Detailed Audit, Assurance, and Compliance Report on DIPL's Financials

VerifiedAdded on 2020/02/24

|11

|2301

|65

Report

AI Summary

This report provides a comprehensive analysis of audit, assurance, and compliance issues related to DIPL's financial performance. The executive summary highlights problems hindering DIPL's progress and identifies material misstatement and fraud risks that could manipulate financial statements. The report examines inheritance risks, including the impact of implementing a new accounting system and financial reporting risks, and suggests relevant audit procedures. It analyzes financial ratios (liquidity, efficiency, solvency, and profitability) to identify inconsistencies and potential errors. The report also explores fraudulent activities, such as misrepresentation of financial records and transactional errors, and their impact on audit procedures. The analysis includes the influence of results on audit procedures, the impact of material misstatements, and the identification of fraud risk factors. The report concludes by emphasizing the importance of a cynical approach and proper auditing systems to detect fraud in DIPL's financial reporting. The report is a student contribution published on Desklib, a platform offering AI-based study tools.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE

1

Executive Summary:

The overall report mainly states the problems that were hindering the progress of DIPL.

Furthermore, assignment also focuses and identifying the overall material misstatement risk

and fraudulent risk, which might be used in manipulating the financial statement of the

organisation. The report directly identifies different types of inheritance risk and then needed

audit procedures for confronting the risk in the financial report. Furthermore, relevant audit

procedures are directly provided in the report it could be used by auditors for analysing the

financial report of DIPL.

1

Executive Summary:

The overall report mainly states the problems that were hindering the progress of DIPL.

Furthermore, assignment also focuses and identifying the overall material misstatement risk

and fraudulent risk, which might be used in manipulating the financial statement of the

organisation. The report directly identifies different types of inheritance risk and then needed

audit procedures for confronting the risk in the financial report. Furthermore, relevant audit

procedures are directly provided in the report it could be used by auditors for analysing the

financial report of DIPL.

