HI6026: Audit Compliance and Enhanced Reporting in Australia, 2018

VerifiedAdded on 2023/06/04

|16

|3897

|457

Report

AI Summary

This report analyzes audit and compliance standards in Wesfarmers, evaluating their annual report and Ernst & Young's audit. It examines auditor independence, non-audit services, auditor remuneration, and major audit matters like non-current asset impairment and discontinued operations. The report also discusses the roles of the audit commission, audit opinions, and the differences between management and auditor responsibilities. The analysis includes events attaining material value and material information evaluated by auditors. The report concludes by highlighting the importance of enhanced auditor reporting in ensuring the quality and transparency of financial statements, and that Desklib offers similar solved assignments for students.

Running head: AUDIT COMPLIANCE IN COMPANIES

Audit Compliance in Companies

Name of the University:

Name of the Student:

Authors Note:

Audit Compliance in Companies

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT COMPLIANCE IN COMPANIES

Executive Summary

In the recent years, the audit committees have considered implementing several effective

approaches in order to enhance their quality of the audit report. The paper will focus on

analyzing the audit and compliance standards followed in Wesfarmers through evaluating

the annual report of the company. Conversely, Ernst & Young have not considered the event

attaining material value as it is anticipated not to attain any material effect on the

company’s financial statements. It has also been gathered that in alignment with the yearly

statements of Wesfarmers Limited in the year 2018 it is also important that the auditors

Ernst and Young did not fail to encompass certain material factors or information attaining

material collationregarding the company’s financial reporting.

Executive Summary

In the recent years, the audit committees have considered implementing several effective

approaches in order to enhance their quality of the audit report. The paper will focus on

analyzing the audit and compliance standards followed in Wesfarmers through evaluating

the annual report of the company. Conversely, Ernst & Young have not considered the event

attaining material value as it is anticipated not to attain any material effect on the

company’s financial statements. It has also been gathered that in alignment with the yearly

statements of Wesfarmers Limited in the year 2018 it is also important that the auditors

Ernst and Young did not fail to encompass certain material factors or information attaining

material collationregarding the company’s financial reporting.

2AUDIT COMPLIANCE IN COMPANIES

Table of Contents

1. Introduction............................................................................................................................3

2. Auditors Independence Requirement Adherence.................................................................3

3. Non-Audit Services.................................................................................................................4

4. Renumeration of Auditors......................................................................................................4

5. Major Audit Factors................................................................................................................5

6. Audit Commission..................................................................................................................8

7. Audit Opinion.........................................................................................................................8

8. Management and Auditor Responsibilities Difference..........................................................9

9. Material Based Events..........................................................................................................10

10. Analysis of Material Information by Auditors....................................................................10

11. Lack of Material Information.............................................................................................11

12. Questions for Follow-Up....................................................................................................11

13. Conclusion..........................................................................................................................12

References................................................................................................................................13

Table of Contents

1. Introduction............................................................................................................................3

2. Auditors Independence Requirement Adherence.................................................................3

3. Non-Audit Services.................................................................................................................4

4. Renumeration of Auditors......................................................................................................4

5. Major Audit Factors................................................................................................................5

6. Audit Commission..................................................................................................................8

7. Audit Opinion.........................................................................................................................8

8. Management and Auditor Responsibilities Difference..........................................................9

9. Material Based Events..........................................................................................................10

10. Analysis of Material Information by Auditors....................................................................10

11. Lack of Material Information.............................................................................................11

12. Questions for Follow-Up....................................................................................................11

13. Conclusion..........................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT COMPLIANCE IN COMPANIES

1. Introduction

Auditing can be explained as the process of evaluating along with investigating the

financial reports published by the companies for evaluating that such reports are devoid of

any material misstatements, frauds, errors and certain aspects. For this reason, the auditors

need to enhance the quality of its audit report by means of revealing material-based

information related with the company’s annual report(Chand, Patel & White, 2015). In

addition, the companies alsorequire to offer such information to all its stakeholders in a

format that will be simple for them to understand. In the recent years, the audit committees

have considered implementing several effective approaches in order to enhance their

quality of the audit report. Therefore, this is deemed important for the auditors to

considerincreased issues within the company’s financial statements which can facilitate

them in ensuring better quality of audit(Bond, Govendir& Wells, 2016). In accordance with

that, it is important to justify that the selected company “Wesfarmer Limited’s” audit

partner is Ernst and Young.

