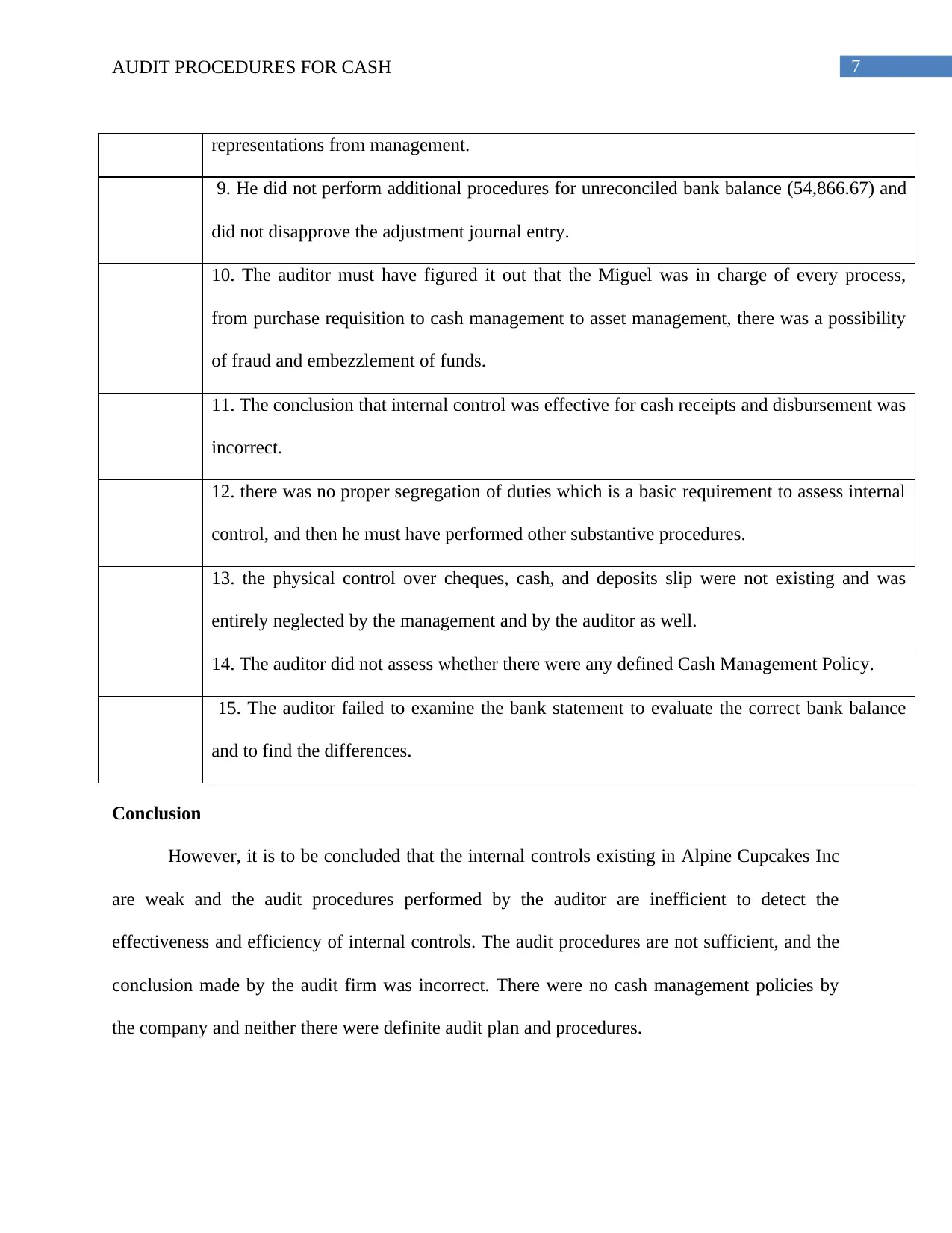

This report critically examines the internal control weaknesses within Alpine Cupcakes Inc. concerning cash receipts, disbursements, and bank reconciliation processes, as well as the audit procedures performed by the auditor. The analysis highlights specific deficiencies, such as inadequate segregation of duties, lack of preservation of remittance advice, and insufficient physical control over cash and checks. The report further evaluates the auditor's work, identifying inefficiencies in the audit procedures, including the absence of a comprehensive audit plan, inadequate documentation, and failure to detect potential fraud risks. The conclusion underscores the weakness of existing internal controls and the insufficiency of the audit procedures, emphasizing the need for improved cash management policies and more thorough audit practices to ensure financial accuracy and prevent potential misappropriation of funds. The report leverages tables to present the weaknesses in internal control and the deficiencies in the audit procedures performed by the auditor.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.