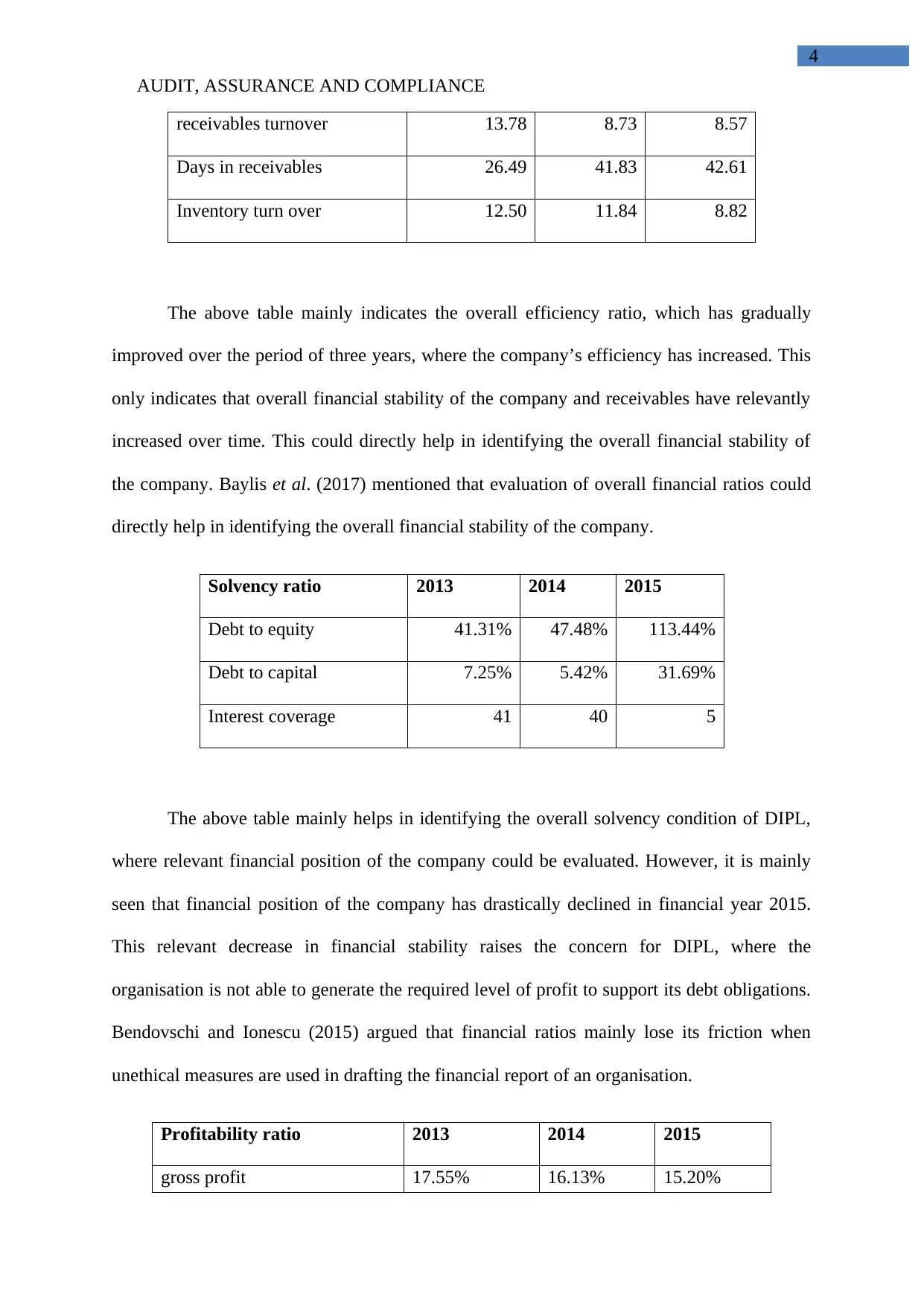

AUDIT, ASSURANCE AND COMPLIANCE

2

Table of Contents

Question 1: Audit procedures influenced by results..................................................................3

Question 2: Material misstatement influencing inheritance risk................................................5

Question 3a: Fraudulent activities of risk factors......................................................................7

Question 3b: Fraud risk affecting audit procedure.....................................................................9

Reference:................................................................................................................................10

2

Table of Contents

Question 1: Audit procedures influenced by results..................................................................3

Question 2: Material misstatement influencing inheritance risk................................................5

Question 3a: Fraudulent activities of risk factors......................................................................7

Question 3b: Fraud risk affecting audit procedure.....................................................................9

Reference:................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE

3

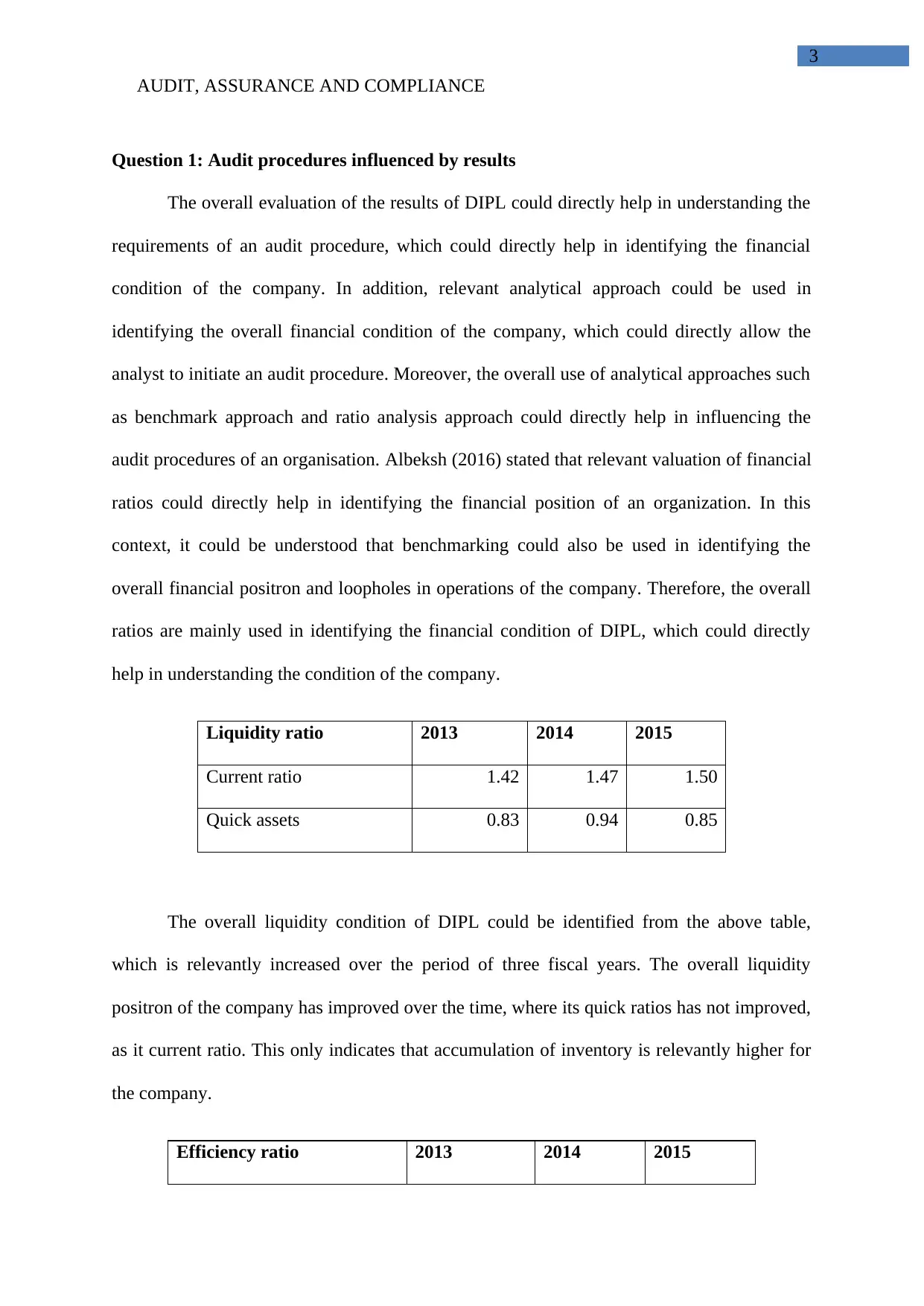

Question 1: Audit procedures influenced by results

The overall evaluation of the results of DIPL could directly help in understanding the

