HI6026 Audit, Assurance and Compliance: DIPL Case Study Analysis

VerifiedAdded on 2020/03/04

|10

|2255

|40

Case Study

AI Summary

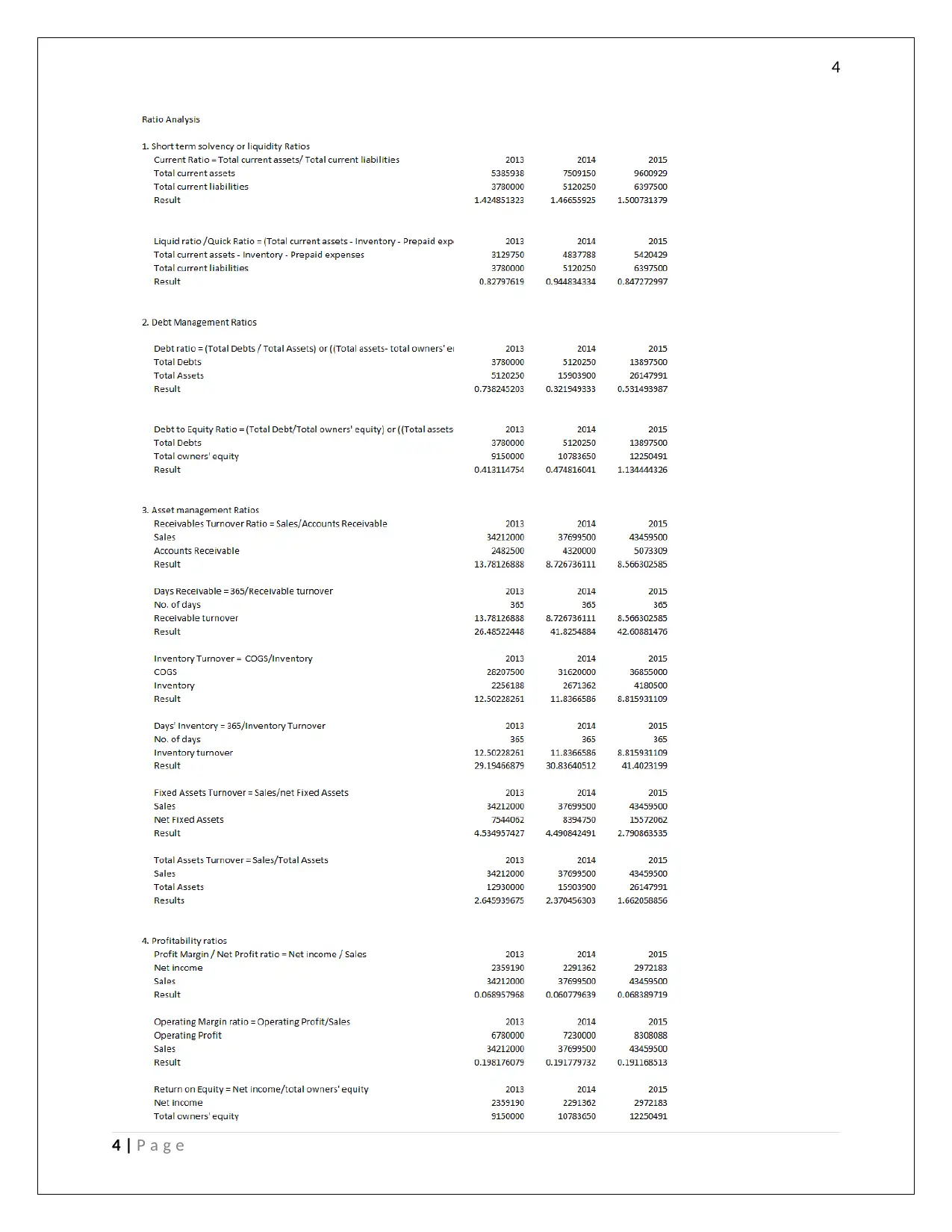

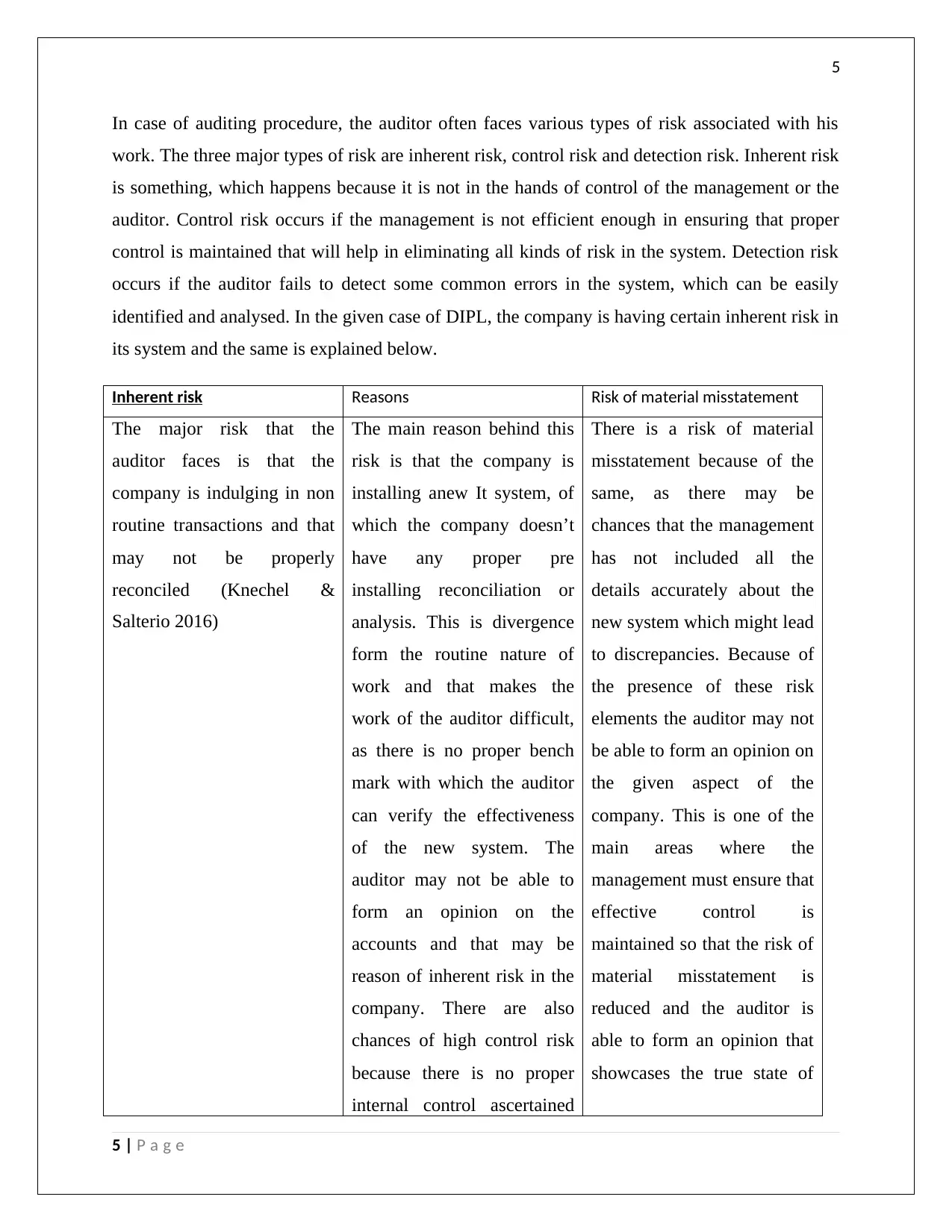

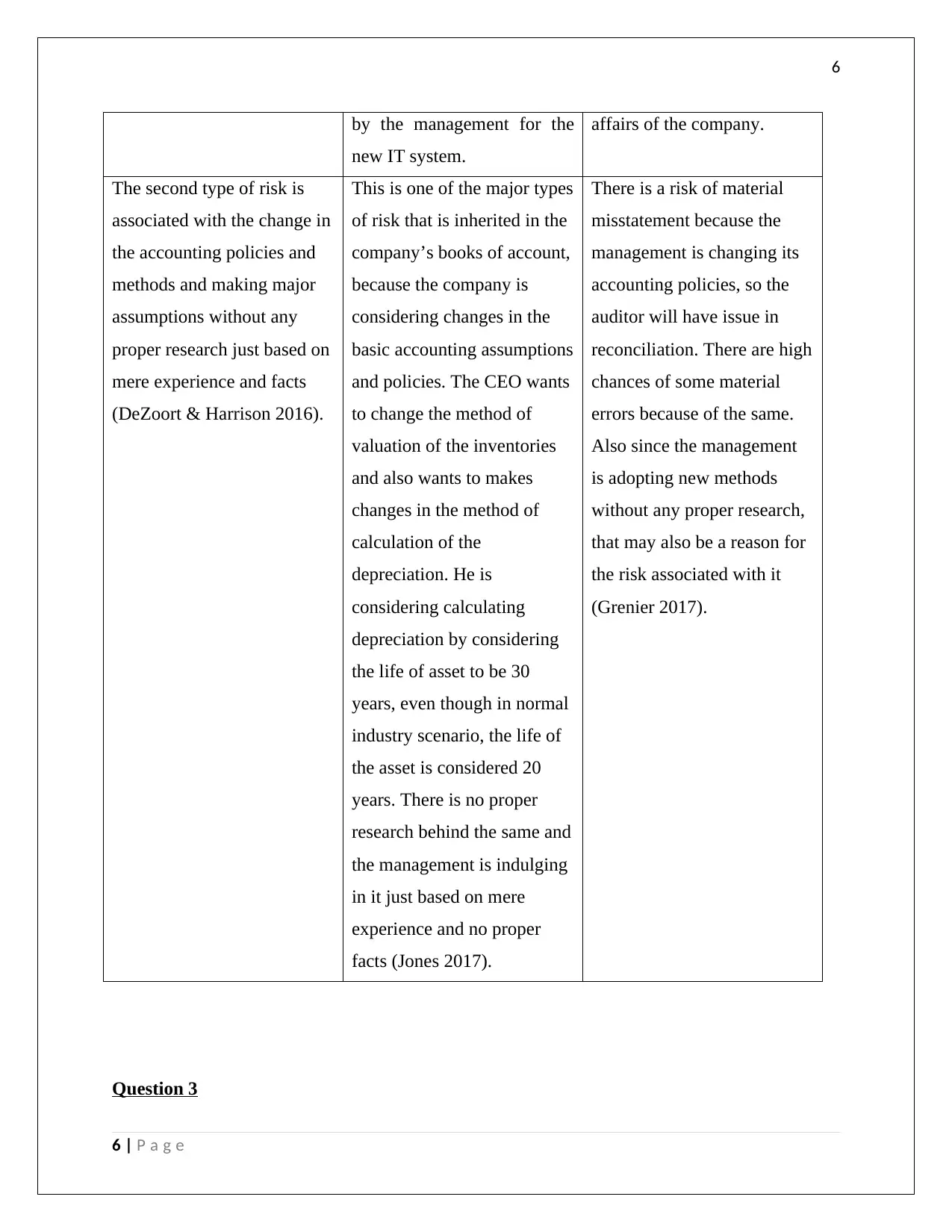

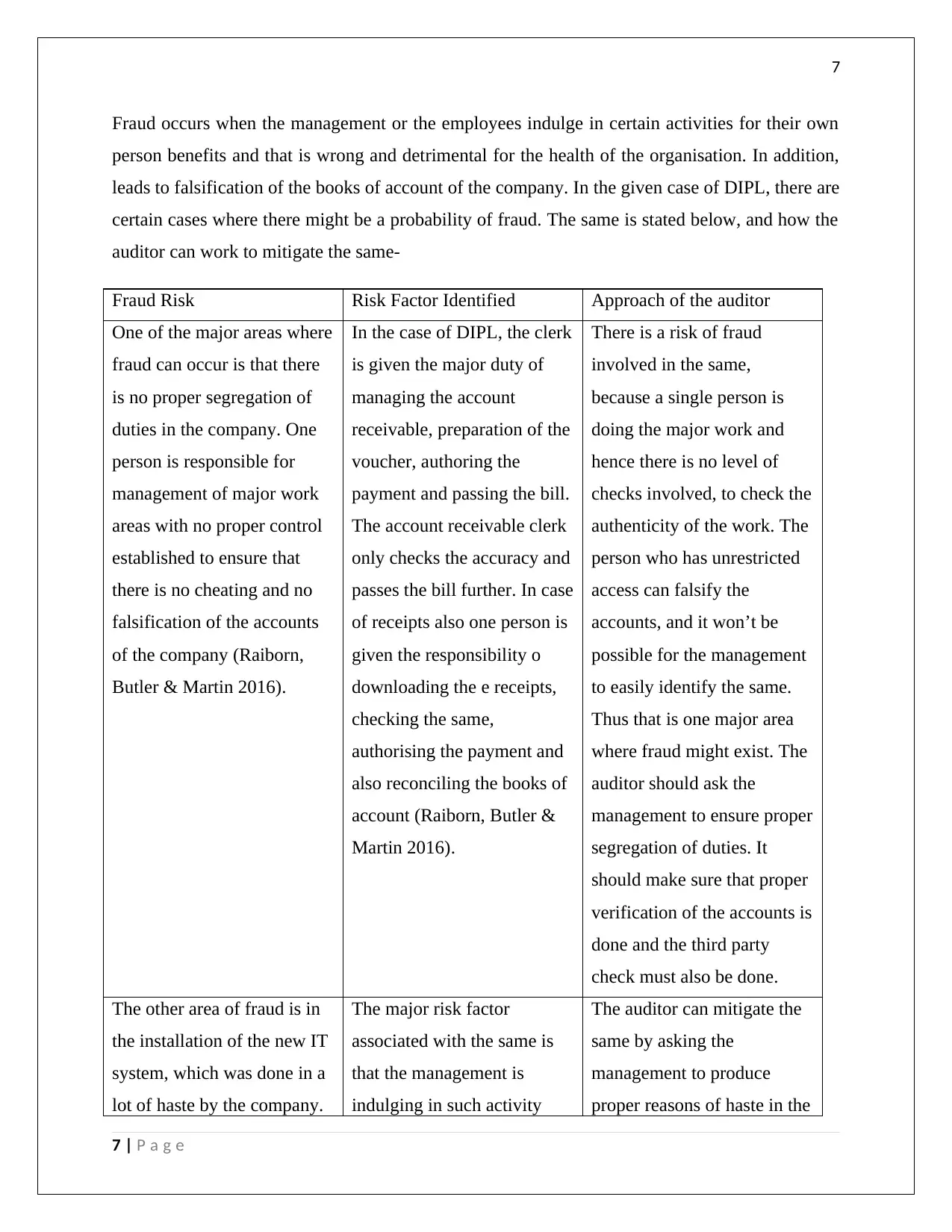

