Comprehensive Audit Program: Financial Reporting Analysis

VerifiedAdded on 2023/06/12

|16

|4207

|115

Report

AI Summary

This audit program analyzes a corporate entity's financial statements for the year 2017, focusing on business operations, investment and financing activities, and financial reporting practices in accordance with International Financial Reporting Standards (IFRS). Key business operations include Zinclear product growth, US manufacturing commencement, and Australian manufacturing considerations. Investment activities involve investments in subsidiaries, while financing activities focus on cash flow components. The program assesses financial performance using ratios like asset turnover, return on equity, current ratio, and gross operating margin, comparing results from 2016 to 2017 to determine the firm's efficiency and liquidity. The analysis concludes with an evaluation of the firm's ability to meet its debt obligations and maintain a true and fair view of its financial position.

Running head: AUDIT PROGRAM

Audit Program

Name of the Student:

Name of the University:

Author Note

Audit Program

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT PROGRAM

Table of Contents

Introduction......................................................................................................................................2

Business Operations.........................................................................................................................2

Investment activities........................................................................................................................4

Financing activities..........................................................................................................................4

Financial reporting practices............................................................................................................4

Auditing framework.......................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

AUDIT PROGRAM

Table of Contents

Introduction......................................................................................................................................2

Business Operations.........................................................................................................................2

Investment activities........................................................................................................................4

Financing activities..........................................................................................................................4

Financial reporting practices............................................................................................................4

Auditing framework.......................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2

AUDIT PROGRAM

Introduction

The issue that has been presented in the question refers to the fact that the accounting

statements of a corporate entity can be analyzed for the purpose of understanding the operations

of a corporate entity in regards to a single financial year. This means that the financial report of a

corporate entity describes the financial performance of the business organization. Moreover, the

stakeholders and the other investors of the corporate firms tend to understand and forecast the

business performance of the corporate entities on the basis of the financial information that has

been represented in the annual report of the firm (Raju et al. 2015). Furthermore, this kind of

financial information can be utilized for the purpose of analyzing the business operations that

have been carried out by a business entity and whether the business operations have been in

accordance to the accounting standards that have been established by the accounting regulatory

body.

This particular study aims to analyze the financial statements of a business corporation.

This means that the accounting statements of the corporate entity that has been chosen for the

purpose of the study is of the name…. The financial statements that have been chosen belong to

the financial year of 2017.

Business Operations

The certain business operations that have been carried out by the business entity refers to

the essential operations that have been carried out by the corporate firm throughout a single

financial year. These business operations can be listed down as follows:

Zinclear – the revenue in regards to the Zinclear range of products has continued to grow

in regards to the percentage of 14.32%. This means that the corporate entity has partnered

AUDIT PROGRAM

Introduction

The issue that has been presented in the question refers to the fact that the accounting

statements of a corporate entity can be analyzed for the purpose of understanding the operations

of a corporate entity in regards to a single financial year. This means that the financial report of a

corporate entity describes the financial performance of the business organization. Moreover, the

stakeholders and the other investors of the corporate firms tend to understand and forecast the

business performance of the corporate entities on the basis of the financial information that has

been represented in the annual report of the firm (Raju et al. 2015). Furthermore, this kind of

financial information can be utilized for the purpose of analyzing the business operations that

have been carried out by a business entity and whether the business operations have been in

accordance to the accounting standards that have been established by the accounting regulatory

body.

This particular study aims to analyze the financial statements of a business corporation.

This means that the accounting statements of the corporate entity that has been chosen for the

purpose of the study is of the name…. The financial statements that have been chosen belong to

the financial year of 2017.

Business Operations

The certain business operations that have been carried out by the business entity refers to

the essential operations that have been carried out by the corporate firm throughout a single

financial year. These business operations can be listed down as follows:

Zinclear – the revenue in regards to the Zinclear range of products has continued to grow

in regards to the percentage of 14.32%. This means that the corporate entity has partnered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT PROGRAM

with Devereaux Specialties for the purpose of carrying out partnership with the

distribution partner for a longer period of time. The firm also aims to grow its sales by the

financial year of 2018. ANO has aimed to build the distribution network in Europe.

Manufacturing in the US – the corporate entity of ANO has been planning to result in the

commencement of the production that will be full scale in nature in the country of US in

October 2017. The occurrence of the delays that have been technical in nature and the

equipment that have been required for the assistance in the manufacturing process

(Tuinamuana 2016). The US partners have also been helpful particularly in regards to the

R&D Department that have provided the required assistance in regards to the changes in

the production of the sunscreen. At the time of the commencement of the US

manufacturing the generation of the efficiency of the operation and has reduced the

logistic times to the Europe and US.

Australian Manufacturing – the careful consideration of the different options of

manufacturing in Australia. The management of the corporate entity has been involved in

the negotiation of the long-term lease. This particular transition has been operational in

the creation of a new equipment (Howes et al. 2015).

The financial year of 2017 has been significant for the corporate entity due to the fact that

the company of ANO has resulted in the successful filing of the three new patents. The

patents have been in regards to the products of a battery, a XPA end formulation recipe

and 3D Ceramics. The new patents have also been filled in the financial year of 2018.

It must also be further noted that the corporate entity of ANO has resulted in the

development of a network of chemists that have been global in nature. The corporate

entity had developed a network of 28 chemists with 11 chemists. In the current times, the

AUDIT PROGRAM

with Devereaux Specialties for the purpose of carrying out partnership with the

distribution partner for a longer period of time. The firm also aims to grow its sales by the

financial year of 2018. ANO has aimed to build the distribution network in Europe.

