Analysis of Audit Planning and Financial Statements

VerifiedAdded on 2020/03/16

|16

|3349

|61

Report

AI Summary

This report provides a comprehensive analysis of audit planning, analytical review, and financial statement analysis for Chamoisee Enterprises. It begins with an overview of audit planning, emphasizing its importance in guiding the audit process, identifying key areas for detailed examination, and assessing the risk of distorted financial information. The report then delves into analytical review procedures, including ratio analysis and trend analysis, applied to selected accounts such as consultancy fees, bank charges, interest income, sales, depreciation, cost of sales, and superannuation. A preliminary judgment of materiality is established, with specific materiality percentages suggested for key items. Each selected account is examined, including rationale for selection, relevant assertions, and recommended audit procedures. The analysis highlights significant changes and potential risks, providing insights into the financial health of the company and guiding the auditor's approach. The report emphasizes the importance of accuracy, reliability, and the application of professional judgment throughout the audit process, offering a detailed framework for financial statement analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

PLANNING OF AUDIT...................................................................................................................................4

ANALYTICAL REVIEW...............................................................................................................................4

PRELIMINARY JUDGMENT OF MATERIALITY............................................................................................5

CONSULTANCY FEES....................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

BANK CHARGES...........................................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

INTEREST INCOME.......................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................7

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

SALES...........................................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

DEPRECIATION.............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

COST OF SALES............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................9

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

SUPERANNUATION......................................................................................................................................9

RATIONALE FOR SELECTION....................................................................................................................9

PLANNING OF AUDIT...................................................................................................................................4

ANALYTICAL REVIEW...............................................................................................................................4

PRELIMINARY JUDGMENT OF MATERIALITY............................................................................................5

CONSULTANCY FEES....................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

BANK CHARGES...........................................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

INTEREST INCOME.......................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................7

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

SALES...........................................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

DEPRECIATION.............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

COST OF SALES............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................9

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

SUPERANNUATION......................................................................................................................................9

RATIONALE FOR SELECTION....................................................................................................................9

ASSERTION AND EXPLANATION...............................................................................................................9

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

REFERENCES................................................................................................................................................9

APPENDIX..................................................................................................................................................11

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

REFERENCES................................................................................................................................................9

APPENDIX..................................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PLANNING OF AUDIT

Audit planning is the first stage of the process of the audit. It is regarded as the main part of the whole

process of the audit. It is because the whole process of the audit depends upon the planning only and

that shall be done with the due care and professional responsibilities. The first basic aim of the audit

planning is to equip the auditors with the understanding as to how to conduct the audit, what things are

required to be kept in mind and in the audit documentation while conducting the audit, which areas are

required to be checked in detail and which items as stated in the financial statements has the high

probability of providing the distorted information to the users of the financial statements and etc. In the

given case, company – Chamoisee Enterprises has been provided for analyzing. The second main aim of

the audit planning is to conduct the preliminary analytical review procedures and substantive tests

(Leung, Coram, Copper and Richardson, 2015). The aforesaid two tests are performed to have the

detailed analysis of the financial statements with regard to the accounting ratios and the trend analysis

over the past two years.

ANALYTICAL REVIEW

The analytical review is defined as having the analysis of the financial statements of the company in an

analytical manner. This analytical analysis consists of the two set of processes. First process is known as

the ratio analysis and the second process is known as the analysis through trend or movement in the

items of the financial statements for the last two or three years. The first process is the ratio analysis

and it informs the nature of relationship between two or more items of the financial statements and

describe as to why the figure of the ratio sometimes justifies that the auditor is required to undertake

the audit procedures which are in addition to the normal and defined audit procedures. These

procedures are normally undertaken to ensure that the items as stated in the financial statements of the

company is accurate, complete and authentic (Abidin and Baabbad, 2015).

The other process is the trend analysis. Trend describes the movement of the items of the financial

statements over the past two or three years. The trend may be positive one or negative one. In simple

words, the trend analysis may be upward or downward depending upon the results and the

circumstances. It helps the auditor in considering the reasons for having such an increasing or

decreasing trend during the planning of an audit and laid down the audit procedures which are required

to be followed by the audit team (Glover, Prawitt and Drake, 2014). In this report of the company

Audit planning is the first stage of the process of the audit. It is regarded as the main part of the whole

process of the audit. It is because the whole process of the audit depends upon the planning only and

that shall be done with the due care and professional responsibilities. The first basic aim of the audit

planning is to equip the auditors with the understanding as to how to conduct the audit, what things are

required to be kept in mind and in the audit documentation while conducting the audit, which areas are

required to be checked in detail and which items as stated in the financial statements has the high

probability of providing the distorted information to the users of the financial statements and etc. In the

given case, company – Chamoisee Enterprises has been provided for analyzing. The second main aim of

the audit planning is to conduct the preliminary analytical review procedures and substantive tests

(Leung, Coram, Copper and Richardson, 2015). The aforesaid two tests are performed to have the

detailed analysis of the financial statements with regard to the accounting ratios and the trend analysis

over the past two years.

ANALYTICAL REVIEW

The analytical review is defined as having the analysis of the financial statements of the company in an

analytical manner. This analytical analysis consists of the two set of processes. First process is known as

the ratio analysis and the second process is known as the analysis through trend or movement in the

items of the financial statements for the last two or three years. The first process is the ratio analysis

and it informs the nature of relationship between two or more items of the financial statements and

describe as to why the figure of the ratio sometimes justifies that the auditor is required to undertake

the audit procedures which are in addition to the normal and defined audit procedures. These

procedures are normally undertaken to ensure that the items as stated in the financial statements of the

company is accurate, complete and authentic (Abidin and Baabbad, 2015).

