Audit, Assurance, and Compliance: Financial Analysis of DIPL Company

VerifiedAdded on 2020/03/07

|12

|2884

|37

Report

AI Summary

This report provides a comprehensive analysis of the audit, assurance, and compliance aspects of Double Ink Printers Limited (DIPL). It begins by explaining analytical procedures in accordance with financial report information, emphasizing the use of ratio analysis and common sizing approaches for evaluating financial performance and influencing audit decisions. The report then delves into the classification of inherent risks stemming from DIPL's business operations, focusing on material misstatements, ineffective planning, and staff proficiency issues. Furthermore, the report classifies fraud risks, identifying factors such as worker dissatisfaction and pressure from management that could lead to fraudulent activities and material misstatements. The impact of identified risk factors on the audit process is examined, highlighting the importance of auditors assessing the limitations and potential costs associated with the audit. The report concludes by underscoring the significance of identifying and mitigating risks to ensure the accuracy and reliability of financial reporting.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Question 1........................................................................................................................................3

Explain analytical procedure in accordance to financial report information for Double Ink

Printers limited.................................................................................................................................3

Analyzing the results that influences decisions while auditing for Double Ink Printers limited....4

Question 2........................................................................................................................................5

Classification of inherent risk from the nature of business operations of Double Ink Printers

limited..............................................................................................................................................5

Question 3........................................................................................................................................8

Classifying the fraud risk that arise from fraudulent activities and related to material

misstatement of the company..........................................................................................................8

Impact of the identified risk factors at the time of conducting audit...............................................9

Reference List................................................................................................................................10

Appendix........................................................................................................................................12

Table of Contents

Question 1........................................................................................................................................3

Explain analytical procedure in accordance to financial report information for Double Ink

Printers limited.................................................................................................................................3

Analyzing the results that influences decisions while auditing for Double Ink Printers limited....4

Question 2........................................................................................................................................5

Classification of inherent risk from the nature of business operations of Double Ink Printers

limited..............................................................................................................................................5

Question 3........................................................................................................................................8

Classifying the fraud risk that arise from fraudulent activities and related to material

misstatement of the company..........................................................................................................8

Impact of the identified risk factors at the time of conducting audit...............................................9

Reference List................................................................................................................................10

Appendix........................................................................................................................................12

3AUDIT, ASSURANCE AND COMPLIANCE

Question 1

Explain analytical procedure in accordance to financial report information for Double Ink

Printers limited

Auditors need to carry out the audit function of particular company after using analytical

procedures that contains financial information as presented in the financial report of Double Ink

Printers limited (Wong & Millington, 2014). Auditor need to first plan the audit function of

organization by following the guidelines and standards so that there is no discrepancy of

information, avoid any mistakes, errors or any misrepresentation of figures. The information will

be collected by the auditor from the financial declaration and applies analytical procedures for a

given company. Accountants of any Business Corporation need to undertake strategic, tactical

decisions and these decisions are done after audit is done. It is only after then when accountants

can easily interpret the information and present it by using analytical approach in the financial

declarations.

Business Organization can make use of common sizing approach where they can prepare

the declarations and make the comparison with the financial statement (William, Glover &

Prawitt, 2016). The other tool to measure the financial performance of a company is ratio

analysis and this tool can measure four broad aspects such as liquidity, solvency, profitability as

well as efficiency. Ratio analysis can be termed as one type of analytical procedure that is used

by Business Corporation that helps at the time of conducting audit function. On the other hand,

the common size approach assist auditor for getting access to financial information and there is

positive relationship between financial data and non-financial data. It is the responsibility of the

Question 1

Explain analytical procedure in accordance to financial report information for Double Ink

Printers limited

Auditors need to carry out the audit function of particular company after using analytical

procedures that contains financial information as presented in the financial report of Double Ink

Printers limited (Wong & Millington, 2014). Auditor need to first plan the audit function of

organization by following the guidelines and standards so that there is no discrepancy of

information, avoid any mistakes, errors or any misrepresentation of figures. The information will

be collected by the auditor from the financial declaration and applies analytical procedures for a

given company. Accountants of any Business Corporation need to undertake strategic, tactical

decisions and these decisions are done after audit is done. It is only after then when accountants

can easily interpret the information and present it by using analytical approach in the financial

declarations.

