Audit Report on Enhanced Auditor Reporting for ASX Listed Companies

VerifiedAdded on 2023/06/07

|13

|3189

|398

Report

AI Summary

This report examines the compliance of Ainsworth Game Technology Limited, an Australian Stock Exchange (ASX) listed company, with the enhanced auditor reporting requirements introduced in 2016. The analysis covers key aspects such as auditor independence declarations, the independent auditor's report, non-audit services performed, auditor remuneration, the role of the audit committee, reporting to shareholders, and key audit matters. The report delves into the specifics of how Ainsworth has addressed these requirements, referencing relevant legislation like the Corporations Act 2001 and ethical codes. It discusses the auditor's opinion on the financial statements, the types of non-audit services provided, and the impact of remuneration changes. Furthermore, it highlights the key audit matters identified by the auditors, including revenue recognition, recoverability of trade receivables, and the carrying value of goodwill and intangible assets, providing insights into the audit procedures applied. The report concludes with an assessment of the extent to which Ainsworth has embraced the enhanced reporting standards and the implications for stakeholders.

Audit Assurance and Compliance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The objective of this assignment is to evaluate whether the companies which are listed on the

stock exchange of Australia are complying with the new enhanced audit reporting requirements

or not. The company chosen for this purpose is Ainsworth Game Technology Limited, which

provides gaming solutions across the world.

The report analyses the extent to which enhanced audit reporting requirements have been

fulfilled such as independence of auditors and declaration of independence, types of non-audit

services provided, reporting to shareholders and reporting of key audit matters.

2

The objective of this assignment is to evaluate whether the companies which are listed on the

stock exchange of Australia are complying with the new enhanced audit reporting requirements

or not. The company chosen for this purpose is Ainsworth Game Technology Limited, which

provides gaming solutions across the world.

The report analyses the extent to which enhanced audit reporting requirements have been

fulfilled such as independence of auditors and declaration of independence, types of non-audit

services provided, reporting to shareholders and reporting of key audit matters.

2

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Background of the Report............................................................................................................4

Scope of the Project.....................................................................................................................4

Discussion........................................................................................................................................5

1) Auditor’s Independence Declaration................................................................................5

2) Independent auditor’s report.............................................................................................6

3) Non-Audit services performed by the Auditor.................................................................6

4) Auditors’ remuneration.....................................................................................................7

5) Role, functions and composition of the Audit Committee................................................8

6) Independent Auditors report to the members (shareholders)............................................9

7) Review all Key Audit Matters noted and the associated audit procedures.......................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Background of the Report............................................................................................................4

Scope of the Project.....................................................................................................................4

Discussion........................................................................................................................................5

1) Auditor’s Independence Declaration................................................................................5

2) Independent auditor’s report.............................................................................................6

3) Non-Audit services performed by the Auditor.................................................................6

4) Auditors’ remuneration.....................................................................................................7

5) Role, functions and composition of the Audit Committee................................................8

6) Independent Auditors report to the members (shareholders)............................................9

7) Review all Key Audit Matters noted and the associated audit procedures.......................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Background of the Report

The report is prepared to review and analyze the manner in which the companies listed on ASX

(Australian Stock Exchange) are complying with the Enhanced Auditor Reporting commenced in

the year 2016. For the purposes of this report, Ainsworth Game Technology Limited has been

selected, as it is listed on the stock exchange in Australia. It is a gaming solutions company.

Scope of the Project

The report is prepared with an objective to evaluate the implications of Enhanced Auditor

Reporting on the auditors, by going through the annual report of the selected company. By

incorporating these reporting standards, the company has ensured a greater amount of

transparency in responsibilities of auditors related to reporting. It will also help in getting

insights about the audit’s key areas and performance of the company in those areas.

The matter of enhanced audit reporting is discussed in this report in seven major headings. Those

matters include independence of auditor’s, independent auditor report, other services by auditor,

auditor’s remuneration, key audit matters, audit committee and reporting to shareholders.

Whether these matters have been mentioned in the audit report of the company or not, have been

discussed in detail. These all are required to be reported as per the new guidelines and audit

standards.

4

Background of the Report

The report is prepared to review and analyze the manner in which the companies listed on ASX

(Australian Stock Exchange) are complying with the Enhanced Auditor Reporting commenced in

the year 2016. For the purposes of this report, Ainsworth Game Technology Limited has been

selected, as it is listed on the stock exchange in Australia. It is a gaming solutions company.