The other process is the trend analysis. Trend describes the movement of the items of the financial

statements over the past two or three years. The trend may be positive one or negative one. In simple

words, the trend analysis may be upward or downward depending upon the results and the

circumstances. It helps the auditor in considering the reasons for having such an increasing or

decreasing trend during the planning of an audit and laid down the audit procedures which are required

to be followed by the audit team (Glover, Prawitt and Drake, 2014). In this report of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chamoisee Enterprises, seven accounts has been selected for the purpose of the analysis and which

includes consultancy fees, bank charges, interest income, sales, depreciation, cost of sales and

superannuation has been listed and described and has been accordingly analysed. (ACCA, 2016).

PRELIMINARY JUDGMENT OF MATERIALITY

Materiality concept is the key concept in the management subject as well as in the area of

financial accounting and financial auditing. In the latter case, materiality concept focuses on the

items which have material or significant effect on the financial results and operations of the

company. Preliminary judgment means judgment before start of the audit which is during the

planning of audit. During planning, the auditor through the analytical review identifies the

material items and their likely effect on the financial position and the financial performance of

the company (Chen and Tsay, 2017).

The auditor is required to apply his professional skills and due care while judging for the

materiality. It is required because every head in the financial statements has its own significance

and therefore, the materiality of each head shall be considered. In the given case of the company,

the cost of sales has been considerably increased from 33.93% to 36.77%. Three items are

included in cost of sales- opening inventory, purchases and the closing inventory. If there is the

significant variation then the auditor is required to set the materiality percentage. It is because the

company has not provided any materiality level for each of the item stated in the financial report.

In this case the materiality percentage may be set as 35% and auditor is required to perform the

audit procedures accordingly (Mao, 2014; Langevoort, 2015 and Ullah, 2014). Similarly, for

other items also the auditor is required to set the materiality level and is required to work

accordingly.

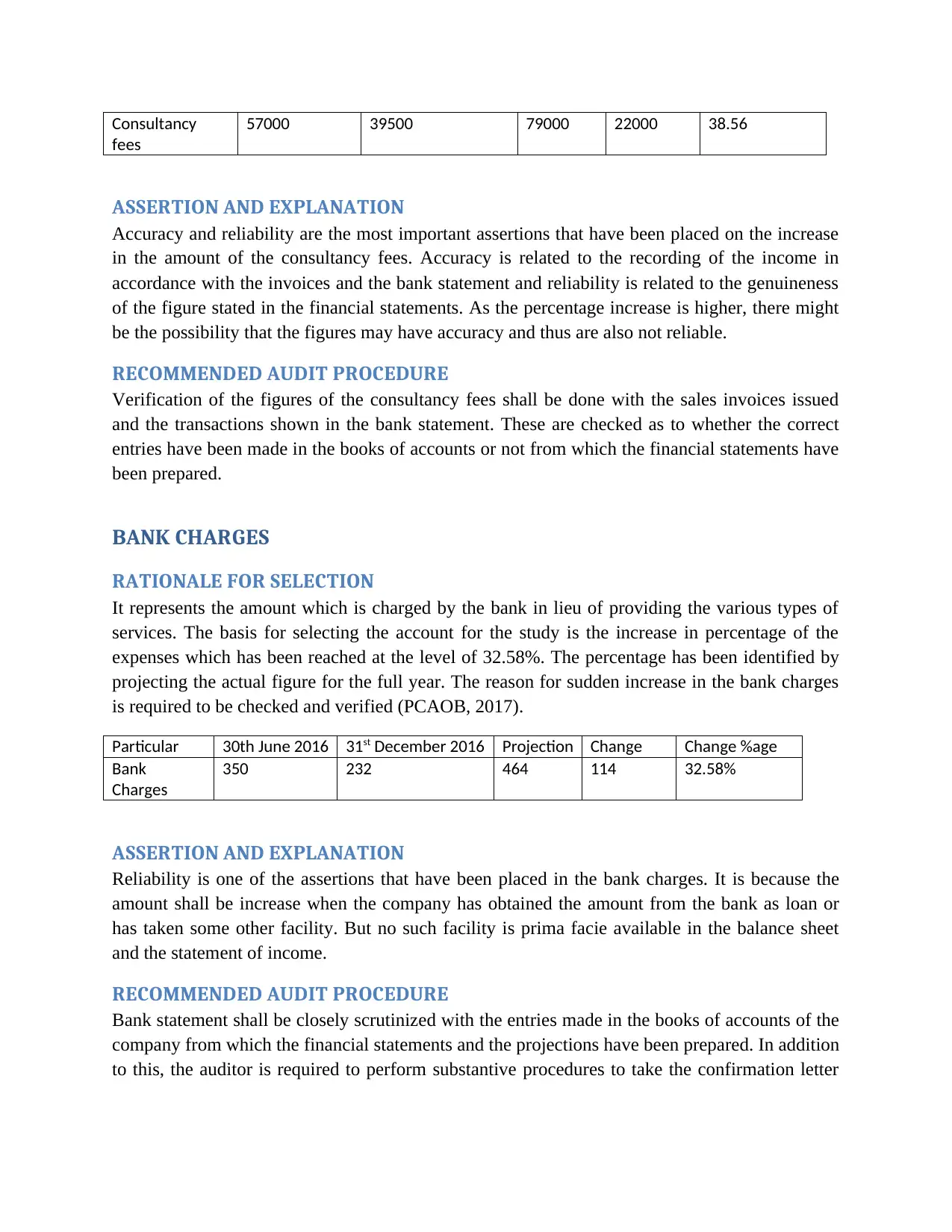

CONSULTANCY FEES

RATIONALE FOR SELECTION

First account that has been selected is the consultancy fees. Consultancy fees have undergone

sudden increase in the six months ending 31st of December 2016 and which will result to 38.56%

increase in the coming financial ending 30th of June 2017. The increase in the consultancy fees

will increase the retained earnings of the company and thus will have the effect on the equity.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

includes consultancy fees, bank charges, interest income, sales, depreciation, cost of sales and

superannuation has been listed and described and has been accordingly analysed. (ACCA, 2016).