requirements of an audit procedure, which could directly help in identifying the financial

condition of the company. In addition, relevant analytical approach could be used in

identifying the overall financial condition of the company, which could directly allow the

analyst to initiate an audit procedure. Moreover, the overall use of analytical approaches such

as benchmark approach and ratio analysis approach could directly help in influencing the

audit procedures of an organisation. Albeksh (2016) stated that relevant valuation of financial

ratios could directly help in identifying the financial position of an organization. In this

context, it could be understood that benchmarking could also be used in identifying the

overall financial positron and loopholes in operations of the company. Therefore, the overall

ratios are mainly used in identifying the financial condition of DIPL, which could directly

help in understanding the condition of the company.

Liquidity ratio 2013 2014 2015

Current ratio 1.42 1.47 1.50

Quick assets 0.83 0.94 0.85

The overall liquidity condition of DIPL could be identified from the above table,

which is relevantly increased over the period of three fiscal years. The overall liquidity

positron of the company has improved over the time, where its quick ratios has not improved,

as it current ratio. This only indicates that accumulation of inventory is relevantly higher for

the company.

Efficiency ratio 2013 2014 2015

3

Question 1: Audit procedures influenced by results

The overall evaluation of the results of DIPL could directly help in understanding the

requirements of an audit procedure, which could directly help in identifying the financial

condition of the company. In addition, relevant analytical approach could be used in

identifying the overall financial condition of the company, which could directly allow the

analyst to initiate an audit procedure. Moreover, the overall use of analytical approaches such

as benchmark approach and ratio analysis approach could directly help in influencing the

audit procedures of an organisation. Albeksh (2016) stated that relevant valuation of financial

ratios could directly help in identifying the financial position of an organization. In this

context, it could be understood that benchmarking could also be used in identifying the

overall financial positron and loopholes in operations of the company. Therefore, the overall

ratios are mainly used in identifying the financial condition of DIPL, which could directly

help in understanding the condition of the company.

Liquidity ratio 2013 2014 2015

Current ratio 1.42 1.47 1.50

Quick assets 0.83 0.94 0.85

The overall liquidity condition of DIPL could be identified from the above table,

which is relevantly increased over the period of three fiscal years. The overall liquidity

positron of the company has improved over the time, where its quick ratios has not improved,

as it current ratio. This only indicates that accumulation of inventory is relevantly higher for

the company.

Efficiency ratio 2013 2014 2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE

4

receivables turnover 13.78 8.73 8.57

Days in receivables 26.49 41.83 42.61

Inventory turn over 12.50 11.84 8.82

The above table mainly indicates the overall efficiency ratio, which has gradually

improved over the period of three years, where the company’s efficiency has increased. This

only indicates that overall financial stability of the company and receivables have relevantly

increased over time. This could directly help in identifying the overall financial stability of

the company. Baylis et al. (2017) mentioned that evaluation of overall financial ratios could

directly help in identifying the overall financial stability of the company.

Solvency ratio 2013 2014 2015

Debt to equity 41.31% 47.48% 113.44%

Debt to capital 7.25% 5.42% 31.69%

Interest coverage 41 40 5

The above table mainly helps in identifying the overall solvency condition of DIPL,

where relevant financial position of the company could be evaluated. However, it is mainly

seen that financial position of the company has drastically declined in financial year 2015.

This relevant decrease in financial stability raises the concern for DIPL, where the

organisation is not able to generate the required level of profit to support its debt obligations.

Bendovschi and Ionescu (2015) argued that financial ratios mainly lose its friction when

unethical measures are used in drafting the financial report of an organisation.