Scope of the Project

The report is prepared with an objective to evaluate the implications of Enhanced Auditor

Reporting on the auditors, by going through the annual report of the selected company. By

incorporating these reporting standards, the company has ensured a greater amount of

transparency in responsibilities of auditors related to reporting. It will also help in getting

insights about the audit’s key areas and performance of the company in those areas.

The matter of enhanced audit reporting is discussed in this report in seven major headings. Those

matters include independence of auditor’s, independent auditor report, other services by auditor,

auditor’s remuneration, key audit matters, audit committee and reporting to shareholders.

Whether these matters have been mentioned in the audit report of the company or not, have been

discussed in detail. These all are required to be reported as per the new guidelines and audit

standards.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Discussion

Ainsworth Game Technology was founded in the year 1995 with an objective to provide people

across the world with innovative and quality gaming solutions. It has its headquarters in

Australia and is listed on ASX. This company is most suitable to study the impact of the changed

auditor reporting requirements and the manner in which such changes in reporting have been

embraced by the auditors of the company. Following are the major points of discussion:

1) Auditor’s Independence Declaration

In Australia, the auditors of the company are governed by the Corporations Act, 2001 (Moroney

et al., 2012). As per the regulations of the act and other regulations, an auditor is required to

work independently from a company in which they are doing the audit (CAANZ (Chartered

Accountants Australia & New Zealand), 2016). There are many requirements that an auditor is

supposed to follow under many laws and regulations. Requirements are detailed as under:

As per section 307C of the Corporations Act, 2001, an auditor is supposed to give a

declaration of his independence from the entity which is known as Auditor’s

Independence Declaration (Australian Government, 2001). Apart from section 307C, the

auditor must also follow Divisions 3, 4 and 5 of Part 2M.4 of the Corporations Act, 2011

(Wolters Kluwer, 2018; Tomasic et al., 2002).

Auditors are also required to follow certain Code of Ethics formulated for professionals

provided under APEC 110 (Campbell & Houghton, 2005). For enhancing the quality of

the report, the Australian regulating authorities came forward with this regulation on

ethics. Now, the auditors are required to report on the ethical matters that are related to

the audit along with other ethical responsibilities, in addition to independence declaration

(Chartered Accountants (Australia-Newzealand), 2018).

5

Ainsworth Game Technology was founded in the year 1995 with an objective to provide people

across the world with innovative and quality gaming solutions. It has its headquarters in

Australia and is listed on ASX. This company is most suitable to study the impact of the changed

auditor reporting requirements and the manner in which such changes in reporting have been

embraced by the auditors of the company. Following are the major points of discussion:

1) Auditor’s Independence Declaration

In Australia, the auditors of the company are governed by the Corporations Act, 2001 (Moroney

et al., 2012). As per the regulations of the act and other regulations, an auditor is required to

work independently from a company in which they are doing the audit (CAANZ (Chartered

Accountants Australia & New Zealand), 2016). There are many requirements that an auditor is

supposed to follow under many laws and regulations. Requirements are detailed as under:

As per section 307C of the Corporations Act, 2001, an auditor is supposed to give a

declaration of his independence from the entity which is known as Auditor’s

Independence Declaration (Australian Government, 2001). Apart from section 307C, the

auditor must also follow Divisions 3, 4 and 5 of Part 2M.4 of the Corporations Act, 2011

(Wolters Kluwer, 2018; Tomasic et al., 2002).

Auditors are also required to follow certain Code of Ethics formulated for professionals

provided under APEC 110 (Campbell & Houghton, 2005). For enhancing the quality of

the report, the Australian regulating authorities came forward with this regulation on

ethics. Now, the auditors are required to report on the ethical matters that are related to

the audit along with other ethical responsibilities, in addition to independence declaration

(Chartered Accountants (Australia-Newzealand), 2018).

5

The auditors of Ainsworth Game Technology Limited have provided the declaration as per the

requirements of Corporations Act, 2001. The auditor’s report also specifies that they have

followed the ethical code of conduct as issued by the Accounting Professional & Ethical

Standards Board and, fulfilled all their ethical responsibilities (Ainsworth Game Technology

Limited, 2017). However, this information did not form the part of the declaration of

independence by auditor. Instead, it was mentioned in Independent auditor’s report.

2) Independent auditor’s report

An auditor is required to express his opinion on the financial statements of a company which has

appointed him as the auditor. There are different types of opinions that an auditor can express.