PRELIMINARY JUDGMENT OF MATERIALITY

Materiality concept is the key concept in the management subject as well as in the area of

financial accounting and financial auditing. In the latter case, materiality concept focuses on the

items which have material or significant effect on the financial results and operations of the

company. Preliminary judgment means judgment before start of the audit which is during the

planning of audit. During planning, the auditor through the analytical review identifies the

material items and their likely effect on the financial position and the financial performance of

the company (Chen and Tsay, 2017).

The auditor is required to apply his professional skills and due care while judging for the

materiality. It is required because every head in the financial statements has its own significance

and therefore, the materiality of each head shall be considered. In the given case of the company,

the cost of sales has been considerably increased from 33.93% to 36.77%. Three items are

included in cost of sales- opening inventory, purchases and the closing inventory. If there is the

significant variation then the auditor is required to set the materiality percentage. It is because the

company has not provided any materiality level for each of the item stated in the financial report.

In this case the materiality percentage may be set as 35% and auditor is required to perform the

audit procedures accordingly (Mao, 2014; Langevoort, 2015 and Ullah, 2014). Similarly, for

other items also the auditor is required to set the materiality level and is required to work

accordingly.

CONSULTANCY FEES

RATIONALE FOR SELECTION

First account that has been selected is the consultancy fees. Consultancy fees have undergone

sudden increase in the six months ending 31st of December 2016 and which will result to 38.56%

increase in the coming financial ending 30th of June 2017. The increase in the consultancy fees

will increase the retained earnings of the company and thus will have the effect on the equity.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Consultancy

fees

57000 39500 79000 22000 38.56

ASSERTION AND EXPLANATION

Accuracy and reliability are the most important assertions that have been placed on the increase

in the amount of the consultancy fees. Accuracy is related to the recording of the income in

accordance with the invoices and the bank statement and reliability is related to the genuineness

of the figure stated in the financial statements. As the percentage increase is higher, there might

be the possibility that the figures may have accuracy and thus are also not reliable.

RECOMMENDED AUDIT PROCEDURE

Verification of the figures of the consultancy fees shall be done with the sales invoices issued

and the transactions shown in the bank statement. These are checked as to whether the correct

entries have been made in the books of accounts or not from which the financial statements have

been prepared.

BANK CHARGES

RATIONALE FOR SELECTION

It represents the amount which is charged by the bank in lieu of providing the various types of

services. The basis for selecting the account for the study is the increase in percentage of the

expenses which has been reached at the level of 32.58%. The percentage has been identified by

projecting the actual figure for the full year. The reason for sudden increase in the bank charges

is required to be checked and verified (PCAOB, 2017).

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Bank

Charges

350 232 464 114 32.58%

ASSERTION AND EXPLANATION

Reliability is one of the assertions that have been placed in the bank charges. It is because the

amount shall be increase when the company has obtained the amount from the bank as loan or

has taken some other facility. But no such facility is prima facie available in the balance sheet

and the statement of income.

RECOMMENDED AUDIT PROCEDURE

Bank statement shall be closely scrutinized with the entries made in the books of accounts of the

company from which the financial statements and the projections have been prepared. In addition

to this, the auditor is required to perform substantive procedures to take the confirmation letter

fees

57000 39500 79000 22000 38.56

ASSERTION AND EXPLANATION

Accuracy and reliability are the most important assertions that have been placed on the increase

in the amount of the consultancy fees. Accuracy is related to the recording of the income in

accordance with the invoices and the bank statement and reliability is related to the genuineness

of the figure stated in the financial statements. As the percentage increase is higher, there might

be the possibility that the figures may have accuracy and thus are also not reliable.

RECOMMENDED AUDIT PROCEDURE

Verification of the figures of the consultancy fees shall be done with the sales invoices issued

and the transactions shown in the bank statement. These are checked as to whether the correct

entries have been made in the books of accounts or not from which the financial statements have

been prepared.

BANK CHARGES

RATIONALE FOR SELECTION

It represents the amount which is charged by the bank in lieu of providing the various types of

services. The basis for selecting the account for the study is the increase in percentage of the

expenses which has been reached at the level of 32.58%. The percentage has been identified by

projecting the actual figure for the full year. The reason for sudden increase in the bank charges

is required to be checked and verified (PCAOB, 2017).

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Bank

Charges

350 232 464 114 32.58%

ASSERTION AND EXPLANATION

Reliability is one of the assertions that have been placed in the bank charges. It is because the

amount shall be increase when the company has obtained the amount from the bank as loan or

has taken some other facility. But no such facility is prima facie available in the balance sheet

and the statement of income.

RECOMMENDED AUDIT PROCEDURE

Bank statement shall be closely scrutinized with the entries made in the books of accounts of the

company from which the financial statements and the projections have been prepared. In addition

to this, the auditor is required to perform substantive procedures to take the confirmation letter