Business Organization can make use of common sizing approach where they can prepare

the declarations and make the comparison with the financial statement (William, Glover &

Prawitt, 2016). The other tool to measure the financial performance of a company is ratio

analysis and this tool can measure four broad aspects such as liquidity, solvency, profitability as

well as efficiency. Ratio analysis can be termed as one type of analytical procedure that is used

by Business Corporation that helps at the time of conducting audit function. On the other hand,

the common size approach assist auditor for getting access to financial information and there is

positive relationship between financial data and non-financial data. It is the responsibility of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDIT, ASSURANCE AND COMPLIANCE

auditor to understand the line of items that are mentioned in the financial report for evaluating

activities. In addition, the auditors should have complete detailed information of their client.

Analytical procedure should be used by the auditor for audit planning like benchmarking. There

are various other factor variances that are present in the financial declaration that are deducted

and any deductions identified in the benchmarking process.

Analyzing the results that influences decisions while auditing for Double Ink Printers

limited

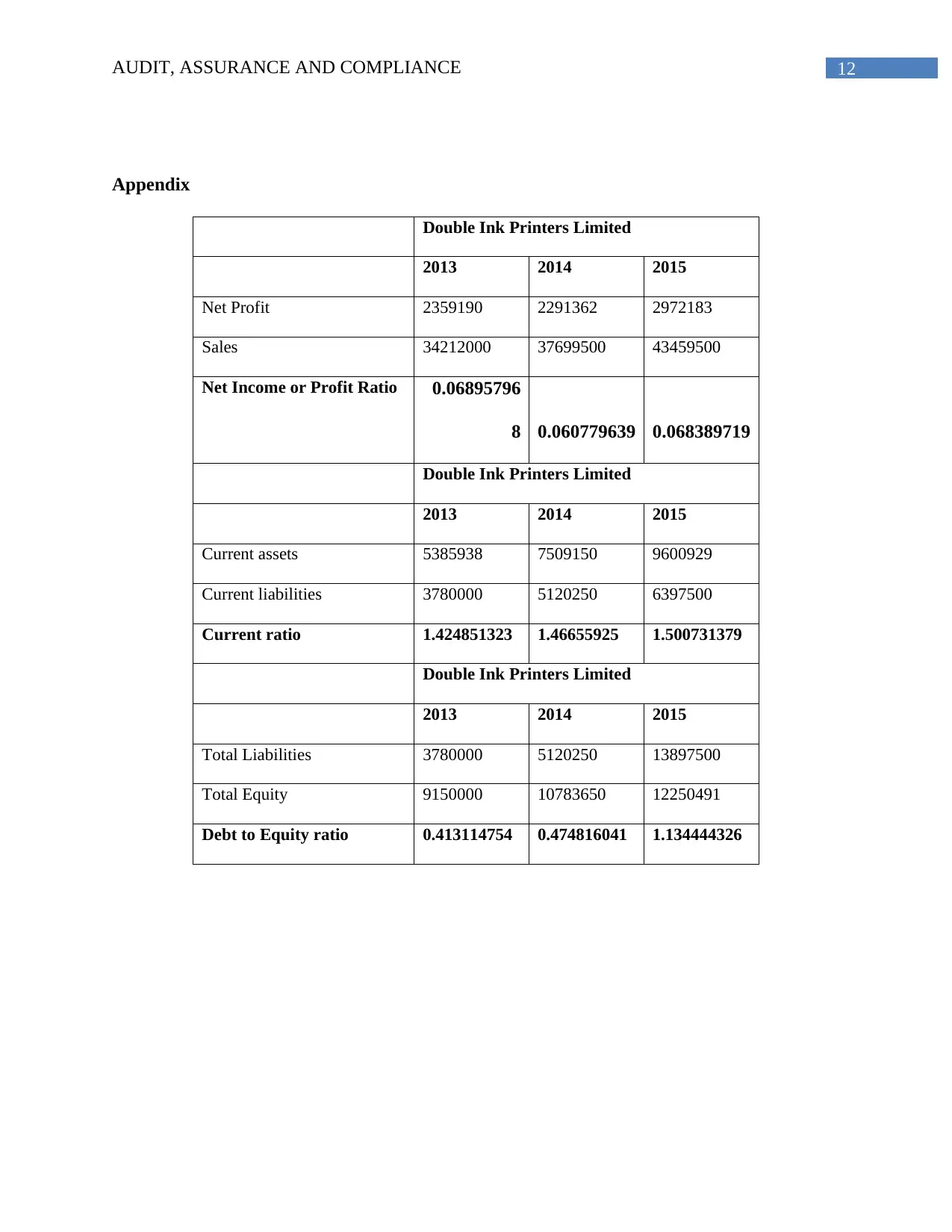

Calculation of financial ratios (Please refer to Appendix)