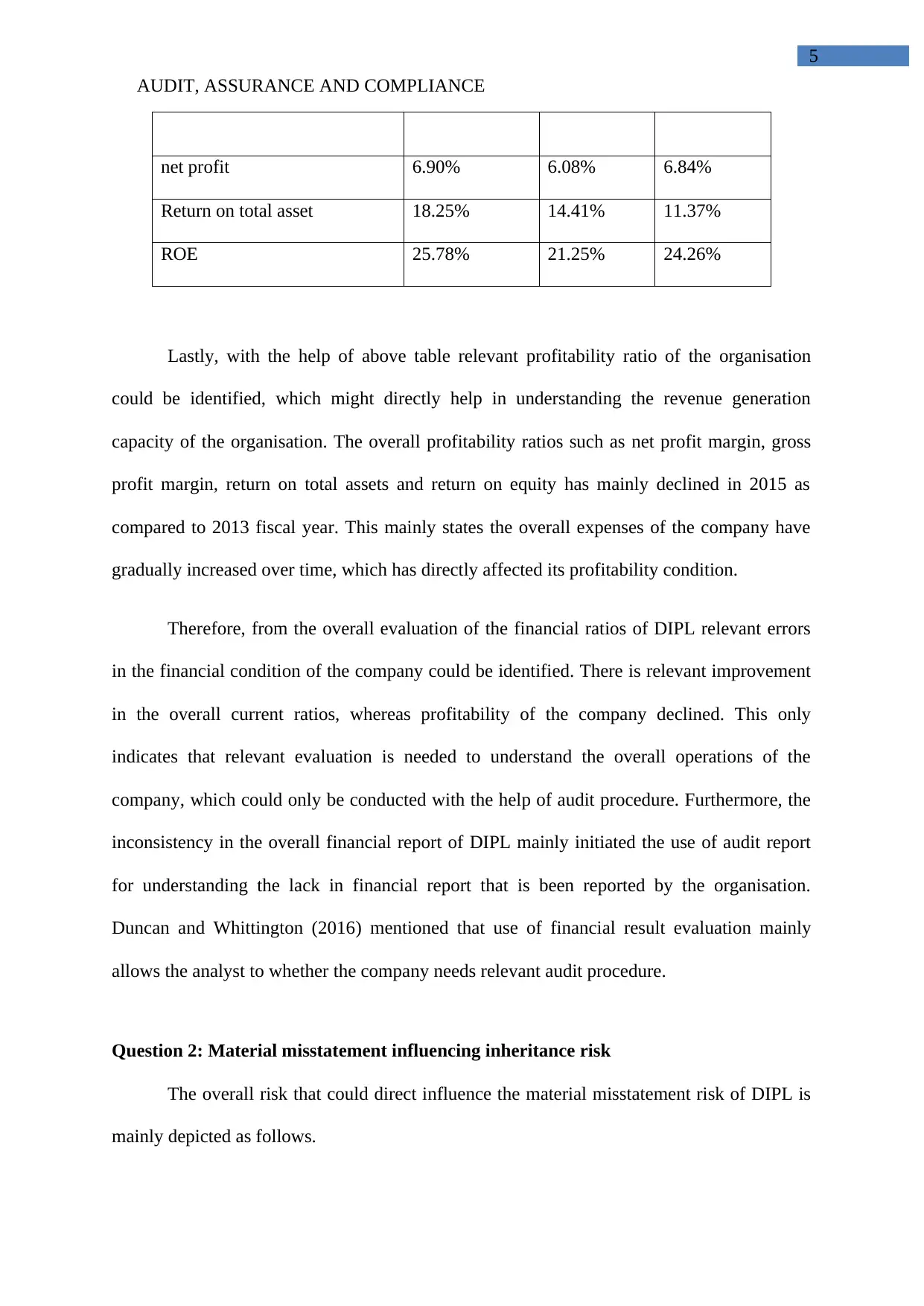

Profitability ratio 2013 2014 2015

gross profit 17.55% 16.13% 15.20%

4

receivables turnover 13.78 8.73 8.57

Days in receivables 26.49 41.83 42.61

Inventory turn over 12.50 11.84 8.82

The above table mainly indicates the overall efficiency ratio, which has gradually

improved over the period of three years, where the company’s efficiency has increased. This

only indicates that overall financial stability of the company and receivables have relevantly

increased over time. This could directly help in identifying the overall financial stability of

the company. Baylis et al. (2017) mentioned that evaluation of overall financial ratios could

directly help in identifying the overall financial stability of the company.

Solvency ratio 2013 2014 2015

Debt to equity 41.31% 47.48% 113.44%

Debt to capital 7.25% 5.42% 31.69%

Interest coverage 41 40 5

The above table mainly helps in identifying the overall solvency condition of DIPL,

where relevant financial position of the company could be evaluated. However, it is mainly

seen that financial position of the company has drastically declined in financial year 2015.

This relevant decrease in financial stability raises the concern for DIPL, where the

organisation is not able to generate the required level of profit to support its debt obligations.

Bendovschi and Ionescu (2015) argued that financial ratios mainly lose its friction when

unethical measures are used in drafting the financial report of an organisation.

Profitability ratio 2013 2014 2015

gross profit 17.55% 16.13% 15.20%

AUDIT, ASSURANCE AND COMPLIANCE

5

net profit 6.90% 6.08% 6.84%

Return on total asset 18.25% 14.41% 11.37%

ROE 25.78% 21.25% 24.26%

Lastly, with the help of above table relevant profitability ratio of the organisation

could be identified, which might directly help in understanding the revenue generation

capacity of the organisation. The overall profitability ratios such as net profit margin, gross

profit margin, return on total assets and return on equity has mainly declined in 2015 as

compared to 2013 fiscal year. This mainly states the overall expenses of the company have

gradually increased over time, which has directly affected its profitability condition.

Therefore, from the overall evaluation of the financial ratios of DIPL relevant errors

in the financial condition of the company could be identified. There is relevant improvement

in the overall current ratios, whereas profitability of the company declined. This only

indicates that relevant evaluation is needed to understand the overall operations of the

company, which could only be conducted with the help of audit procedure. Furthermore, the

inconsistency in the overall financial report of DIPL mainly initiated the use of audit report

for understanding the lack in financial report that is been reported by the organisation.

Duncan and Whittington (2016) mentioned that use of financial result evaluation mainly

allows the analyst to whether the company needs relevant audit procedure.

Question 2: Material misstatement influencing inheritance risk

The overall risk that could direct influence the material misstatement risk of DIPL is

mainly depicted as follows.

