CQUniversity ACCT20075 Audit and Ethics Report: NAB Analysis

VerifiedAdded on 2022/10/04

|12

|2547

|27

Report

AI Summary

This report, prepared for CQUniversity's ACCT20075 Auditing and Ethics course, analyzes the financial statements of National Australia Bank (NAB). It begins by determining materiality levels based on NAB's 2018 financial data, calculating planning materiality using a 2% threshold applied to total assets. The report then conducts a preliminary analytical review, utilizing ratio analysis (liquidity, profitability, and leverage) from 2015 to 2018 to assess trends in NAB's financial performance. Key ratios like current and quick ratios, return on assets, return on equity, and net profit margin are examined. A cash flow statement analysis follows, dissecting NAB's operating, investing, and financing activities in 2018, highlighting significant cash inflows and outflows. The report emphasizes the importance of the going concern principle. Finally, it references the auditor's report, noting its unqualified opinion and highlighting key audit matters, such as credit impairment and risk assessment. The report adheres to relevant accounting standards and principles like AASB and Corporations Act 2001.

Running head: AUDIT AND ETHICS

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note:

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality Level.........................................................................................................................2

Section 2..........................................................................................................................................3

Preliminary Analytical Review....................................................................................................3

Section 3..........................................................................................................................................6

Cash Flow Statement Analysis....................................................................................................6

Auditor Report.............................................................................................................................8

References......................................................................................................................................10

Table of Contents

Section 1..........................................................................................................................................2

Materiality Level.........................................................................................................................2

Section 2..........................................................................................................................................3

Preliminary Analytical Review....................................................................................................3

Section 3..........................................................................................................................................6

Cash Flow Statement Analysis....................................................................................................6

Auditor Report.............................................................................................................................8

References......................................................................................................................................10

2AUDIT AND ETHICS

Section 1

Materiality Level

The auditing process involves effective investigation of the financial statements of the

business in order to estimate whether the financial statements are showing true and fair view of

the financial position of the business (Eilifsen & Messier Jr, 2014). It is on the basis of the audit

report which is issued by the auditor of the business, that investors make decisions whether the

financial statements are appropriate or not and whether they are worth making investments or

not. The auditor has the responsibility of checking each element which is covered in the financial

statement and check whether the same are appropriate or misrepresented. One of the components

which is considered while estimating whether the item is fairly represented in the books of

accounts is the materiality of the item. The determination of the materiality estimate depends on

the judgement of the auditor and the nature of the business which is being audited (Ruhnke &

Schmidt, 2014). The assessment would be considering the materiality estimates for the business

of National Australian Bank (NAB) and also ensure that the financial statements are showing

appropriate view of the financial position of the business or not.

In simple terms, materiality may be defined as the significance which the item has in the

annual report and how the misrepresentation of the same can impact the financial position of the

business. In case to recognise an item as material, various parameters may be considered and

some of the same are complex nature of the items, repetitiveness of the item, numerical size of

the item. The planning materiality of the business and the percentage which is considered to

compute the same are considered at the planning stage of the audit (Legoria, Melendrez &

Reynolds, 2013). In order to estimate the planning materiality of a business a percentage is

Section 1

Materiality Level

The auditing process involves effective investigation of the financial statements of the

business in order to estimate whether the financial statements are showing true and fair view of

the financial position of the business (Eilifsen & Messier Jr, 2014). It is on the basis of the audit

report which is issued by the auditor of the business, that investors make decisions whether the

financial statements are appropriate or not and whether they are worth making investments or

not. The auditor has the responsibility of checking each element which is covered in the financial

statement and check whether the same are appropriate or misrepresented. One of the components

which is considered while estimating whether the item is fairly represented in the books of

accounts is the materiality of the item. The determination of the materiality estimate depends on

the judgement of the auditor and the nature of the business which is being audited (Ruhnke &

Schmidt, 2014). The assessment would be considering the materiality estimates for the business

of National Australian Bank (NAB) and also ensure that the financial statements are showing

appropriate view of the financial position of the business or not.

