Audit, Assurance, and Compliance: DIPL Case Study Analysis Report

VerifiedAdded on 2020/03/04

|12

|2880

|56

Report

AI Summary

This report provides a detailed analysis of audit, assurance, and compliance for Double Ink Printers Limited (DIPL). It begins with an examination of audit planning, emphasizing the value of analytical approaches, particularly in assessing financial information through ratio analysis and benchmarking. The report then identifies various risk factors stemming from DIPL's business operations, including issues related to management practices, staffing levels, and CEO succession. Furthermore, it delves into fraud risks, differentiating between types of risks, such as those related to employee dissatisfaction and financial reporting pressures. The analysis encompasses a discussion of financial reporting and how the need to meet certain financial targets can contribute to fraud risk. The report concludes with an assessment of the valuation of raw materials and provides recommendations on how to monitor tasks to detect fraudulent activities.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Answer to Question 3:.....................................................................................................................6

Answer to Part A:........................................................................................................................6

Answer to Part B:.......................................................................................................................10

References:....................................................................................................................................11

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Answer to Question 3:.....................................................................................................................6

Answer to Part A:........................................................................................................................6

Answer to Part B:.......................................................................................................................10

References:....................................................................................................................................11

2AUDIT, ASSURANCE AND COMPLIANCE

Answer to Question 1:

In the method of preparing the audit plan of Double Ink Printers Limited (DIPL), the

analytical method associated with financial information provides immense value. On the

contrary, audit plan delivers the required directions and guidelines to the auditors during the

audit6 operations. Precisely, audit plan enables the auditors in maintaining the cost of audit in a

particular limit for preventing misunderstanding with the audit clients (Alam 2014). The

analytical approach related to the financial information of DIPL denotes the method of spreading

financial information from the various financial declarations of the organisation. The method of

analysing the financial information of the organisations could be carried out through several

mechanisms.

With the help of analytical approach for assessing the financial information, the

accountants and financial analysts of the organisations could utilise such information for

undertaking different financial and accounting decisions (Baylis et al. 2017). The common size

analytical approach enables in the method of dissecting the financial declaration of the

organisations from the common points of reference. One of the primary benefits is that it helps in

extending support in contrasting the financial reports from various financial timelines.

The accountants and financial analysts could utilise different lines of items from the

financial reports and they could verify their base of preparation for the organisations. For

instance, the registration procedure of different financial and accounting items in the financial

reports such as net liabilities, assets, owner’s equity and others could be considered coupled with

assessment of digression from the normal scenario (Brawley et al. 2015). Benchmarking is the

main analytical process of financial information and this method could be utilised for evaluation

Answer to Question 1:

In the method of preparing the audit plan of Double Ink Printers Limited (DIPL), the

analytical method associated with financial information provides immense value. On the

contrary, audit plan delivers the required directions and guidelines to the auditors during the

audit6 operations. Precisely, audit plan enables the auditors in maintaining the cost of audit in a

particular limit for preventing misunderstanding with the audit clients (Alam 2014). The

analytical approach related to the financial information of DIPL denotes the method of spreading

financial information from the various financial declarations of the organisation. The method of

analysing the financial information of the organisations could be carried out through several

mechanisms.

With the help of analytical approach for assessing the financial information, the

accountants and financial analysts of the organisations could utilise such information for

undertaking different financial and accounting decisions (Baylis et al. 2017). The common size

analytical approach enables in the method of dissecting the financial declaration of the

organisations from the common points of reference. One of the primary benefits is that it helps in

extending support in contrasting the financial reports from various financial timelines.

The accountants and financial analysts could utilise different lines of items from the

financial reports and they could verify their base of preparation for the organisations. For

instance, the registration procedure of different financial and accounting items in the financial

reports such as net liabilities, assets, owner’s equity and others could be considered coupled with

assessment of digression from the normal scenario (Brawley et al. 2015). Benchmarking is the

main analytical process of financial information and this method could be utilised for evaluation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

of the audit plan of the organisation. The benchmarking process helps in identifying the

variances in the financial reports of the organisations and the real reasons behind the occurrences

of these variances could be ascertained by identifying the root cause of these variances. Besides

the process of benchmarking, ratio analysis is adjudged as a major analytical method of financial

information of the organisations. Ratio analysis is immensely beneficial in contrasting the

financial statements of two or more organisations for preparing the plan of audit (Chambers and

Odar 2015).