Analytical approach can be used by the auditor for analyzing the results that get

influenced by audit planning function (Srivastava, Rao & Mock, 2013). In addition, ratio

analysis is a tool that renders information and depicts the financial position of Business

Corporation. The case study on the company DIPL shows profitability ratio, liquidity ratio and

solvency ratio that need to be found out by the auditor. The profitability ratio of DIPL for three

consecutive years are 0.068 (2013), 0.060 (2014) and 0.068 (2015). The current ratio of DIPL for

three consecutive years are 1.42 (2013), 1.46 (2014) and 1.50 (2015). Furthermore, the

profitability ratio is one of the ratios that assist auditor while making comparison between net

income earned and net sales (William, Glover & Prawitt, 2016).

It becomes essential to evaluate the financial health of DIPL and this is possible by

identifying favorable and unfavorable changes through use of ratio analysis as a point of

reference. Furthermore, the solvency ratio of DIPL for three consecutive years are 0.41 (2013),

0.47 (2014) and 1.13 (2015). Auditor need to compare the ratios for three consecutive years and

auditor to understand the line of items that are mentioned in the financial report for evaluating

activities. In addition, the auditors should have complete detailed information of their client.

Analytical procedure should be used by the auditor for audit planning like benchmarking. There

are various other factor variances that are present in the financial declaration that are deducted

and any deductions identified in the benchmarking process.

Analyzing the results that influences decisions while auditing for Double Ink Printers

limited

Calculation of financial ratios (Please refer to Appendix)

Analytical approach can be used by the auditor for analyzing the results that get

influenced by audit planning function (Srivastava, Rao & Mock, 2013). In addition, ratio

analysis is a tool that renders information and depicts the financial position of Business

Corporation. The case study on the company DIPL shows profitability ratio, liquidity ratio and

solvency ratio that need to be found out by the auditor. The profitability ratio of DIPL for three

consecutive years are 0.068 (2013), 0.060 (2014) and 0.068 (2015). The current ratio of DIPL for

three consecutive years are 1.42 (2013), 1.46 (2014) and 1.50 (2015). Furthermore, the

profitability ratio is one of the ratios that assist auditor while making comparison between net

income earned and net sales (William, Glover & Prawitt, 2016).

It becomes essential to evaluate the financial health of DIPL and this is possible by

identifying favorable and unfavorable changes through use of ratio analysis as a point of

reference. Furthermore, the solvency ratio of DIPL for three consecutive years are 0.41 (2013),

0.47 (2014) and 1.13 (2015). Auditor need to compare the ratios for three consecutive years and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDIT, ASSURANCE AND COMPLIANCE

then interpret the information for determining the capacity of business on the fact on whether the

business can meet short-term or long-term obligations. Using ratio analysis help in establishing a

benchmarking that maintains relationship between an accounts as well as financial statement that

can be either financial or non-financial by nature

There are various factors identified that need to be analyzed as it help in generating

profits for DIPL at any of the given favorable conditions (Soh & Martinov-Bennie, 2015). It is

essential for identifying the material difference as mentioned in the ratio analysis interpretation.

Question 2

Classification of inherent risk from the nature of business operations of Double Ink

Printers limited

In this particular question, it is needed to identify the inherent risk that is faced by Double

Ink Printers Limited (Simnett, Carson & Vanstraelen, 2016). The material misstated figures are

present in the financial declarations that need to be evaluated by an auditor at the time of

undertaking audit function. The financial statement depicts the overall financial health of

Business Corporation where it identifies systematic risks and unsystematic risks. Hence,

financial statement shows true and fair view where risk need to be identified that can be either

financial or non-financial by nature (William, Glover & Prawitt, 2016).

