Audit Assurance and Compliance Assignment: DIPL Case Study Analysis

VerifiedAdded on 2020/03/04

|10

|2715

|41

Homework Assignment

AI Summary

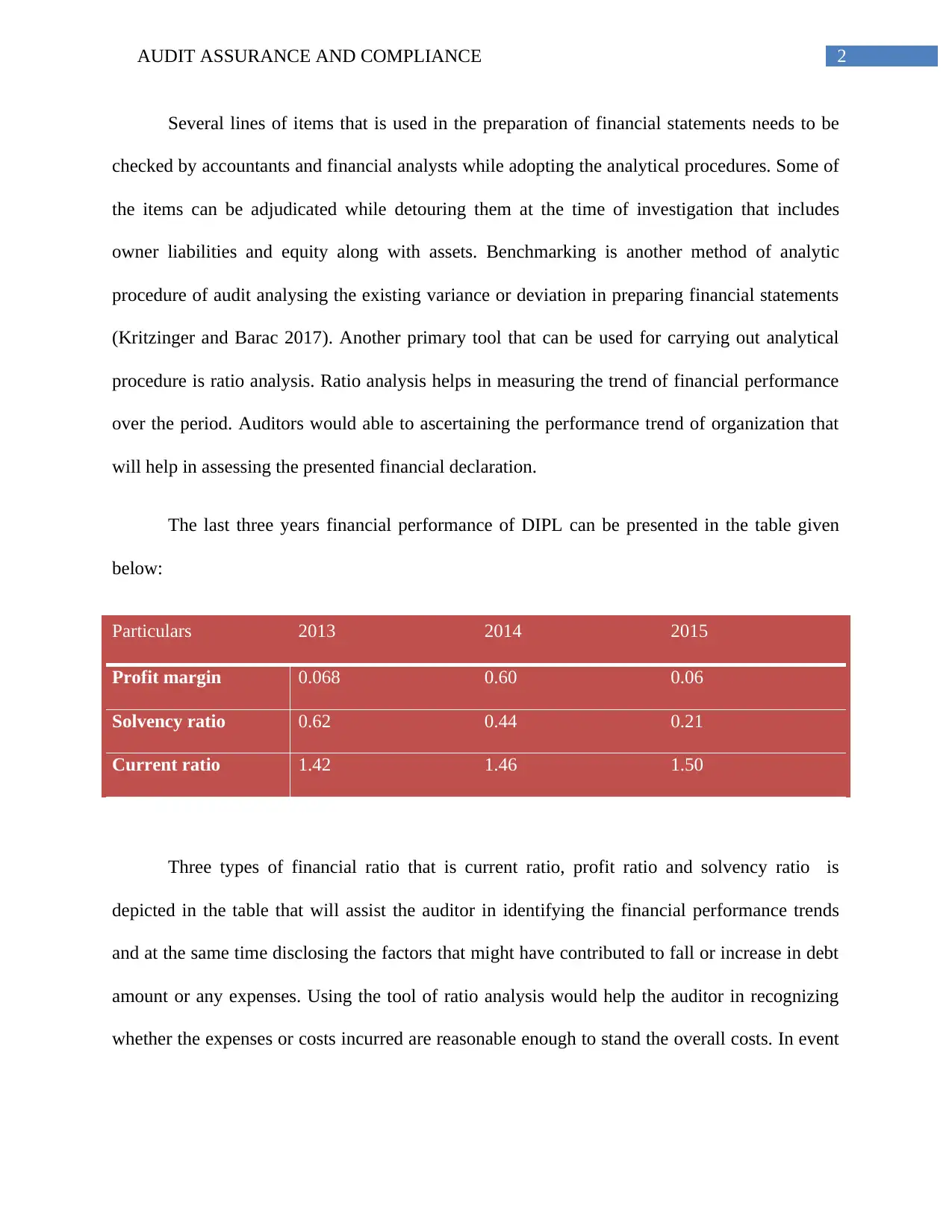

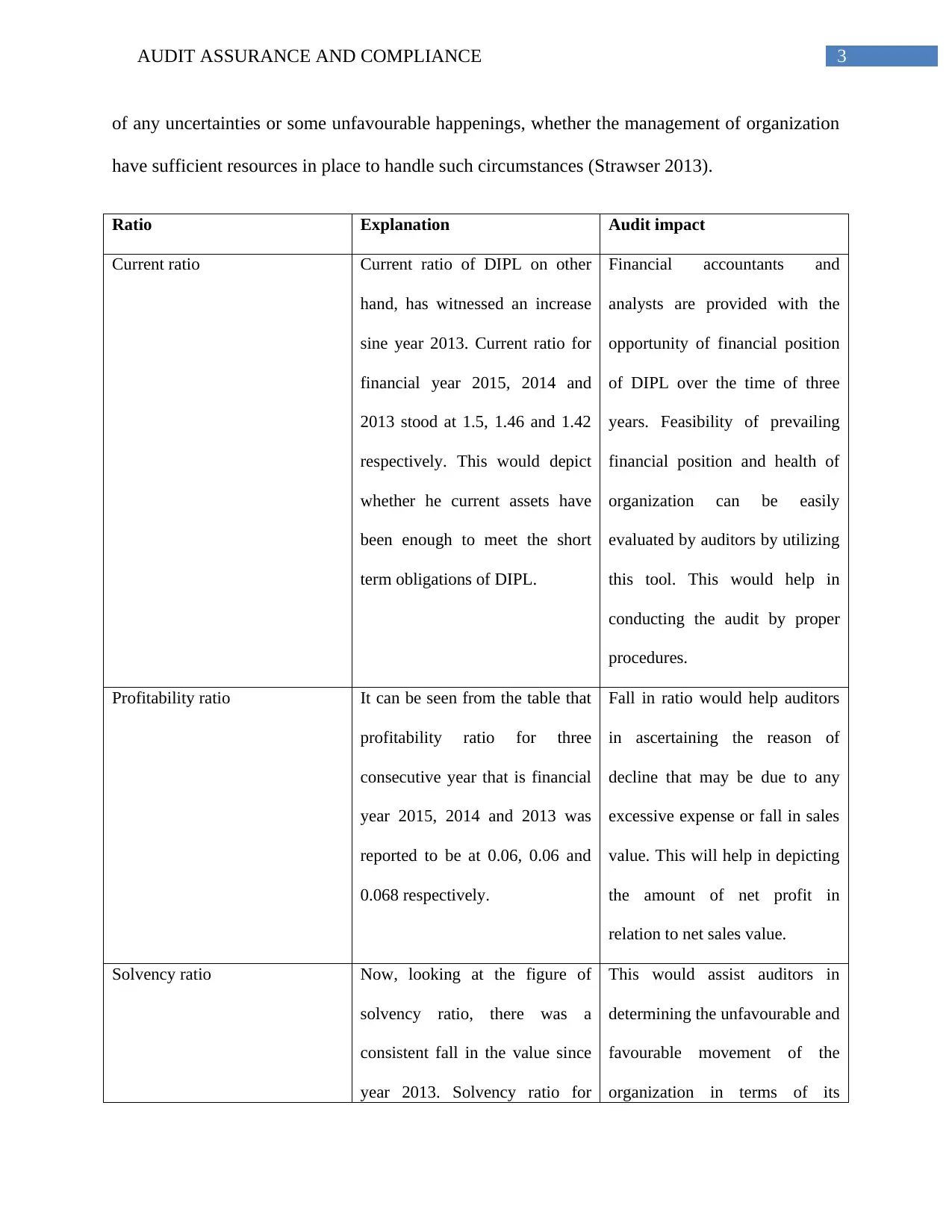

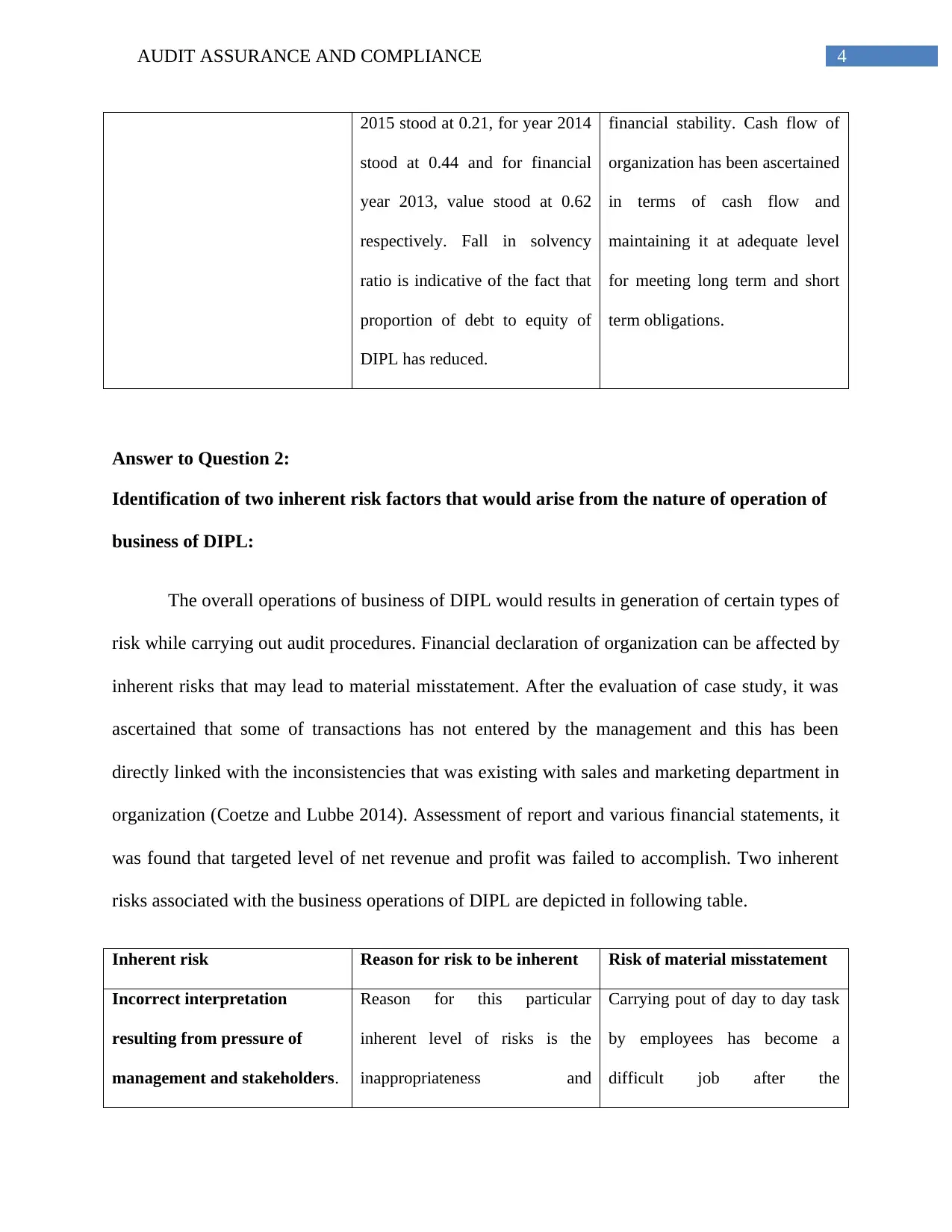

This assignment is a comprehensive analysis of the audit, assurance, and compliance aspects related to Double Ink Printers Ltd (DIPL). The student begins by explaining the role of analytical procedures in audit planning, emphasizing their importance in providing reasonable assurance that financial statements are free from material errors and conform to reporting standards. Common size statements, benchmarking, and ratio analysis are discussed as key tools. The assignment presents a detailed ratio analysis of DIPL's financial performance from 2013 to 2015, including current, profitability, and solvency ratios, and their audit implications. The second part of the assignment identifies two inherent risk factors arising from DIPL's business operations, such as incorrect interpretations due to management pressure and the nature of the business entity, and explains how these risks could lead to material misstatements. The third section focuses on fraud risks associated with material misstatements in financial reporting, specifically addressing worker involvement in fraudulent activities and the pressure on the organization to meet certain financial targets. The assignment concludes by highlighting how these risks impact the conduct of an audit and the potential for misstated financial declarations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.