Manufacturing in the US – the corporate entity of ANO has been planning to result in the

commencement of the production that will be full scale in nature in the country of US in

October 2017. The occurrence of the delays that have been technical in nature and the

equipment that have been required for the assistance in the manufacturing process

(Tuinamuana 2016). The US partners have also been helpful particularly in regards to the

R&D Department that have provided the required assistance in regards to the changes in

the production of the sunscreen. At the time of the commencement of the US

manufacturing the generation of the efficiency of the operation and has reduced the

logistic times to the Europe and US.

Australian Manufacturing – the careful consideration of the different options of

manufacturing in Australia. The management of the corporate entity has been involved in

the negotiation of the long-term lease. This particular transition has been operational in

the creation of a new equipment (Howes et al. 2015).

The financial year of 2017 has been significant for the corporate entity due to the fact that

the company of ANO has resulted in the successful filing of the three new patents. The

patents have been in regards to the products of a battery, a XPA end formulation recipe

and 3D Ceramics. The new patents have also been filled in the financial year of 2018.

It must also be further noted that the corporate entity of ANO has resulted in the

development of a network of chemists that have been global in nature. The corporate

entity had developed a network of 28 chemists with 11 chemists. In the current times, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT PROGRAM

corporate entity have developed 29 end formulations. The cost in regards to the

development of the project has been anticipated to be less than $500,000 includes the

approvals that are fully regulated in nature.

Investment activities

The investment activities that have been carried out by the corporate entities is that the

corporate entity has resulted in the investment in the subsidiaries and have been accounted for at

cost in the accounting statements in the books of the business entity. The investment activities

that have been included in the corporate accounting statements refer to the fact that the particular

amounts that have been included are the financial components of the purchase of the property,

plant and equipment (Lakhanpal et al. 2015). The other financial components are the payment in

regards to the development of the assets and the net amount of cash that has been used in regards

to the investing activities.

Financing activities

The financial component that has been included in the financing activities in the cash

flow statement of the corporate entity are the increase or decrease in regards to the cash and cash

equivalents. Moreover, the component of cash and cash equivalents have also been included in

the annual report of the corporate entity (Lehner et al. 2018). The next financial component that

has been included in the cash flow from the financing activities include the adjustment in regards

to the rate of exchange. The cash and cash equivalent that has resulted from the financial

components at the end of the financial year amount to $908,287.

AUDIT PROGRAM

corporate entity have developed 29 end formulations. The cost in regards to the

development of the project has been anticipated to be less than $500,000 includes the

approvals that are fully regulated in nature.

Investment activities

The investment activities that have been carried out by the corporate entities is that the

corporate entity has resulted in the investment in the subsidiaries and have been accounted for at

cost in the accounting statements in the books of the business entity. The investment activities

that have been included in the corporate accounting statements refer to the fact that the particular

amounts that have been included are the financial components of the purchase of the property,

plant and equipment (Lakhanpal et al. 2015). The other financial components are the payment in

regards to the development of the assets and the net amount of cash that has been used in regards

to the investing activities.

Financing activities

The financial component that has been included in the financing activities in the cash

flow statement of the corporate entity are the increase or decrease in regards to the cash and cash

equivalents. Moreover, the component of cash and cash equivalents have also been included in

the annual report of the corporate entity (Lehner et al. 2018). The next financial component that

has been included in the cash flow from the financing activities include the adjustment in regards

to the rate of exchange. The cash and cash equivalent that has resulted from the financial

components at the end of the financial year amount to $908,287.

5

AUDIT PROGRAM

Financial reporting practices

The financial reporting practices that have been included in the accounting statements of

the corporate entity refer to the fact that the accounting statements or the books of accounts have

been prepared on the basis of the International Financial Reporting Standards. This means that

the books that have been prepared by the accounting body, are based upon the accounting

guidelines, that are issued by the accounting regulatory body of International Accounting

Standards Board. These accounting standards are known as the International Financial Reporting

Standards. Furthermore, the declarations or the assertions that have been included in the financial

report of the corporate entity can be listed down as follows:

The compliance with the accounting standards, which has been included in the basis of

preparation of the financial statements, has been stated accounting statements the

International Financial Reporting Standards.

The accounting statements that have been included tend to give a fair and true image of

the accounting statements of the corporate entity.

It has been further mentioned in the annual report of the corporate entity that the financial

statements that have been prepared have been properly constructed and maintained in

accordance to the section 286 under the Corporations Act 2001.

The financial statements the particular accounting notes also comply with the mentioned

accounting standards. This means that the management of the firm has asserted the

particular value that the financial statements have been prepared to reflect a proper true

and fair view of the accounting statements of the corporate entity (Wang et al. 2017).

Lastly, the directors of the corporate entity have reported in the financial report of the

corporate entity that the financial statements have been prepared in accordance to the

AUDIT PROGRAM

Financial reporting practices

The financial reporting practices that have been included in the accounting statements of

the corporate entity refer to the fact that the accounting statements or the books of accounts have

been prepared on the basis of the International Financial Reporting Standards. This means that

the books that have been prepared by the accounting body, are based upon the accounting

guidelines, that are issued by the accounting regulatory body of International Accounting

Standards Board. These accounting standards are known as the International Financial Reporting

Standards. Furthermore, the declarations or the assertions that have been included in the financial

report of the corporate entity can be listed down as follows:

The compliance with the accounting standards, which has been included in the basis of

preparation of the financial statements, has been stated accounting statements the

International Financial Reporting Standards.