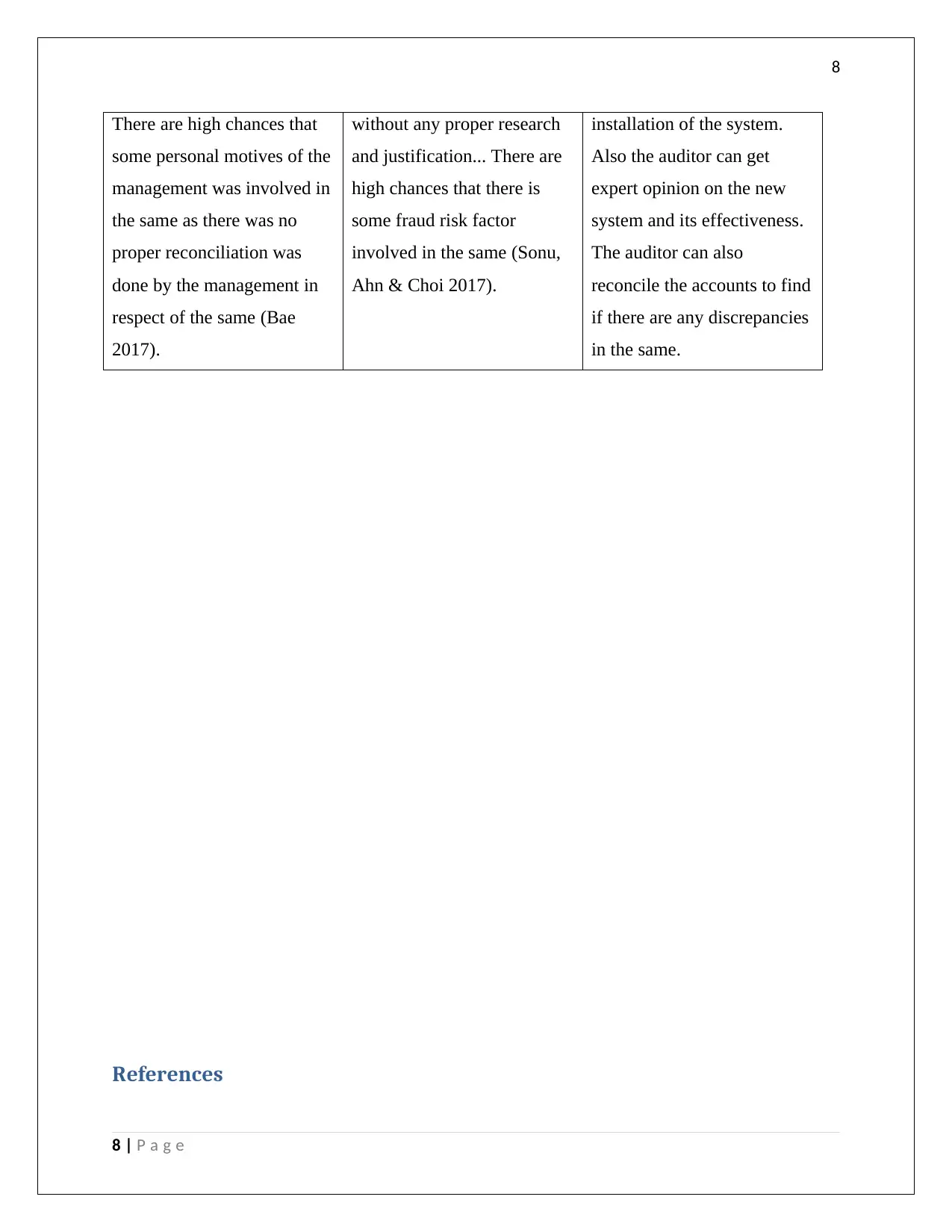

This document presents a comprehensive case study analysis of the audit of Double Ink Printers Ltd (DIPL). The analysis begins with an overview of the audit process, emphasizing the auditor's role in assessing financial statements and the application of substantive and analytical audit procedures. The study examines key financial ratios and trends over three years, including current, liquid, debt-equity, net profit, and return on equity ratios. It then delves into the identification of audit risks, specifically inherent, control, and detection risks, within DIPL's operations, including risks related to non-routine transactions, the implementation of a new IT system, and changes in accounting policies. The case study also explores potential fraud risks, such as the lack of segregation of duties and issues related to the hasty installation of the new IT system. Finally, it outlines the auditor's approach to mitigating these risks through appropriate procedures, such as verifying accounts, seeking expert opinions, and reconciling financial records.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.