These opinions are unqualified opinion, qualified opinion, adverse opinion and giving a

disclaimer of opinion (Leung, 2009). The auditors of Ainsworth Game Technology Limited have

evaluated the financial statements of the year 2017 and opined that the company has diligently

followed the regulations and provisions of Corporations Act 2001 and hence, it is an unqualified

opinion.

3) Non-Audit services performed by the Auditor

One of the major causes that can hamper an auditor’s independence is the non- audit (or non-

assurance) services provided by him in addition to the statutory audits. There are a number of

aspects of independence of an auditor, one of which is the relationship between the client and

auditor (Houghton et al., 2010). Hence, it is essential for him to exercise significant judgment

prior to taking up any non-audit services in addition to the audit and determine in advance

whether such service is a threat to independence or not (Frankel, 2018). In the United States of

America, the provision of providing non-audit services by the same firm which is performing the

6

requirements of Corporations Act, 2001. The auditor’s report also specifies that they have

followed the ethical code of conduct as issued by the Accounting Professional & Ethical

Standards Board and, fulfilled all their ethical responsibilities (Ainsworth Game Technology

Limited, 2017). However, this information did not form the part of the declaration of

independence by auditor. Instead, it was mentioned in Independent auditor’s report.

2) Independent auditor’s report

An auditor is required to express his opinion on the financial statements of a company which has

appointed him as the auditor. There are different types of opinions that an auditor can express.

These opinions are unqualified opinion, qualified opinion, adverse opinion and giving a

disclaimer of opinion (Leung, 2009). The auditors of Ainsworth Game Technology Limited have

evaluated the financial statements of the year 2017 and opined that the company has diligently

followed the regulations and provisions of Corporations Act 2001 and hence, it is an unqualified

opinion.

3) Non-Audit services performed by the Auditor

One of the major causes that can hamper an auditor’s independence is the non- audit (or non-

assurance) services provided by him in addition to the statutory audits. There are a number of

aspects of independence of an auditor, one of which is the relationship between the client and

auditor (Houghton et al., 2010). Hence, it is essential for him to exercise significant judgment

prior to taking up any non-audit services in addition to the audit and determine in advance

whether such service is a threat to independence or not (Frankel, 2018). In the United States of

America, the provision of providing non-audit services by the same firm which is performing the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

audit for that client has been restricted by the Sarbanes Oxley Act. However, in Australia, these

services can still be provided along with audit services (Mitchell, 2018).

Various regulations have been brought in place regarding the provision of non- audit services by

the auditors of the company which involves, giving a written declaration in the audit report that

non -audit services have also been provided (Malaysian Accountancy Research and Education

Foundation, 2007). In case any situation arises which leads to conflict of interest, the auditors

must inform the authorities within the time specified.

As per the annual report of the company, the auditors have undertaken certain other services for

it, apart from the audit services. However, they have given the declaration that such services did

not impact the independence of the auditor. They also stated in the report that they have followed

the code of ethics issued by the relevant authority. In a separate section by the name Non- Audit

Services, they have mentioned the type of services they have performed as non- audit services.

The services provided by them include transaction support services and other regulatory audit

services (Ainsworth Game Technology Limited, 2017). Nature of such services is transaction

advisory and compliance services. Such services might have an impact on auditor’s

independence but a declaration has been provided by the auditors.

4) Auditors’ remuneration

The auditors of the company are given remuneration for the audit services provided by them to

the company. However, in Australia, the auditors are also permitted to perform non- audit

services such as assistance in accounting and investigation services related to due diligence

(Caanz (Chartered Accountants Australia & New Zealand), 2015).

The auditors of the Ainsworth Game Technology Limited performed both audit as well as non-

audit services for the company. Their remuneration is given in the table below:

7

services can still be provided along with audit services (Mitchell, 2018).

Various regulations have been brought in place regarding the provision of non- audit services by

the auditors of the company which involves, giving a written declaration in the audit report that

non -audit services have also been provided (Malaysian Accountancy Research and Education

Foundation, 2007). In case any situation arises which leads to conflict of interest, the auditors

must inform the authorities within the time specified.

As per the annual report of the company, the auditors have undertaken certain other services for

it, apart from the audit services. However, they have given the declaration that such services did

not impact the independence of the auditor. They also stated in the report that they have followed

the code of ethics issued by the relevant authority. In a separate section by the name Non- Audit

Services, they have mentioned the type of services they have performed as non- audit services.