In simple terms, materiality may be defined as the significance which the item has in the

annual report and how the misrepresentation of the same can impact the financial position of the

business. In case to recognise an item as material, various parameters may be considered and

some of the same are complex nature of the items, repetitiveness of the item, numerical size of

the item. The planning materiality of the business and the percentage which is considered to

compute the same are considered at the planning stage of the audit (Legoria, Melendrez &

Reynolds, 2013). In order to estimate the planning materiality of a business a percentage is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT AND ETHICS

considered which would be applied to a base to compute the planning materiality of the business.

In order to consider the base for the computation process, the total asset figure is considered for

estimating the planning materiality of the business (Vîlsănoiu & Buzenche, 2014). The total asset

figure which is represented in the financial statement of the company for the year 2018 is shown

to be $ 806,510 million. The percentage which is considered for ascertaining the planning

materiality of the business is considered to be 2%. It is to be noted that on the basis of the

planning materiality of the business, the performance materiality of different items would be

estimated. The performance materiality is the benchmark showing whether the item is material or

not. The computation of materiality for the business is shown below in details:

Planning Materiality=Total Assets of the Company × Percentage estimated

¿ $ 806,510 million ×2 %

¿ $ 16,130.2million

Therefore, the above figure shows the planning materiality of the business which is

estimated by the auditor and the same would be considered by the auditor of the business for

estimating the performance materiality of the business.

Section 2

Preliminary Analytical Review

The Preliminary Article Review can be well done in order to assess the changes observed

in the financial performance of the company. Ratio analysis will be sued as the primary tool for

the purpose of evaluating the key changes observed in the financials of the company. The key

ratio that has been evaluated for the company includes the Liquidity Ratio, Profitability Ratio

considered which would be applied to a base to compute the planning materiality of the business.

In order to consider the base for the computation process, the total asset figure is considered for

estimating the planning materiality of the business (Vîlsănoiu & Buzenche, 2014). The total asset

figure which is represented in the financial statement of the company for the year 2018 is shown

to be $ 806,510 million. The percentage which is considered for ascertaining the planning

materiality of the business is considered to be 2%. It is to be noted that on the basis of the

planning materiality of the business, the performance materiality of different items would be

estimated. The performance materiality is the benchmark showing whether the item is material or

not. The computation of materiality for the business is shown below in details:

Planning Materiality=Total Assets of the Company × Percentage estimated

¿ $ 806,510 million ×2 %

¿ $ 16,130.2million

Therefore, the above figure shows the planning materiality of the business which is

estimated by the auditor and the same would be considered by the auditor of the business for

estimating the performance materiality of the business.

Section 2

Preliminary Analytical Review

The Preliminary Article Review can be well done in order to assess the changes observed

in the financial performance of the company. Ratio analysis will be sued as the primary tool for

the purpose of evaluating the key changes observed in the financials of the company. The key

ratio that has been evaluated for the company includes the Liquidity Ratio, Profitability Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT AND ETHICS

and Leverage and Coverage Ratio’s that are well carried out for the purpose of evaluating the

trend shown by the company in the trend period. The trend period that has been selected for the

purpose of analysis is between the period of 2015-2018 (Carraher and Van Auken 2013).

Liquidity Ratios: The liquidity ratio of the company can be well computed with the help of the

current and quick ratio for the company where the liquidity position of the company will be well

assessed with the help of liquid assets presents in the business. The liquidity ratio for the

company has been continuously for the company in the trend period evaluated for the company

which well reflects that the bank is maintain enough amount of liquid assets such as cash and

cash equivalents in respond to the current liabilities that it has in the financial statements of the

company (Annual Report NAB, 2015). It is adequately important that the companies have an

adequate and increasing liquidity ratio for the company so that the banks operations can go on

for a sustainable basis. It is well equally important that the Auditor well assesses the

appropriateness of the current assets and current liabilities of the banks for assessing the

classification done and there relevance with the current Australian Accounting Standards and

Corporations Act 2001.

Profitability Ratios: The profitability ratio is a key ratio that is computed for assessing the

financial performance and the net wealth created by the companies for the equity shareholders

and for the company as a whole (Williams & Dobelman, 2017). On an overall basis it was found

that the net profitability of the company is consistently falling for the company and the Auditors

of the company should be carefully reviewing the various aspects of the income statement where

changes in the value especially in relation to the Impairment Charges and Operating Expenses

for the company that was found to be quite volatile for the trend period analysed for the

company.

and Leverage and Coverage Ratio’s that are well carried out for the purpose of evaluating the

trend shown by the company in the trend period. The trend period that has been selected for the

purpose of analysis is between the period of 2015-2018 (Carraher and Van Auken 2013).