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

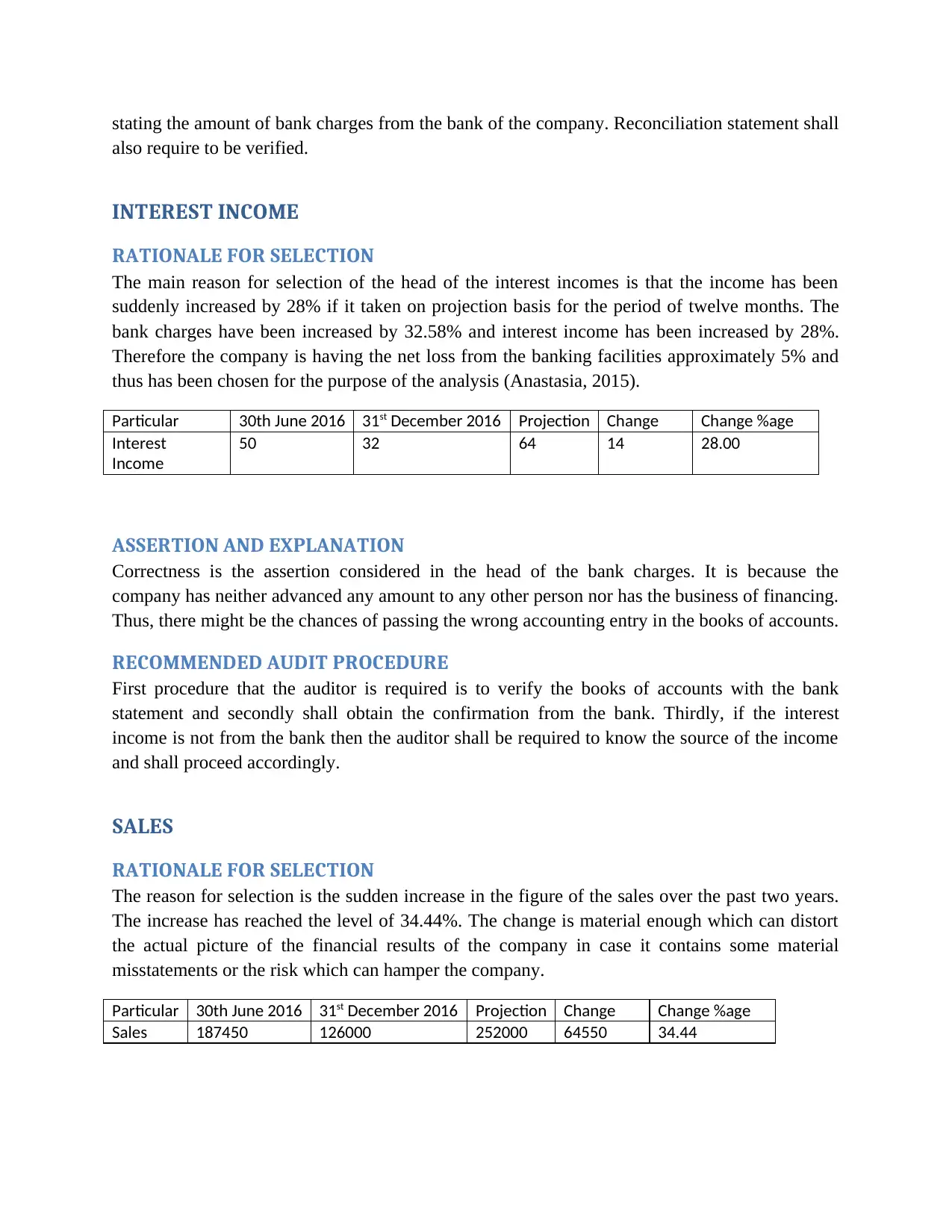

stating the amount of bank charges from the bank of the company. Reconciliation statement shall

also require to be verified.

INTEREST INCOME

RATIONALE FOR SELECTION

The main reason for selection of the head of the interest incomes is that the income has been

suddenly increased by 28% if it taken on projection basis for the period of twelve months. The

bank charges have been increased by 32.58% and interest income has been increased by 28%.

Therefore the company is having the net loss from the banking facilities approximately 5% and

thus has been chosen for the purpose of the analysis (Anastasia, 2015).

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Interest

Income

50 32 64 14 28.00

ASSERTION AND EXPLANATION

Correctness is the assertion considered in the head of the bank charges. It is because the

company has neither advanced any amount to any other person nor has the business of financing.

Thus, there might be the chances of passing the wrong accounting entry in the books of accounts.

RECOMMENDED AUDIT PROCEDURE

First procedure that the auditor is required is to verify the books of accounts with the bank

statement and secondly shall obtain the confirmation from the bank. Thirdly, if the interest

income is not from the bank then the auditor shall be required to know the source of the income

and shall proceed accordingly.

SALES

RATIONALE FOR SELECTION

The reason for selection is the sudden increase in the figure of the sales over the past two years.

The increase has reached the level of 34.44%. The change is material enough which can distort

the actual picture of the financial results of the company in case it contains some material

misstatements or the risk which can hamper the company.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Sales 187450 126000 252000 64550 34.44

also require to be verified.

INTEREST INCOME

RATIONALE FOR SELECTION

The main reason for selection of the head of the interest incomes is that the income has been

suddenly increased by 28% if it taken on projection basis for the period of twelve months. The

bank charges have been increased by 32.58% and interest income has been increased by 28%.

Therefore the company is having the net loss from the banking facilities approximately 5% and

thus has been chosen for the purpose of the analysis (Anastasia, 2015).

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Interest

Income

50 32 64 14 28.00

ASSERTION AND EXPLANATION

Correctness is the assertion considered in the head of the bank charges. It is because the

company has neither advanced any amount to any other person nor has the business of financing.

Thus, there might be the chances of passing the wrong accounting entry in the books of accounts.

RECOMMENDED AUDIT PROCEDURE

First procedure that the auditor is required is to verify the books of accounts with the bank

statement and secondly shall obtain the confirmation from the bank. Thirdly, if the interest

income is not from the bank then the auditor shall be required to know the source of the income

and shall proceed accordingly.

SALES

RATIONALE FOR SELECTION

The reason for selection is the sudden increase in the figure of the sales over the past two years.

The increase has reached the level of 34.44%. The change is material enough which can distort

the actual picture of the financial results of the company in case it contains some material

misstatements or the risk which can hamper the company.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Sales 187450 126000 252000 64550 34.44

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASSERTION AND EXPLANATION

Reliability is major assertion concerned with the sales. It is because the increase made over the

year is material and there might be the chances that the company has inflated the turnover by

following the manipulating practices (Kharisova, 2014).

RECOMMENDED AUDIT PROCEDURE

Verify each and every sale invoices with the books of accounts and shall obtain the ledger

account of the debtors including the balance confirmation as on date.

