Audit Assignment 1: University Audit of Far Faraway Pastoral Limited

VerifiedAdded on 2023/01/17

|10

|3214

|48

Report

AI Summary

This audit assignment report analyzes the 2019 audit of Far Faraway Pastoral Limited (FFA), an agricultural company listed on the ASX, by the accounting firm Samway Baker Fitzgerald (SBF). The report addresses several key issues raised by the audit team. Firstly, it identifies breaches of ASX Corporate Governance Principles related to the composition of the board of directors, particularly concerning the independence of the chairman and other non-executive directors due to their shareholdings and supplier relationships. Secondly, it examines ethical issues arising from discrepancies in revenue recognition policies, highlighting conflicts of interest and threats to integrity and objectivity, as well as violations of the Code of Ethics for Professional Accountants. The report also includes a report to the managing partner of SBF regarding a subsidiary's operational issues and potential negligence claims. The report explores the implications of these issues, including contributory negligence, and provides recommendations for corrective actions. The assignment provides a comprehensive analysis of auditing practices, corporate governance, and ethical considerations within a real-world context.

AUDIT ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

[Type here]

By student name

Professor

University

Date: 25 April 2018.

[Type here]

2

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................3

Question 1: Breach of ASX Corporate Governance Principles.................................................................3

Question 2: Issue w.r.t. Code of Ethics for Professional Accountants......................................................4

Question 3: Report to the managing partner of SBF................................................................................5

Introduction.........................................................................................................................................5

Discussion and Analysis.......................................................................................................................6

Conclusion...........................................................................................................................................6

Conclusion...................................................................................................................................................6

References...................................................................................................................................................8

[Type here]

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................3

Question 1: Breach of ASX Corporate Governance Principles.................................................................3

Question 2: Issue w.r.t. Code of Ethics for Professional Accountants......................................................4

Question 3: Report to the managing partner of SBF................................................................................5

Introduction.........................................................................................................................................5

Discussion and Analysis.......................................................................................................................6

Conclusion...........................................................................................................................................6

Conclusion...................................................................................................................................................6

References...................................................................................................................................................8

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction

In the given scenario, the audit manager of the accounting firm Samway Baker Fitzgerald (SBF), is

carrying out the annual audit of Far Faraway Pastoral Limited (FFA) for the year ended 30th June 2019

with the team of audit seniors and it is found that the company there are certain accounting and

auditing issues as highlighted by the audit seniors in the team. SBF main clientele includes companies

from mining manufacturing and agriculture industries but for some of the reasons, all of them are under

severe pressure either due to downtown in commodity market (mining), overseas competition

(manufacturing) or devastating draught in Eastern Australia (agriculture). FFA is an agricultural company

which is based out of Orange city and is one of the largest clients of SBF in terms of revenue. FFA is listed

on the ASX. The course of action that should be undertaken by SBF has also been suggested in each

scenario (Bumgarner & Vasarhelyi, 2018).

Discussion and Analysis

Question 1: Breach of ASX Corporate Governance Principles

In the given case, one of the audit seniors Samantha Gabrielle observed that the corporate governance

arrangements of the company as on 30th June 2019 are not as per the standards. The Board of the

company comprises the CEO and CFO of the company namely Bruce Blanch and Alexandra Rose

respectively and three non-executive directors. Kevin Oliver, former executive at Macquarie Bank who is

holding 11% of the share capital of FFA, Matthew James, one of the retired farmers of the supplier who

used to supply to FFA and Jacqueline Grace, an orthopaedic surgeon based out of Orange form the

group of non-executive directors. Kevin Oliver is the Chairman of the Board (Arnott, Lizama, & Song,

2017).

As per the Principles laid down in the Charter of Corporate Governance and Recommendation 2.1, the

board should have independent directors and the chairman of the board should also be an independent

director (Recommendation 2.2). The role of the Chairman as well as the CEO of the company should not

be exercised by the same individual (Recommendation 2.3), the board should also have a Nomination

Committee (Recommendation 2.4), there should always be a process for evaluation of the performance

of the board, the committee and the individual directors (Recommendation 2.5) and finally the company

should report the information above in the disclosure section of the annual report of the company

(Recommendation 2.6). An independent director is the one who is not a member of the management

and who is free from any material relationship or business with the company and which could materially

interfere or reasonably seen to be partially interfering with the independent exercise of judgement by

directors (Boccia & Leonardi, 2016). Furthermore, as per the definition of the independent directors,

he/she should not be a substantial shareholder of the company or an officer or otherwise directly

associated with the substantial shareholder of the company. He should also not be a material customer

or supplier of the company or any other group member or an officer or otherwise directly or indirectly

associated with the material supplier or customer of the company as it affects and hinders the concept

of independence (Dopuch & Sunder, 1980).

