Audit and Assurance Services Report: Ethical and Legal Issues

VerifiedAdded on 2022/08/26

|7

|1686

|25

Report

AI Summary

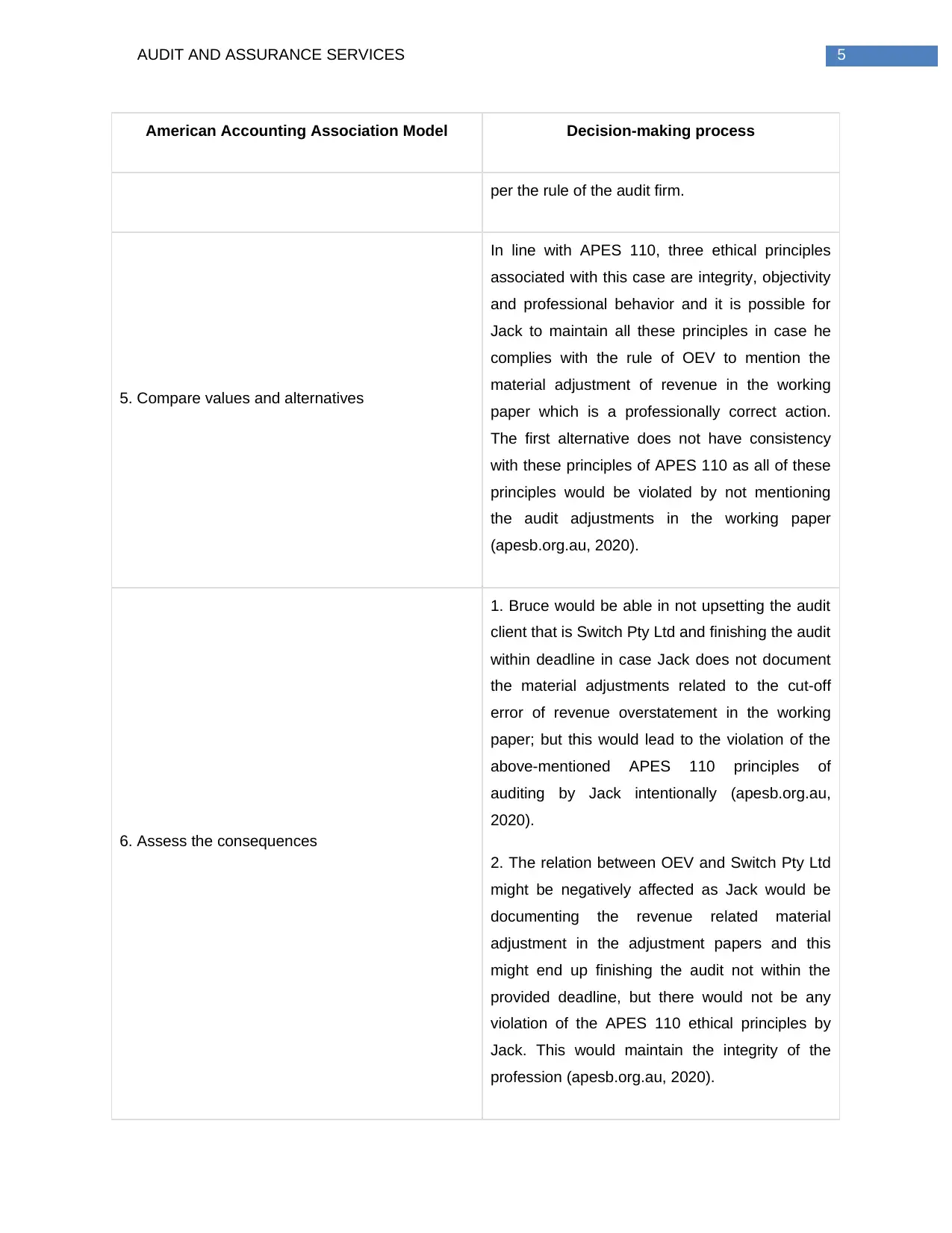

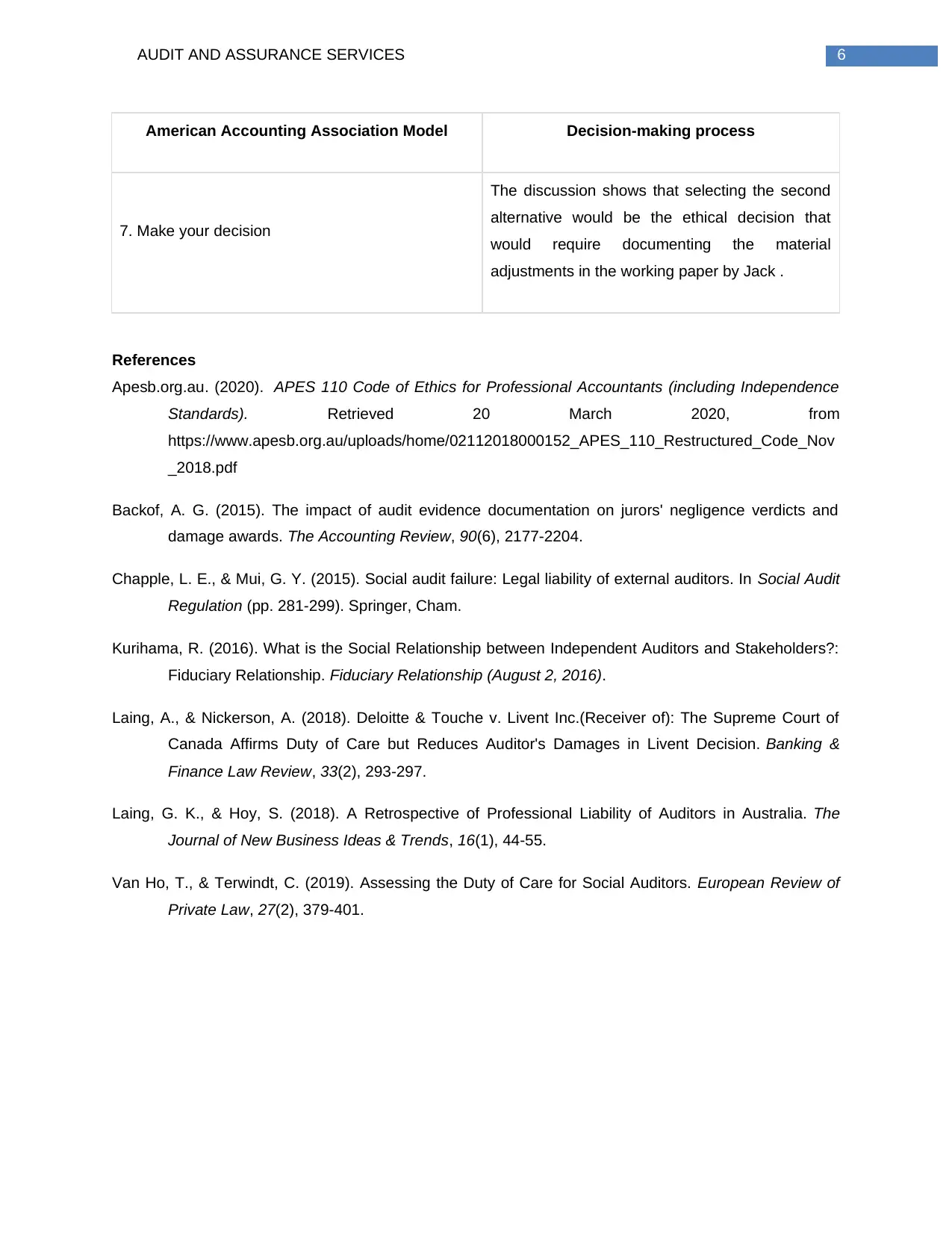

This report examines the audit and assurance services provided by Oscar Edwards Vance (OEV), focusing on the cases of Framed Ltd and Switch Pty Ltd. It analyzes the elements of tort of negligence, including duty of care, breach of duty, causation, and harm, to assess the potential success of legal actions by Framed's liquidators and VicBank against OEV. The report highlights OEV's failure to identify material misstatements and assess going concern risks, leading to financial losses for stakeholders. Furthermore, the report applies the American Accounting Association's model to address ethical issues related to documenting material adjustments. The analysis includes ethical principles from APES 110, considering integrity, objectivity, and professional behavior, and discusses alternative actions and their consequences. The report concludes by emphasizing the importance of auditors adhering to ethical standards and considering negligence when performing audits.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.