2. Auditors Independence Requirement Adherence

At the time of offering better audit services, all the auditing companies requires to

make sure that the important guidelines along with norms associated with auditor’s

independence. In other words, it must also be indicated that the auditors requirebeing

associated with the audit partner in which they offer certain better audit-based

operations(Perera& Chand, 2015). The directors associated with the company have

alsoindicated that Ernst and Young has abided by every important professional guidelines

and principles associated with auditing standards(Leung &Verriest, 2015). “Accounting

Professional and Ethical Standards Board’s APES 110 Code of Ethics for Professional

1. Introduction

Auditing can be explained as the process of evaluating along with investigating the

financial reports published by the companies for evaluating that such reports are devoid of

any material misstatements, frauds, errors and certain aspects. For this reason, the auditors

need to enhance the quality of its audit report by means of revealing material-based

information related with the company’s annual report(Chand, Patel & White, 2015). In

addition, the companies alsorequire to offer such information to all its stakeholders in a

format that will be simple for them to understand. In the recent years, the audit committees

have considered implementing several effective approaches in order to enhance their

quality of the audit report. Therefore, this is deemed important for the auditors to

considerincreased issues within the company’s financial statements which can facilitate

them in ensuring better quality of audit(Bond, Govendir& Wells, 2016). In accordance with

that, it is important to justify that the selected company “Wesfarmer Limited’s” audit

partner is Ernst and Young.

2. Auditors Independence Requirement Adherence

At the time of offering better audit services, all the auditing companies requires to

make sure that the important guidelines along with norms associated with auditor’s

independence. In other words, it must also be indicated that the auditors requirebeing

associated with the audit partner in which they offer certain better audit-based

operations(Perera& Chand, 2015). The directors associated with the company have

alsoindicated that Ernst and Young has abided by every important professional guidelines

and principles associated with auditing standards(Leung &Verriest, 2015). “Accounting

Professional and Ethical Standards Board’s APES 110 Code of Ethics for Professional

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT COMPLIANCE IN COMPANIES

Accountants’’ and “Corporations Act 2001” are followed by the company in maintaining

effective reporting. These standards are implemented so that the auditor’s independence

can be sustained in a better manner.

3. Non-Audit Services

For Wesfarmers Company, its audit partner provided certain non-audit services that

encompass tax complianceservice along with certain other services. In tax-based services,

the Ernst and Young was paid $683,000 and $343,000 was offered to the audit firm for its

non-audit services. Conversely, Wesfarmers have also entertained that the needed

compliance for Ernst and Young with all the important standardsfor attaining certain non-

audit services. Rather than that, Wesfarmers have offered the auditor with certain type of

work which encompass the work review of auditor itself for undertaking certain

management decisions(Chapple, 2017). In addition, certain corporategovernance guidelines

as well as norms followed by means of offering certain non-audit services. Moreover, all the

factors indicate the auditor independence.

4. Renumeration of Auditors

The table indicated below facilitates in analyzing the audit service payments taking

into consideration the Australian along with cross-border network companies. Non-audit

services like tax compliance and some additional services are provided by Ernst and Young

to Wesfarmers. As gathered from the table above, it is observed that Wesfarmers has

decreased its audit service payment to its audit partner by 5.50% for the year 2018 in

comparison to the previous year(Howieson, 2017).

Accountants’’ and “Corporations Act 2001” are followed by the company in maintaining

effective reporting. These standards are implemented so that the auditor’s independence

can be sustained in a better manner.