[Type here]

Introduction

In the given scenario, the audit manager of the accounting firm Samway Baker Fitzgerald (SBF), is

carrying out the annual audit of Far Faraway Pastoral Limited (FFA) for the year ended 30th June 2019

with the team of audit seniors and it is found that the company there are certain accounting and

auditing issues as highlighted by the audit seniors in the team. SBF main clientele includes companies

from mining manufacturing and agriculture industries but for some of the reasons, all of them are under

severe pressure either due to downtown in commodity market (mining), overseas competition

(manufacturing) or devastating draught in Eastern Australia (agriculture). FFA is an agricultural company

which is based out of Orange city and is one of the largest clients of SBF in terms of revenue. FFA is listed

on the ASX. The course of action that should be undertaken by SBF has also been suggested in each

scenario (Bumgarner & Vasarhelyi, 2018).

Discussion and Analysis

Question 1: Breach of ASX Corporate Governance Principles

In the given case, one of the audit seniors Samantha Gabrielle observed that the corporate governance

arrangements of the company as on 30th June 2019 are not as per the standards. The Board of the

company comprises the CEO and CFO of the company namely Bruce Blanch and Alexandra Rose

respectively and three non-executive directors. Kevin Oliver, former executive at Macquarie Bank who is

holding 11% of the share capital of FFA, Matthew James, one of the retired farmers of the supplier who

used to supply to FFA and Jacqueline Grace, an orthopaedic surgeon based out of Orange form the

group of non-executive directors. Kevin Oliver is the Chairman of the Board (Arnott, Lizama, & Song,

2017).

As per the Principles laid down in the Charter of Corporate Governance and Recommendation 2.1, the

board should have independent directors and the chairman of the board should also be an independent

director (Recommendation 2.2). The role of the Chairman as well as the CEO of the company should not

be exercised by the same individual (Recommendation 2.3), the board should also have a Nomination

Committee (Recommendation 2.4), there should always be a process for evaluation of the performance

of the board, the committee and the individual directors (Recommendation 2.5) and finally the company

should report the information above in the disclosure section of the annual report of the company

(Recommendation 2.6). An independent director is the one who is not a member of the management

and who is free from any material relationship or business with the company and which could materially

interfere or reasonably seen to be partially interfering with the independent exercise of judgement by

directors (Boccia & Leonardi, 2016). Furthermore, as per the definition of the independent directors,

he/she should not be a substantial shareholder of the company or an officer or otherwise directly

associated with the substantial shareholder of the company. He should also not be a material customer

or supplier of the company or any other group member or an officer or otherwise directly or indirectly

associated with the material supplier or customer of the company as it affects and hinders the concept

of independence (Dopuch & Sunder, 1980).