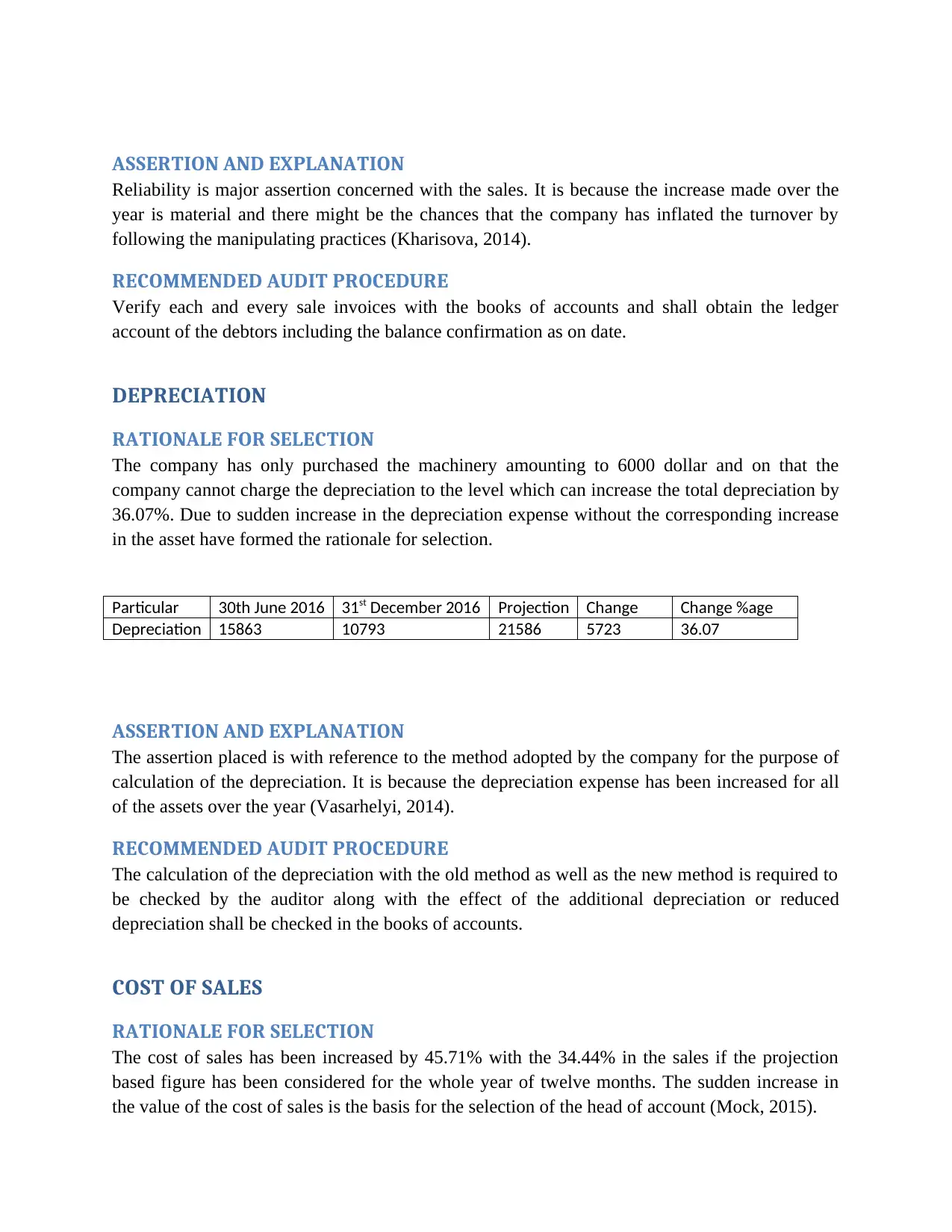

DEPRECIATION

RATIONALE FOR SELECTION

The company has only purchased the machinery amounting to 6000 dollar and on that the

company cannot charge the depreciation to the level which can increase the total depreciation by

36.07%. Due to sudden increase in the depreciation expense without the corresponding increase

in the asset have formed the rationale for selection.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Depreciation 15863 10793 21586 5723 36.07

ASSERTION AND EXPLANATION

The assertion placed is with reference to the method adopted by the company for the purpose of

calculation of the depreciation. It is because the depreciation expense has been increased for all

of the assets over the year (Vasarhelyi, 2014).

RECOMMENDED AUDIT PROCEDURE

The calculation of the depreciation with the old method as well as the new method is required to

be checked by the auditor along with the effect of the additional depreciation or reduced

depreciation shall be checked in the books of accounts.

COST OF SALES

RATIONALE FOR SELECTION

The cost of sales has been increased by 45.71% with the 34.44% in the sales if the projection

based figure has been considered for the whole year of twelve months. The sudden increase in

the value of the cost of sales is the basis for the selection of the head of account (Mock, 2015).

Reliability is major assertion concerned with the sales. It is because the increase made over the

year is material and there might be the chances that the company has inflated the turnover by

following the manipulating practices (Kharisova, 2014).

RECOMMENDED AUDIT PROCEDURE

Verify each and every sale invoices with the books of accounts and shall obtain the ledger

account of the debtors including the balance confirmation as on date.

DEPRECIATION

RATIONALE FOR SELECTION

The company has only purchased the machinery amounting to 6000 dollar and on that the

company cannot charge the depreciation to the level which can increase the total depreciation by

36.07%. Due to sudden increase in the depreciation expense without the corresponding increase

in the asset have formed the rationale for selection.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Depreciation 15863 10793 21586 5723 36.07

ASSERTION AND EXPLANATION

The assertion placed is with reference to the method adopted by the company for the purpose of

calculation of the depreciation. It is because the depreciation expense has been increased for all

of the assets over the year (Vasarhelyi, 2014).