The accounting statements that have been included tend to give a fair and true image of

the accounting statements of the corporate entity.

It has been further mentioned in the annual report of the corporate entity that the financial

statements that have been prepared have been properly constructed and maintained in

accordance to the section 286 under the Corporations Act 2001.

The financial statements the particular accounting notes also comply with the mentioned

accounting standards. This means that the management of the firm has asserted the

particular value that the financial statements have been prepared to reflect a proper true

and fair view of the accounting statements of the corporate entity (Wang et al. 2017).

Lastly, the directors of the corporate entity have reported in the financial report of the

corporate entity that the financial statements have been prepared in accordance to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT PROGRAM

accounting standards. Moreover, the financial position of the firm has been such that

there are reasonable grounds to make the corporate entity believe that the company will

be able to make the required payment of the debts of the company at the point when it

becomes due in nature and has to be paid immediately.

The issue that has been presented in the question refers to the fact that the financial

performance of the firm has been asked to be analyzed for the purpose of the fact that the

investors and the other stakeholders of the firm can determine the investment or the

economic decisions in regards to the investment in the selected corporate entity. This means

that the particular financial tool that can be utilized for the purpose of determining the

financial performance of the firm (Worthington and Pardy 2015). This means that the

significant ratios that have been utilized for the purpose of determining the financial

performance of the firm can be listed down as follows:

Asset turnover ratio

Return on equity ratio

Current ratio

Gross Operating margin

The asset turnover ratio refers to the particular ratio that results in the identification of the

result whether the optimum amount of returns from the assets of the firm has been acquired by

the corporate entity of the firm. The higher the amount of the asset turnover ratio more is the

ability of the firm to acquire the optimum amount of returns from the financial assets of the firm.

The return on equity ratio refers to the ability of the firm to secure optimum amount of

returns by utilizing the amount of equity that has been contributed by the stakeholders of the

AUDIT PROGRAM

accounting standards. Moreover, the financial position of the firm has been such that

there are reasonable grounds to make the corporate entity believe that the company will

be able to make the required payment of the debts of the company at the point when it

becomes due in nature and has to be paid immediately.

The issue that has been presented in the question refers to the fact that the financial

performance of the firm has been asked to be analyzed for the purpose of the fact that the

investors and the other stakeholders of the firm can determine the investment or the

economic decisions in regards to the investment in the selected corporate entity. This means

that the particular financial tool that can be utilized for the purpose of determining the

financial performance of the firm (Worthington and Pardy 2015). This means that the

significant ratios that have been utilized for the purpose of determining the financial

performance of the firm can be listed down as follows:

Asset turnover ratio

Return on equity ratio

Current ratio

Gross Operating margin

The asset turnover ratio refers to the particular ratio that results in the identification of the

result whether the optimum amount of returns from the assets of the firm has been acquired by

the corporate entity of the firm. The higher the amount of the asset turnover ratio more is the

ability of the firm to acquire the optimum amount of returns from the financial assets of the firm.

The return on equity ratio refers to the ability of the firm to secure optimum amount of

returns by utilizing the amount of equity that has been contributed by the stakeholders of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT PROGRAM

firm. The higher the amount of the return on equity ratio more is the ability of the firm to acquire

the optimum amount of returns from the equity capital of the firm (Thompson et al. 2015).

The current ratio refers to the liquidity position of the firm. This means that the current

ratio refers to the ability of the current assets of the firm to make the payment for the current

liabilities of the firm. It must be noted here that more the amount of the current more improved

will be the liquidity position of the firm.

The gross operating margin on the other hand refers to the returns that have been secured

from the operating profit of the firm. This means that higher the operating profit of the firm

higher will be the value of the ratio that has been obtained from the operating margin of the firm

(Kurmis et al. 2015).