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

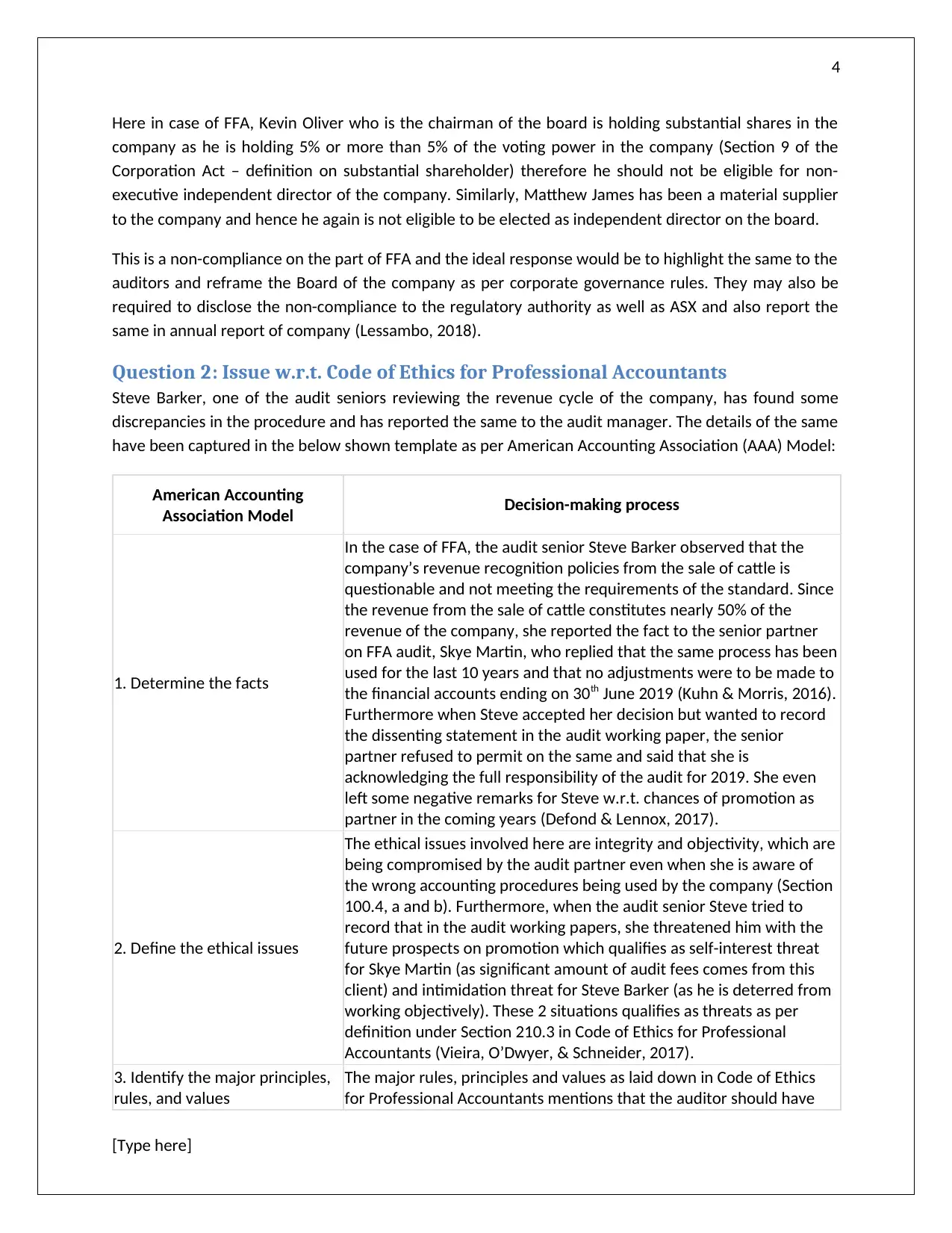

Here in case of FFA, Kevin Oliver who is the chairman of the board is holding substantial shares in the

company as he is holding 5% or more than 5% of the voting power in the company (Section 9 of the

Corporation Act – definition on substantial shareholder) therefore he should not be eligible for non-

executive independent director of the company. Similarly, Matthew James has been a material supplier

to the company and hence he again is not eligible to be elected as independent director on the board.

This is a non-compliance on the part of FFA and the ideal response would be to highlight the same to the

auditors and reframe the Board of the company as per corporate governance rules. They may also be

required to disclose the non-compliance to the regulatory authority as well as ASX and also report the

same in annual report of company (Lessambo, 2018).

Question 2: Issue w.r.t. Code of Ethics for Professional Accountants

Steve Barker, one of the audit seniors reviewing the revenue cycle of the company, has found some

discrepancies in the procedure and has reported the same to the audit manager. The details of the same

have been captured in the below shown template as per American Accounting Association (AAA) Model:

American Accounting

Association Model Decision-making process

1. Determine the facts

In the case of FFA, the audit senior Steve Barker observed that the

company’s revenue recognition policies from the sale of cattle is

questionable and not meeting the requirements of the standard. Since

the revenue from the sale of cattle constitutes nearly 50% of the

revenue of the company, she reported the fact to the senior partner

on FFA audit, Skye Martin, who replied that the same process has been

used for the last 10 years and that no adjustments were to be made to

the financial accounts ending on 30th June 2019 (Kuhn & Morris, 2016).

Furthermore when Steve accepted her decision but wanted to record

the dissenting statement in the audit working paper, the senior

partner refused to permit on the same and said that she is

acknowledging the full responsibility of the audit for 2019. She even

left some negative remarks for Steve w.r.t. chances of promotion as

partner in the coming years (Defond & Lennox, 2017).

2. Define the ethical issues

The ethical issues involved here are integrity and objectivity, which are

being compromised by the audit partner even when she is aware of

the wrong accounting procedures being used by the company (Section

100.4, a and b). Furthermore, when the audit senior Steve tried to

record that in the audit working papers, she threatened him with the

future prospects on promotion which qualifies as self-interest threat

for Skye Martin (as significant amount of audit fees comes from this

client) and intimidation threat for Steve Barker (as he is deterred from

working objectively). These 2 situations qualifies as threats as per

definition under Section 210.3 in Code of Ethics for Professional

Accountants (Vieira, O’Dwyer, & Schneider, 2017).

3. Identify the major principles,

rules, and values

The major rules, principles and values as laid down in Code of Ethics

for Professional Accountants mentions that the auditor should have

[Type here]

Here in case of FFA, Kevin Oliver who is the chairman of the board is holding substantial shares in the

company as he is holding 5% or more than 5% of the voting power in the company (Section 9 of the

Corporation Act – definition on substantial shareholder) therefore he should not be eligible for non-

executive independent director of the company. Similarly, Matthew James has been a material supplier

to the company and hence he again is not eligible to be elected as independent director on the board.