Explanation:

The adopted analytical approaches of the organisations in evaluating the financial

information has significant effect on the development of the process related to audit planning and

this is crucial to spread financial information amongst the different departments of the

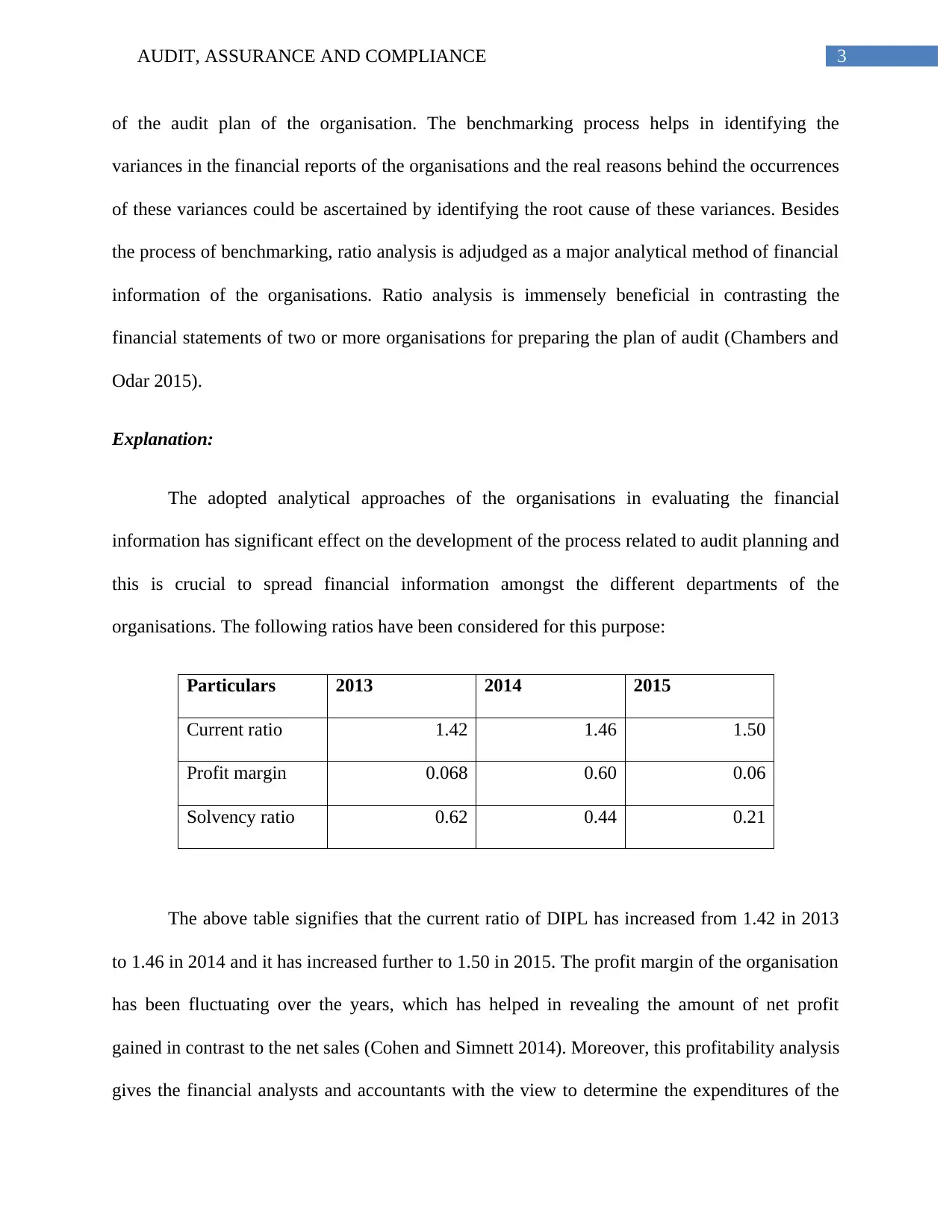

organisations. The following ratios have been considered for this purpose:

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

The above table signifies that the current ratio of DIPL has increased from 1.42 in 2013

to 1.46 in 2014 and it has increased further to 1.50 in 2015. The profit margin of the organisation

has been fluctuating over the years, which has helped in revealing the amount of net profit

gained in contrast to the net sales (Cohen and Simnett 2014). Moreover, this profitability analysis

gives the financial analysts and accountants with the view to determine the expenditures of the

of the audit plan of the organisation. The benchmarking process helps in identifying the

variances in the financial reports of the organisations and the real reasons behind the occurrences

of these variances could be ascertained by identifying the root cause of these variances. Besides

the process of benchmarking, ratio analysis is adjudged as a major analytical method of financial

information of the organisations. Ratio analysis is immensely beneficial in contrasting the

financial statements of two or more organisations for preparing the plan of audit (Chambers and

Odar 2015).