5

net profit 6.90% 6.08% 6.84%

Return on total asset 18.25% 14.41% 11.37%

ROE 25.78% 21.25% 24.26%

Lastly, with the help of above table relevant profitability ratio of the organisation

could be identified, which might directly help in understanding the revenue generation

capacity of the organisation. The overall profitability ratios such as net profit margin, gross

profit margin, return on total assets and return on equity has mainly declined in 2015 as

compared to 2013 fiscal year. This mainly states the overall expenses of the company have

gradually increased over time, which has directly affected its profitability condition.

Therefore, from the overall evaluation of the financial ratios of DIPL relevant errors

in the financial condition of the company could be identified. There is relevant improvement

in the overall current ratios, whereas profitability of the company declined. This only

indicates that relevant evaluation is needed to understand the overall operations of the

company, which could only be conducted with the help of audit procedure. Furthermore, the

inconsistency in the overall financial report of DIPL mainly initiated the use of audit report

for understanding the lack in financial report that is been reported by the organisation.

Duncan and Whittington (2016) mentioned that use of financial result evaluation mainly

allows the analyst to whether the company needs relevant audit procedure.

Question 2: Material misstatement influencing inheritance risk

The overall risk that could direct influence the material misstatement risk of DIPL is

mainly depicted as follows.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE

6

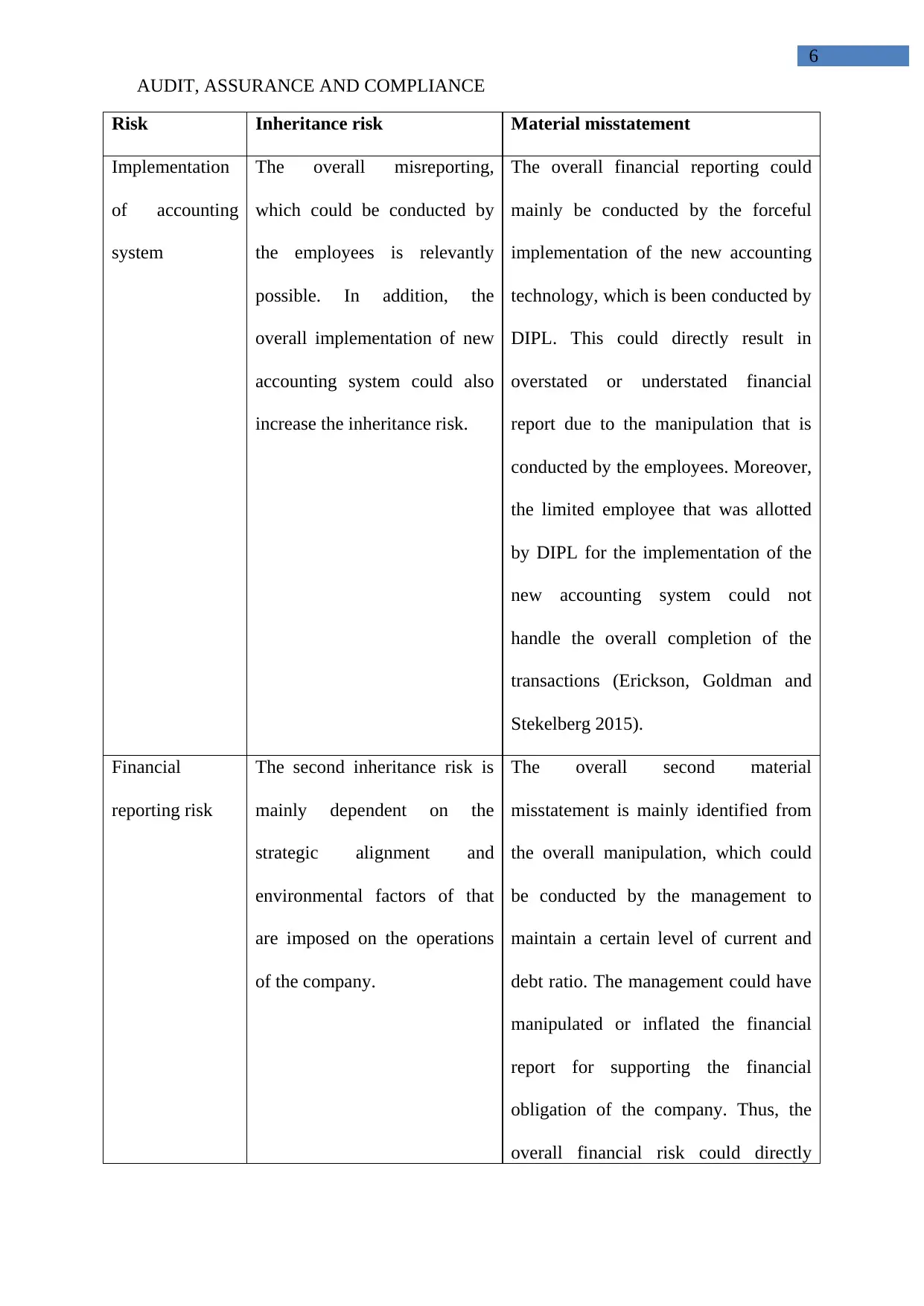

Risk Inheritance risk Material misstatement

Implementation

of accounting

system

The overall misreporting,

which could be conducted by

the employees is relevantly

possible. In addition, the

overall implementation of new

accounting system could also

increase the inheritance risk.