3. Non-Audit Services

For Wesfarmers Company, its audit partner provided certain non-audit services that

encompass tax complianceservice along with certain other services. In tax-based services,

the Ernst and Young was paid $683,000 and $343,000 was offered to the audit firm for its

non-audit services. Conversely, Wesfarmers have also entertained that the needed

compliance for Ernst and Young with all the important standardsfor attaining certain non-

audit services. Rather than that, Wesfarmers have offered the auditor with certain type of

work which encompass the work review of auditor itself for undertaking certain

management decisions(Chapple, 2017). In addition, certain corporategovernance guidelines

as well as norms followed by means of offering certain non-audit services. Moreover, all the

factors indicate the auditor independence.

4. Renumeration of Auditors

The table indicated below facilitates in analyzing the audit service payments taking

into consideration the Australian along with cross-border network companies. Non-audit

services like tax compliance and some additional services are provided by Ernst and Young

to Wesfarmers. As gathered from the table above, it is observed that Wesfarmers has

decreased its audit service payment to its audit partner by 5.50% for the year 2018 in

comparison to the previous year(Howieson, 2017).

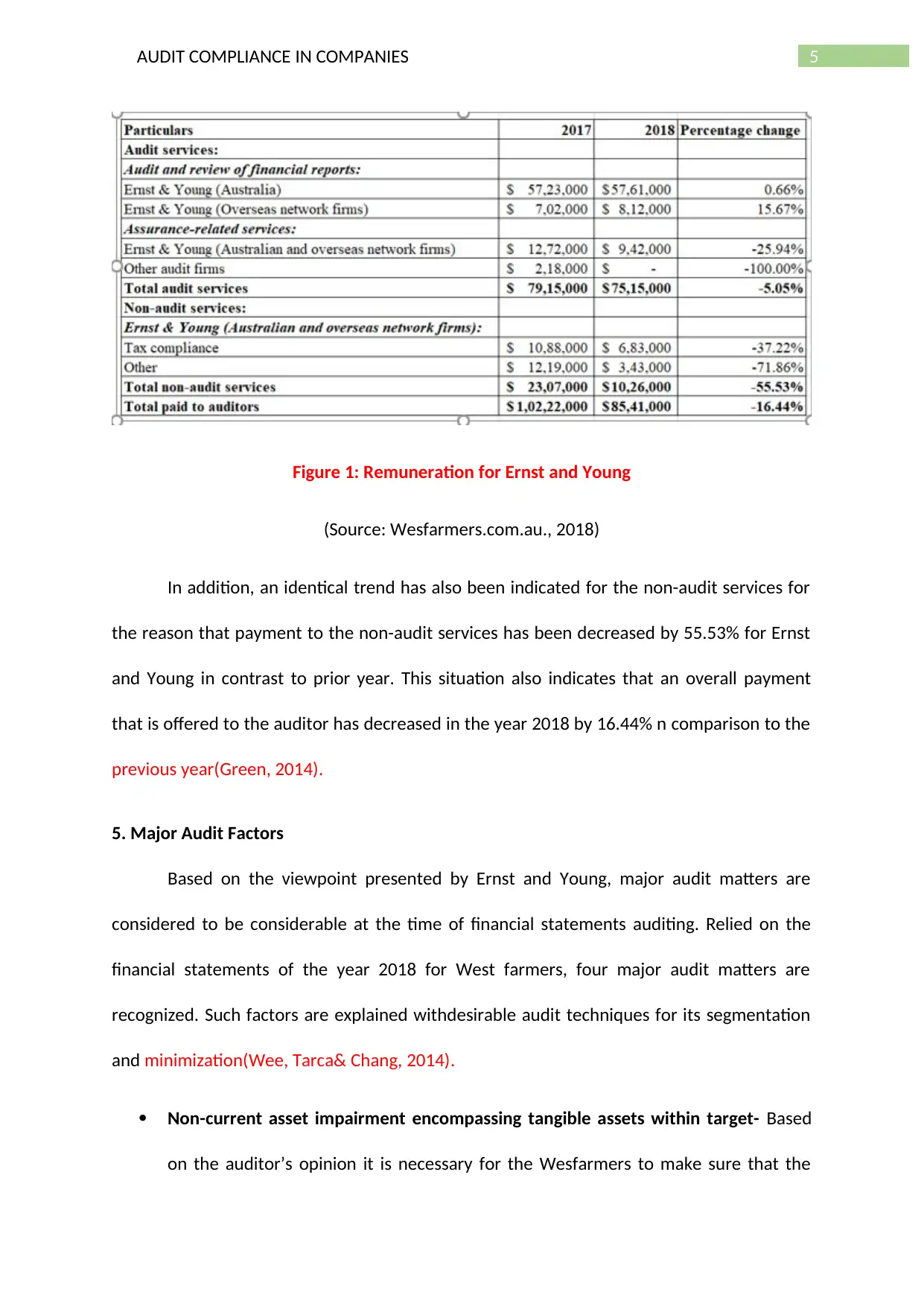

5AUDIT COMPLIANCE IN COMPANIES

Figure 1: Remuneration for Ernst and Young

(Source: Wesfarmers.com.au., 2018)

In addition, an identical trend has also been indicated for the non-audit services for

the reason that payment to the non-audit services has been decreased by 55.53% for Ernst

and Young in contrast to prior year. This situation also indicates that an overall payment

that is offered to the auditor has decreased in the year 2018 by 16.44% n comparison to the

previous year(Green, 2014).

5. Major Audit Factors

Based on the viewpoint presented by Ernst and Young, major audit matters are

considered to be considerable at the time of financial statements auditing. Relied on the

financial statements of the year 2018 for West farmers, four major audit matters are

recognized. Such factors are explained withdesirable audit techniques for its segmentation

and minimization(Wee, Tarca& Chang, 2014).

Non-current asset impairment encompassing tangible assets within target- Based

on the auditor’s opinion it is necessary for the Wesfarmers to make sure that the

Figure 1: Remuneration for Ernst and Young

(Source: Wesfarmers.com.au., 2018)