Explanation:

The adopted analytical approaches of the organisations in evaluating the financial

information has significant effect on the development of the process related to audit planning and

this is crucial to spread financial information amongst the different departments of the

organisations. The following ratios have been considered for this purpose:

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

The above table signifies that the current ratio of DIPL has increased from 1.42 in 2013

to 1.46 in 2014 and it has increased further to 1.50 in 2015. The profit margin of the organisation

has been fluctuating over the years, which has helped in revealing the amount of net profit

gained in contrast to the net sales (Cohen and Simnett 2014). Moreover, this profitability analysis

gives the financial analysts and accountants with the view to determine the expenditures of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

organisation. Besides, it enables the financial analysts and accountants to gain an overview of the

effectiveness of the organisational budget along with the need for business diversification

(Decaux and Sarens 2015).

The favourable and unfavourable changes in the financial performance and ratios of

DIPL enable the auditors to create an insight about the existing financial position of the

organisations. In this context, the solvency ratio has been considered, which has declined over

the years. Such evaluation is helpful in determining the desirable or undesirable trend of the

organisational performance over the subsequent years. The contrast of ratios has its significance

in ascertaining whether the existing cash flow of the organisation is adequate for meeting both

short-term and long-term obligations.

Precisely, it could be stated that the comparison and evaluation of financial performance

and ratios enables the financial analysts and accountants for ascertaining the relative financial

position of the organisation over three-year period. It enables in ascertaining whether the existing

financial position of the organisation is desirable or not. In case of the latter, the management of

the organisation is required to undertake corrective actions for reviving its overall financial

performance. Due to all these reasons, the analytical procedure pertaining to financial

information has significant value (Duncan and Whittington 2014).

Answer to Question 2:

Certain risk factors could be raised from the business operations of DIPL. In accordance

with the case study, the management of an organisation has failed to enter various business

transactions of the organisation. This procedure has direct relationship with the inconsistencies in

the planning of different marketing and sales activities of the organisation (Earley et al. 2016).

organisation. Besides, it enables the financial analysts and accountants to gain an overview of the

effectiveness of the organisational budget along with the need for business diversification

(Decaux and Sarens 2015).

The favourable and unfavourable changes in the financial performance and ratios of

DIPL enable the auditors to create an insight about the existing financial position of the

organisations. In this context, the solvency ratio has been considered, which has declined over

the years. Such evaluation is helpful in determining the desirable or undesirable trend of the

organisational performance over the subsequent years. The contrast of ratios has its significance

in ascertaining whether the existing cash flow of the organisation is adequate for meeting both

short-term and long-term obligations.

Precisely, it could be stated that the comparison and evaluation of financial performance

and ratios enables the financial analysts and accountants for ascertaining the relative financial

position of the organisation over three-year period. It enables in ascertaining whether the existing

financial position of the organisation is desirable or not. In case of the latter, the management of

the organisation is required to undertake corrective actions for reviving its overall financial

performance. Due to all these reasons, the analytical procedure pertaining to financial

information has significant value (Duncan and Whittington 2014).

Answer to Question 2:

Certain risk factors could be raised from the business operations of DIPL. In accordance

with the case study, the management of an organisation has failed to enter various business

transactions of the organisation. This procedure has direct relationship with the inconsistencies in

the planning of different marketing and sales activities of the organisation (Earley et al. 2016).

5AUDIT, ASSURANCE AND COMPLIANCE

The overall financial analysis carried out in the context of DIPL states that the organisation has

failed to accomplish the targeted level of profit from the overall sales revenue. The primary

reason is the ineffectiveness and inefficiency of the management of the organisation in business

operations. Therefore, it could be observed that the organisation has failed to gauge the effect of

different micro and macro-economic factors having impact on the business operations of DIPL

like political, economic and social factors. Hence, it could be stated that the lower revenue and

profit margin of the organisation has resulted in inherent risks (Graham 2015).