The overall financial reporting could

mainly be conducted by the forceful

implementation of the new accounting

technology, which is been conducted by

DIPL. This could directly result in

overstated or understated financial

report due to the manipulation that is

conducted by the employees. Moreover,

the limited employee that was allotted

by DIPL for the implementation of the

new accounting system could not

handle the overall completion of the

transactions (Erickson, Goldman and

Stekelberg 2015).

Financial

reporting risk

The second inheritance risk is

mainly dependent on the

strategic alignment and

environmental factors of that

are imposed on the operations

of the company.

The overall second material

misstatement is mainly identified from

the overall manipulation, which could

be conducted by the management to

maintain a certain level of current and

debt ratio. The management could have

manipulated or inflated the financial

report for supporting the financial

obligation of the company. Thus, the

overall financial risk could directly

6

Risk Inheritance risk Material misstatement

Implementation

of accounting

system

The overall misreporting,

which could be conducted by

the employees is relevantly

possible. In addition, the

overall implementation of new

accounting system could also

increase the inheritance risk.

The overall financial reporting could

mainly be conducted by the forceful

implementation of the new accounting

technology, which is been conducted by

DIPL. This could directly result in

overstated or understated financial

report due to the manipulation that is

conducted by the employees. Moreover,

the limited employee that was allotted

by DIPL for the implementation of the

new accounting system could not

handle the overall completion of the

transactions (Erickson, Goldman and

Stekelberg 2015).

Financial

reporting risk

The second inheritance risk is

mainly dependent on the

strategic alignment and

environmental factors of that

are imposed on the operations

of the company.

The overall second material

misstatement is mainly identified from

the overall manipulation, which could

be conducted by the management to

maintain a certain level of current and

debt ratio. The management could have

manipulated or inflated the financial

report for supporting the financial

obligation of the company. Thus, the

overall financial risk could directly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE

7

result in material misstatements, which

needs to be evaluated by the auditors

(Knechel and Salterio 2016).

The two inheritance risk that is depicted in the above table mainly states the overall

manipulations, which could be found in the financial report of DIPL. Therefore, this

identified risk could directly influence the financial stability of the company, which is not

depicted in its financial report. Koinig, Tjoa and Ryoo (2015) mentioned that the

identification of relevant material misstatement risk could mainly help the auditors to take

relevant precaution, which could help in identifying viability of the financial report.

Moreover, the inherent risk that is identified from the overall valuation of DIPL case study

could directly increase the chance of material misstatement in its financial report.