In addition, an identical trend has also been indicated for the non-audit services for

the reason that payment to the non-audit services has been decreased by 55.53% for Ernst

and Young in contrast to prior year. This situation also indicates that an overall payment

that is offered to the auditor has decreased in the year 2018 by 16.44% n comparison to the

previous year(Green, 2014).

5. Major Audit Factors

Based on the viewpoint presented by Ernst and Young, major audit matters are

considered to be considerable at the time of financial statements auditing. Relied on the

financial statements of the year 2018 for West farmers, four major audit matters are

recognized. Such factors are explained withdesirable audit techniques for its segmentation

and minimization(Wee, Tarca& Chang, 2014).

Non-current asset impairment encompassing tangible assets within target- Based

on the auditor’s opinion it is necessary for the Wesfarmers to make sure that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT COMPLIANCE IN COMPANIES

recoverable amount based on the plant, property and equipment in consideration to

a considerable judgement. For this reason, it might lead to impairment within the

Target’s cash generatingunits (Zeff, Radcliffe &Gunz, 2014). Additionally, the

relevance of the company’s financial statements in accordance of the impairment

test, anticipations along with sensitivities those are employed by the audit Partner

“Ernst and Young”. This technique can also be categorized in the form of analytical

techniques.

Suppliers Rebate- Supplier rebates are taken into consideration through acting as a

major audit matter because of the supplier rebate quantum realized at this period

along with the judgement is required being implemented through considering major

factors. Effective audit techniques are implemented by the audit patner of

Wesfarmers that which includes analysis of supplier rebates, internal control analysis

of the company and analysis of rebate contracts with conducting comparisons from

budget of previous year (Mita, Utama &Wulandari, 2018). Conversely, the audit

processesencompass sample testing related with supplier rebates, analyzing the

suppliers those have promotion-based credit, analyzing sample focused on materials

of new contracts, legal counsel enquiry along with the related business

representatives. For this reason, it turns out to be likely to segment like processes

like control tests, substantive detail evaluation and substantive balance along with

tests related with analyticalprocesses.