Liquidity Ratios: The liquidity ratio of the company can be well computed with the help of the

current and quick ratio for the company where the liquidity position of the company will be well

assessed with the help of liquid assets presents in the business. The liquidity ratio for the

company has been continuously for the company in the trend period evaluated for the company

which well reflects that the bank is maintain enough amount of liquid assets such as cash and

cash equivalents in respond to the current liabilities that it has in the financial statements of the

company (Annual Report NAB, 2015). It is adequately important that the companies have an

adequate and increasing liquidity ratio for the company so that the banks operations can go on

for a sustainable basis. It is well equally important that the Auditor well assesses the

appropriateness of the current assets and current liabilities of the banks for assessing the

classification done and there relevance with the current Australian Accounting Standards and

Corporations Act 2001.

Profitability Ratios: The profitability ratio is a key ratio that is computed for assessing the

financial performance and the net wealth created by the companies for the equity shareholders

and for the company as a whole (Williams & Dobelman, 2017). On an overall basis it was found

that the net profitability of the company is consistently falling for the company and the Auditors

of the company should be carefully reviewing the various aspects of the income statement where

changes in the value especially in relation to the Impairment Charges and Operating Expenses

for the company that was found to be quite volatile for the trend period analysed for the

company.

5AUDIT AND ETHICS

Return on Assets: The return on assets for the company shows the amount of return generated

by the banks with the help of given set of total assets deployed in the due course of business. The

return on total assets for the Bank has fallen in the trend period and the same can be well

attributed to the falling profitability of the company for the reinstated period (Robinson et al.,

2015).

Return on Equity: The return on equity for the company shows the amount of return generated

by the company for the equity shareholders of the company for the time period analysed wherein

the net profit will be compared with the amount of equity invested by the shareholders of the

company (Uechi et al., 2015). The return on equity for the bank has fallen in the trend period due

to the fall in the profitability of the company and the overall rise in the equity value of the

company making the return to fall for the banks over the time period analysed.

Net Profit Margin: The net profit margin for the company shows the amount of net income

generated by the banks after taking in all the interest income and other income generated by the

banks and the expenses that are well in association with the operations of the banks. The net

profit margin for the company has been falling for the company in the trend period whereby

changes in the operating expenses have significantly impacted the net profitability of bank.

Leverage and Coverage Ratios: The leverage ratio that is debt to equity ratio for the banks has

been increasing consistently for the bank due to the high proportion to debt weightage in the

financials of the company which is currently greater than 9 times of the equity value. The auditor

of the company should be carefully reviewing the various aspects of debt account by carefully

analysing the terms and classification under which the debt stands in the books of banks. The

coverage ratio that is the debt to total assets for the company has been around 90%, however it si

Return on Assets: The return on assets for the company shows the amount of return generated

by the banks with the help of given set of total assets deployed in the due course of business. The

return on total assets for the Bank has fallen in the trend period and the same can be well

attributed to the falling profitability of the company for the reinstated period (Robinson et al.,

2015).

Return on Equity: The return on equity for the company shows the amount of return generated

by the company for the equity shareholders of the company for the time period analysed wherein

the net profit will be compared with the amount of equity invested by the shareholders of the

company (Uechi et al., 2015). The return on equity for the bank has fallen in the trend period due

to the fall in the profitability of the company and the overall rise in the equity value of the

company making the return to fall for the banks over the time period analysed.

Net Profit Margin: The net profit margin for the company shows the amount of net income

generated by the banks after taking in all the interest income and other income generated by the

banks and the expenses that are well in association with the operations of the banks. The net

profit margin for the company has been falling for the company in the trend period whereby

changes in the operating expenses have significantly impacted the net profitability of bank.

Leverage and Coverage Ratios: The leverage ratio that is debt to equity ratio for the banks has

been increasing consistently for the bank due to the high proportion to debt weightage in the

financials of the company which is currently greater than 9 times of the equity value. The auditor

of the company should be carefully reviewing the various aspects of debt account by carefully

analysing the terms and classification under which the debt stands in the books of banks. The

coverage ratio that is the debt to total assets for the company has been around 90%, however it si

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT AND ETHICS

well recommended that the same remains above 100% whereby the assets of the company well

covers all the debt associated with banks.