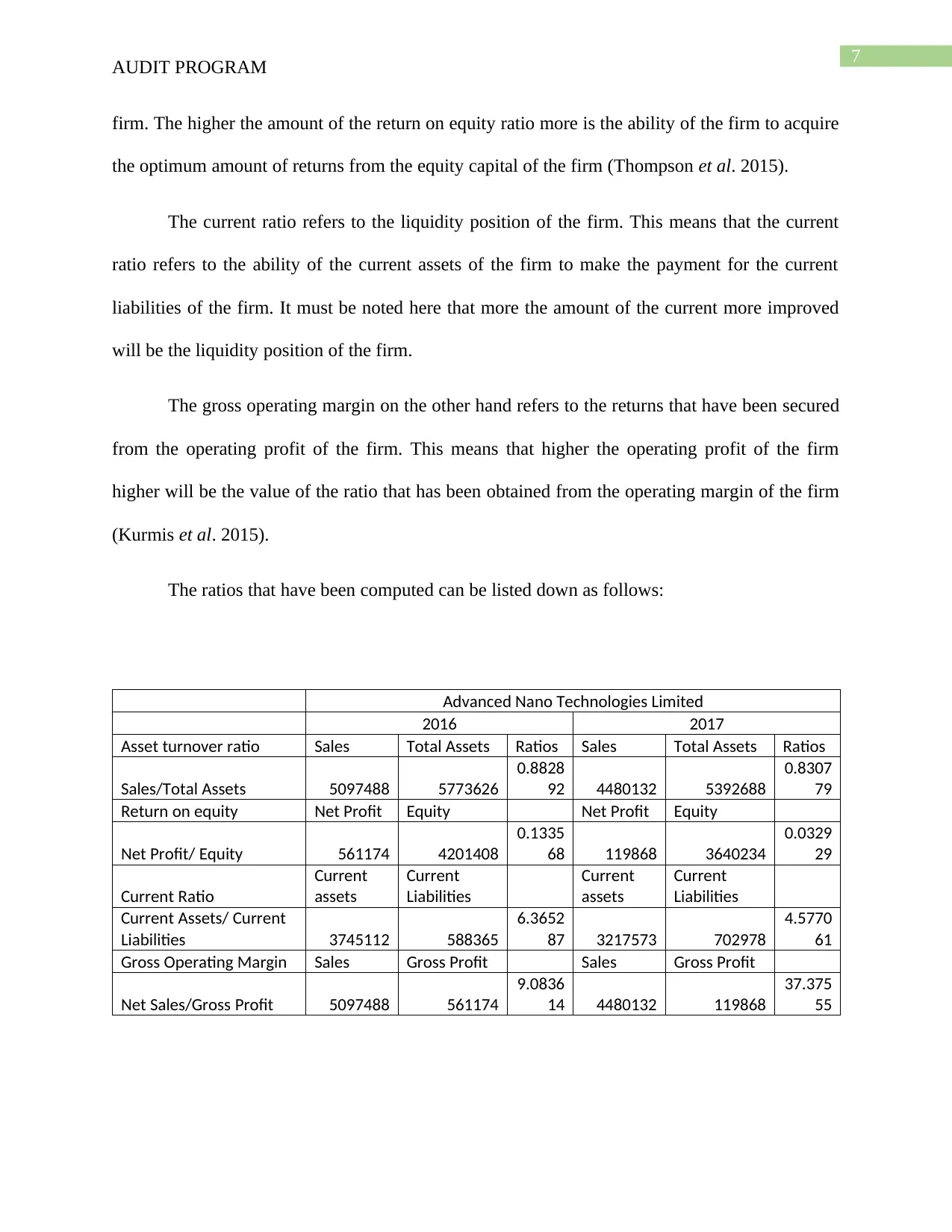

The ratios that have been computed can be listed down as follows:

Advanced Nano Technologies Limited

2016 2017

Asset turnover ratio Sales Total Assets Ratios Sales Total Assets Ratios

Sales/Total Assets 5097488 5773626

0.8828

92 4480132 5392688

0.8307

79

Return on equity Net Profit Equity Net Profit Equity

Net Profit/ Equity 561174 4201408

0.1335

68 119868 3640234

0.0329

29

Current Ratio

Current

assets

Current

Liabilities

Current

assets

Current

Liabilities

Current Assets/ Current

Liabilities 3745112 588365

6.3652

87 3217573 702978

4.5770

61

Gross Operating Margin Sales Gross Profit Sales Gross Profit

Net Sales/Gross Profit 5097488 561174

9.0836

14 4480132 119868

37.375

55

AUDIT PROGRAM

firm. The higher the amount of the return on equity ratio more is the ability of the firm to acquire

the optimum amount of returns from the equity capital of the firm (Thompson et al. 2015).

The current ratio refers to the liquidity position of the firm. This means that the current

ratio refers to the ability of the current assets of the firm to make the payment for the current

liabilities of the firm. It must be noted here that more the amount of the current more improved

will be the liquidity position of the firm.

The gross operating margin on the other hand refers to the returns that have been secured

from the operating profit of the firm. This means that higher the operating profit of the firm

higher will be the value of the ratio that has been obtained from the operating margin of the firm

(Kurmis et al. 2015).

The ratios that have been computed can be listed down as follows:

Advanced Nano Technologies Limited

2016 2017

Asset turnover ratio Sales Total Assets Ratios Sales Total Assets Ratios

Sales/Total Assets 5097488 5773626

0.8828

92 4480132 5392688

0.8307

79

Return on equity Net Profit Equity Net Profit Equity

Net Profit/ Equity 561174 4201408

0.1335

68 119868 3640234

0.0329

29

Current Ratio

Current

assets

Current

Liabilities

Current

assets

Current

Liabilities

Current Assets/ Current

Liabilities 3745112 588365

6.3652

87 3217573 702978

4.5770

61

Gross Operating Margin Sales Gross Profit Sales Gross Profit

Net Sales/Gross Profit 5097488 561174

9.0836

14 4480132 119868

37.375

55

8

AUDIT PROGRAM

The table that has been included above shows the financial performance of the selected

firm in terms of the ratios that have been computed on the basis of the financial components that

have been included in the financial statement of the corporate entity. This means that the asset

turnover ratio has decreased over the financial year of 2017 from the financial year of 2016. This

means that the firm has not been able to obtain the required amount of returns from the assets of

the company in comparison to the financial year of 2016 (Chintrakarn et al. 2017).

Next, the particular ratio that has been included refers to the return on equity ratio which

has fallen over the financial year of 2017 in comparison to the financial year of 2016. This means

that the management of the firm due to reasons like a high debt structure and other potential

issues has not been able to acquire the optimum amount of returns from the equity capital of the

corporate entity in regards to the financial year of 2016 (Rey‐Conde et al. 2016). This means that

the management of the business entity has not been able to secure the required returns from the

equity or the retained capital. The potential reasons might bad acquires or involvement in too

much debt that belongs to the third party investors.