Discontinued operation in the region of Curragh- In the recent year, Wesfarmers

Company has made increased attempts in getting rid of its coal mine within this

region that is worth$700 million (Van Akkeren&Tarr, 2014). The agreement includes

a process of analyzing sharing value associated with metallurgical coal cost in the

recoverable amount based on the plant, property and equipment in consideration to

a considerable judgement. For this reason, it might lead to impairment within the

Target’s cash generatingunits (Zeff, Radcliffe &Gunz, 2014). Additionally, the

relevance of the company’s financial statements in accordance of the impairment

test, anticipations along with sensitivities those are employed by the audit Partner

“Ernst and Young”. This technique can also be categorized in the form of analytical

techniques.

Suppliers Rebate- Supplier rebates are taken into consideration through acting as a

major audit matter because of the supplier rebate quantum realized at this period

along with the judgement is required being implemented through considering major

factors. Effective audit techniques are implemented by the audit patner of

Wesfarmers that which includes analysis of supplier rebates, internal control analysis

of the company and analysis of rebate contracts with conducting comparisons from

budget of previous year (Mita, Utama &Wulandari, 2018). Conversely, the audit

processesencompass sample testing related with supplier rebates, analyzing the

suppliers those have promotion-based credit, analyzing sample focused on materials

of new contracts, legal counsel enquiry along with the related business

representatives. For this reason, it turns out to be likely to segment like processes

like control tests, substantive detail evaluation and substantive balance along with

tests related with analyticalprocesses.

Discontinued operation in the region of Curragh- In the recent year, Wesfarmers

Company has made increased attempts in getting rid of its coal mine within this

region that is worth$700 million (Van Akkeren&Tarr, 2014). The agreement includes

a process of analyzing sharing value associated with metallurgical coal cost in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT COMPLIANCE IN COMPANIES

future years. This is also recognized that the company has attained an increased

profit after tax of around $250 million from its discontinued operations within the

coal mine. This considers certain trading outcomes within the efficient disposal point

along with disposal gain. Moreover, this is the cause for which the audit of the

company has considered it as an important matter. In dealing with such matter,

Ernst and Young has realized the sale along with purchase agreements as well as

related documents in analyzing the calculation of disposal gain post-tax

(Wesfarmers.com.au., 2018). In addition, this has also evaluated certain considerable

inputs related with post-tax sales gain computation based on which this is

ascertained that there are non-recognized liability and asset values (Bugeja,

Czernkowski& Moran, 2015). The final step encompass association with the tax

specialists in taking into consideration the tax impacts of divestment and at last,

certain disclosures related with the company’s financial statements are considered.

Burnings UK and Ireland (BUKI) discontinued operations- n the first half period of

the current year i.e. 2018, Buki has recognized an amount of $953 million as the

impairment charges while on 25th May’18, Wesfarmers has sold the business at a

very nominal price. In the financial statement of 2018, the company has recorded a

loss of $1.66 billion from such operations that has been discontinued which also

includes the impairment charges which has been realized in the initial half-year of

2018(Junior, Best & Cotter, 2014). Moreover, it also includes the trading result of

actual disposal point and the loss associated with the same. It is the very reason

which prompted Ernst & Young to consider it as the most crucial matter in FY2018.

In order to deal with this particular matter Ernst & Young has considered the

precision of the impairment cost along with the assumption as well as methodology

future years. This is also recognized that the company has attained an increased

profit after tax of around $250 million from its discontinued operations within the

coal mine. This considers certain trading outcomes within the efficient disposal point

along with disposal gain. Moreover, this is the cause for which the audit of the

company has considered it as an important matter. In dealing with such matter,

Ernst and Young has realized the sale along with purchase agreements as well as

related documents in analyzing the calculation of disposal gain post-tax

(Wesfarmers.com.au., 2018). In addition, this has also evaluated certain considerable

inputs related with post-tax sales gain computation based on which this is

ascertained that there are non-recognized liability and asset values (Bugeja,

Czernkowski& Moran, 2015). The final step encompass association with the tax

specialists in taking into consideration the tax impacts of divestment and at last,

certain disclosures related with the company’s financial statements are considered.