This is a non-compliance on the part of FFA and the ideal response would be to highlight the same to the

auditors and reframe the Board of the company as per corporate governance rules. They may also be

required to disclose the non-compliance to the regulatory authority as well as ASX and also report the

same in annual report of company (Lessambo, 2018).

Question 2: Issue w.r.t. Code of Ethics for Professional Accountants

Steve Barker, one of the audit seniors reviewing the revenue cycle of the company, has found some

discrepancies in the procedure and has reported the same to the audit manager. The details of the same

have been captured in the below shown template as per American Accounting Association (AAA) Model:

American Accounting

Association Model Decision-making process

1. Determine the facts

In the case of FFA, the audit senior Steve Barker observed that the

company’s revenue recognition policies from the sale of cattle is

questionable and not meeting the requirements of the standard. Since

the revenue from the sale of cattle constitutes nearly 50% of the

revenue of the company, she reported the fact to the senior partner

on FFA audit, Skye Martin, who replied that the same process has been

used for the last 10 years and that no adjustments were to be made to

the financial accounts ending on 30th June 2019 (Kuhn & Morris, 2016).

Furthermore when Steve accepted her decision but wanted to record

the dissenting statement in the audit working paper, the senior

partner refused to permit on the same and said that she is

acknowledging the full responsibility of the audit for 2019. She even

left some negative remarks for Steve w.r.t. chances of promotion as

partner in the coming years (Defond & Lennox, 2017).

2. Define the ethical issues

The ethical issues involved here are integrity and objectivity, which are

being compromised by the audit partner even when she is aware of

the wrong accounting procedures being used by the company (Section

100.4, a and b). Furthermore, when the audit senior Steve tried to

record that in the audit working papers, she threatened him with the

future prospects on promotion which qualifies as self-interest threat

for Skye Martin (as significant amount of audit fees comes from this

client) and intimidation threat for Steve Barker (as he is deterred from

working objectively). These 2 situations qualifies as threats as per

definition under Section 210.3 in Code of Ethics for Professional

Accountants (Vieira, O’Dwyer, & Schneider, 2017).

3. Identify the major principles,

rules, and values

The major rules, principles and values as laid down in Code of Ethics

for Professional Accountants mentions that the auditor should have

[Type here]