The current ratio on the other hands clearly indicates the liquidity position of the firm.

This means that if the liquidity position of the firm is good then the health of the business entity

can be regarded as healthy. However, it must be noted here that the a firm having a too high

liquidity position refers to the fact that the liquid cash content of the firm is too high which again

reflects the fact that the financial structure of the firm is not strong enough. In case of the

selected firm, it can be noted that the liquidity position of the firm has fallen in regards to the

financial year of 2016. This means that the management of the firm has not been able to maintain

an optimum amount of current assets that will be required to substitute the current liabilities of

the firm (Heng et al. 2018). This means that the situation might have been such that the firm has

AUDIT PROGRAM

The table that has been included above shows the financial performance of the selected

firm in terms of the ratios that have been computed on the basis of the financial components that

have been included in the financial statement of the corporate entity. This means that the asset

turnover ratio has decreased over the financial year of 2017 from the financial year of 2016. This

means that the firm has not been able to obtain the required amount of returns from the assets of

the company in comparison to the financial year of 2016 (Chintrakarn et al. 2017).

Next, the particular ratio that has been included refers to the return on equity ratio which

has fallen over the financial year of 2017 in comparison to the financial year of 2016. This means

that the management of the firm due to reasons like a high debt structure and other potential

issues has not been able to acquire the optimum amount of returns from the equity capital of the

corporate entity in regards to the financial year of 2016 (Rey‐Conde et al. 2016). This means that

the management of the business entity has not been able to secure the required returns from the

equity or the retained capital. The potential reasons might bad acquires or involvement in too

much debt that belongs to the third party investors.

The current ratio on the other hands clearly indicates the liquidity position of the firm.

This means that if the liquidity position of the firm is good then the health of the business entity

can be regarded as healthy. However, it must be noted here that the a firm having a too high

liquidity position refers to the fact that the liquid cash content of the firm is too high which again

reflects the fact that the financial structure of the firm is not strong enough. In case of the

selected firm, it can be noted that the liquidity position of the firm has fallen in regards to the

financial year of 2016. This means that the management of the firm has not been able to maintain

an optimum amount of current assets that will be required to substitute the current liabilities of

the firm (Heng et al. 2018). This means that the situation might have been such that the firm has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT PROGRAM

to sell or give up certain current assets of the firm for the purpose of meeting up to certain debts.

This has reduced the ability of the firms to make the payment for the current liabilities that have

been acquired by the firm in the current financial year of 2017 in comparison to the financial

year of 2016.

The gross operating margin reflects the fact that the ratio has increased over the financial

year of 2017 in comparison to the financial year of 2016. This means that the management of the

firm has been able to make certain that the profitability of the firm increases from the financial

year of 2016 to the financial year of 2017 (Wilkinson et al. 2015).