From the specific case study on Double Ink Printers Limited, it is noted that it becomes

essential for determining the transactions that are omitted or misinterpreted by the business

management (Sierra, Zorio & García‐Benau, 2013). On analysis, it is noted that there was

then interpret the information for determining the capacity of business on the fact on whether the

business can meet short-term or long-term obligations. Using ratio analysis help in establishing a

benchmarking that maintains relationship between an accounts as well as financial statement that

can be either financial or non-financial by nature

There are various factors identified that need to be analyzed as it help in generating

profits for DIPL at any of the given favorable conditions (Soh & Martinov-Bennie, 2015). It is

essential for identifying the material difference as mentioned in the ratio analysis interpretation.

Question 2

Classification of inherent risk from the nature of business operations of Double Ink

Printers limited

In this particular question, it is needed to identify the inherent risk that is faced by Double

Ink Printers Limited (Simnett, Carson & Vanstraelen, 2016). The material misstated figures are

present in the financial declarations that need to be evaluated by an auditor at the time of

undertaking audit function. The financial statement depicts the overall financial health of

Business Corporation where it identifies systematic risks and unsystematic risks. Hence,

financial statement shows true and fair view where risk need to be identified that can be either

financial or non-financial by nature (William, Glover & Prawitt, 2016).

From the specific case study on Double Ink Printers Limited, it is noted that it becomes

essential for determining the transactions that are omitted or misinterpreted by the business

management (Sierra, Zorio & García‐Benau, 2013). On analysis, it is noted that there was

6AUDIT, ASSURANCE AND COMPLIANCE

ineffective planning in both sales and marketing that lead to inconsistencies. It is an important

thing to analyze the financial declaration for the company that favors business management as

well as adjusted to the functionalities and that can be achieved at certain level of revenue for

maintaining at desirable profit.

On analysis, it is found that there are various categories of factors that lead to inherent

risk. Companies may face material misstatement due to falsification of various items and

external factors that deals with present working conditions (William, Glover & Prawitt, 2016).

Inherent risk directly link with the environmental factor as well as composed of shortage

of sufficient capital requirements. The reason for this risk is issues relating to valuation of stock

and existence of inflexible competition in the present competitive markets. Inherent risk

considered as one risk that addresses misstated figures that need to be reduced by Business

Corporation. DIPL faced inherent risk that need to be escalated by the workers who are presently

working for the Business Corporation (Louwers et al., 2015).

It is important to consider the fact that there had been considerable escalations present for

the company who faced inherent risks that lead to lack of experience and proficiency of workers

that mainly work for the Business Corporation. Companies should recruit experienced staff

members and employees who work for the company and be productive at the same time. Inherent

risk links with the business firm performance and enhanced if they have non-proficient workers

as they mainly make mistakes that are not acceptable all the time (Kend, Houghton & Jubb,

2014). Business Corporation faces material misstatement in the financial statement analysis that

give rise to error or exclusion that are mainly committed by the employees who work for the

company.

ineffective planning in both sales and marketing that lead to inconsistencies. It is an important

thing to analyze the financial declaration for the company that favors business management as

well as adjusted to the functionalities and that can be achieved at certain level of revenue for

maintaining at desirable profit.

On analysis, it is found that there are various categories of factors that lead to inherent

risk. Companies may face material misstatement due to falsification of various items and

external factors that deals with present working conditions (William, Glover & Prawitt, 2016).

Inherent risk directly link with the environmental factor as well as composed of shortage

of sufficient capital requirements. The reason for this risk is issues relating to valuation of stock

and existence of inflexible competition in the present competitive markets. Inherent risk

considered as one risk that addresses misstated figures that need to be reduced by Business

Corporation. DIPL faced inherent risk that need to be escalated by the workers who are presently

working for the Business Corporation (Louwers et al., 2015).

It is important to consider the fact that there had been considerable escalations present for

the company who faced inherent risks that lead to lack of experience and proficiency of workers

that mainly work for the Business Corporation. Companies should recruit experienced staff

members and employees who work for the company and be productive at the same time. Inherent

risk links with the business firm performance and enhanced if they have non-proficient workers

as they mainly make mistakes that are not acceptable all the time (Kend, Houghton & Jubb,

2014). Business Corporation faces material misstatement in the financial statement analysis that

give rise to error or exclusion that are mainly committed by the employees who work for the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDIT, ASSURANCE AND COMPLIANCE

There is different issue that takes place due to novel IT system. The company was not

having access to sufficient staff members who actually handle the reconciliation and execution of

installation that aligns with the testing system. Furthermore, the initial testing should be carried

that was not accurate and proper in given transactions that are taken by the business enterprise.