5

American Accounting

Association Model Decision-making process

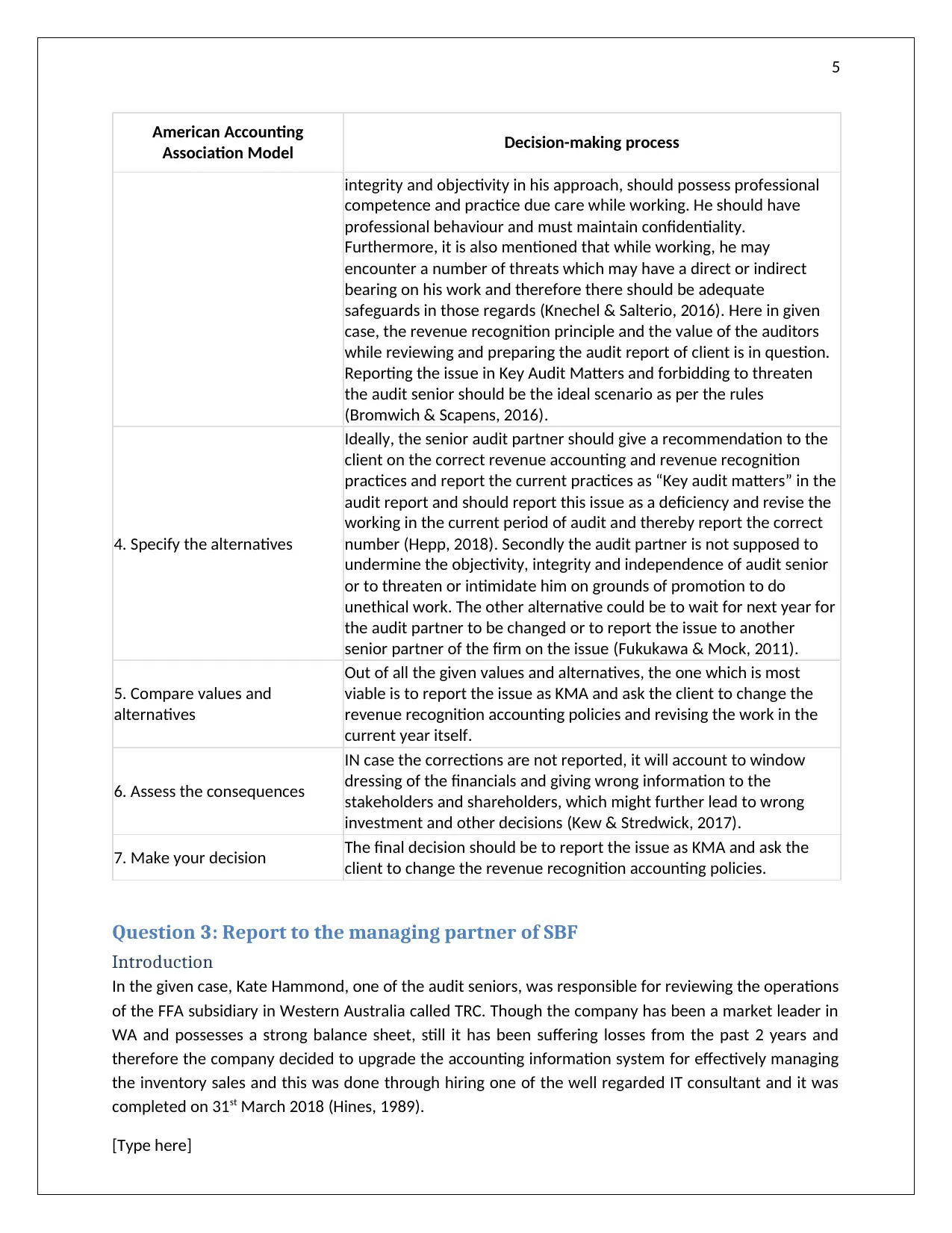

integrity and objectivity in his approach, should possess professional

competence and practice due care while working. He should have

professional behaviour and must maintain confidentiality.

Furthermore, it is also mentioned that while working, he may

encounter a number of threats which may have a direct or indirect

bearing on his work and therefore there should be adequate

safeguards in those regards (Knechel & Salterio, 2016). Here in given

case, the revenue recognition principle and the value of the auditors

while reviewing and preparing the audit report of client is in question.

Reporting the issue in Key Audit Matters and forbidding to threaten

the audit senior should be the ideal scenario as per the rules

(Bromwich & Scapens, 2016).

4. Specify the alternatives

Ideally, the senior audit partner should give a recommendation to the

client on the correct revenue accounting and revenue recognition

practices and report the current practices as “Key audit matters” in the

audit report and should report this issue as a deficiency and revise the

working in the current period of audit and thereby report the correct

number (Hepp, 2018). Secondly the audit partner is not supposed to

undermine the objectivity, integrity and independence of audit senior

or to threaten or intimidate him on grounds of promotion to do

unethical work. The other alternative could be to wait for next year for

the audit partner to be changed or to report the issue to another

senior partner of the firm on the issue (Fukukawa & Mock, 2011).

5. Compare values and

alternatives

Out of all the given values and alternatives, the one which is most

viable is to report the issue as KMA and ask the client to change the

revenue recognition accounting policies and revising the work in the

current year itself.

6. Assess the consequences

IN case the corrections are not reported, it will account to window

dressing of the financials and giving wrong information to the

stakeholders and shareholders, which might further lead to wrong

investment and other decisions (Kew & Stredwick, 2017).

7. Make your decision The final decision should be to report the issue as KMA and ask the

client to change the revenue recognition accounting policies.

Question 3: Report to the managing partner of SBF

Introduction

In the given case, Kate Hammond, one of the audit seniors, was responsible for reviewing the operations

of the FFA subsidiary in Western Australia called TRC. Though the company has been a market leader in

WA and possesses a strong balance sheet, still it has been suffering losses from the past 2 years and

therefore the company decided to upgrade the accounting information system for effectively managing

the inventory sales and this was done through hiring one of the well regarded IT consultant and it was

completed on 31st March 2018 (Hines, 1989).

[Type here]

American Accounting

Association Model Decision-making process

integrity and objectivity in his approach, should possess professional

competence and practice due care while working. He should have

professional behaviour and must maintain confidentiality.

Furthermore, it is also mentioned that while working, he may

encounter a number of threats which may have a direct or indirect

bearing on his work and therefore there should be adequate

safeguards in those regards (Knechel & Salterio, 2016). Here in given

case, the revenue recognition principle and the value of the auditors

while reviewing and preparing the audit report of client is in question.

Reporting the issue in Key Audit Matters and forbidding to threaten

the audit senior should be the ideal scenario as per the rules

(Bromwich & Scapens, 2016).

4. Specify the alternatives

Ideally, the senior audit partner should give a recommendation to the

client on the correct revenue accounting and revenue recognition

practices and report the current practices as “Key audit matters” in the

audit report and should report this issue as a deficiency and revise the

working in the current period of audit and thereby report the correct

number (Hepp, 2018). Secondly the audit partner is not supposed to

undermine the objectivity, integrity and independence of audit senior

or to threaten or intimidate him on grounds of promotion to do

unethical work. The other alternative could be to wait for next year for

the audit partner to be changed or to report the issue to another

senior partner of the firm on the issue (Fukukawa & Mock, 2011).