The services provided by them include transaction support services and other regulatory audit

services (Ainsworth Game Technology Limited, 2017). Nature of such services is transaction

advisory and compliance services. Such services might have an impact on auditor’s

independence but a declaration has been provided by the auditors.

4) Auditors’ remuneration

The auditors of the company are given remuneration for the audit services provided by them to

the company. However, in Australia, the auditors are also permitted to perform non- audit

services such as assistance in accounting and investigation services related to due diligence

(Caanz (Chartered Accountants Australia & New Zealand), 2015).

The auditors of the Ainsworth Game Technology Limited performed both audit as well as non-

audit services for the company. Their remuneration is given in the table below:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

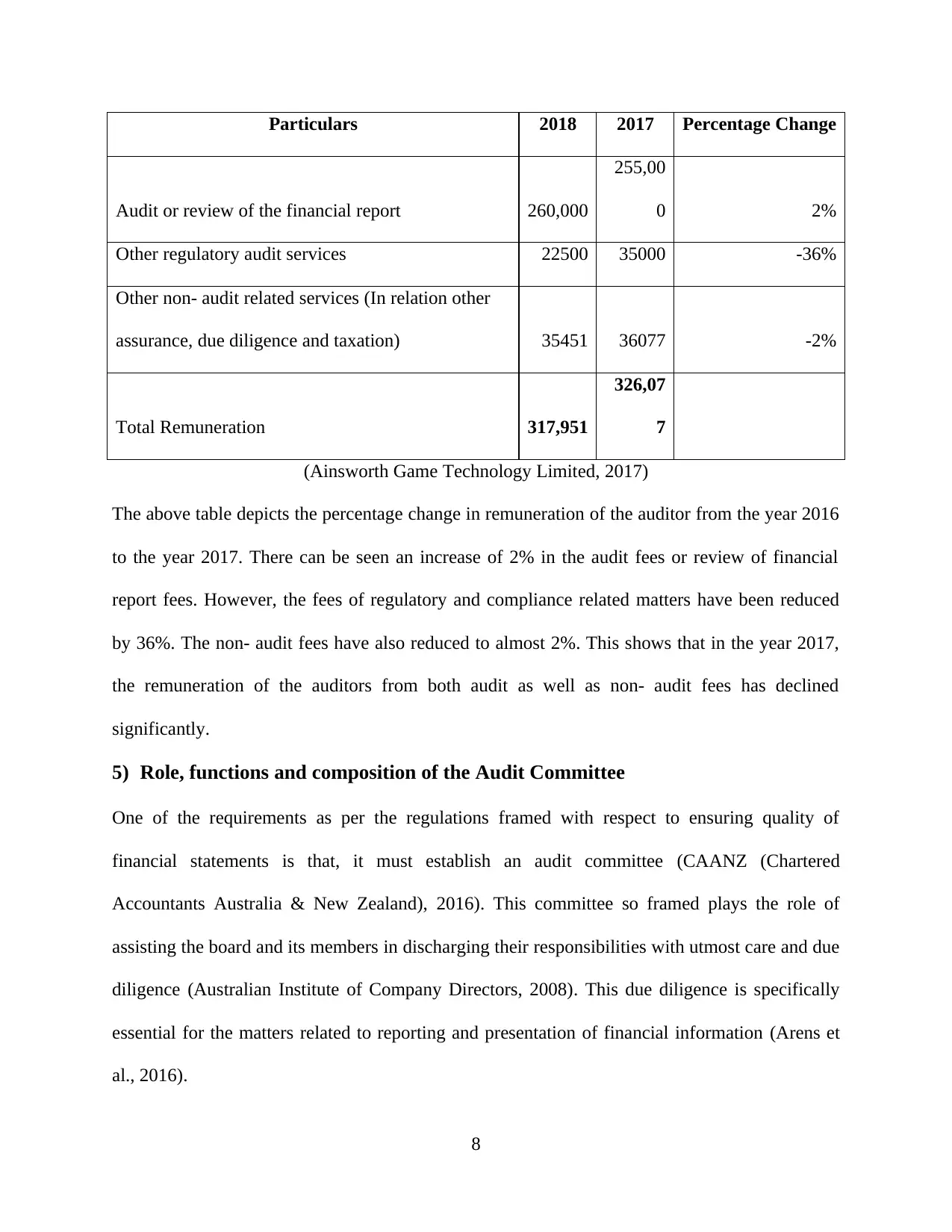

Particulars 2018 2017 Percentage Change

Audit or review of the financial report 260,000

255,00

0 2%

Other regulatory audit services 22500 35000 -36%

Other non- audit related services (In relation other

assurance, due diligence and taxation) 35451 36077 -2%

Total Remuneration 317,951

326,07

7

(Ainsworth Game Technology Limited, 2017)