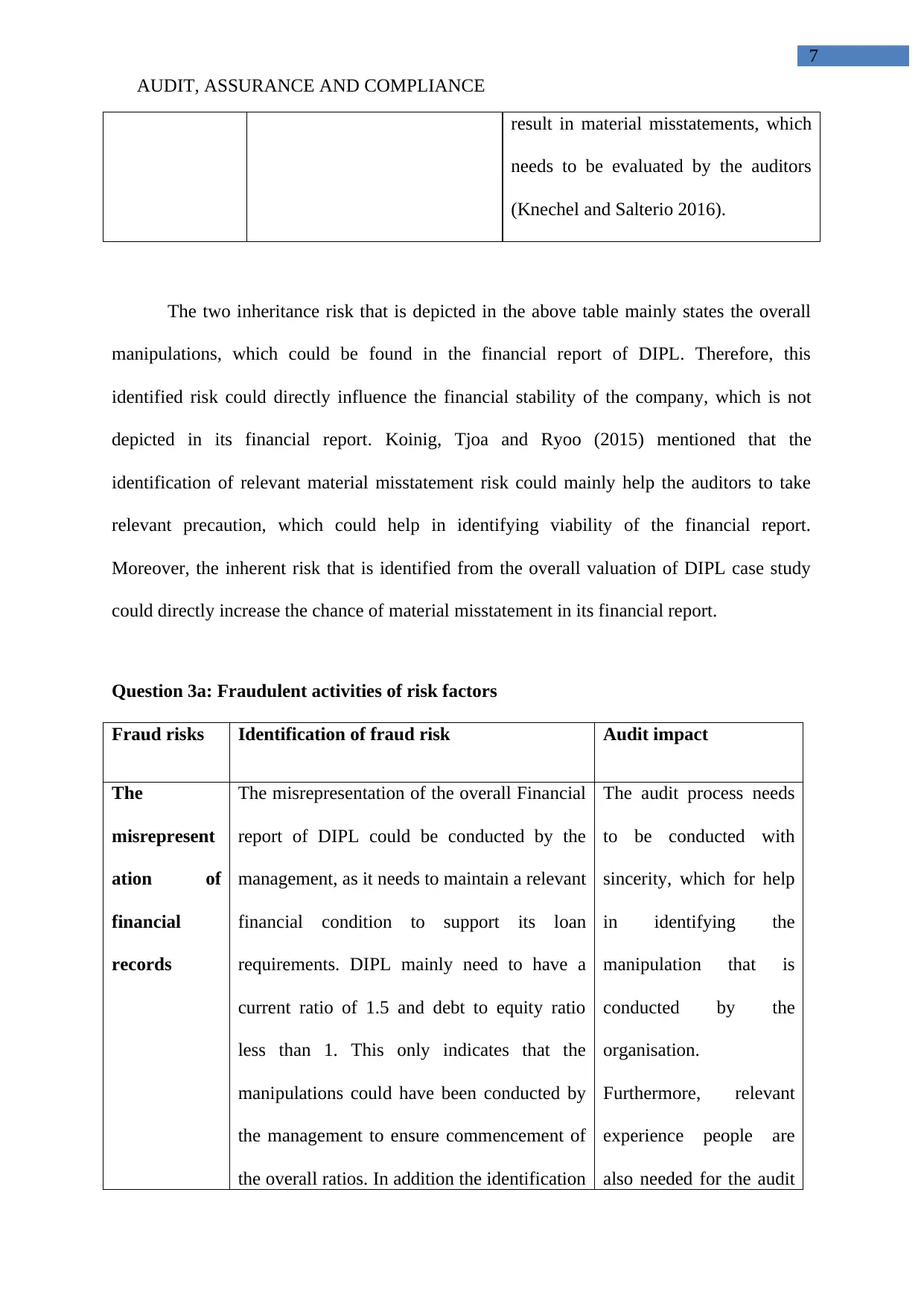

Question 3a: Fraudulent activities of risk factors

Fraud risks Identification of fraud risk Audit impact

The

misrepresent

ation of

financial

records

The misrepresentation of the overall Financial

report of DIPL could be conducted by the

management, as it needs to maintain a relevant

financial condition to support its loan

requirements. DIPL mainly need to have a

current ratio of 1.5 and debt to equity ratio

less than 1. This only indicates that the

manipulations could have been conducted by

the management to ensure commencement of

the overall ratios. In addition the identification

The audit process needs

to be conducted with

sincerity, which for help

in identifying the

manipulation that is

conducted by the

organisation.

Furthermore, relevant

experience people are

also needed for the audit

7

result in material misstatements, which

needs to be evaluated by the auditors

(Knechel and Salterio 2016).

The two inheritance risk that is depicted in the above table mainly states the overall

manipulations, which could be found in the financial report of DIPL. Therefore, this

identified risk could directly influence the financial stability of the company, which is not

depicted in its financial report. Koinig, Tjoa and Ryoo (2015) mentioned that the

identification of relevant material misstatement risk could mainly help the auditors to take

relevant precaution, which could help in identifying viability of the financial report.

Moreover, the inherent risk that is identified from the overall valuation of DIPL case study

could directly increase the chance of material misstatement in its financial report.

Question 3a: Fraudulent activities of risk factors

Fraud risks Identification of fraud risk Audit impact

The

misrepresent

ation of

financial

records

The misrepresentation of the overall Financial

report of DIPL could be conducted by the

management, as it needs to maintain a relevant

financial condition to support its loan

requirements. DIPL mainly need to have a

current ratio of 1.5 and debt to equity ratio

less than 1. This only indicates that the

manipulations could have been conducted by

the management to ensure commencement of

the overall ratios. In addition the identification

The audit process needs

to be conducted with

sincerity, which for help

in identifying the

manipulation that is

conducted by the

organisation.

Furthermore, relevant

experience people are

also needed for the audit

AUDIT, ASSURANCE AND COMPLIANCE

8

of the overall fraud could directly increase the

material misstatement in the annual report,

which could only be detected with the help of

relevant audit procedures (Lenz and Hahn

2015).

procedure, as it could

help in identifying the

ways in which the

company has

manipulated the financial

records (O’Regan 2017).

The

manipulation

from

transactional

error

The second fraud risk is mainly identified

from the overall transaction manipulation that

might be conducted by employees, while

implementing the new accounting system.

There was a relevant pressure on the

employees, while changing the overall

accounting systems. This pressure on the

employees could have told them to use

manipulations in the transaction

recordings. These manipulations in the overall

accounting system could have led to the

material misstatement of financial report

(Shafii, Abidin and Salleh 2015).

Relevant checks needs to

be conducted on the

overall sales receipts and

other transactions

conducted by the

company in the three

fiscal years. Moreover

the new accounting

system needs to be

evaluated with the old

system, where all the

transactions are recorded.

This could mean we have

the auditors to identify

the problem and

manipulation that has

been conducted by the

employees.

8

of the overall fraud could directly increase the

material misstatement in the annual report,

which could only be detected with the help of

relevant audit procedures (Lenz and Hahn

2015).

procedure, as it could

help in identifying the

ways in which the

company has

manipulated the financial

records (O’Regan 2017).

The

manipulation

from

transactional

error

The second fraud risk is mainly identified

from the overall transaction manipulation that

might be conducted by employees, while

implementing the new accounting system.

There was a relevant pressure on the

employees, while changing the overall

accounting systems. This pressure on the

employees could have told them to use

manipulations in the transaction

recordings. These manipulations in the overall

accounting system could have led to the

material misstatement of financial report

(Shafii, Abidin and Salleh 2015).