5. Compare values and

alternatives

Out of all the given values and alternatives, the one which is most

viable is to report the issue as KMA and ask the client to change the

revenue recognition accounting policies and revising the work in the

current year itself.

6. Assess the consequences

IN case the corrections are not reported, it will account to window

dressing of the financials and giving wrong information to the

stakeholders and shareholders, which might further lead to wrong

investment and other decisions (Kew & Stredwick, 2017).

7. Make your decision The final decision should be to report the issue as KMA and ask the

client to change the revenue recognition accounting policies.

Question 3: Report to the managing partner of SBF

Introduction

In the given case, Kate Hammond, one of the audit seniors, was responsible for reviewing the operations

of the FFA subsidiary in Western Australia called TRC. Though the company has been a market leader in

WA and possesses a strong balance sheet, still it has been suffering losses from the past 2 years and

therefore the company decided to upgrade the accounting information system for effectively managing

the inventory sales and this was done through hiring one of the well regarded IT consultant and it was

completed on 31st March 2018 (Hines, 1989).

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

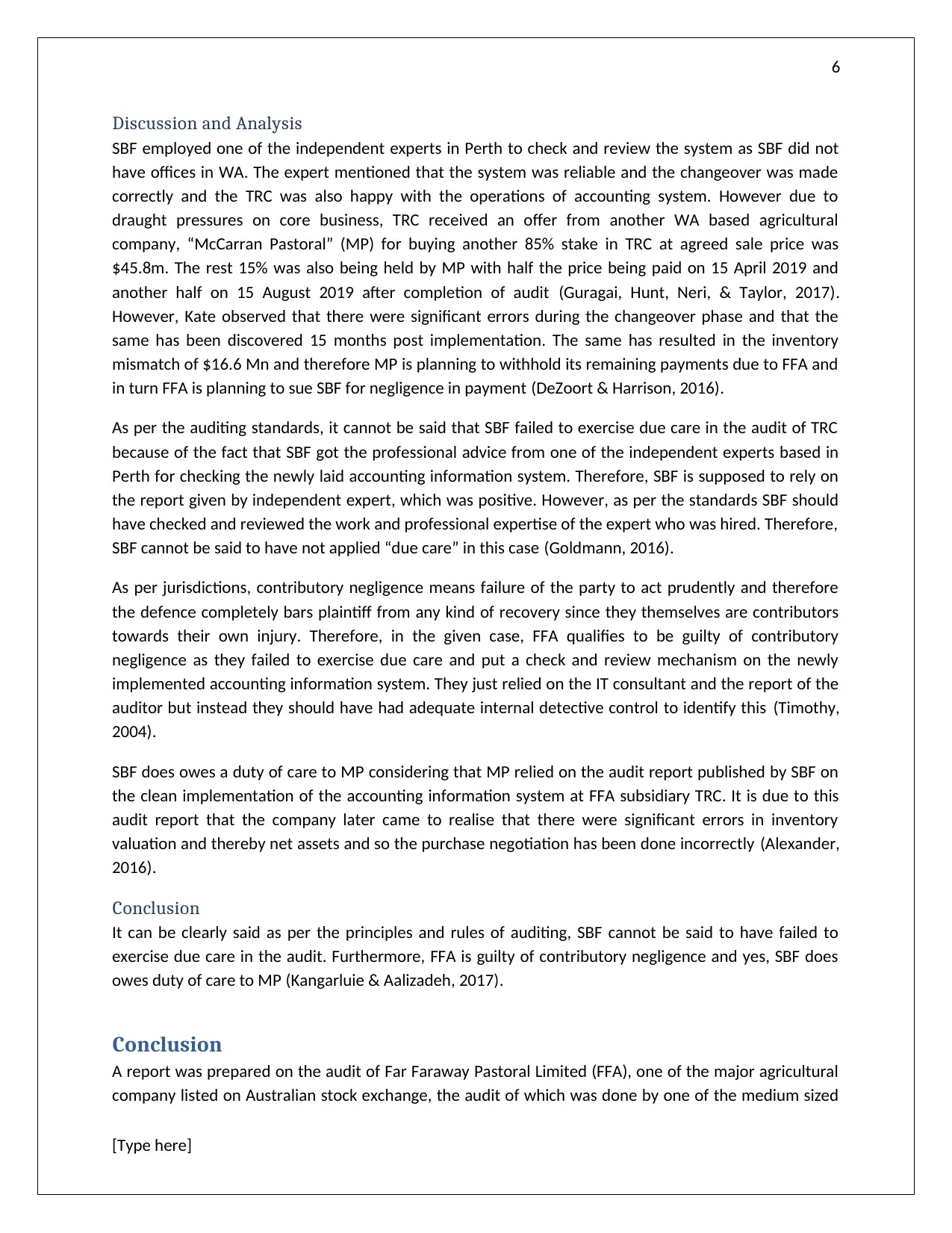

Discussion and Analysis

SBF employed one of the independent experts in Perth to check and review the system as SBF did not

have offices in WA. The expert mentioned that the system was reliable and the changeover was made

correctly and the TRC was also happy with the operations of accounting system. However due to

draught pressures on core business, TRC received an offer from another WA based agricultural

company, “McCarran Pastoral” (MP) for buying another 85% stake in TRC at agreed sale price was

