Audit and Assurance Theory: Audit Expectation Gap and Independence

VerifiedAdded on 2022/10/11

|8

|1701

|11

Report

AI Summary

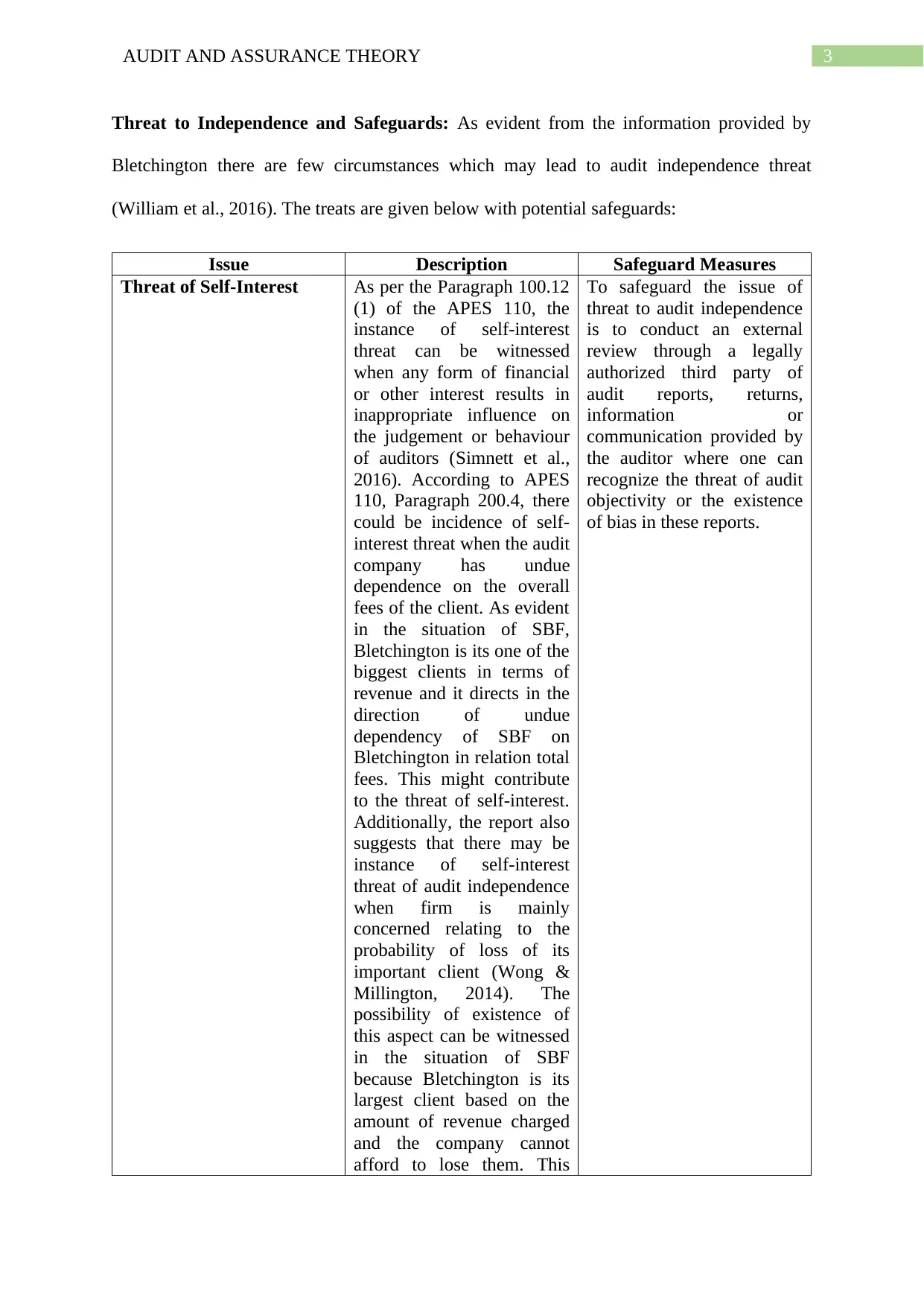

This report, prepared for Samway Baker Fitzgerald (SBF), examines the audit expectation gap and threats to auditor independence concerning the audit of Bletchington Ltd, a major client. The report highlights the disparity between the public's expectations of auditors and the auditors' actual responsibilities, particularly in areas such as providing absolute assurance and guaranteeing future viability. It identifies and analyzes specific threats to auditor independence, including self-interest, self-review, and familiarity threats, detailing how these threats could arise within the context of Bletchington Ltd's operations and the relationship between SBF and its client. The report proposes safeguard measures to mitigate these threats, such as external reviews, ensuring the independence of internal audit teams, and implementing monitoring processes. The analysis is supported by relevant accounting literature and professional standards, such as APES 110.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.