RECOMMENDED AUDIT PROCEDURE

The calculation of the depreciation with the old method as well as the new method is required to

be checked by the auditor along with the effect of the additional depreciation or reduced

depreciation shall be checked in the books of accounts.

COST OF SALES

RATIONALE FOR SELECTION

The cost of sales has been increased by 45.71% with the 34.44% in the sales if the projection

based figure has been considered for the whole year of twelve months. The sudden increase in

the value of the cost of sales is the basis for the selection of the head of account (Mock, 2015).

Particular 30th June 2016 31st December 2016 Projection Change Change %age

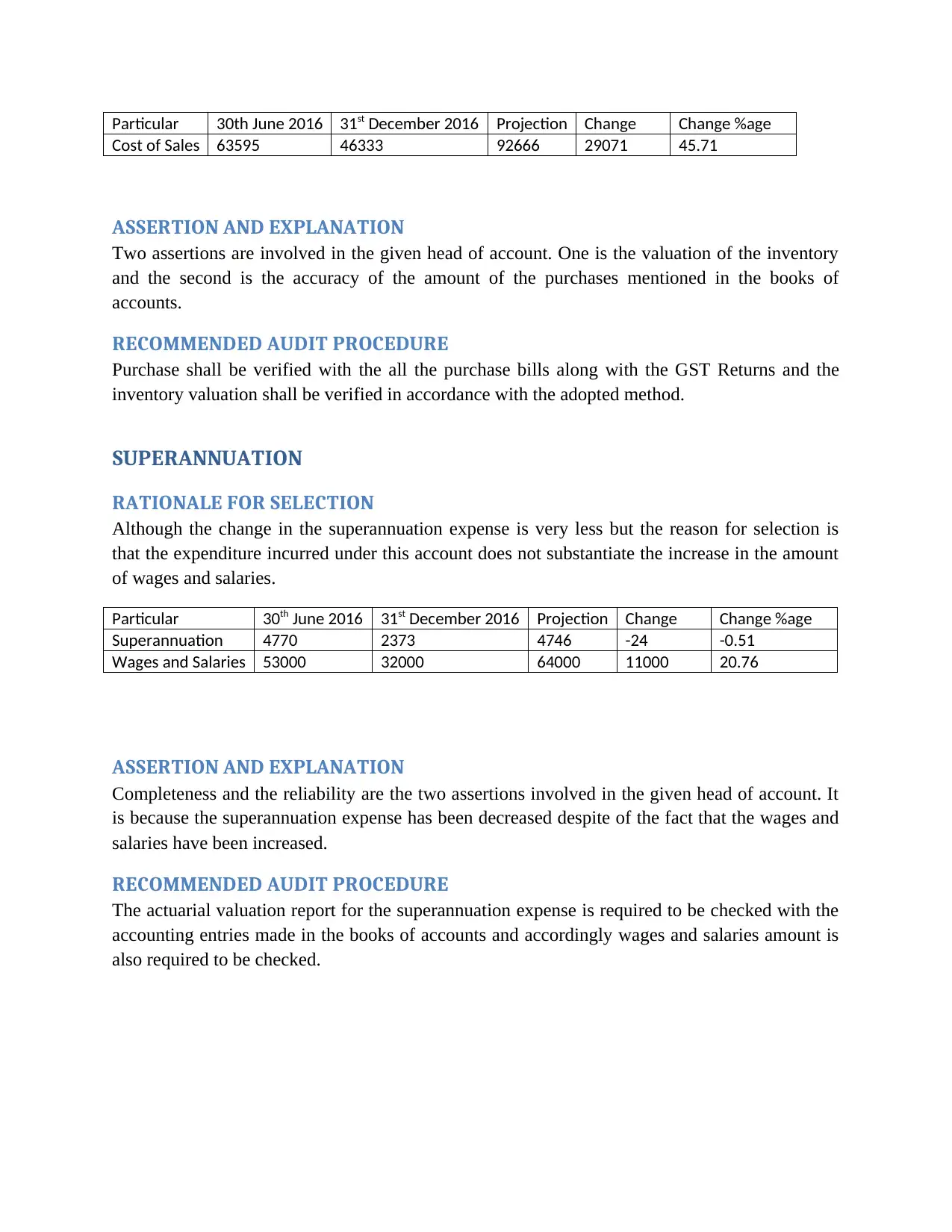

Cost of Sales 63595 46333 92666 29071 45.71

ASSERTION AND EXPLANATION

Two assertions are involved in the given head of account. One is the valuation of the inventory

and the second is the accuracy of the amount of the purchases mentioned in the books of

accounts.

RECOMMENDED AUDIT PROCEDURE

Purchase shall be verified with the all the purchase bills along with the GST Returns and the

inventory valuation shall be verified in accordance with the adopted method.

SUPERANNUATION

RATIONALE FOR SELECTION

Although the change in the superannuation expense is very less but the reason for selection is

that the expenditure incurred under this account does not substantiate the increase in the amount

of wages and salaries.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Superannuation 4770 2373 4746 -24 -0.51

Wages and Salaries 53000 32000 64000 11000 20.76

ASSERTION AND EXPLANATION

Completeness and the reliability are the two assertions involved in the given head of account. It

is because the superannuation expense has been decreased despite of the fact that the wages and

salaries have been increased.

RECOMMENDED AUDIT PROCEDURE

The actuarial valuation report for the superannuation expense is required to be checked with the

accounting entries made in the books of accounts and accordingly wages and salaries amount is

also required to be checked.

Cost of Sales 63595 46333 92666 29071 45.71

ASSERTION AND EXPLANATION

Two assertions are involved in the given head of account. One is the valuation of the inventory

and the second is the accuracy of the amount of the purchases mentioned in the books of

accounts.

RECOMMENDED AUDIT PROCEDURE

Purchase shall be verified with the all the purchase bills along with the GST Returns and the

inventory valuation shall be verified in accordance with the adopted method.