$45.8m. The rest 15% was also being held by MP with half the price being paid on 15 April 2019 and

another half on 15 August 2019 after completion of audit (Guragai, Hunt, Neri, & Taylor, 2017).

However, Kate observed that there were significant errors during the changeover phase and that the

same has been discovered 15 months post implementation. The same has resulted in the inventory

mismatch of $16.6 Mn and therefore MP is planning to withhold its remaining payments due to FFA and

in turn FFA is planning to sue SBF for negligence in payment (DeZoort & Harrison, 2016).

As per the auditing standards, it cannot be said that SBF failed to exercise due care in the audit of TRC

because of the fact that SBF got the professional advice from one of the independent experts based in

Perth for checking the newly laid accounting information system. Therefore, SBF is supposed to rely on

the report given by independent expert, which was positive. However, as per the standards SBF should

have checked and reviewed the work and professional expertise of the expert who was hired. Therefore,

SBF cannot be said to have not applied “due care” in this case (Goldmann, 2016).

As per jurisdictions, contributory negligence means failure of the party to act prudently and therefore

the defence completely bars plaintiff from any kind of recovery since they themselves are contributors

towards their own injury. Therefore, in the given case, FFA qualifies to be guilty of contributory

negligence as they failed to exercise due care and put a check and review mechanism on the newly

implemented accounting information system. They just relied on the IT consultant and the report of the

auditor but instead they should have had adequate internal detective control to identify this (Timothy,

2004).

SBF does owes a duty of care to MP considering that MP relied on the audit report published by SBF on

the clean implementation of the accounting information system at FFA subsidiary TRC. It is due to this

audit report that the company later came to realise that there were significant errors in inventory

valuation and thereby net assets and so the purchase negotiation has been done incorrectly (Alexander,

2016).

Conclusion

It can be clearly said as per the principles and rules of auditing, SBF cannot be said to have failed to

exercise due care in the audit. Furthermore, FFA is guilty of contributory negligence and yes, SBF does

owes duty of care to MP (Kangarluie & Aalizadeh, 2017).

Conclusion

A report was prepared on the audit of Far Faraway Pastoral Limited (FFA), one of the major agricultural

company listed on Australian stock exchange, the audit of which was done by one of the medium sized

[Type here]

Discussion and Analysis

SBF employed one of the independent experts in Perth to check and review the system as SBF did not

have offices in WA. The expert mentioned that the system was reliable and the changeover was made

correctly and the TRC was also happy with the operations of accounting system. However due to

draught pressures on core business, TRC received an offer from another WA based agricultural

company, “McCarran Pastoral” (MP) for buying another 85% stake in TRC at agreed sale price was

$45.8m. The rest 15% was also being held by MP with half the price being paid on 15 April 2019 and

another half on 15 August 2019 after completion of audit (Guragai, Hunt, Neri, & Taylor, 2017).

However, Kate observed that there were significant errors during the changeover phase and that the

same has been discovered 15 months post implementation. The same has resulted in the inventory

mismatch of $16.6 Mn and therefore MP is planning to withhold its remaining payments due to FFA and

in turn FFA is planning to sue SBF for negligence in payment (DeZoort & Harrison, 2016).

As per the auditing standards, it cannot be said that SBF failed to exercise due care in the audit of TRC

because of the fact that SBF got the professional advice from one of the independent experts based in

Perth for checking the newly laid accounting information system. Therefore, SBF is supposed to rely on

the report given by independent expert, which was positive. However, as per the standards SBF should

have checked and reviewed the work and professional expertise of the expert who was hired. Therefore,

SBF cannot be said to have not applied “due care” in this case (Goldmann, 2016).

As per jurisdictions, contributory negligence means failure of the party to act prudently and therefore

the defence completely bars plaintiff from any kind of recovery since they themselves are contributors

towards their own injury. Therefore, in the given case, FFA qualifies to be guilty of contributory

negligence as they failed to exercise due care and put a check and review mechanism on the newly

implemented accounting information system. They just relied on the IT consultant and the report of the

auditor but instead they should have had adequate internal detective control to identify this (Timothy,

2004).