There are different omission present and mentioned in the financial declaration due to inherent

risk and lead to material misstatements (William, Glover & Prawitt, 2016).

The inherent risk faced by DIPL takes place due to success of CEO as they used to follow

complex procedure. Candidates who are there for the post of CEO need to handle the decision-

making process. The process of CEO successes mainly comes from identified inherent risks and

risk that are related while handling the process or quality procedure. It is important to note the

factor that lead to developing inherent risks due to selected procedure that delays in the process

and does not comply with the strategy and departing the candidates who actually left the

company (Junior, Best & Cotter, 2014).

There are different factors where the company faces inherent risk such as recording of

cash receipts by the financial professional. It is the job role of accounting professional need to

maintain proper bank reconciliation statement and proper recording of accounts and registering

the accounts receivable. It is important to record the process of transactions that are complex and

give rise to diverse inherent risk. It starts from book reprinting and e-book revenue generation in

an effective way (Hayes, Wallage & Gortemaker, 2014).

There is different issue that takes place due to novel IT system. The company was not

having access to sufficient staff members who actually handle the reconciliation and execution of

installation that aligns with the testing system. Furthermore, the initial testing should be carried

that was not accurate and proper in given transactions that are taken by the business enterprise.

There are different omission present and mentioned in the financial declaration due to inherent

risk and lead to material misstatements (William, Glover & Prawitt, 2016).

The inherent risk faced by DIPL takes place due to success of CEO as they used to follow

complex procedure. Candidates who are there for the post of CEO need to handle the decision-

making process. The process of CEO successes mainly comes from identified inherent risks and

risk that are related while handling the process or quality procedure. It is important to note the

factor that lead to developing inherent risks due to selected procedure that delays in the process

and does not comply with the strategy and departing the candidates who actually left the

company (Junior, Best & Cotter, 2014).

There are different factors where the company faces inherent risk such as recording of

cash receipts by the financial professional. It is the job role of accounting professional need to

maintain proper bank reconciliation statement and proper recording of accounts and registering

the accounts receivable. It is important to record the process of transactions that are complex and

give rise to diverse inherent risk. It starts from book reprinting and e-book revenue generation in

an effective way (Hayes, Wallage & Gortemaker, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDIT, ASSURANCE AND COMPLIANCE

Question 3

Classifying the fraud risk that arise from fraudulent activities and related to material

misstatement of the company

Any business or an operating entity can face considerable loss in their assets that take

place because of fraudulent activities. Fraud in business is common factor and there is different

reason to those fraudulent activities like worker dissatisfaction when they had to work with

excessive pressure from the management. It is a common fact where business faces high fraud

risk due to management and pressure on investors that lead to financial outcomes for attainment

of future goals or objectives at specific target (Eilifsen et al., 2013).

Double Ink Printers Limited is a company that had faced fraud risk and the reason for this

risk was operational activities of the company where workers were instigated to engage in

fraudulent activities due to high level of dissatisfaction. The use of novel accounting system will

lead to excessive workload and work pressure who are working for the company (Cohen &

Simnett, 2014). At Double Ink Printers Limited, there are various fraudulent activities that take

place due to creation of excessive pressure on employees who actually carry out the installation

process of novel IT system. The reason for fraudulent activities in company is mainly because of

the situation when employees start with improper handling of reconciliation process that results

in material misstatement figures. From the case study on Double Ink Printers Limited, it is noted

that there have been improper allocation of resources that deals with inappropriate handling

process for executing information technology for the accounting system in the most appropriate

way (Arens et al., 2016).

Question 3

Classifying the fraud risk that arise from fraudulent activities and related to material

misstatement of the company

Any business or an operating entity can face considerable loss in their assets that take

place because of fraudulent activities. Fraud in business is common factor and there is different

reason to those fraudulent activities like worker dissatisfaction when they had to work with

excessive pressure from the management. It is a common fact where business faces high fraud

risk due to management and pressure on investors that lead to financial outcomes for attainment

of future goals or objectives at specific target (Eilifsen et al., 2013).