Relevant checks needs to

be conducted on the

overall sales receipts and

other transactions

conducted by the

company in the three

fiscal years. Moreover

the new accounting

system needs to be

evaluated with the old

system, where all the

transactions are recorded.

This could mean we have

the auditors to identify

the problem and

manipulation that has

been conducted by the

employees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE

9

The above table mainly helps in identifying the overall fraud risk that could be

hampering the overall financial statement of DIPL. in addition relevant audit procedures also

provided in the table which can help auditors to adequately evaluate the actual financial

performance of the organisation. Moreover, the overall fraudulent was mainly derived from

the tell management that is been conducted in DIPL (Short and Toffel 2015).

Question 3b: Fraud risk affecting audit procedure

The overall identified risk mainly represents the Chance of manipulation, which could

be conducted by the management of DIPL. this could mean to be conducted due to the loan

obligations that is used by the company to support its future activity. Euro loan requirements

means the company to hold a relevant financial condition or else it would directly be nullified

by the finance provider. Therefore, relevant manipulations could have been conducted by the

company to ensure continuity of a loan process. Hence, auditors need to adequately evaluate

the overall financial condition of the company by implementing proper methodology.

Moreover, your auditor's also needs to be cynical while evaluating the overall financial report

of DIPL. Proper system in the auditing process also needs to be conducted, which might

increase the chance of fraud detection conducted in the preparation of the financial report (Uc

and Haxhiraj 2015).

9

The above table mainly helps in identifying the overall fraud risk that could be

hampering the overall financial statement of DIPL. in addition relevant audit procedures also

provided in the table which can help auditors to adequately evaluate the actual financial

performance of the organisation. Moreover, the overall fraudulent was mainly derived from

the tell management that is been conducted in DIPL (Short and Toffel 2015).

Question 3b: Fraud risk affecting audit procedure

The overall identified risk mainly represents the Chance of manipulation, which could

be conducted by the management of DIPL. this could mean to be conducted due to the loan

obligations that is used by the company to support its future activity. Euro loan requirements

means the company to hold a relevant financial condition or else it would directly be nullified

by the finance provider. Therefore, relevant manipulations could have been conducted by the

company to ensure continuity of a loan process. Hence, auditors need to adequately evaluate

the overall financial condition of the company by implementing proper methodology.

Moreover, your auditor's also needs to be cynical while evaluating the overall financial report

of DIPL. Proper system in the auditing process also needs to be conducted, which might

increase the chance of fraud detection conducted in the preparation of the financial report (Uc

and Haxhiraj 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE

10

Reference:

ALBEKSH, H.M., 2016. Compliance of Auditors to Ethics and Rules of Professional

Conduct and Its Impact on Audit Quality. Imperial Journal of Interdisciplinary

Research, 2(12).

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private

lenders’ demand for audit. Journal of Accounting and Economics.

BENDOVSCHI, A.C. and IONESCU, B.Ş., 2015. The Gap between Cloud Computing

Technology and the Audit and Information Security. Audit Financiar, 13(125).

Duncan, R.A.K. and Whittington, M., 2016. Enhancing cloud security and privacy: the power

and the weakness of the audit trail. Cloud Computing 2016.

Erickson, M.J., Goldman, N.C. and Stekelberg, J., 2015. The cost of compliance: FIN 48 and

audit fees. The Journal of the American Taxation Association, 38(2), pp.67-85.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Koinig, U., Tjoa, S. and Ryoo, J., 2015, June. Contrology-an ontology-based cloud assurance

approach. In Enabling Technologies: Infrastructure for Collaborative Enterprises (WETICE),

2015 IEEE 24th International Conference on (pp. 105-107). IEEE.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

O’Regan, G., 2017. Software Quality Assurance. In Concise Guide to Software

Engineering (pp. 131-138). Springer International Publishing.

10

Reference:

ALBEKSH, H.M., 2016. Compliance of Auditors to Ethics and Rules of Professional

Conduct and Its Impact on Audit Quality. Imperial Journal of Interdisciplinary

Research, 2(12).

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private

lenders’ demand for audit. Journal of Accounting and Economics.

BENDOVSCHI, A.C. and IONESCU, B.Ş., 2015. The Gap between Cloud Computing

Technology and the Audit and Information Security. Audit Financiar, 13(125).

Duncan, R.A.K. and Whittington, M., 2016. Enhancing cloud security and privacy: the power

and the weakness of the audit trail. Cloud Computing 2016.

Erickson, M.J., Goldman, N.C. and Stekelberg, J., 2015. The cost of compliance: FIN 48 and

audit fees. The Journal of the American Taxation Association, 38(2), pp.67-85.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Koinig, U., Tjoa, S. and Ryoo, J., 2015, June. Contrology-an ontology-based cloud assurance

approach. In Enabling Technologies: Infrastructure for Collaborative Enterprises (WETICE),

2015 IEEE 24th International Conference on (pp. 105-107). IEEE.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

O’Regan, G., 2017. Software Quality Assurance. In Concise Guide to Software

Engineering (pp. 131-138). Springer International Publishing.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.