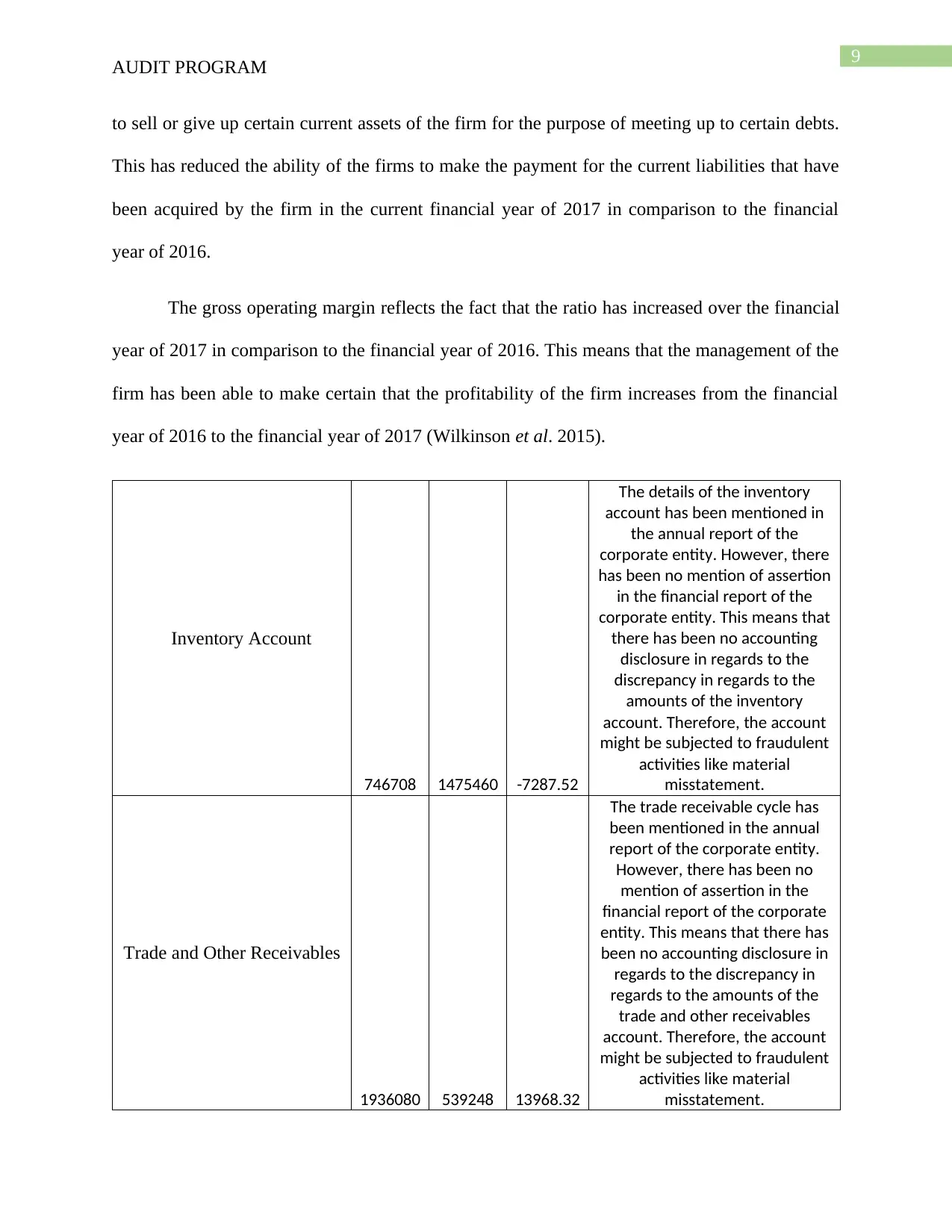

Inventory Account

746708 1475460 -7287.52

The details of the inventory

account has been mentioned in

the annual report of the

corporate entity. However, there

has been no mention of assertion

in the financial report of the

corporate entity. This means that

there has been no accounting

disclosure in regards to the

discrepancy in regards to the

amounts of the inventory

account. Therefore, the account

might be subjected to fraudulent

activities like material

misstatement.

Trade and Other Receivables

1936080 539248 13968.32

The trade receivable cycle has

been mentioned in the annual

report of the corporate entity.

However, there has been no

mention of assertion in the

financial report of the corporate

entity. This means that there has

been no accounting disclosure in

regards to the discrepancy in

regards to the amounts of the

trade and other receivables

account. Therefore, the account

might be subjected to fraudulent

activities like material

misstatement.

AUDIT PROGRAM

to sell or give up certain current assets of the firm for the purpose of meeting up to certain debts.

This has reduced the ability of the firms to make the payment for the current liabilities that have

been acquired by the firm in the current financial year of 2017 in comparison to the financial

year of 2016.

The gross operating margin reflects the fact that the ratio has increased over the financial

year of 2017 in comparison to the financial year of 2016. This means that the management of the

firm has been able to make certain that the profitability of the firm increases from the financial

year of 2016 to the financial year of 2017 (Wilkinson et al. 2015).

Inventory Account

746708 1475460 -7287.52

The details of the inventory

account has been mentioned in

the annual report of the

corporate entity. However, there

has been no mention of assertion

in the financial report of the

corporate entity. This means that

there has been no accounting

disclosure in regards to the

discrepancy in regards to the

amounts of the inventory

account. Therefore, the account

might be subjected to fraudulent

activities like material

misstatement.

Trade and Other Receivables

1936080 539248 13968.32

The trade receivable cycle has

been mentioned in the annual

report of the corporate entity.