Burnings UK and Ireland (BUKI) discontinued operations- n the first half period of

the current year i.e. 2018, Buki has recognized an amount of $953 million as the

impairment charges while on 25th May’18, Wesfarmers has sold the business at a

very nominal price. In the financial statement of 2018, the company has recorded a

loss of $1.66 billion from such operations that has been discontinued which also

includes the impairment charges which has been realized in the initial half-year of

2018(Junior, Best & Cotter, 2014). Moreover, it also includes the trading result of

actual disposal point and the loss associated with the same. It is the very reason

which prompted Ernst & Young to consider it as the most crucial matter in FY2018.

In order to deal with this particular matter Ernst & Young has considered the

precision of the impairment cost along with the assumption as well as methodology

8AUDIT COMPLIANCE IN COMPANIES

analysis. In addition, growth rate including the terminal ones, inflation as well as

discount rate is reported within the annual report of Wesfarmers having commodity

prices anticipation.The auditor has also taken notice of the agreement associated

with the purchase and sale in order to evaluate the disposal gains after payment of

the taxes. Furthermore, it also assessed the inputs of the post-tax loss after the sale

and post the same, the derecognized assets and liability values are also ascertained.

In the next step, a tax specialist is brought into picture to consider the effect of the

tax after sale and then the disclosure of financial statement is considered.

6. Audit Commission

The annual report analysis of the company signified the company’s management has

maintained an audit and risk committee within Wesfarmers. The responsibilities fulfilled by

them includes maintaining efficiency of internal control in, analyzing usefulness of assets

through maintaining integrity of annual report information (Susela Devi& Helen Samujh,

2015). The committee of the organization is observed to include few important executive

directors including J.A. Westacott and D.L. Smith Gander. The committee also has a

responsibility of including efficiency of financial reporting, analysis and review of

commercial incomes that is necessary in “audit risk management”.

7. Audit Opinion

The auditor independence information offered by Wesfarmers indicated that the

organization prepared its remuneration section in adherence to “Section 300A of the

Corporations Act 2001”guidelines. In addition, based on the viewpoint of Ernst and Young,

the financial statements are prepared and represented in a way that every Australian

accounting standards-based reporting along with different norms are suitably followed by

analysis. In addition, growth rate including the terminal ones, inflation as well as

discount rate is reported within the annual report of Wesfarmers having commodity

prices anticipation.The auditor has also taken notice of the agreement associated

with the purchase and sale in order to evaluate the disposal gains after payment of

the taxes. Furthermore, it also assessed the inputs of the post-tax loss after the sale

and post the same, the derecognized assets and liability values are also ascertained.

In the next step, a tax specialist is brought into picture to consider the effect of the

tax after sale and then the disclosure of financial statement is considered.

6. Audit Commission

The annual report analysis of the company signified the company’s management has

maintained an audit and risk committee within Wesfarmers. The responsibilities fulfilled by

them includes maintaining efficiency of internal control in, analyzing usefulness of assets

through maintaining integrity of annual report information (Susela Devi& Helen Samujh,

2015). The committee of the organization is observed to include few important executive

directors including J.A. Westacott and D.L. Smith Gander. The committee also has a

responsibility of including efficiency of financial reporting, analysis and review of

commercial incomes that is necessary in “audit risk management”.

7. Audit Opinion

The auditor independence information offered by Wesfarmers indicated that the

organization prepared its remuneration section in adherence to “Section 300A of the

Corporations Act 2001”guidelines. In addition, based on the viewpoint of Ernst and Young,

the financial statements are prepared and represented in a way that every Australian

accounting standards-based reporting along with different norms are suitably followed by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT COMPLIANCE IN COMPANIES

the Wesfarmers. For this reason, in such scenario, Ernst and Young issued an unqualified

audit viewpoint.