SUPERANNUATION

RATIONALE FOR SELECTION

Although the change in the superannuation expense is very less but the reason for selection is

that the expenditure incurred under this account does not substantiate the increase in the amount

of wages and salaries.

Particular 30th June 2016 31st December 2016 Projection Change Change %age

Superannuation 4770 2373 4746 -24 -0.51

Wages and Salaries 53000 32000 64000 11000 20.76

ASSERTION AND EXPLANATION

Completeness and the reliability are the two assertions involved in the given head of account. It

is because the superannuation expense has been decreased despite of the fact that the wages and

salaries have been increased.

RECOMMENDED AUDIT PROCEDURE

The actuarial valuation report for the superannuation expense is required to be checked with the

accounting entries made in the books of accounts and accordingly wages and salaries amount is

also required to be checked.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html accessed on 08-10-2017.

Abidin, S., & Baabbad, M. A. (2015), “The use of analytical procedures by yemeni

auditors”,Corporate Ownership & Control, 12(2), 17-25.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 08-10-2017

Chen, S., & Tsay, B. Y. (2017), “Refer to Materiality as a Legal Concept”. Journal of

Corporate Accounting & Finance, 28(2), 55-61.

Glover, S. M., Prawitt, D. F., & Drake, M. S. (2014), “Between a Rock and a Hard Place: A Path

Forward for Using Substantive Analytical Procedures in Auditing Large P&L

Accounts:Commentary and Analysis”. Auditing: A Journal of Practice & Theory, 34(3), 161-

179.

Kharisova, F. I., (2014), “Applying the category of Assertions (or preconditions)» in audit of

financial statement”. Mediterranean Journal of Social Sciences, 5(24), 180

Langevoort, D. C. (2015), “Judgment Day for Fraud-on-the-Market: Reflections on Amgen and

the Second Coming of Halliburton”. Ariz. L. Rev., 57, 37.

Leung P, Coram P, Copper B and Richardson P, (2015), “Modern Auditing and Assurance

Services”, Wiley John and Sons, Ed. 6, Pp 425-463, 582-684.

Mao, M., (2014), “Experimental Methods of Materiality Judgment on Auditor’s Experience

and Performance” In 3rd International Conference on Science and Social Research

(ICSSR 2014) Atlantis Press.

Mock, T. J, (2015). “Auditors' Risk Assessments: The Effects of Elicitation Approach and

Assertion Framing” Behavioral Research in Accounting, 28(2), 75-84.

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html accessed on 08-10-2017.

Abidin, S., & Baabbad, M. A. (2015), “The use of analytical procedures by yemeni

auditors”,Corporate Ownership & Control, 12(2), 17-25.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 08-10-2017

Chen, S., & Tsay, B. Y. (2017), “Refer to Materiality as a Legal Concept”. Journal of

Corporate Accounting & Finance, 28(2), 55-61.

Glover, S. M., Prawitt, D. F., & Drake, M. S. (2014), “Between a Rock and a Hard Place: A Path

Forward for Using Substantive Analytical Procedures in Auditing Large P&L

Accounts:Commentary and Analysis”. Auditing: A Journal of Practice & Theory, 34(3), 161-

179.

Kharisova, F. I., (2014), “Applying the category of Assertions (or preconditions)» in audit of

financial statement”. Mediterranean Journal of Social Sciences, 5(24), 180

Langevoort, D. C. (2015), “Judgment Day for Fraud-on-the-Market: Reflections on Amgen and

the Second Coming of Halliburton”. Ariz. L. Rev., 57, 37.

Leung P, Coram P, Copper B and Richardson P, (2015), “Modern Auditing and Assurance

Services”, Wiley John and Sons, Ed. 6, Pp 425-463, 582-684.

Mao, M., (2014), “Experimental Methods of Materiality Judgment on Auditor’s Experience

and Performance” In 3rd International Conference on Science and Social Research

(ICSSR 2014) Atlantis Press.

Mock, T. J, (2015). “Auditors' Risk Assessments: The Effects of Elicitation Approach and

Assertion Framing” Behavioral Research in Accounting, 28(2), 75-84.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PCAOB, (2017), “Analytical Procedures” available at

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 08-10-2017

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-financial -

statements/ accessed on 08-10-2017

Vasarhelyi, M. A., (2014), “Embracing the Automated Audit: How the Audit Data Standards and

Audit Tools Can Enhance Auditor Judgment and Assurance” Journal of

accountancy, 217(4), 34.

APPENDIX

Chamoisee Enterprises

Ratio Analysis

Jul 1, 2016 - Dec 31, 2016 Jul 1, 2015 - June 30, 2016

Current Assets 390,840 365,000

Current Liability 0 0

Working Capital 390,840 365,000

Cost of Sales 46,333 63,595

Sales 126,000 187,450

Costs % of Sales 36.77% 33.93%

Gross Profit 79,667 123,855

Gross Profit Margin 63.23% 66.07%

Net Profit 65,005 90,122

Sales 126,000 187,450

Net Profit Margin 51.59% 48.08%

Accounts Receivable 118,340 111,000

Sales 126,000 187,450

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 08-10-2017

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-financial -

statements/ accessed on 08-10-2017

Vasarhelyi, M. A., (2014), “Embracing the Automated Audit: How the Audit Data Standards and

Audit Tools Can Enhance Auditor Judgment and Assurance” Journal of

accountancy, 217(4), 34.