Double Ink Printers Limited is a company that had faced fraud risk and the reason for this

risk was operational activities of the company where workers were instigated to engage in

fraudulent activities due to high level of dissatisfaction. The use of novel accounting system will

lead to excessive workload and work pressure who are working for the company (Cohen &

Simnett, 2014). At Double Ink Printers Limited, there are various fraudulent activities that take

place due to creation of excessive pressure on employees who actually carry out the installation

process of novel IT system. The reason for fraudulent activities in company is mainly because of

the situation when employees start with improper handling of reconciliation process that results

in material misstatement figures. From the case study on Double Ink Printers Limited, it is noted

that there have been improper allocation of resources that deals with inappropriate handling

process for executing information technology for the accounting system in the most appropriate

way (Arens et al., 2016).

9AUDIT, ASSURANCE AND COMPLIANCE

In the financial statement of any company, risk is mentioned and it is one of the fraud

risks that are faced by Double Ink Printers Limited. DIPL had witnessed increased revenue from

the year 2013 to 2015. The company had increase in net profit margin and gross profit margin.

Risk is actually mentioned in the financial statement as well as reported as one of the fraud risk

faced by the company (Arens et al., 2015). DIPL has acquired a loan amount of 7.5 million from

BDO Finance. It is all about acquisition of loan that was made on agreement where DIPL should

maintain debt ratio that should be lower than current ratio of 1.5. The company was under

pressure as they had to main the financial ratio as decided by the credit lending organization

when they go for opting acquisition of credit. There are different factor that enhances the

company for making improper reflection for checking the financial status when they start

involving in fraudulent activities (William, Glover & Prawitt, 2016).

Impact of the identified risk factors at the time of conducting audit

It is the responsibility of the auditor to first identify the risk that takes place while

implementing novel IT accounting system for monitoring the activities at different phases. The

raw materials of DIPL need to be audited by the auditor. The limitation that are found in the

audit report is cost of paper was higher than their average cost (Becker, Stead & Stead, 2016).

The auditor are responsible for carrying out audit function by accessing information from

financial statement of Double Ink Printers Limited after monitoring the mechanisms on regular

basis. Therefore the auditor needs to detect the risk so that there is smooth functioning of

business enterprise.

In the financial statement of any company, risk is mentioned and it is one of the fraud

risks that are faced by Double Ink Printers Limited. DIPL had witnessed increased revenue from

the year 2013 to 2015. The company had increase in net profit margin and gross profit margin.

Risk is actually mentioned in the financial statement as well as reported as one of the fraud risk

faced by the company (Arens et al., 2015). DIPL has acquired a loan amount of 7.5 million from

BDO Finance. It is all about acquisition of loan that was made on agreement where DIPL should

maintain debt ratio that should be lower than current ratio of 1.5. The company was under

pressure as they had to main the financial ratio as decided by the credit lending organization

when they go for opting acquisition of credit. There are different factor that enhances the

company for making improper reflection for checking the financial status when they start

involving in fraudulent activities (William, Glover & Prawitt, 2016).

Impact of the identified risk factors at the time of conducting audit

It is the responsibility of the auditor to first identify the risk that takes place while

implementing novel IT accounting system for monitoring the activities at different phases. The

raw materials of DIPL need to be audited by the auditor. The limitation that are found in the

audit report is cost of paper was higher than their average cost (Becker, Stead & Stead, 2016).

The auditor are responsible for carrying out audit function by accessing information from

financial statement of Double Ink Printers Limited after monitoring the mechanisms on regular

basis. Therefore the auditor needs to detect the risk so that there is smooth functioning of

business enterprise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10AUDIT, ASSURANCE AND COMPLIANCE

Reference List

Arens, A. A., Elder, R. J., Beasley, M. S., & Hogan, C. E. (2016). Auditing and assurance

services. Pearson.

Arens, A. A., Elder, R. J., Beasley, M. S., & Jones, J. (2015). Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Becker, L. L., Stead, J. G., & Stead, W. E. (2016). Sustainability Assurance: A Strategic

Opportunity for CPA Firms. Management Accounting Quarterly, 17(3), 29.

Cohen, J. R., & Simnett, R. (2014). CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), 59-74.