The above table depicts the percentage change in remuneration of the auditor from the year 2016

to the year 2017. There can be seen an increase of 2% in the audit fees or review of financial

report fees. However, the fees of regulatory and compliance related matters have been reduced

by 36%. The non- audit fees have also reduced to almost 2%. This shows that in the year 2017,

the remuneration of the auditors from both audit as well as non- audit fees has declined

significantly.

5) Role, functions and composition of the Audit Committee

One of the requirements as per the regulations framed with respect to ensuring quality of

financial statements is that, it must establish an audit committee (CAANZ (Chartered

Accountants Australia & New Zealand), 2016). This committee so framed plays the role of

assisting the board and its members in discharging their responsibilities with utmost care and due

diligence (Australian Institute of Company Directors, 2008). This due diligence is specifically

essential for the matters related to reporting and presentation of financial information (Arens et

al., 2016).

8

Audit or review of the financial report 260,000

255,00

0 2%

Other regulatory audit services 22500 35000 -36%

Other non- audit related services (In relation other

assurance, due diligence and taxation) 35451 36077 -2%

Total Remuneration 317,951

326,07

7

(Ainsworth Game Technology Limited, 2017)

The above table depicts the percentage change in remuneration of the auditor from the year 2016

to the year 2017. There can be seen an increase of 2% in the audit fees or review of financial

report fees. However, the fees of regulatory and compliance related matters have been reduced

by 36%. The non- audit fees have also reduced to almost 2%. This shows that in the year 2017,

the remuneration of the auditors from both audit as well as non- audit fees has declined

significantly.

5) Role, functions and composition of the Audit Committee

One of the requirements as per the regulations framed with respect to ensuring quality of

financial statements is that, it must establish an audit committee (CAANZ (Chartered

Accountants Australia & New Zealand), 2016). This committee so framed plays the role of

assisting the board and its members in discharging their responsibilities with utmost care and due

diligence (Australian Institute of Company Directors, 2008). This due diligence is specifically

essential for the matters related to reporting and presentation of financial information (Arens et

al., 2016).

8

Ainsworth Game Technology Limited also has framed an audit committee as per the

requirements of the Corporate Act, 2001 and other regulations. The committee consists of three

non-executive directors who are having the required knowledge and are also financially literate.

The audit committee is responsible for matters related to non-audit services and preparation and

evaluation of risk management framework (Ainsworth Game Technology Limited, 2017).

However, detailed information about audit committee could not be found in report and also was

not available on website.

6) Independent Auditors report to the members (shareholders)

All the companies are required to appoint an auditor so that they express their opinion on the

financial statements prepared by the management (Marks, 2016). Such opinion is framed based

on the findings during the audit. Such findings are reported in a report format to the shareholders

(Gay & Simnett, 2015). The auditors are responsible for the evaluation of the financial

statements and expressing their opinion thereon. On the contrary, management of the company

has the responsibility to prepare the financial statements by choosing sound accounting policies

(Media, 2015).

No subsequent event arose in the company that was having any significant impact on the

company.

7) Review all Key Audit Matters noted and the associated audit procedures

There are some new regulations that have been framed for the purpose of providing assistance to

auditors in reporting. These are termed as Enhanced Auditor Reporting Requirements. This

regulation requires that the auditors must report to the members of the company, regarding the

key audit matters that came to their notice during the audit of the financial statements (Gay &

Simnett, 2018). The key audit matters can be explained as those matters which according to the

9

requirements of the Corporate Act, 2001 and other regulations. The committee consists of three

non-executive directors who are having the required knowledge and are also financially literate.

The audit committee is responsible for matters related to non-audit services and preparation and

evaluation of risk management framework (Ainsworth Game Technology Limited, 2017).

However, detailed information about audit committee could not be found in report and also was

not available on website.