Moreover, the staffs of DIPL have increased rapidly and as a result, the inherent risk has

increased as well. The inherent risk level of the organisation rises because of the lack of

professionalism and experienced proficiency of the staffs. This is because the success of a

business is reliant largely on the performance of its staffs (Homb et al. 2014). Due to such

inexperience and inefficiency of the workforce of DIPL, there is greater chance of inherent risks,

since the employees are bound to conduct mistakes. Based on the provided case of DIPL, the

issues could be found in the succession process of CEO of the organisation. Due to this, such

process has resulted in rise in inherent risks of the organisation. The main inherent risk could be

observed in the ineffective method of selecting the CEO succession of the organisation.

Besides this, it could be observed that DIPL does not have sufficient staffs for managing

its business operations. This reason has resulted in rise in inherent risks in the overall business

functioning of DIPL. Hence, from the above evaluation, it could be observed that these are the

primary reasons of the rise in inherent risks in the business operations of DIPL (Jones and

Beattie 2015).

Explanation:

The overall financial analysis carried out in the context of DIPL states that the organisation has

failed to accomplish the targeted level of profit from the overall sales revenue. The primary

reason is the ineffectiveness and inefficiency of the management of the organisation in business

operations. Therefore, it could be observed that the organisation has failed to gauge the effect of

different micro and macro-economic factors having impact on the business operations of DIPL

like political, economic and social factors. Hence, it could be stated that the lower revenue and

profit margin of the organisation has resulted in inherent risks (Graham 2015).

Moreover, the staffs of DIPL have increased rapidly and as a result, the inherent risk has

increased as well. The inherent risk level of the organisation rises because of the lack of

professionalism and experienced proficiency of the staffs. This is because the success of a

business is reliant largely on the performance of its staffs (Homb et al. 2014). Due to such

inexperience and inefficiency of the workforce of DIPL, there is greater chance of inherent risks,

since the employees are bound to conduct mistakes. Based on the provided case of DIPL, the

issues could be found in the succession process of CEO of the organisation. Due to this, such

process has resulted in rise in inherent risks of the organisation. The main inherent risk could be

observed in the ineffective method of selecting the CEO succession of the organisation.

Besides this, it could be observed that DIPL does not have sufficient staffs for managing

its business operations. This reason has resulted in rise in inherent risks in the overall business

functioning of DIPL. Hence, from the above evaluation, it could be observed that these are the

primary reasons of the rise in inherent risks in the business operations of DIPL (Jones and

Beattie 2015).

Explanation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

It has been observed that there is huge amount of workload on the employees of the

organisation. The increasing workload results in poor bookkeeping of the organisation and this

problem further results in different issues of cash flow, ineffective operating results ineffective

solvency and liquidity position of the organisation. Besides this, the risk of error could be

depicted in the financial statements due to lack of effective interpretation. In this context, the

management of DIPL needs to play an effective role. It has been observed that the DIPL

management lacks accountability and integrity and due to this reason, they are encountering the

concern of losing reputation in the business community. The greater incentive structure related to

management forms additional pressure on management and it results in material misstatements in

the financial reports (Levy 2015).

Answer to Question 3:

Answer to Part A:

In the current business organisations, fraud risk is adjudged as the main risk in the

context of the same. Due to the occurrence of such fraudulent risk, the business organisations

often incur severe losses in its business assets (Martin, Sanders and Scalan 2014). In majority of

the situations, the primary dissatisfaction could be observed among the workforce and such

dissatisfaction often compel them to engage in various types of frauds in organisations. Another

primary reason of fraud is the expectation of various investors of the organisations. The

organisations often make promises for achieving a specific financial performance that

contributes to greater fraud level (Nalewaik and Mills 2016).

Types of risk Identification

Fraud risk In the context of the business operations of

It has been observed that there is huge amount of workload on the employees of the

organisation. The increasing workload results in poor bookkeeping of the organisation and this

problem further results in different issues of cash flow, ineffective operating results ineffective

solvency and liquidity position of the organisation. Besides this, the risk of error could be

depicted in the financial statements due to lack of effective interpretation. In this context, the

management of DIPL needs to play an effective role. It has been observed that the DIPL

management lacks accountability and integrity and due to this reason, they are encountering the

concern of losing reputation in the business community. The greater incentive structure related to

management forms additional pressure on management and it results in material misstatements in

the financial reports (Levy 2015).

Answer to Question 3:

Answer to Part A:

In the current business organisations, fraud risk is adjudged as the main risk in the

context of the same. Due to the occurrence of such fraudulent risk, the business organisations

often incur severe losses in its business assets (Martin, Sanders and Scalan 2014). In majority of

the situations, the primary dissatisfaction could be observed among the workforce and such

dissatisfaction often compel them to engage in various types of frauds in organisations. Another

primary reason of fraud is the expectation of various investors of the organisations. The

organisations often make promises for achieving a specific financial performance that

contributes to greater fraud level (Nalewaik and Mills 2016).