APPENDIX

Chamoisee Enterprises

Ratio Analysis

Jul 1, 2016 - Dec 31, 2016 Jul 1, 2015 - June 30, 2016

Current Assets 390,840 365,000

Current Liability 0 0

Working Capital 390,840 365,000

Cost of Sales 46,333 63,595

Sales 126,000 187,450

Costs % of Sales 36.77% 33.93%

Gross Profit 79,667 123,855

Gross Profit Margin 63.23% 66.07%

Net Profit 65,005 90,122

Sales 126,000 187,450

Net Profit Margin 51.59% 48.08%

Accounts Receivable 118,340 111,000

Sales 126,000 187,450

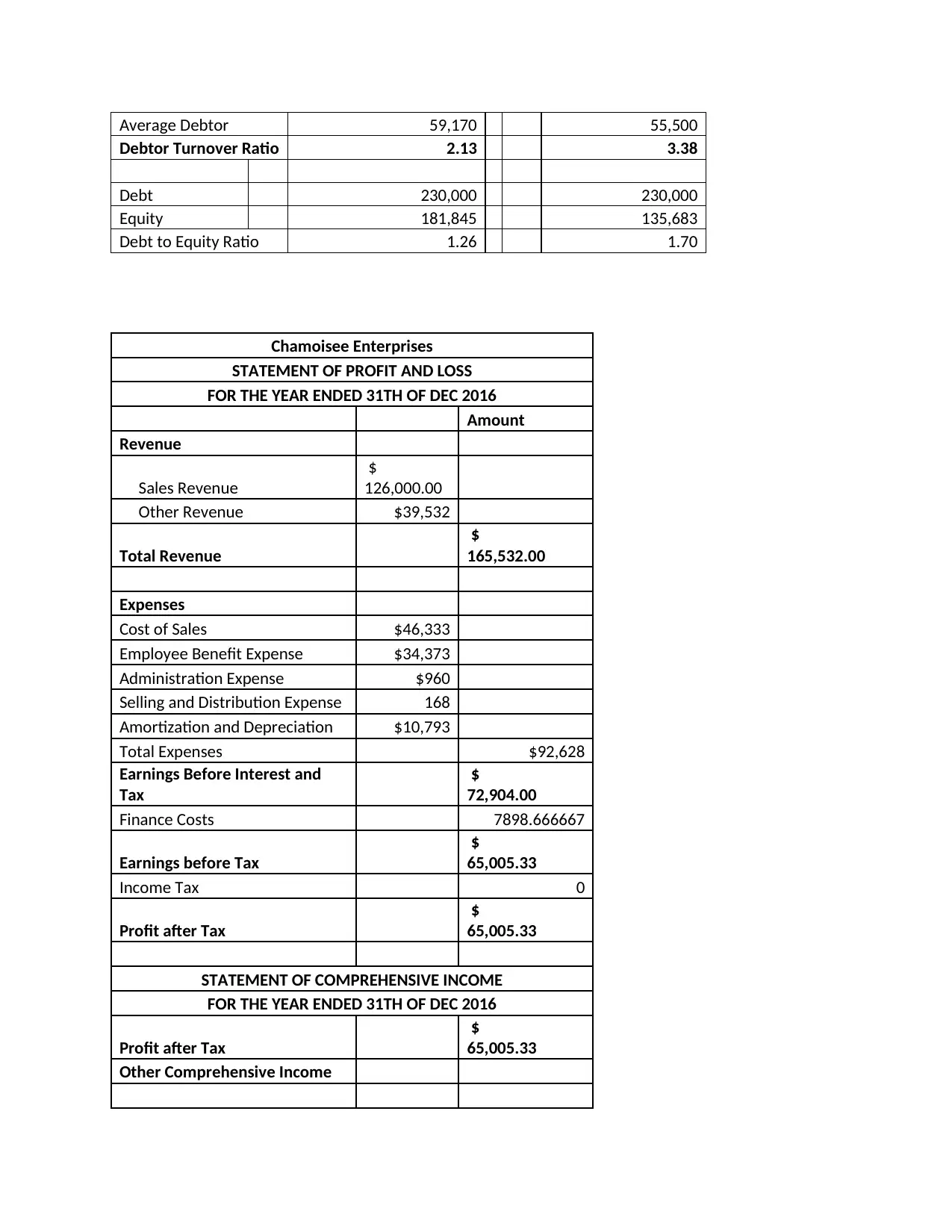

Average Debtor 59,170 55,500

Debtor Turnover Ratio 2.13 3.38

Debt 230,000 230,000

Equity 181,845 135,683

Debt to Equity Ratio 1.26 1.70

Chamoisee Enterprises

STATEMENT OF PROFIT AND LOSS

FOR THE YEAR ENDED 31TH OF DEC 2016

Amount

Revenue

Sales Revenue

$

126,000.00

Other Revenue $39,532

Total Revenue

$

165,532.00

Expenses

Cost of Sales $46,333

Employee Benefit Expense $34,373

Administration Expense $960

Selling and Distribution Expense 168

Amortization and Depreciation $10,793

Total Expenses $92,628

Earnings Before Interest and

Tax

$

72,904.00

Finance Costs 7898.666667

Earnings before Tax

$

65,005.33

Income Tax 0

Profit after Tax

$

65,005.33

STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31TH OF DEC 2016

Profit after Tax

$

65,005.33

Other Comprehensive Income

Debtor Turnover Ratio 2.13 3.38

Debt 230,000 230,000

Equity 181,845 135,683

Debt to Equity Ratio 1.26 1.70

Chamoisee Enterprises

STATEMENT OF PROFIT AND LOSS

FOR THE YEAR ENDED 31TH OF DEC 2016

Amount

Revenue

Sales Revenue

$

126,000.00

Other Revenue $39,532

Total Revenue

$

165,532.00

Expenses

Cost of Sales $46,333

Employee Benefit Expense $34,373

Administration Expense $960

Selling and Distribution Expense 168

Amortization and Depreciation $10,793

Total Expenses $92,628

Earnings Before Interest and

Tax

$

72,904.00

Finance Costs 7898.666667

Earnings before Tax

$

65,005.33

Income Tax 0

Profit after Tax

$

65,005.33

STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31TH OF DEC 2016

Profit after Tax

$

65,005.33

Other Comprehensive Income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.