Section 3

Cash Flow Statement Analysis

The cash flow statement of the company for the National Australia Bank will be well

analysed with the help of the various operating, investing and financial activities that were well

carried out by the banks during the financial year 2018. The cash flow statement is an important

statement reflecting the liquidity position and the classification of the various business activities

that were carried out by the bank during the financial year 2018 (Annual Report NAB, 2018).

The maximum cash was generated from the financing activities of the banks whereby the

Bank has shown an overall cash inflow of around $4,926 million for the year 2018 and the same

can be well contributed to the proceeds from issue of bonds and repayments of bonds that was

well carried out by the company (Annual Report NAB, 2017). On the other the net cash flow

from operating activities for the company has been negative balance of -$9,196. The negative

balance has been primary after taking into account all of the changes in association with the

Operating Assets and Liabilities of the Company. The primary cash receipt for the company has

been from the interest received that has been reported in the operating activities of the company

which was around $28,340. On the other hand, proceeds from issue of bonds, notes and

subordinated debt amounted to around $32,139 for the year 2018 (Annual Review NAB, 2016).

The primary cash payment for the year 2018 was around $14,778 in the form of interest paid by

the Bank.

well recommended that the same remains above 100% whereby the assets of the company well

covers all the debt associated with banks.

Section 3

Cash Flow Statement Analysis

The cash flow statement of the company for the National Australia Bank will be well

analysed with the help of the various operating, investing and financial activities that were well

carried out by the banks during the financial year 2018. The cash flow statement is an important

statement reflecting the liquidity position and the classification of the various business activities

that were carried out by the bank during the financial year 2018 (Annual Report NAB, 2018).

The maximum cash was generated from the financing activities of the banks whereby the

Bank has shown an overall cash inflow of around $4,926 million for the year 2018 and the same

can be well contributed to the proceeds from issue of bonds and repayments of bonds that was

well carried out by the company (Annual Report NAB, 2017). On the other the net cash flow

from operating activities for the company has been negative balance of -$9,196. The negative

balance has been primary after taking into account all of the changes in association with the

Operating Assets and Liabilities of the Company. The primary cash receipt for the company has

been from the interest received that has been reported in the operating activities of the company

which was around $28,340. On the other hand, proceeds from issue of bonds, notes and

subordinated debt amounted to around $32,139 for the year 2018 (Annual Review NAB, 2016).

The primary cash payment for the year 2018 was around $14,778 in the form of interest paid by

the Bank.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT AND ETHICS

The main items that were included in the investing activities of the company were

primarily in the field of movement in debt instruments which are held at fair value by the

company amounted to $22,018 and proceeds received from disposal and maturity of debt

instruments valued at inflow of 22,228. The financing activities included key items of the

company including the repayment of bonds, proceeds from issue of bonds and other dividend

that were paid by the bank for the financial year 2018. The total cash inflow from the financing

activities of the company for the year 2018 was around $4,926 and the same has provided the

maximum amount of cash flows for the company.

The principle of going concern plays a very important and vital role in the overall

operations continuation basis that has been applied by the bank. The going concern principle

well states that the business carried on by the bank is going on well whereby the bank do not

have any intention to cease any operations in the near term future. The principle applied by the

management of the company has been based on the fundamental principles of accounting where

relevant judgement and assumption has been made and the auditor of the company needs to

analyse the materiality of the principle applied.