However, there has been no

mention of assertion in the

financial report of the corporate

entity. This means that there has

been no accounting disclosure in

regards to the discrepancy in

regards to the amounts of the

trade and other receivables

account. Therefore, the account

might be subjected to fraudulent

activities like material

misstatement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT PROGRAM

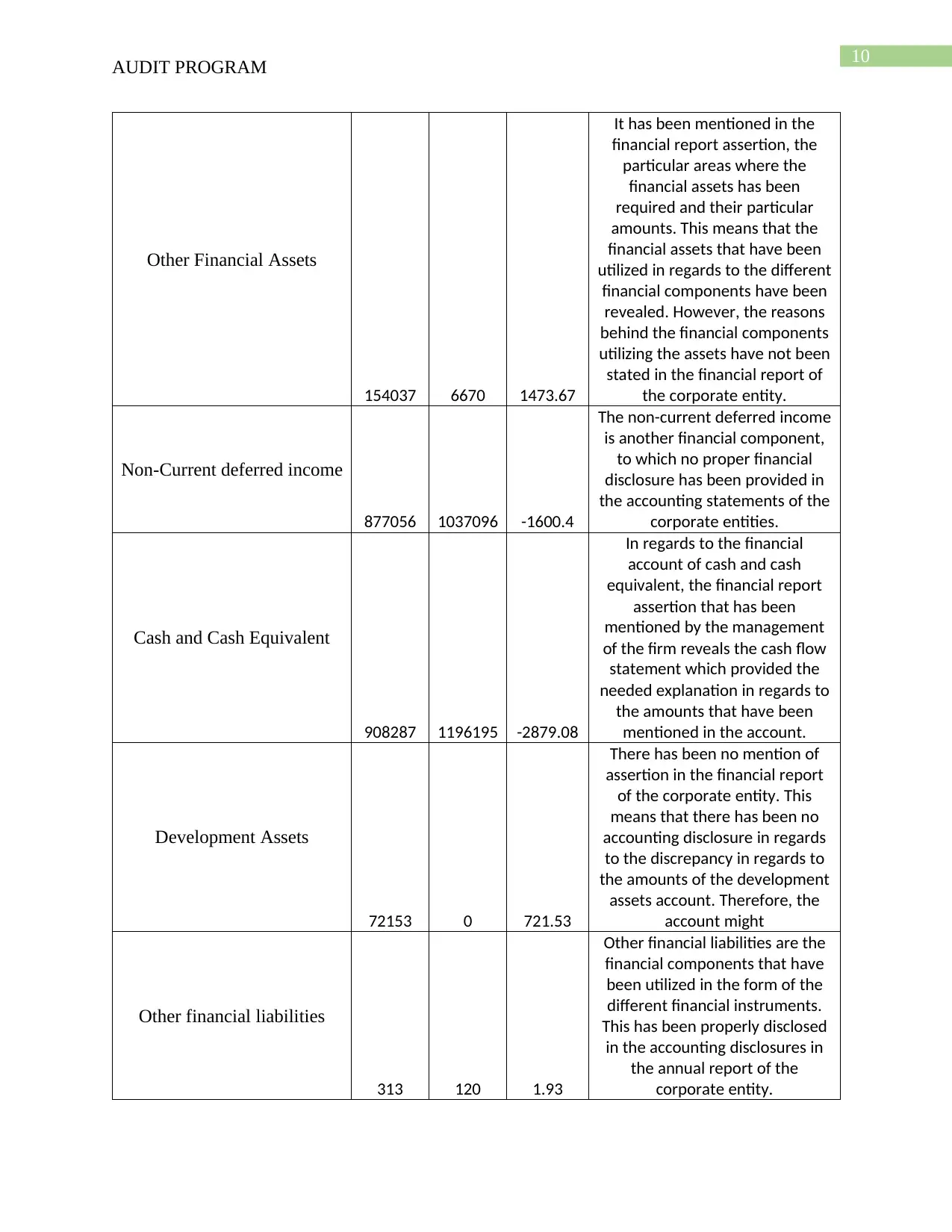

Other Financial Assets

154037 6670 1473.67

It has been mentioned in the

financial report assertion, the

particular areas where the

financial assets has been

required and their particular

amounts. This means that the

financial assets that have been

utilized in regards to the different

financial components have been

revealed. However, the reasons

behind the financial components

utilizing the assets have not been

stated in the financial report of

the corporate entity.

Non-Current deferred income

877056 1037096 -1600.4

The non-current deferred income

is another financial component,

to which no proper financial

disclosure has been provided in

the accounting statements of the

corporate entities.

Cash and Cash Equivalent

908287 1196195 -2879.08

In regards to the financial

account of cash and cash

equivalent, the financial report

assertion that has been

mentioned by the management

of the firm reveals the cash flow

statement which provided the

needed explanation in regards to

the amounts that have been

mentioned in the account.

Development Assets

72153 0 721.53

There has been no mention of

assertion in the financial report

of the corporate entity. This

means that there has been no

accounting disclosure in regards

to the discrepancy in regards to

the amounts of the development

assets account. Therefore, the

account might

Other financial liabilities

313 120 1.93

Other financial liabilities are the

financial components that have

been utilized in the form of the

different financial instruments.

This has been properly disclosed

in the accounting disclosures in

the annual report of the

corporate entity.

AUDIT PROGRAM

Other Financial Assets

154037 6670 1473.67

It has been mentioned in the

financial report assertion, the

particular areas where the

financial assets has been

required and their particular

amounts. This means that the

financial assets that have been

utilized in regards to the different

financial components have been

revealed. However, the reasons

behind the financial components

utilizing the assets have not been

stated in the financial report of

the corporate entity.

Non-Current deferred income

877056 1037096 -1600.4

The non-current deferred income

is another financial component,

to which no proper financial

disclosure has been provided in

the accounting statements of the

corporate entities.

Cash and Cash Equivalent

908287 1196195 -2879.08

In regards to the financial

account of cash and cash

equivalent, the financial report

assertion that has been

mentioned by the management

of the firm reveals the cash flow

statement which provided the

needed explanation in regards to

the amounts that have been

mentioned in the account.

Development Assets

72153 0 721.53

There has been no mention of

assertion in the financial report

of the corporate entity. This

means that there has been no

accounting disclosure in regards

to the discrepancy in regards to

the amounts of the development

assets account. Therefore, the

account might

Other financial liabilities

313 120 1.93

Other financial liabilities are the

financial components that have

been utilized in the form of the

different financial instruments.

This has been properly disclosed

in the accounting disclosures in

the annual report of the

corporate entity.