8. Management and Auditor Responsibilities Difference

Based on the recent yearly report of Wesfarmers, the responsibilities fulfilled by the

directors and management are different from that of the part of the auditor. This is

observed to be apparent at the time of developing and indicating effectiveness of the

financial statements. The directors along with the company’s management are needed to

entertain that the financial statements are developed for offering suitable overview

regarding the “2001 Corporations Act” along with the accounting standards existing within

Australia. In addition, the directors have the responsibility to analyses the ability of the

company to carry out functioning in increasing concern basis at the time of developing the

financial statements(Liu, 2015). On the other hand, the auditors attain some responsibilities

which is not aligned with the responsibilities of management and directors.

The auditors are associated in evaluating and analyzing the financial reports reported

by the companies for analyzing that such factors are devoid of the financial frauds, errors,

material statements along with others. Certain important responsibilities of the auditors

encompass recognizing along with analyzing the uncertainties related with material

misstatements andattaining suitable knowledge considering internal control (Santos, Ponte

&Mapurunga, 2014). This also facilitates in analyzing the analysis of accounting policies

along with indicating the suitability related with increasing concern base regarding

accounting employed by the directors. Conversely, the auditors are responsible for

evaluating the development along with financial statements presentation as well as

attaining enough examples focused on audit.

the Wesfarmers. For this reason, in such scenario, Ernst and Young issued an unqualified

audit viewpoint.

8. Management and Auditor Responsibilities Difference

Based on the recent yearly report of Wesfarmers, the responsibilities fulfilled by the

directors and management are different from that of the part of the auditor. This is

observed to be apparent at the time of developing and indicating effectiveness of the

financial statements. The directors along with the company’s management are needed to

entertain that the financial statements are developed for offering suitable overview

regarding the “2001 Corporations Act” along with the accounting standards existing within

Australia. In addition, the directors have the responsibility to analyses the ability of the

company to carry out functioning in increasing concern basis at the time of developing the

financial statements(Liu, 2015). On the other hand, the auditors attain some responsibilities

which is not aligned with the responsibilities of management and directors.

The auditors are associated in evaluating and analyzing the financial reports reported

by the companies for analyzing that such factors are devoid of the financial frauds, errors,

material statements along with others. Certain important responsibilities of the auditors

encompass recognizing along with analyzing the uncertainties related with material

misstatements andattaining suitable knowledge considering internal control (Santos, Ponte

&Mapurunga, 2014). This also facilitates in analyzing the analysis of accounting policies

along with indicating the suitability related with increasing concern base regarding

accounting employed by the directors. Conversely, the auditors are responsible for

evaluating the development along with financial statements presentation as well as

attaining enough examples focused on audit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT COMPLIANCE IN COMPANIES

9. Material Based Events

It is deemed important to indicate that two considerable events for Wesfarmers that

took place for the recent year. In such case Coles demerger is also carried out in the current

year in March (Bodle, Cybinski&Monem,2016). Conversely, Ernst & Young have not

considered the event attaining material value as it is anticipated not to attain any material

effect on the company’s financial statements. The Wes farmer Company’s board of directors

has announced totally aligned ordinary dividend of around 120 cents each share because of

which the overall amount of the yearly dividend to be offed to the stakeholders might be

223 cents for each share in the year 2018 and the dividend is yet is to be offered to the

shareholders (Ipino&Parbonetti, 2017).

10. Analysis of Material Information by Auditors

Relied on the perception of the third-party stakeholder, it is deemed important that

Ernst and Young has been increasingly effective in evaluating the material information of

Wesfarmers Limited relied on the financial statements. This is caused based on the auditing

ad reporting regulations mentioned within “APES 110, auditing standards of Australia as well

as Corporations Act 2001” (Perera, 2016). On the other hand, the auditors attain some

responsibilities which is not aligned with the responsibilities of management and directors.