Types of risk Identification

Fraud risk In the context of the business operations of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

DIPL, the main risk that could occur from its

business activities is the involvement of the

staffs in various kinds of fraudulent activities.

This could take place due to dissatisfaction of

the employees. In accordance with the

provided case of DIPL, it could be observed

that there is enormous pressure from the part of

the board of the organisation to adopt a new

system of accounting. The adoption of this new

system of accounting develops a heavy

pressure on the workforce of the organisation

and such pressure results in fraud. Hence, it

could be stated that for coping up with the

reconciliation pressure, the staffs might adopt

fraudulent activities, which would lead to

incorrect handling of the overall procedure

resulting in material misstatements.

According to the case study, it could be

observed that the procedure of inefficient

handling of the implementation of new

information technology results in ineffective

treatment of few primary financial and

accounting transactions at the finish of the

DIPL, the main risk that could occur from its

business activities is the involvement of the

staffs in various kinds of fraudulent activities.

This could take place due to dissatisfaction of

the employees. In accordance with the

provided case of DIPL, it could be observed

that there is enormous pressure from the part of

the board of the organisation to adopt a new

system of accounting. The adoption of this new

system of accounting develops a heavy

pressure on the workforce of the organisation

and such pressure results in fraud. Hence, it

could be stated that for coping up with the

reconciliation pressure, the staffs might adopt

fraudulent activities, which would lead to

incorrect handling of the overall procedure

resulting in material misstatements.

According to the case study, it could be

observed that the procedure of inefficient

handling of the implementation of new

information technology results in ineffective

treatment of few primary financial and

accounting transactions at the finish of the

8AUDIT, ASSURANCE AND COMPLIANCE

year. This overall process might result in loss

of material misstatements and financial

information.

Due to such inexperience and inefficiency of

the workforce of DIPL, there is greater chance

of inherent risks, since the employees are

bound to conduct mistakes. Based on the

provided case of DIPL, the issues could be

found in the succession process of CEO of the

organisation. Due to this, such process has

resulted in rise in inherent risks of the

organisation. The main inherent risk could be

observed in the ineffective method of selecting

the CEO succession of the organisation. It has

been observed that the DIPL management

lacks accountability and integrity and due to

this reason, they are encountering the concern

of losing reputation in the business community.

Process of financial reporting Another major risk is associated with the

procedure of financial reporting. The greater

risk of ineffective financial declarations could

be viewed, if additional financial expectations

could be observed from different stakeholders

year. This overall process might result in loss

of material misstatements and financial

information.

Due to such inexperience and inefficiency of

the workforce of DIPL, there is greater chance

of inherent risks, since the employees are

bound to conduct mistakes. Based on the

provided case of DIPL, the issues could be

found in the succession process of CEO of the

organisation. Due to this, such process has

resulted in rise in inherent risks of the

organisation. The main inherent risk could be

observed in the ineffective method of selecting

the CEO succession of the organisation. It has

been observed that the DIPL management

lacks accountability and integrity and due to

this reason, they are encountering the concern

of losing reputation in the business community.

Process of financial reporting Another major risk is associated with the

procedure of financial reporting. The greater

risk of ineffective financial declarations could

be viewed, if additional financial expectations

could be observed from different stakeholders

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

for the financial declarations. This is true in

cases of announcement from the management

of the organisation to achieve particular target

of performance and particular target of the

objectives for debt acquisition. Based on the

financial reports of DIPL, it could be observed

that there is rise in revenue of the organisation

from 2013 to 2015. Besides this, there is rise in

gross income and net income of the

organisation. Based on the case study, it could

be stated that DIPL has acquired a loan of 7.5

million from BDO Finance in 2015.

According to the case study, it could be

observed that in accordance with the agreement

of loan, DIPL is required to maintain a current

ratio of 1.5 and debt-to-equity ratio below 1.

The requirement of this particular arrangement

might be to develop pressure on the

organisation for repaying the loan in

accordance with the agreed timeline. These

needs could result in fraudulent activities, since

DIPL might manipulate the financial

statements for false depiction of the financial

for the financial declarations. This is true in

cases of announcement from the management

of the organisation to achieve particular target

of performance and particular target of the

objectives for debt acquisition. Based on the

financial reports of DIPL, it could be observed

that there is rise in revenue of the organisation

from 2013 to 2015. Besides this, there is rise in

gross income and net income of the

organisation. Based on the case study, it could

be stated that DIPL has acquired a loan of 7.5

million from BDO Finance in 2015.