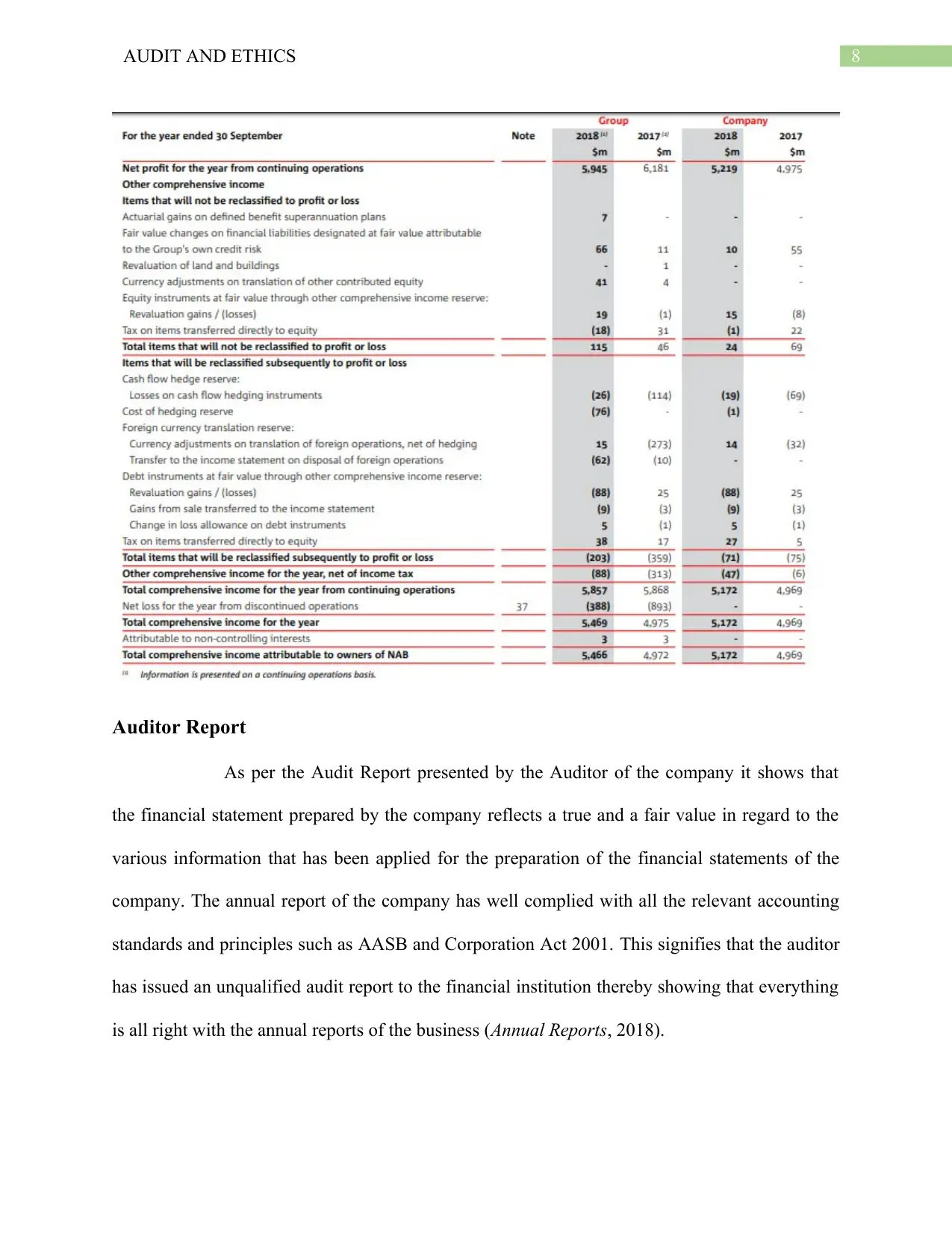

The extract of the consolidated Cash Flow Statement is shown below:

The main items that were included in the investing activities of the company were

primarily in the field of movement in debt instruments which are held at fair value by the

company amounted to $22,018 and proceeds received from disposal and maturity of debt

instruments valued at inflow of 22,228. The financing activities included key items of the

company including the repayment of bonds, proceeds from issue of bonds and other dividend

that were paid by the bank for the financial year 2018. The total cash inflow from the financing

activities of the company for the year 2018 was around $4,926 and the same has provided the

maximum amount of cash flows for the company.

The principle of going concern plays a very important and vital role in the overall

operations continuation basis that has been applied by the bank. The going concern principle

well states that the business carried on by the bank is going on well whereby the bank do not

have any intention to cease any operations in the near term future. The principle applied by the

management of the company has been based on the fundamental principles of accounting where

relevant judgement and assumption has been made and the auditor of the company needs to

analyse the materiality of the principle applied.

The extract of the consolidated Cash Flow Statement is shown below:

8AUDIT AND ETHICS

Auditor Report

As per the Audit Report presented by the Auditor of the company it shows that

the financial statement prepared by the company reflects a true and a fair value in regard to the

various information that has been applied for the preparation of the financial statements of the

company. The annual report of the company has well complied with all the relevant accounting

standards and principles such as AASB and Corporation Act 2001. This signifies that the auditor

has issued an unqualified audit report to the financial institution thereby showing that everything

is all right with the annual reports of the business (Annual Reports, 2018).