6) Independent Auditors report to the members (shareholders)

All the companies are required to appoint an auditor so that they express their opinion on the

financial statements prepared by the management (Marks, 2016). Such opinion is framed based

on the findings during the audit. Such findings are reported in a report format to the shareholders

(Gay & Simnett, 2015). The auditors are responsible for the evaluation of the financial

statements and expressing their opinion thereon. On the contrary, management of the company

has the responsibility to prepare the financial statements by choosing sound accounting policies

(Media, 2015).

No subsequent event arose in the company that was having any significant impact on the

company.

7) Review all Key Audit Matters noted and the associated audit procedures

There are some new regulations that have been framed for the purpose of providing assistance to

auditors in reporting. These are termed as Enhanced Auditor Reporting Requirements. This

regulation requires that the auditors must report to the members of the company, regarding the

key audit matters that came to their notice during the audit of the financial statements (Gay &

Simnett, 2018). The key audit matters can be explained as those matters which according to the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

auditors were the most significant matters that must be reported in a separate section. Such

matters warrant separate and focused attention by the shareholders before they reach any

conclusion based on audited financial statements. As per the provisions, now, the auditors are

required to report on key audit matters and state the manner in which they approached and

evaluated such matters during the audit.

The auditors of Ainsworth Game Technology Limited reviewed the financial statements and

identified three significant key audit matters. These are as follows:

1. Revenue recognition

2. Recoverability of trade receivables

3. Carrying value of goodwill and intangible assets (Ainsworth Game Technology Limited,

2017).

These matters are summarized as under:

Revenue Recognition - The auditors of the company considered this as the key audit matter

because the company operates globally and has many revenue streams. This required the auditors

to put in a lot of effort to identify the main revenue streams that came from different geographic

locations and such difference in location came with difference in criteria of recognizing

revenues. Also, the auditors had to evaluate such global transactions that include revenues from

gaming royalties, sales of machine parts, revenue from rentals and other revenue streams. This

complexity and difference in revenue recognition criteria required involvement of several senior

members of the audit team to understand the complex transactions.

The auditors of the company applied test of control to evaluate the internal control system

regarding revenue recognition from various streams and test of details of balances to evaluate the

correctness of accounts.

10

matters warrant separate and focused attention by the shareholders before they reach any

conclusion based on audited financial statements. As per the provisions, now, the auditors are

required to report on key audit matters and state the manner in which they approached and

evaluated such matters during the audit.

The auditors of Ainsworth Game Technology Limited reviewed the financial statements and

identified three significant key audit matters. These are as follows:

1. Revenue recognition

2. Recoverability of trade receivables

3. Carrying value of goodwill and intangible assets (Ainsworth Game Technology Limited,

2017).

These matters are summarized as under:

Revenue Recognition - The auditors of the company considered this as the key audit matter

because the company operates globally and has many revenue streams. This required the auditors

to put in a lot of effort to identify the main revenue streams that came from different geographic

locations and such difference in location came with difference in criteria of recognizing

revenues. Also, the auditors had to evaluate such global transactions that include revenues from

gaming royalties, sales of machine parts, revenue from rentals and other revenue streams. This

complexity and difference in revenue recognition criteria required involvement of several senior

members of the audit team to understand the complex transactions.

The auditors of the company applied test of control to evaluate the internal control system

regarding revenue recognition from various streams and test of details of balances to evaluate the

correctness of accounts.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Recoverability of trade receivables - Another matter which was considered a key audit matter by

the auditors was related to recovery of trade receivables. Reason behind this is that owing to the

difference in geographical conditions of operations, the industry practices that are prevailing in

the market differ significantly from place to place. Furthermore, market conditions also differ.

Both of these conditions give rise to increased credit risk exposure and therefore, warranted more

audit focus. The major issue was that there was a difference in the terms of payment across

locations. This required the auditors to exercise a significant amount of judgment and also

scrutinize such transactions closely.

For this key audit matter, the auditors applied test of controls for evaluating the internal control

system applied by the management in such transactions. Also, they assessed the credit risk by

applying test of details of balances. To some extent, substantive procedures were also applied to

understand the pattern of credit risk.

Carrying value of goodwill and intangible assets - This is also considered as a key audit matter

by the auditors of the company, as the matter requires a great deal of judgment while evaluating

the assumptions taken by the management in this regard. The auditors developed a model of their

own to test the effectiveness of the assumptions taken. The models used by the company are

complex in nature and thus, this is a key audit matter.

The auditors applied analytical procedures and test of details of balances to verify the procedures

adopted by the management in this regard.