Eilifsen, A., Messier, W. F., Glover, S. M., & Prawitt, D. F. (2013). Auditing and assurance

services. McGraw-Hill.

Hayes, R., Wallage, P., & Gortemaker, H. (2014). Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Junior, R. M., Best, P. J., & Cotter, J. (2014). Sustainability reporting and assurance: A historical

analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), 1-11.

Kend, M., Houghton, K. A., & Jubb, C. (2014). Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4),

313-320.

Reference List

Arens, A. A., Elder, R. J., Beasley, M. S., & Hogan, C. E. (2016). Auditing and assurance

services. Pearson.

Arens, A. A., Elder, R. J., Beasley, M. S., & Jones, J. (2015). Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Becker, L. L., Stead, J. G., & Stead, W. E. (2016). Sustainability Assurance: A Strategic

Opportunity for CPA Firms. Management Accounting Quarterly, 17(3), 29.

Cohen, J. R., & Simnett, R. (2014). CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), 59-74.

Eilifsen, A., Messier, W. F., Glover, S. M., & Prawitt, D. F. (2013). Auditing and assurance

services. McGraw-Hill.

Hayes, R., Wallage, P., & Gortemaker, H. (2014). Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Junior, R. M., Best, P. J., & Cotter, J. (2014). Sustainability reporting and assurance: A historical

analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), 1-11.

Kend, M., Houghton, K. A., & Jubb, C. (2014). Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4),

313-320.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11AUDIT, ASSURANCE AND COMPLIANCE

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Sierra, L., Zorio, A., & García‐Benau, M. A. (2013). Sustainable development and assurance of

corporate social responsibility reports published by Ibex‐35 companies. Corporate Social

Responsibility and Environmental Management, 20(6), 359-370.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International Archival Auditing and

Assurance Research: Trends, Methodological Issues, and Opportunities. Auditing: A

Journal of Practice & Theory, 35(3), 1-32.

Soh, D. S., & Martinov-Bennie, N. (2015). Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), 80-111.

Srivastava, R. P., Rao, S. S., & Mock, T. J. (2013). Planning and evaluation of assurance services

for sustainability reporting: An evidential reasoning approach. Journal of Information

Systems, 27(2), 107-126.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Wong, R., & Millington, A. (2014). Corporate social disclosures: a user perspective on

assurance. Accounting, Auditing & Accountability Journal, 27(5), 863-887.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Sierra, L., Zorio, A., & García‐Benau, M. A. (2013). Sustainable development and assurance of

corporate social responsibility reports published by Ibex‐35 companies. Corporate Social

Responsibility and Environmental Management, 20(6), 359-370.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International Archival Auditing and

Assurance Research: Trends, Methodological Issues, and Opportunities. Auditing: A

Journal of Practice & Theory, 35(3), 1-32.

Soh, D. S., & Martinov-Bennie, N. (2015). Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), 80-111.

Srivastava, R. P., Rao, S. S., & Mock, T. J. (2013). Planning and evaluation of assurance services

for sustainability reporting: An evidential reasoning approach. Journal of Information

Systems, 27(2), 107-126.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Wong, R., & Millington, A. (2014). Corporate social disclosures: a user perspective on

assurance. Accounting, Auditing & Accountability Journal, 27(5), 863-887.

12AUDIT, ASSURANCE AND COMPLIANCE

Appendix

Double Ink Printers Limited

2013 2014 2015

Net Profit 2359190 2291362 2972183

Sales 34212000 37699500 43459500

Net Income or Profit Ratio 0.06895796

8 0.060779639 0.068389719

Double Ink Printers Limited

2013 2014 2015

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

Current ratio 1.424851323 1.46655925 1.500731379

Double Ink Printers Limited

2013 2014 2015

Total Liabilities 3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to Equity ratio 0.413114754 0.474816041 1.134444326

Appendix

Double Ink Printers Limited

2013 2014 2015

Net Profit 2359190 2291362 2972183

Sales 34212000 37699500 43459500

Net Income or Profit Ratio 0.06895796

8 0.060779639 0.068389719

Double Ink Printers Limited

2013 2014 2015

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

Current ratio 1.424851323 1.46655925 1.500731379

Double Ink Printers Limited

2013 2014 2015

Total Liabilities 3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to Equity ratio 0.413114754 0.474816041 1.134444326

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.