Auditor Report

As per the Audit Report presented by the Auditor of the company it shows that

the financial statement prepared by the company reflects a true and a fair value in regard to the

various information that has been applied for the preparation of the financial statements of the

company. The annual report of the company has well complied with all the relevant accounting

standards and principles such as AASB and Corporation Act 2001. This signifies that the auditor

has issued an unqualified audit report to the financial institution thereby showing that everything

is all right with the annual reports of the business (Annual Reports, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT AND ETHICS

The key Audit matters that were taken into account by the Auditors of the company

included the Provision for Credit Impairment on Loans at Amortised Cost, Conducting Risks and

analysing various provisions measures that are made by the bank which included the

restructuring provisions. The above matter has been considered significant by the Auditor of the

company and they have taken several steps in order to check the materiality of the same with the

accounting principles applied for recording and valuation of the same.

The key Audit matters that were taken into account by the Auditors of the company

included the Provision for Credit Impairment on Loans at Amortised Cost, Conducting Risks and

analysing various provisions measures that are made by the bank which included the

restructuring provisions. The above matter has been considered significant by the Auditor of the

company and they have taken several steps in order to check the materiality of the same with the

accounting principles applied for recording and valuation of the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT AND ETHICS

References

Annual Report NAB (2015). Nab.com.au. Retrieved 29 August 2019, from

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/annual-

financial-report-2015.pdf

Annual Report NAB (2017). Capital.nab.com.au. Retrieved 29 August 2019, from

https://capital.nab.com.au/docs/NAB-2017-annual-financial-report.pdf

Annual Report NAB (2018). Capital.nab.com.au. Retrieved 29 August 2019, from

https://capital.nab.com.au/docs/2018_NAB_Annual_Financial_Report.pdf

Annual Reports. (2018). Nab.com.au. Retrieved 29 August 2019, from

https://www.nab.com.au/about-us/shareholder-centre/financial-disclosuresandreporting/

annual-reports-and-presentations

Annual Review NAB (2016). Nab.com.au. Retrieved 29 August 2019, from

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2016-annual-

review.pdf

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), 414-442.

References

Annual Report NAB (2015). Nab.com.au. Retrieved 29 August 2019, from

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/annual-

financial-report-2015.pdf

Annual Report NAB (2017). Capital.nab.com.au. Retrieved 29 August 2019, from

https://capital.nab.com.au/docs/NAB-2017-annual-financial-report.pdf

Annual Report NAB (2018). Capital.nab.com.au. Retrieved 29 August 2019, from

https://capital.nab.com.au/docs/2018_NAB_Annual_Financial_Report.pdf

Annual Reports. (2018). Nab.com.au. Retrieved 29 August 2019, from

https://www.nab.com.au/about-us/shareholder-centre/financial-disclosuresandreporting/

annual-reports-and-presentations

Annual Review NAB (2016). Nab.com.au. Retrieved 29 August 2019, from

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2016-annual-

review.pdf

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), 414-442.

11AUDIT AND ETHICS

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Ruhnke, K., & Schmidt, M. (2014). Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), 247-269.

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J., & Kenett, D. Y. (2015). Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, 488-509.

Vîlsănoiu, D., & Buzenche, S. (2014). Determining Audit Materiality in the Banking Industry–a

Knowledge Based Approach. Procedia Economics and Finance, 15, 935-942.

Williams, E. E., & Dobelman, J. A. (2017). Financial statement analysis. World Scientific Book

Chapters, 109-169.

Zainudin, E. F., & Hashim, H. A. (2016). Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), 266-278.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Ruhnke, K., & Schmidt, M. (2014). Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), 247-269.

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J., & Kenett, D. Y. (2015). Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, 488-509.

Vîlsănoiu, D., & Buzenche, S. (2014). Determining Audit Materiality in the Banking Industry–a

Knowledge Based Approach. Procedia Economics and Finance, 15, 935-942.

Williams, E. E., & Dobelman, J. A. (2017). Financial statement analysis. World Scientific Book

Chapters, 109-169.

Zainudin, E. F., & Hashim, H. A. (2016). Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), 266-278.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.