11

AUDIT PROGRAM

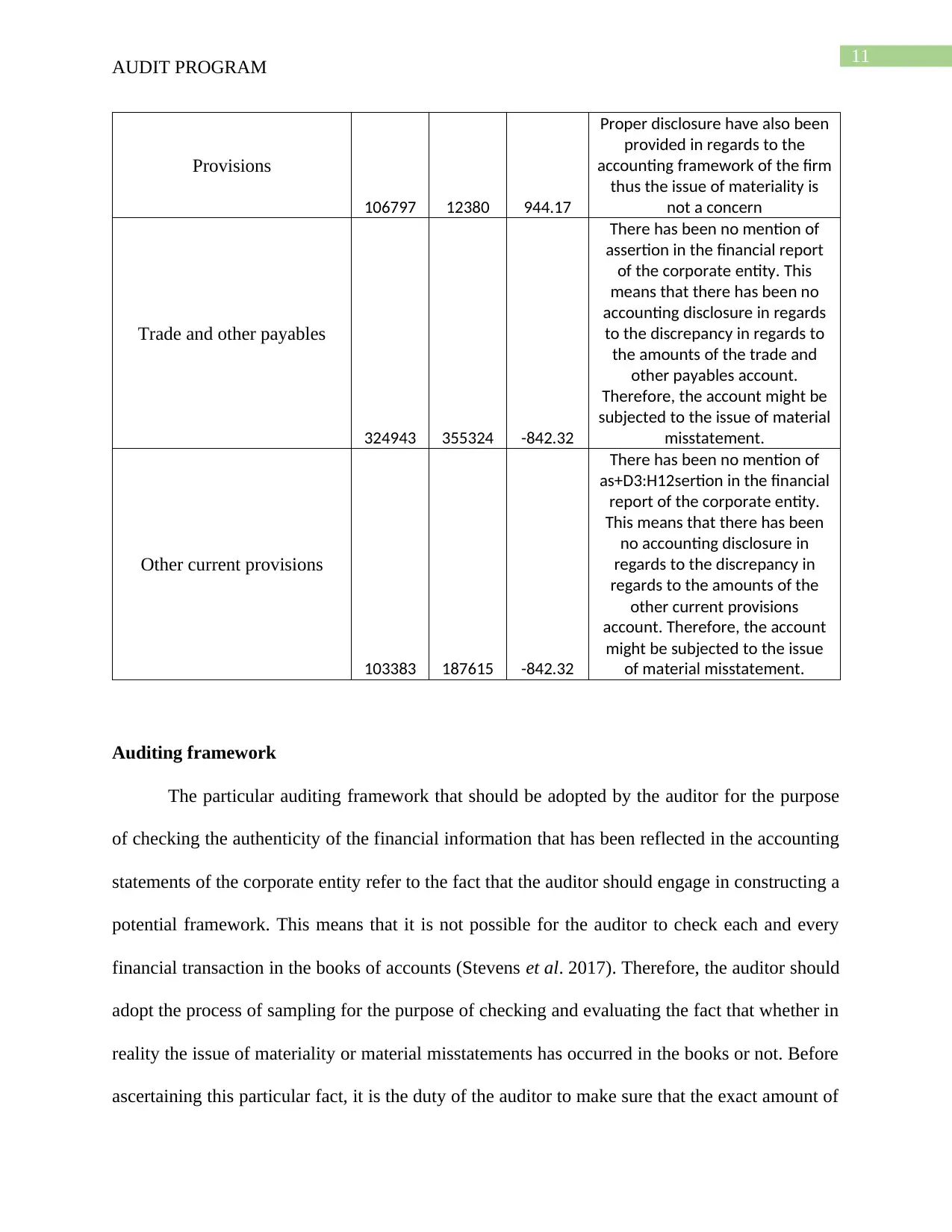

Provisions

106797 12380 944.17

Proper disclosure have also been

provided in regards to the

accounting framework of the firm

thus the issue of materiality is

not a concern

Trade and other payables

324943 355324 -842.32

There has been no mention of

assertion in the financial report

of the corporate entity. This

means that there has been no

accounting disclosure in regards

to the discrepancy in regards to

the amounts of the trade and

other payables account.

Therefore, the account might be

subjected to the issue of material

misstatement.

Other current provisions

103383 187615 -842.32

There has been no mention of

as+D3:H12sertion in the financial

report of the corporate entity.

This means that there has been

no accounting disclosure in

regards to the discrepancy in

regards to the amounts of the

other current provisions

account. Therefore, the account

might be subjected to the issue

of material misstatement.

Auditing framework

The particular auditing framework that should be adopted by the auditor for the purpose

of checking the authenticity of the financial information that has been reflected in the accounting

statements of the corporate entity refer to the fact that the auditor should engage in constructing a

potential framework. This means that it is not possible for the auditor to check each and every

financial transaction in the books of accounts (Stevens et al. 2017). Therefore, the auditor should

adopt the process of sampling for the purpose of checking and evaluating the fact that whether in

reality the issue of materiality or material misstatements has occurred in the books or not. Before

ascertaining this particular fact, it is the duty of the auditor to make sure that the exact amount of

AUDIT PROGRAM

Provisions

106797 12380 944.17

Proper disclosure have also been

provided in regards to the

accounting framework of the firm

thus the issue of materiality is

not a concern

Trade and other payables

324943 355324 -842.32

There has been no mention of

assertion in the financial report

of the corporate entity. This

means that there has been no

accounting disclosure in regards

to the discrepancy in regards to

the amounts of the trade and

other payables account.

Therefore, the account might be

subjected to the issue of material

misstatement.

Other current provisions

103383 187615 -842.32

There has been no mention of

as+D3:H12sertion in the financial

report of the corporate entity.

This means that there has been

no accounting disclosure in

regards to the discrepancy in

regards to the amounts of the

other current provisions

account. Therefore, the account

might be subjected to the issue

of material misstatement.

Auditing framework

The particular auditing framework that should be adopted by the auditor for the purpose

of checking the authenticity of the financial information that has been reflected in the accounting

statements of the corporate entity refer to the fact that the auditor should engage in constructing a

potential framework. This means that it is not possible for the auditor to check each and every

financial transaction in the books of accounts (Stevens et al. 2017). Therefore, the auditor should

adopt the process of sampling for the purpose of checking and evaluating the fact that whether in

reality the issue of materiality or material misstatements has occurred in the books or not. Before

ascertaining this particular fact, it is the duty of the auditor to make sure that the exact amount of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.