SBF does owes a duty of care to MP considering that MP relied on the audit report published by SBF on

the clean implementation of the accounting information system at FFA subsidiary TRC. It is due to this

audit report that the company later came to realise that there were significant errors in inventory

valuation and thereby net assets and so the purchase negotiation has been done incorrectly (Alexander,

2016).

Conclusion

It can be clearly said as per the principles and rules of auditing, SBF cannot be said to have failed to

exercise due care in the audit. Furthermore, FFA is guilty of contributory negligence and yes, SBF does

owes duty of care to MP (Kangarluie & Aalizadeh, 2017).

Conclusion

A report was prepared on the audit of Far Faraway Pastoral Limited (FFA), one of the major agricultural

company listed on Australian stock exchange, the audit of which was done by one of the medium sized

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

accounting and auditing firm Samway Baker Fitzgerald (SBF), but during the course of audit, several

potential and ethical issues are being pointed out by the audit seniors who are on job. The same has

been explained and analysed for its validity and to check if there is any breach of the laws and

regulations by the company. The company is facing several ethical issues in terms of board composition,

revenue accounting and laying of accounting information system and suggestion, recommendation and

ideal course of scenario has been given for all the respective scenarios.

[Type here]

accounting and auditing firm Samway Baker Fitzgerald (SBF), but during the course of audit, several

potential and ethical issues are being pointed out by the audit seniors who are on job. The same has

been explained and analysed for its validity and to check if there is any breach of the laws and

regulations by the company. The company is facing several ethical issues in terms of board composition,

revenue accounting and laying of accounting information system and suggestion, recommendation and

ideal course of scenario has been given for all the respective scenarios.

[Type here]

8

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Boccia, F., & Leonardi, R. (2016). The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models, 1-16.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), 1-9.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Defond, M., & Lennox, C. (2017). Do PCAOB Inspections Improve the Quality of Internal Control Audits?

Journal of Accounting Research, 55(3), 591-627.

DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting fraud

within organization. Journal of Business Ethics, 1-18.

Dopuch, N., & Sunder, S. (1980). FASB's Statement on Objectives and Elements of Financial Accounting:

A Review. The Accounting Review, 1(1), 16-18.

Fukukawa, H., & Mock, T. (2011). Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), 75-99.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Guragai, B., Hunt, N., Neri, M., & Taylor, E. (2017). Accounting Information Systems and Ethics Research:

Review, Synthesis, and the Future. Journal of Information Systems: Summer 2017, 31(2), 65-81.

Hepp, J. (2018). ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), 49-51.

Hines, R. (1989). Financial Accounting Knowledge, Conceptual Framework Projects and the Social

Construction of the Accounting Profession. Accounting, Auditing & Accountability Journal, 2(2),

72-92.

Kangarluie, S., & Aalizadeh, A. (2017). 'The expectation gap in auditing. Accounting, 3(1), 19-22.

[Type here]

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Boccia, F., & Leonardi, R. (2016). The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models, 1-16.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), 1-9.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Defond, M., & Lennox, C. (2017). Do PCAOB Inspections Improve the Quality of Internal Control Audits?

Journal of Accounting Research, 55(3), 591-627.

DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting fraud

within organization. Journal of Business Ethics, 1-18.

Dopuch, N., & Sunder, S. (1980). FASB's Statement on Objectives and Elements of Financial Accounting:

A Review. The Accounting Review, 1(1), 16-18.

Fukukawa, H., & Mock, T. (2011). Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), 75-99.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Guragai, B., Hunt, N., Neri, M., & Taylor, E. (2017). Accounting Information Systems and Ethics Research:

Review, Synthesis, and the Future. Journal of Information Systems: Summer 2017, 31(2), 65-81.

Hepp, J. (2018). ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), 49-51.

Hines, R. (1989). Financial Accounting Knowledge, Conceptual Framework Projects and the Social

Construction of the Accounting Profession. Accounting, Auditing & Accountability Journal, 2(2),

72-92.

Kangarluie, S., & Aalizadeh, A. (2017). 'The expectation gap in auditing. Accounting, 3(1), 19-22.

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (2nd ed.).

London: Chartered Institute of Personnel and Development.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Kuhn, J., & Morris, B. (2016). IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

Timothy, G. (2004). Managing interest rate risk in a rising rate environment. RMA Journal, Risk

Management Association (RMA), 3(1), 29-41.

Vieira, R., O’Dwyer, B., & Schneider, R. (2017). Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1), 23-48.

[Type here]

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (2nd ed.).

London: Chartered Institute of Personnel and Development.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Kuhn, J., & Morris, B. (2016). IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

Timothy, G. (2004). Managing interest rate risk in a rising rate environment. RMA Journal, Risk

Management Association (RMA), 3(1), 29-41.

Vieira, R., O’Dwyer, B., & Schneider, R. (2017). Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1), 23-48.

[Type here]

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.