According to the case study, it could be

observed that in accordance with the agreement

of loan, DIPL is required to maintain a current

ratio of 1.5 and debt-to-equity ratio below 1.

The requirement of this particular arrangement

might be to develop pressure on the

organisation for repaying the loan in

accordance with the agreed timeline. These

needs could result in fraudulent activities, since

DIPL might manipulate the financial

statements for false depiction of the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

condition of the organisation. If DIPL is not

able to maintain the needed benchmark, the

organisation would not be eligible to obtain

loan from BDO Finance (Pitt 2014).

Answer to Part B:

Based on the provided case, it could be observed that the process of valuation of the raw

materials of the organisation based on average cost is not appropriate and effective, since the

present paper cost is above the average cost. The primary risk in the detection of fraudulent

activities of the staffs for implementing new system of information technology could be

identified by monitoring the tasks in various phrases of jobs. Besides this risk, the risk associated

with the process of financial reporting could be detected through evaluation of the different

financial reports and statements of the organisations on the part of the accountants and financial

analysts through different control and analytical mechanisms. Such process of monitoring is

required to be conducted in a timely manner (Warren 2014).

condition of the organisation. If DIPL is not

able to maintain the needed benchmark, the

organisation would not be eligible to obtain

loan from BDO Finance (Pitt 2014).

Answer to Part B:

Based on the provided case, it could be observed that the process of valuation of the raw

materials of the organisation based on average cost is not appropriate and effective, since the

present paper cost is above the average cost. The primary risk in the detection of fraudulent

activities of the staffs for implementing new system of information technology could be

identified by monitoring the tasks in various phrases of jobs. Besides this risk, the risk associated

with the process of financial reporting could be detected through evaluation of the different

financial reports and statements of the organisations on the part of the accountants and financial

analysts through different control and analytical mechanisms. Such process of monitoring is

required to be conducted in a timely manner (Warren 2014).

11AUDIT, ASSURANCE AND COMPLIANCE

References:

Alam, I.U., 2014. Effectual compliance audit of vendors development.

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private lenders’

demand for audit. Journal of Accounting and Economics.

Brawley, S., Clark, J., Dixon, C., Ford, L., Nielsen, E., Ross, S. and Upton, S., 2015. History on

trial: Evaluating learning outcomes through audit and accreditation in a national standards

environment. Teaching and Learning Inquiry: The ISSOTL Journal, 3(2), pp.89-105.

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), pp.59-74.

Decaux, L. and Sarens, G., 2015. Implementing combined assurance: insights from multiple case

studies. Managerial Auditing Journal, 30(1), pp.56-79.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance and

audit: Does this equal security?. In Proceedings of the 7th International Conference on Security

of Information and Networks (p. 77). ACM.

Earley, C.E., Hooks, K.L., Joe, J.R., Polinski, P.W., Rezaee, Z., Roush, P.B., Sanderson, K.A.

and Wu, Y.J., 2016. The Auditing Standards Committee of the Auditing Section of the American

Accounting Association's Response to the International Auditing and Assurance Standard's

References:

Alam, I.U., 2014. Effectual compliance audit of vendors development.

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private lenders’

demand for audit. Journal of Accounting and Economics.

Brawley, S., Clark, J., Dixon, C., Ford, L., Nielsen, E., Ross, S. and Upton, S., 2015. History on

trial: Evaluating learning outcomes through audit and accreditation in a national standards

environment. Teaching and Learning Inquiry: The ISSOTL Journal, 3(2), pp.89-105.

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), pp.59-74.

Decaux, L. and Sarens, G., 2015. Implementing combined assurance: insights from multiple case

studies. Managerial Auditing Journal, 30(1), pp.56-79.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance and

audit: Does this equal security?. In Proceedings of the 7th International Conference on Security

of Information and Networks (p. 77). ACM.

Earley, C.E., Hooks, K.L., Joe, J.R., Polinski, P.W., Rezaee, Z., Roush, P.B., Sanderson, K.A.

and Wu, Y.J., 2016. The Auditing Standards Committee of the Auditing Section of the American

Accounting Association's Response to the International Auditing and Assurance Standard's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.