In addition, it can also be indicated that the auditor has disclosed four major audit factors

within the financial statements along with decreasing their impacts as well. These factors

focus on the fact that Ernst and Young have been increasingly effective for dealing with

material information.

9. Material Based Events

It is deemed important to indicate that two considerable events for Wesfarmers that

took place for the recent year. In such case Coles demerger is also carried out in the current

year in March (Bodle, Cybinski&Monem,2016). Conversely, Ernst & Young have not

considered the event attaining material value as it is anticipated not to attain any material

effect on the company’s financial statements. The Wes farmer Company’s board of directors

has announced totally aligned ordinary dividend of around 120 cents each share because of

which the overall amount of the yearly dividend to be offed to the stakeholders might be

223 cents for each share in the year 2018 and the dividend is yet is to be offered to the

shareholders (Ipino&Parbonetti, 2017).

10. Analysis of Material Information by Auditors

Relied on the perception of the third-party stakeholder, it is deemed important that

Ernst and Young has been increasingly effective in evaluating the material information of

Wesfarmers Limited relied on the financial statements. This is caused based on the auditing

ad reporting regulations mentioned within “APES 110, auditing standards of Australia as well

as Corporations Act 2001” (Perera, 2016). On the other hand, the auditors attain some

responsibilities which is not aligned with the responsibilities of management and directors.

In addition, it can also be indicated that the auditor has disclosed four major audit factors

within the financial statements along with decreasing their impacts as well. These factors

focus on the fact that Ernst and Young have been increasingly effective for dealing with

material information.

11AUDIT COMPLIANCE IN COMPANIES

11. Lack of Material Information

In alignment with the yearly statements of Wesfarmers Limited in the year 2018 it is

also important that the auditors Ernst and Young did not fail to encompass certain material

factors or information attaining material collationregarding the company’s financial

reporting. Every information is elaborated and represented in a better manner by the

Wesfarmers auditors concerned with the material factors which can have drat effect on the

operations of business (Kabir & Rahman, 2016). Wesfarmers have also entertained that the

needed compliance for Ernst and Young with all the important standards for attaining

certain non-audit services. Rather than that, Wesfarmers have offered the auditor with

certain type of work which encompass the work review of auditor itself for undertaking

certain management decisions. For this reason, it can also be indicated that there is lack of

under or partially reported along with material information within the Wesfarmers yearly

financial statements.

12. Questions for Follow-Up

At the duration of the general meeting within Wesfarmers Company, several

relevant questions might be asked to the shareholders of the company (Hardy, 2014). Such

questions are briefly explained in the following points:

Is there existence of any auditor those are associated with financial reports auditing

within the company?

What are the factors those are considered by the audit partner in carrying out

auditing process in companies?

What are functions fulfilled by the companies audit services?

11. Lack of Material Information

In alignment with the yearly statements of Wesfarmers Limited in the year 2018 it is

also important that the auditors Ernst and Young did not fail to encompass certain material

factors or information attaining material collationregarding the company’s financial

reporting. Every information is elaborated and represented in a better manner by the

Wesfarmers auditors concerned with the material factors which can have drat effect on the

operations of business (Kabir & Rahman, 2016). Wesfarmers have also entertained that the

needed compliance for Ernst and Young with all the important standards for attaining

certain non-audit services. Rather than that, Wesfarmers have offered the auditor with

certain type of work which encompass the work review of auditor itself for undertaking

certain management decisions. For this reason, it can also be indicated that there is lack of

under or partially reported along with material information within the Wesfarmers yearly

financial statements.

12. Questions for Follow-Up

At the duration of the general meeting within Wesfarmers Company, several

relevant questions might be asked to the shareholders of the company (Hardy, 2014). Such

questions are briefly explained in the following points:

Is there existence of any auditor those are associated with financial reports auditing

within the company?

What are the factors those are considered by the audit partner in carrying out

auditing process in companies?

What are functions fulfilled by the companies audit services?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.