Conclusion

From the above analysis, it is clear that the auditors have taken utmost care about the regulations

specified in various laws regarding audit quality, independence of auditors and reporting of key

11

the auditors was related to recovery of trade receivables. Reason behind this is that owing to the

difference in geographical conditions of operations, the industry practices that are prevailing in

the market differ significantly from place to place. Furthermore, market conditions also differ.

Both of these conditions give rise to increased credit risk exposure and therefore, warranted more

audit focus. The major issue was that there was a difference in the terms of payment across

locations. This required the auditors to exercise a significant amount of judgment and also

scrutinize such transactions closely.

For this key audit matter, the auditors applied test of controls for evaluating the internal control

system applied by the management in such transactions. Also, they assessed the credit risk by

applying test of details of balances. To some extent, substantive procedures were also applied to

understand the pattern of credit risk.

Carrying value of goodwill and intangible assets - This is also considered as a key audit matter

by the auditors of the company, as the matter requires a great deal of judgment while evaluating

the assumptions taken by the management in this regard. The auditors developed a model of their

own to test the effectiveness of the assumptions taken. The models used by the company are

complex in nature and thus, this is a key audit matter.

The auditors applied analytical procedures and test of details of balances to verify the procedures

adopted by the management in this regard.

Conclusion

From the above analysis, it is clear that the auditors have taken utmost care about the regulations

specified in various laws regarding audit quality, independence of auditors and reporting of key

11

audit matters. However, the information regarding the audit committee formation, roles and

functions is not clearly given by the company. It is not available in the report, neither it is

available on the website. Hence, it is suggested that the company must provide such information

to the members of the company.

References

Ainsworth Game Technology Limited, 2017. Annual Report. Ainsworth Game Technology

Limited.

Arens, A. et al., 2016. Auditing, Assurance Services and Ethics in Australia with ACL Access

Code Card. Pearson Education Australia.

Australian Government, 2001. Corporations Act 2001.

Australian Institute of Company Directors, 2008. Audit Committees: A Guide to Good Practice.

AICD.

Caanz (Chartered Accountants Australia & New Zealand), 2015. Auditing and Assurance

Handbook 2015 New Zealand+auditing and Assurance Handbook 2015 New Zealand Wiley E-

Text Card. John Wiley & Sons Australia, Limited.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

Campbell, T. & Houghton, K.A., 2005. Ethics and Auditing. ANU E Press.

Chartered Accountants (Australia-Newzealand), 2018. Perspective.

Frankel, R.M., 2018. The Relation Between Auditors' Fees for Non-Audit Services and Earnings

Quality (Classic Reprint). Fb&c Limited.

Gay, G.E. & Simnett, R., 2015. Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Gay, G. & Simnett, R., 2018. Auditing and Assurance Services in Australia, Seventh Edition.

McGraw-Hill Education Australia.

Houghton, K.A., Jubb, C., Kend, M. & Ng, J., 2010. The Future of Audit: Keeping Capital

Markets Efficient. ANU E Press.

12

functions is not clearly given by the company. It is not available in the report, neither it is

available on the website. Hence, it is suggested that the company must provide such information

to the members of the company.

References

Ainsworth Game Technology Limited, 2017. Annual Report. Ainsworth Game Technology

Limited.

Arens, A. et al., 2016. Auditing, Assurance Services and Ethics in Australia with ACL Access

Code Card. Pearson Education Australia.

Australian Government, 2001. Corporations Act 2001.

Australian Institute of Company Directors, 2008. Audit Committees: A Guide to Good Practice.

AICD.

Caanz (Chartered Accountants Australia & New Zealand), 2015. Auditing and Assurance

Handbook 2015 New Zealand+auditing and Assurance Handbook 2015 New Zealand Wiley E-

Text Card. John Wiley & Sons Australia, Limited.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

Campbell, T. & Houghton, K.A., 2005. Ethics and Auditing. ANU E Press.

Chartered Accountants (Australia-Newzealand), 2018. Perspective.

Frankel, R.M., 2018. The Relation Between Auditors' Fees for Non-Audit Services and Earnings

Quality (Classic Reprint). Fb&c Limited.

Gay, G.E. & Simnett, R., 2015. Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Gay, G. & Simnett, R., 2018. Auditing and Assurance Services in Australia, Seventh Edition.

McGraw-Hill Education Australia.

Houghton, K.A., Jubb, C., Kend, M. & Ng, J., 2010. The Future of Audit: Keeping Capital

Markets Efficient. ANU E Press.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.